Here’s the mistake California business owners keep making: they incorporate as a C Corp or stay in their default entity structure, pay their accountant to file the return, and assume everything is handled. What they don’t realize is that the way C Corp S Corp taxation works in California creates one of the most avoidable tax gaps in the entire U.S. tax code — and it’s costing the average California business owner between $20,000 and $50,000 every single year.

This isn’t theoretical. The numbers are real, the IRS rules are clear, and the fix is available to most business owners right now. The only thing standing between you and a dramatically lower tax bill is understanding exactly how these two structures differ — and which one your business should be using.

This information is current as of 3/12/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Quick Answer: How Does C Corp vs S Corp Taxation Actually Work?

C Corp taxation operates on a double-taxation model. The corporation pays federal income tax at 21% on its profits. Then, when those profits are distributed to shareholders as dividends, the shareholders pay personal income tax again — up to 20% federally plus California’s top rate of 13.3%. In practice, you can end up paying an effective combined rate north of 46% on the same dollar of income.

S Corp taxation eliminates the corporate-level tax entirely. Profits “pass through” directly to the owners’ personal tax returns, where they’re taxed only once. Better yet, only the owner’s salary portion is subject to self-employment taxes — distributions are not. For a business generating $200,000 in profit, that distinction alone can save $14,000 to $20,000 annually.

California adds another layer. C Corps pay an 8.84% state franchise tax on net income. S Corps pay just 1.5%. On $200,000 in profit, that’s a $14,680 difference before you even account for federal tax savings.

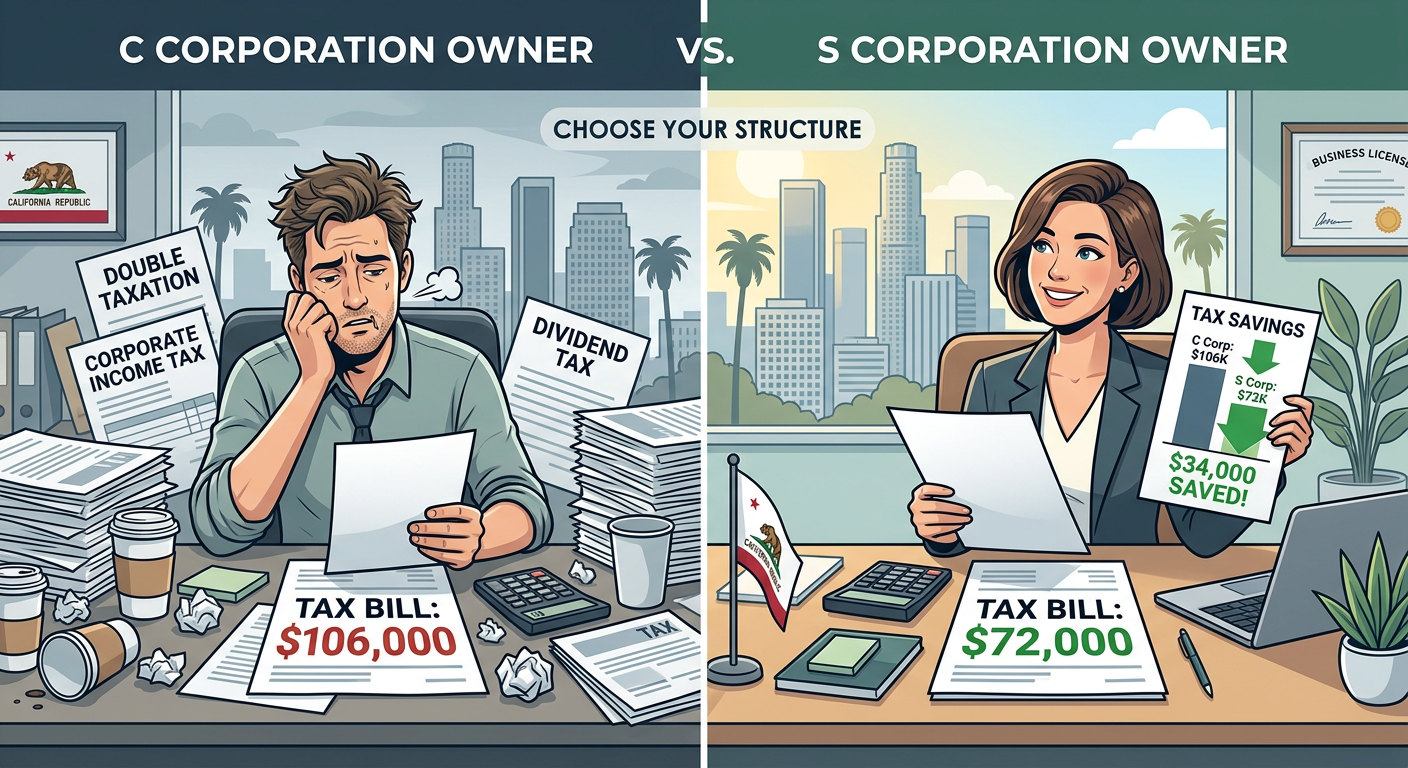

The Real Math: What C Corp S Corp Taxation Costs You in California

Let’s run the actual numbers for a California business generating $200,000 in net profit, so this stops being abstract and starts being a decision.

As a C Corp (Default for Most “Inc.” Entities)

- Federal corporate income tax at 21%: $42,000

- California franchise tax at 8.84%: $17,680

- Remaining after-tax profit: $140,320

- Federal dividend tax on distribution (qualified, 15%): $21,048

- California personal income tax on dividend (~9.3%): $13,050

- Total tax burden: approximately $93,778

- Effective combined rate: ~46.9%

As an S Corp (With Reasonable Salary of $85,000)

- Payroll taxes on $85,000 salary (employer + employee share): ~$13,005

- Federal income tax on $115,000 pass-through at 22%: $25,300

- California personal income tax on $200,000 total income at ~9.3%: $18,600

- California S Corp franchise tax at 1.5%: $3,000

- Total tax burden: approximately $59,905

- Effective combined rate: ~29.9%

The difference: $33,873 saved annually by structuring as an S Corp instead of a C Corp. Over five years, that’s $169,365 — enough to fund a retirement account, buy investment property, or simply keep in your pocket where it belongs.

Want to see exactly how your business profit lands under both structures? Plug your numbers into this small business tax calculator to get a clear picture before your next filing.

For a comprehensive breakdown of every S Corp strategy available to California business owners, see our complete guide to S Corp tax strategy in California.

KDA Case Study: Sacramento Consultant Saves $31,200 in Year One

A Sacramento-based management consultant came to KDA in early 2025. She had been operating as a single-member LLC taxed as a C Corp — a structure her original attorney set up when she launched the business five years earlier. Her gross revenue was $285,000, and her net profit after expenses was $210,000. She was paying roughly $87,000 in combined federal and California taxes annually and assumed that was simply “the cost of doing business.”

KDA ran a full entity analysis. The diagnosis was straightforward: her C Corp structure was generating a double-taxation penalty of over $30,000 per year. We filed IRS Form 2553 (the S Corp election form) and California FTB Form 3560 simultaneously, establishing her as an S Corp effective January 1, 2025. We set her reasonable salary at $92,000 — well-supported by Bureau of Labor Statistics data for her industry — and structured the remainder of her income as S Corp distributions.

The results in year one:

- Self-employment tax savings on $118,000 in distributions: $16,650

- California franchise tax reduction (8.84% to 1.5%): $7,770

- Federal QBI deduction on pass-through income (20%): $6,780

- Total first-year tax savings: $31,200

- KDA engagement fee: $4,500

- First-year ROI: 6.9x

She now runs payroll through QuickBooks, files a clean Form 1120-S each year, and puts the difference into a SEP-IRA — which creates an additional $16,500 in annual deductions on top of the entity savings.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

The Five C Corp S Corp Taxation Traps California Business Owners Fall Into

Understanding the math is one thing. Avoiding the mistakes that erase those savings is another. These are the five traps that cost California business owners the most money when navigating C Corp and S Corp taxation.

Trap 1: Missing the S Corp Election Deadline

To elect S Corp status for a given tax year, you must file IRS Form 2553 within 75 days of the start of that tax year — or within 75 days of formation for a new entity. For existing businesses wanting S Corp status effective January 1, 2026, the filing deadline was March 15, 2026. Miss that window and you’re locked into your current tax treatment for the entire year.

There is a late election relief provision under IRS Revenue Procedure 2013-30, but it requires showing “reasonable cause” for the failure. Don’t count on it as a fallback plan.

Trap 2: Ignoring California’s FTB Form 3560

Filing IRS Form 2553 at the federal level is not enough in California. The FTB requires a separate S Corp election on FTB Form 3560. Skip this step and the IRS will treat you as an S Corp while California continues taxing you as a C Corp at 8.84%. This is one of the most expensive state-federal mismatches in the California tax code, and it happens more often than you’d expect — even with otherwise competent tax preparers.

Trap 3: Setting an Unreasonably Low Salary

The entire S Corp tax savings strategy hinges on splitting income between a “reasonable salary” (subject to payroll taxes) and distributions (not subject to payroll taxes). The IRS requires that the salary be reasonable for the work performed. If you pay yourself $30,000 and take $170,000 in distributions on $200,000 in profit, expect scrutiny. The IRS has won multiple tax court cases on this issue. Use Bureau of Labor Statistics data for your industry and document your compensation analysis.

Trap 4: Overlooking the Built-In Gains Tax on C Corp Conversion

When a C Corp converts to S Corp status, any built-in gains (the appreciation in the C Corp’s assets at the time of conversion) remain subject to the built-in gains (BIG) tax under IRC Section 1374 for five years post-conversion. If you sell appreciated assets within that five-year recognition period, you’ll owe a 21% corporate-level tax on those gains as if you were still a C Corp. Plan your asset sales accordingly.

Trap 5: Assuming S Corp Is Always Better

S Corp taxation outperforms C Corp taxation for most California small business owners — but not all. C Corp structure makes more sense if you’re planning to raise venture capital (most VC firms require C Corp structure), pursuing QSBS exclusion under IRC Section 1202 (which exempts up to $10 million in capital gains), retaining large amounts of capital inside the business for reinvestment, or anticipating a high-value acquisition where deal structure favors C Corp. For many business owners building toward an exit, the answer is more nuanced than a simple tax rate comparison.

The QBI Deduction: The S Corp Advantage Most Owners Don’t Know About

Under the One Big Beautiful Bill Act (OBBBA), the Section 199A Qualified Business Income (QBI) deduction is now permanent. This deduction allows S Corp owners to deduct up to 20% of their qualified business income from their taxable income — permanently reducing federal tax liability without requiring additional spending or investment.

On $115,000 in S Corp pass-through income (after the reasonable salary), the 20% QBI deduction creates a $23,000 deduction. At a 22% federal rate, that’s $5,060 in direct tax savings. C Corp owners get zero access to this deduction — it applies exclusively to pass-through income from sole proprietorships, partnerships, LLCs, and S Corps.

The income thresholds for 2025 are $197,300 for single filers and $394,600 for married filing jointly. Above those thresholds, some service businesses face phase-outs. Work with a strategist who understands the Section 199A rules to confirm your eligibility and maximize the deduction before year-end.

California’s AB 150 PTE Election: The SALT Cap Workaround Most S Corp Owners Miss

The federal SALT deduction cap — now raised to $40,000 under the OBBBA — still limits how much state tax California business owners can deduct on their federal return. California’s AB 150 Pass-Through Entity (PTE) elective tax is the state-authorized workaround.

Here’s how it works: S Corps and partnerships can elect to pay California income tax at the entity level (at a 9.3% rate) rather than passing the entire tax burden to the owner’s personal return. The entity-level payment is fully deductible as a business expense on the federal return — completely bypassing the SALT cap. The owners then receive a dollar-for-dollar credit on their California personal return.

For a California S Corp owner paying $18,000 in state income tax, the PTE election converts that payment from a capped, limited personal deduction into a full federal business deduction — saving an additional $3,960 in federal taxes (at a 22% rate). You must opt in annually by June 15 of the tax year. Missing the deadline means losing the benefit for that entire year.

Our tax planning services include AB 150 PTE election analysis and implementation as part of every California entity engagement — because missing this one deadline can cost thousands.

How to Execute the S Corp Election: A Step-by-Step Guide

If you’ve determined that S Corp taxation is the right structure for your California business, here is the exact process to make it happen for the 2026 tax year (or retroactively with late relief).

Step 1: Confirm Eligibility

Your entity must be a domestic corporation or LLC that has elected to be taxed as a corporation. S Corp eligibility requirements under IRS guidelines include: no more than 100 shareholders, all shareholders must be U.S. citizens or resident aliens, only one class of stock is permitted, and partnerships, corporations, and most trusts cannot be shareholders.

Step 2: File IRS Form 2553

Download the current version of Form 2553 from IRS.gov. Complete Section I with your business name, EIN, and address exactly as they appear on your incorporation documents. List all shareholders and their consent signatures in Section I, Column K. File by certified mail with return receipt or electronically through your tax preparer. The IRS will issue a CP261 notice confirming the election — keep this document permanently in your corporate records.

Step 3: File California FTB Form 3560

File FTB Form 3560 to notify the California Franchise Tax Board of your S Corp election. This must be filed within the same timeframe as the federal election. Failure to file means California will continue treating your entity as a C Corp regardless of your federal S Corp status.

Step 4: Establish Payroll

Once your S Corp election is confirmed, set up a payroll system to pay yourself a reasonable salary. Register with the California Employment Development Department (EDD) for state payroll tax purposes. Use a payroll platform that handles federal and California withholding, employer matching, and W-2 generation. Your salary should be documented with a compensation analysis referencing comparable market rates.

Step 5: Set Up a Separate Business Bank Account and Bookkeeping

S Corp distributions must be tracked separately from salary payments. Maintain clean books showing salary payments, employer payroll tax remittances, and distribution payments. Commingling salary and distributions is a red flag in an IRS audit and weakens your reasonable compensation argument.

What If I’m Already a C Corp — Is It Too Late to Switch?

No — but timing and planning matter. Converting from a C Corp to an S Corp mid-business-lifecycle is entirely doable, and KDA has guided dozens of California businesses through this process. The key considerations are the five-year built-in gains window (see Trap 4 above), any accumulated earnings and profits from C Corp years (which must be tracked separately and can trigger dividend treatment on distributions), and whether your shareholder structure currently meets S Corp eligibility requirements.

For most California business owners who have been operating as a C Corp for one to five years and have not accumulated significant appreciated assets, the conversion math almost always favors switching. The longer you wait, the more you pay in unnecessary double taxation.

Red Flag Alert: The IRS Audit Profile of an S Corp Done Wrong

S Corps with zero or near-zero officer compensation are one of the IRS’s highest-audit-rate categories. According to IRS examination data, S Corps that report no W-2 wages for shareholders who are actively working in the business are automatically flagged. In 2023, the IRS assessed over $1.4 billion in additional taxes and penalties from S Corp reasonable compensation audits alone.

The fix is simple but must be executed correctly: pay yourself a salary supported by documented market rate analysis, run payroll through a registered payroll system, file Form W-2 by January 31 each year, and keep records showing the services you performed that justify the compensation. A qualified tax strategist should review your salary structure annually as your revenue grows.

Pro Tip: The IRS compares your reported officer compensation to your total S Corp revenue as a ratio. If you’re taking in $300,000 and paying yourself $24,000, that ratio will trigger scrutiny. As a general benchmark, officer compensation should represent at least 40-50% of net income in service businesses — though this varies significantly by industry and workload.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions: C Corp S Corp Taxation in California

Can an LLC elect to be taxed as an S Corp in California?

Yes. An LLC can elect S Corp taxation by first electing to be treated as a corporation for federal tax purposes (using IRS Form 8832) and then filing IRS Form 2553 to elect S Corp status. California recognizes this structure and applies the 1.5% franchise tax rate instead of the 8.84% C Corp rate. This is one of the most tax-efficient structures available to California self-employed individuals and small business owners.

Does California conform to federal S Corp election rules?

California generally conforms to federal S Corp eligibility rules but requires a separate state-level election via FTB Form 3560. There are also California-specific non-conformity items — including California’s treatment of bonus depreciation and certain federal deductions — that can create differences between your federal and state S Corp returns. Always maintain separate federal and California workpapers.

What is the minimum California franchise tax for an S Corp?

California S Corps are subject to a minimum franchise tax of $800 per year, regardless of whether the business had income. New S Corps in their first year of existence are exempt from this $800 minimum under the first-year exemption enacted in 2000. However, the exemption applies only to the first tax year — the $800 minimum applies in every subsequent year, including years with zero income or a net loss.

Can I retroactively elect S Corp status?

Yes, under IRS Revenue Procedure 2013-30, late S Corp elections can be granted if the entity acted as if it were an S Corp (filed no C Corp returns, all shareholders consented, etc.) and can demonstrate reasonable cause for the failure to timely file. This relief is commonly granted and can be executed retroactively for up to three years and 75 days in some cases. Work with a tax professional to document and file the relief request properly.

Book Your Entity Tax Strategy Session

If your California business is operating under the wrong tax structure right now, every quarter that passes is money you’re handing to the IRS and FTB that you didn’t have to. C Corp and S Corp taxation rules are not complicated once someone walks you through the actual numbers for your specific situation — and the savings are real, immediate, and repeatable year after year.

At KDA, we run a full entity analysis for every new client, compare your current structure against every available alternative, and give you a clear recommendation with real dollar amounts attached — not vague advice. If the switch makes sense, we handle the IRS and FTB filings, payroll setup, and ongoing compliance so nothing falls through the cracks.

Click here to book your entity tax strategy consultation now. Come in with your last tax return. Leave with a plan that pays for itself.