Pull up any generic business formation website and you’ll find a tidy comparison table that lists “pass-through taxation” under S Corp and “double taxation” under C Corp — and then stops there. What those tables don’t show you is that the difference between C Corp and S Corp chart looks very different when you add California’s franchise tax layer, the One Big Beautiful Bill Act’s updated deductions, and the actual dollar math on $150,000 to $500,000 in annual business income. Miss those nuances and you’re not just misunderstanding a chart — you’re signing up for tens of thousands in unnecessary taxes every year.

This information is current as of 3/12/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

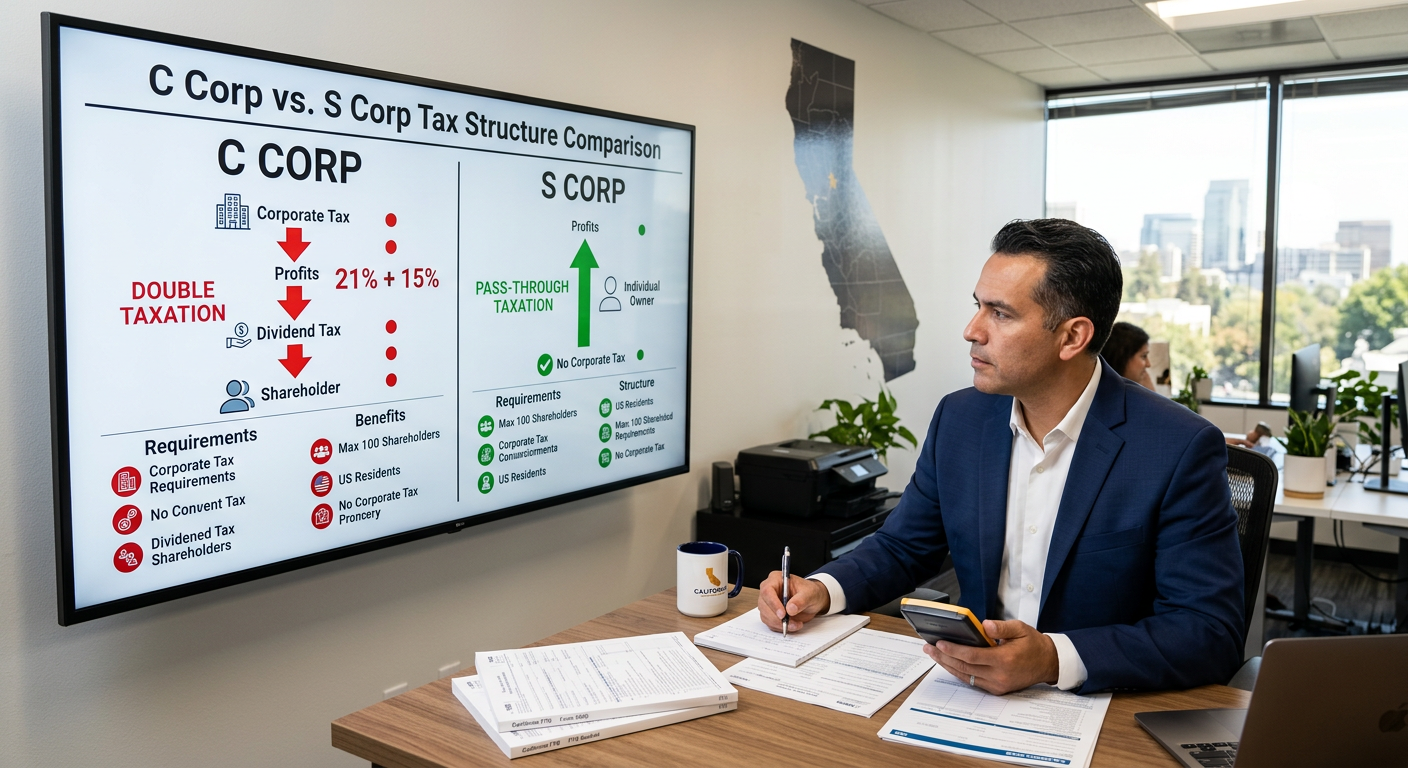

Quick Answer: What Does the C Corp vs S Corp Chart Actually Show?

At its core, the difference between a C Corp and an S Corp comes down to how the IRS taxes corporate profits. A C Corp pays tax at the entity level (currently 21% federal flat rate) and then shareholders pay tax again on dividends received — creating what tax professionals call “double taxation.” An S Corp passes all profits and losses directly to shareholders’ personal tax returns, meaning the company itself pays no federal income tax. That one structural difference can be worth $20,000 to $50,000 annually for a California business owner earning $200,000 or more.

But the chart gets much more complicated once California enters the picture. The state franchise tax rate for a C Corp is 8.84% — versus only 1.5% for an S Corp. That’s a 7.34 percentage point gap on every dollar of taxable business income, and most comparison charts don’t flag it.

The Full C Corp vs S Corp Tax Comparison Chart (California 2026)

Many business owners have seen abbreviated comparison tables. Here’s what the full chart looks like when you include federal tax, California state tax, self-employment tax impact, and 2026 deduction rules side by side.

| Factor | C Corp | S Corp |

|---|---|---|

| Federal Tax Rate | Flat 21% (entity level) | 0% at entity level; pass-through to owner |

| California Franchise Tax Rate | 8.84% on net income | 1.5% on net income (min. $800) |

| Double Taxation? | Yes — corporate + dividend tax | No — single layer of tax |

| Self-Employment Tax | Not applicable (no SE tax) | Only on W-2 salary (not distributions) |

| QBI Deduction (20%) | Not available to C Corps | Available on qualified business income |

| AB 150 PTE Election | Not eligible | Eligible — bypass $40,000 SALT cap |

| Shareholder Limit | Unlimited shareholders | 100 shareholders max |

| Foreign Shareholders? | Allowed | Not allowed |

| QSBS Exclusion (IRC §1202) | Eligible for up to 100% gain exclusion | Not eligible |

| Retained Earnings Reinvestment | Can retain at 21% federal rate | Taxed to owner even if not distributed |

| Ideal for Venture Funding? | Yes | No — investors typically require C Corp |

For a California business owner, the most important rows in that table are the franchise tax rates, the QBI deduction availability, and the AB 150 PTE election. Those three factors alone can shift the tax outcome by $25,000 to $45,000 annually at the $200,000–$400,000 profit range.

For a comprehensive breakdown of how California S Corp strategy works in practice, see our complete guide to S Corp tax strategy in California.

The Real Dollar Math: C Corp vs S Corp on $200,000 Business Profit

Charts tell part of the story. Numbers tell the rest. Here’s the actual tax math for a California business owner earning $200,000 in net profit under each structure in 2026.

C Corp Scenario

- $200,000 net profit

- Federal corporate tax at 21%: $42,000

- California franchise tax at 8.84%: $17,680

- After-tax corporate profit available for distribution: $140,320

- Federal dividend tax on distribution (qualified, 20% rate): $28,064

- California personal income tax on dividend (13.3% top rate): $18,663

- Total tax paid: $106,407 (53.2% effective rate)

S Corp Scenario

- $200,000 net profit

- Reasonable W-2 salary to owner: $80,000

- Distribution: $120,000

- Payroll taxes (FICA) on salary: $12,240

- California franchise tax at 1.5%: $3,000

- Federal income tax on $200,000 (after QBI deduction of $24,000): $39,520

- California income tax on $200,000: $17,600

- Total tax paid: $72,360 (36.2% effective rate)

Annual tax savings from S Corp election: $34,047

That’s not a projection or a best-case scenario. That’s the math. Want to see how those numbers shift at your specific profit level? Run your business income through this small business tax calculator to get a quick baseline before your strategy session.

KDA Case Study: Sacramento Consultant Switches from C Corp and Saves $36,800

Marcus is a 41-year-old management consultant based in Sacramento who incorporated as a C Corp in 2019 on the advice of a business attorney who said it would “look more professional” to clients. By 2025, his firm was generating $235,000 in annual net profit. He was paying close to $115,000 in combined federal, California, and dividend taxes annually — an effective rate north of 48%.

Marcus came to KDA after receiving a California FTB notice questioning his franchise tax calculation. During the intake review, our team identified that he had zero business reason to be a C Corp and was losing roughly $35,000 per year to unnecessary double taxation.

Here is what KDA did:

- Filed IRS Form 2553 to elect S Corp status effective January 1, 2026

- Filed California FTB Form 3560 simultaneously to recognize the California S Corp election

- Restructured his compensation to a $90,000 W-2 salary with $145,000 in annual distributions

- Applied the permanent 20% QBI deduction under the One Big Beautiful Bill Act to $145,000 of qualified business income

- Enrolled Marcus in the AB 150 PTE elective tax to bypass California’s $40,000 SALT cap

Year one results: Marcus’s combined tax obligation dropped from $113,400 to $76,600 — a savings of $36,800. KDA’s fee was $4,800. His first-year ROI was 7.7x.

The FTB notice that triggered the review? It was resolved during the restructuring with no penalty owed.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

What the Comparison Chart Misses: Five California-Specific Traps

Generic C Corp vs S Corp comparison charts are almost always built around federal tax law. California has its own rules, and several of them are expensive if you miss them. Our audit representation services regularly encounter clients who got tripped up by exactly these traps — often after relying on an out-of-state accountant or an online formation service.

Trap 1: The FTB Form 3560 Deadline

When a California LLC or C Corp elects S Corp status with the IRS using Form 2553, most business owners assume the federal election automatically applies to California. It does not. California requires a separate state-level S Corp election filed on FTB Form 3560. Miss the California deadline — which mirrors the federal 2.5-month window from the start of the tax year — and you’ll pay C Corp franchise tax rates (8.84%) in California even while enjoying S Corp treatment federally.

Trap 2: California Non-Conformity on Bonus Depreciation

California does not conform to federal bonus depreciation rules. If your C Corp or S Corp takes 40% federal bonus depreciation on new equipment under current OBBBA phase-down rules, California disallows that deduction entirely. You must maintain two separate depreciation schedules — one for your federal return, one for your California return. Business owners who skip this end up with FTB underpayment notices and interest charges that compound quickly.

Trap 3: The California S Corp Minimum Franchise Tax

S Corps in California are subject to a minimum franchise tax of $800 per year, even if the business has zero net income. New S Corps are exempt in their first year, but the exemption only applies once. Many multi-entity holders who form a new S Corp annually to capture the first-year exemption are playing with fire — the FTB has flagged this pattern as a compliance risk.

Trap 4: Built-In Gains Tax on C-to-S Conversion

When a C Corp converts to an S Corp, the IRS imposes a built-in gains (BIG) tax under IRC Section 1374 on any appreciated assets that existed at the time of conversion. This BIG tax applies for five years following the conversion date. California conforms to this rule. If you have real estate, equipment, or intellectual property inside your C Corp with significant unrealized gain, the conversion strategy requires careful timing — rushing it can generate a large BIG tax bill in the first few years.

Trap 5: The AB 150 PTE Election Is Not Automatic

California’s pass-through entity (PTE) elective tax under AB 150 allows S Corp owners to pay California income tax at the entity level and deduct it federally — effectively bypassing the $40,000 SALT deduction cap for 2026. But this election must be made annually, on time, and requires prepayment by June 15 of the tax year. If you miss the prepayment deadline, you lose the benefit entirely for that year. Many S Corp owners who could save $8,000 to $18,000 through the AB 150 election miss it simply because they didn’t know it existed or assumed it was handled automatically.

Why Most Business Owners Choose the Wrong Entity From the Start

The single biggest driver of costly entity mistakes is formation timing. Most business owners choose their entity structure at the moment they start a business — when their annual revenue is zero. An attorney or online formation service recommends a C Corp because it sounds serious and scalable. By the time the business is generating real income, the owner has been operating as a C Corp for three to five years, has built-in gains in the entity, and faces a complex conversion process to get to the right structure.

The better framework is to evaluate your entity structure at every revenue milestone:

- Under $40,000 net profit: Single-member LLC or sole proprietor. The overhead of S Corp payroll doesn’t pay off yet.

- $40,000 to $80,000 net profit: S Corp election starts making sense. Self-employment tax savings begin to outweigh administrative costs.

- $80,000 to $500,000 net profit: S Corp is almost always the right answer for California business owners without VC funding or QSBS aspirations. The tax savings are substantial and ongoing.

- Above $500,000 with investor interest or international shareholders: C Corp with QSBS planning may become worth revisiting. The Qualified Small Business Stock exclusion under IRC Section 1202 can eliminate up to 100% of capital gains at exit — but requires C Corp status.

Key Takeaway: The “right” entity is not a static choice. It’s a revenue-dependent decision that should be reviewed every one to two years as your business grows.

The QBI Deduction: The Column Most Comparison Charts Leave Blank for C Corps

One of the most consequential rows in the difference between C Corp and S Corp chart is the Qualified Business Income (QBI) deduction — and it’s the column most general comparison charts leave incomplete.

Under the One Big Beautiful Bill Act (OBBBA), the 20% QBI deduction for pass-through businesses has been made permanent. This means S Corp owners can deduct 20% of their qualified business income before calculating their federal income tax. On $150,000 in qualifying S Corp distributions, that’s a $30,000 deduction off the top — worth approximately $6,600 to $9,900 in actual federal tax savings depending on your bracket.

C Corps are categorically ineligible for the QBI deduction. It is a pass-through benefit only. When you see a comparison chart that lists “QBI deduction: Yes/No,” this is what it means in real money: a $30,000 deduction that C Corp owners simply cannot access.

Does the QBI Deduction Have Limits?

Yes. The deduction phases out at higher income levels for specified service trades or businesses (SSTBs) — which include law, consulting, financial services, and accounting. For 2026, the phase-out begins at $197,300 for single filers and $394,600 for married filing jointly under updated OBBBA thresholds. If you’re a California consultant earning above those thresholds, strategic income deferral or entity restructuring may be required to preserve the QBI benefit. This is exactly the kind of planning that should happen before year-end, not at tax time.

Common Mistake: Assuming the IRS Will Tell You When to Switch

The IRS will not send you a letter telling you that you’ve outgrown your C Corp. The FTB will not flag your franchise tax overpayments and suggest you restructure. The entire burden of identifying the more tax-efficient structure falls on you — or your tax team.

This is one of the most expensive passive mistakes in California business taxation. A C Corp owner generating $250,000 in annual profit who stays in that structure for five years — when an S Corp would have been appropriate after year two — could lose $150,000 to $175,000 in cumulative unnecessary taxes. Not from anything they did wrong. Simply from not reviewing their entity structure at the right time.

Red Flag Alert: If you formed a C Corp more than 18 months ago and your business profit now exceeds $80,000 per year, you have almost certainly overpaid California franchise tax. A single entity review session can quantify that exposure and determine whether a retroactive S Corp election (the IRS does allow late elections under Revenue Procedure 2013-30 in many cases) is available.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About the C Corp vs S Corp Comparison

Can I switch from a C Corp to an S Corp at any time?

You can file IRS Form 2553 to elect S Corp status at any time, but the election is generally only effective for the current tax year if filed within 2.5 months of the start of that year. Late elections are available under Revenue Procedure 2013-30 if you can show reasonable cause. California requires the same timing via FTB Form 3560. Miss the California deadline and you’ll pay C Corp rates in California for the full year.

Does the difference between C Corp and S Corp chart change if I have a partner?

Yes. S Corps are limited to 100 shareholders and all shareholders must be U.S. citizens or residents. If you have an international partner or investor, S Corp status may be unavailable. Multi-owner structures may also consider an LLC taxed as a partnership, which has different QBI and SE tax implications than both C Corp and S Corp structures.

Is an S Corp always better than a C Corp in California?

For most profitable California businesses without venture capital requirements or international shareholders, yes. The franchise tax rate differential (8.84% vs 1.5%) and the QBI deduction unavailability make C Corp status expensive to maintain at typical small-to-mid-market income levels. The exceptions are businesses planning for a QSBS-eligible exit, businesses with significant retained earnings they plan to reinvest at the corporate level, or businesses actively seeking institutional investors who require C Corp structure.

Will switching from C Corp to S Corp trigger an audit?

A properly filed entity election does not trigger an audit on its own. The IRS and FTB review the forms as part of standard processing. However, if the conversion involves appreciated assets and no BIG tax is reported on Form 1120-S Schedule D in the years following conversion, that can attract scrutiny. This is why the built-in gains analysis matters — and why it should be documented before the election is filed.

Book Your Entity Strategy Session Before You File Another Year at the Wrong Rate

If you’ve been operating as a C Corp and your annual profit is above $80,000, the numbers in this article apply directly to your situation. Every year you stay in the wrong structure is a year you’re leaving $20,000 to $40,000 on the table — not because of anything complicated, but because no one ran the comparison on your actual numbers.

Our team at KDA works specifically with California business owners who want to stop overpaying and start keeping more of what they earn. We’ll review your current entity structure, run the actual tax math for your income level, evaluate your AB 150 PTE election eligibility, and map out the most efficient conversion path if restructuring makes sense.

Click here to book your entity strategy consultation now. Come in as a C Corp. Leave with a plan that could save you $30,000 or more every year going forward.