What Is the California Income Tax Rate in 2026?

Tax rate in California income structures operate on a progressive system that can take up to 13.3% of your highest earnings. Most business owners and high earners leave thousands on the table every year because they focus only on federal brackets while California silently claims its share. The difference between planning around both systems versus ignoring California-specific strategies can mean $8,000 to $25,000 in annual savings.

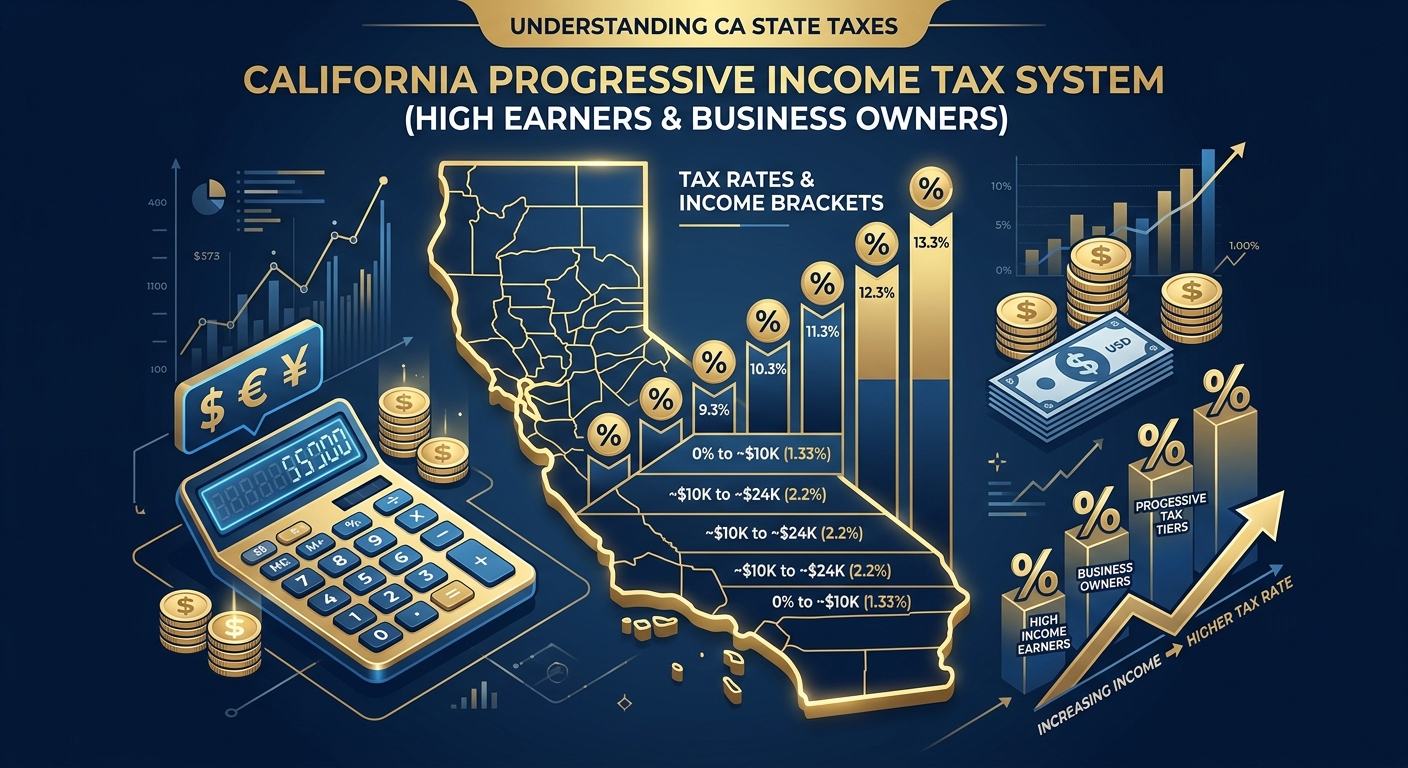

California uses nine income tax brackets for 2026, ranging from 1% on the lowest incomes to 13.3% on income over $1 million for single filers. If you earned $250,000 as a business owner this year, your effective California tax rate sits around 9.8%, but your marginal rate on the last dollar earned hits 10.3%. That marginal rate is what you should focus on when planning deductions, entity structure, and timing strategies.

Quick Answer

California’s 2026 income tax rates range from 1% to 13.3% depending on your filing status and income level. Single filers pay 13.3% on income exceeding $1,000,000, while married couples filing jointly hit that top rate above $1,198,024. These rates apply on top of federal income tax, making California one of the highest-tax states in the nation for high earners.

California Income Tax Brackets for 2026: What You Actually Pay

California operates a nine-bracket progressive income tax system. Unlike flat-tax states, you don’t pay your top rate on all income. You pay increasing rates as your income climbs through each bracket threshold.

2026 California Tax Brackets for Single Filers

| Income Range | Tax Rate | Tax Owed on Bracket |

|---|---|---|

| $0 – $10,412 | 1% | Up to $104.12 |

| $10,413 – $24,684 | 2% | $285.44 |

| $24,685 – $38,959 | 4% | $570.96 |

| $38,960 – $54,081 | 6% | $907.26 |

| $54,082 – $68,350 | 8% | $1,141.44 |

| $68,351 – $349,137 | 9.3% | $26,123.14 |

| $349,138 – $418,961 | 10.3% | $7,191.79 |

| $418,962 – $698,271 | 11.3% | $31,561.97 |

| $698,272+ | 13.3% | Variable based on total income |

If you’re a single filer earning $150,000 in 2026, you don’t pay 9.3% on the entire amount. You pay 1% on the first $10,412, then 2% on the next bracket, and so on. Your actual effective California tax rate would be approximately 6.8%, resulting in about $10,200 in state income tax before deductions.

2026 California Tax Brackets for Married Filing Jointly

| Income Range | Tax Rate |

|---|---|

| $0 – $20,824 | 1% |

| $20,825 – $49,368 | 2% |

| $49,369 – $77,918 | 4% |

| $77,919 – $108,162 | 6% |

| $108,163 – $136,700 | 8% |

| $136,701 – $698,274 | 9.3% |

| $698,275 – $837,922 | 10.3% |

| $837,923 – $1,396,542 | 11.3% |

| $1,396,543+ | 13.3% |

Married couples benefit from roughly doubled bracket thresholds, but the top rate still reaches 13.3% once combined income exceeds approximately $1.4 million.

How California Income Tax Rates Impact Business Owners and High Earners

Business owners face unique California tax challenges because entity structure directly impacts how income flows through to your personal return. If you operate as a sole proprietorship or single-member LLC, all net profit hits your California tax return at your marginal rate.

S Corp vs LLC: California Income Tax Differences

An LLC taxed as a partnership or sole proprietorship pays California income tax on all net business income. If your LLC generates $200,000 in profit, you pay California income tax on the full $200,000 at your marginal rates, plus the 15.3% federal self-employment tax on most of that income.

An S Corp allows you to split income into salary and distributions. You still pay California income tax on both portions, but you avoid the 15.3% self-employment tax on distributions. For a business owner earning $200,000, electing S Corp status and taking a $90,000 salary with $110,000 in distributions saves approximately $16,830 in federal self-employment tax annually. Your California income tax remains the same on the full $200,000, but the federal savings are substantial.

Key Takeaway: Entity structure won’t reduce your California income tax bill directly, but it can significantly reduce your federal tax liability, improving your overall tax position by $10,000 to $25,000 annually depending on your profit level.

California vs Federal Tax Coordination

California generally conforms to federal tax law but maintains several critical differences. The state allows most federal deductions, but California does not conform to bonus depreciation rules that let you write off business equipment purchases faster at the federal level. This means you might depreciate a $50,000 equipment purchase over five years for California purposes while deducting it fully in year one federally.

You must track these differences on Schedule CA (540), adding back or subtracting amounts that differ between federal and California treatment. Missing these adjustments triggers FTB notices and potential audits. Our bookkeeping services help business owners maintain accurate dual-tracking systems that prevent costly reconciliation errors.

Strategies to Lower Your California Income Tax Liability

You cannot avoid California income tax if you’re a state resident or earn California-source income, but you can strategically reduce your taxable income through legitimate deductions, credits, and timing strategies.

Maximize Retirement Contributions

California allows deductions for traditional IRA, 401(k), and SEP IRA contributions just like the federal system. For 2026, you can contribute up to $23,500 to a 401(k) if you’re under 50, or $31,000 if you’re 50 or older. Self-employed individuals can contribute up to 25% of net self-employment earnings to a SEP IRA, with a maximum contribution of $70,000 for 2026.

A business owner earning $250,000 who maxmaxes a SEP IRA contribution of $50,000 reduces California taxable income to $200,000. At a 10.3% marginal California rate, that’s $5,150 in California tax savings, plus approximately $12,000 in federal tax savings, for a combined first-year benefit of $17,150. The money grows tax-deferred until retirement.

Claim the California Earned Income Tax Credit

California offers its own Earned Income Tax Credit (CalEITC) for lower-income working families. For 2026, you may qualify if your adjusted gross income is below approximately $31,000 for filers with no qualifying children, or up to $63,000 for filers with three or more qualifying children.

The credit ranges from a few hundred dollars to over $3,400 depending on income and family size. Unlike a deduction that reduces taxable income, this is a refundable credit, meaning if the credit exceeds your California tax liability, you receive the difference as a refund.

Use the Standard Deduction or Itemize Strategically

California offers a standard deduction of approximately $5,363 for single filers and $10,726 for married couples filing jointly in 2026. If your itemized deductions exceed these amounts, itemizing will reduce your California taxable income further.

Common California itemized deductions include mortgage interest on loans up to $1 million for homes purchased before December 15, 2017, state and local property taxes without the federal $10,000 SALT cap limitation, charitable contributions to qualified organizations, and unreimbursed medical expenses exceeding 7.5% of your adjusted gross income.

California does not impose the $10,000 SALT cap that federal law includes, so if you paid $18,000 in property taxes and $12,000 in other state taxes, you can deduct the full $30,000 on your California return if you itemize. This makes itemizing more valuable for California purposes than federal purposes for many homeowners.

Leverage Business Deductions

If you’re self-employed or own a business, ordinary and necessary business expenses reduce your California taxable income. This includes home office deductions, business mileage at $0.70 per mile for 2026, health insurance premiums if you’re self-employed, and business travel, meals, and entertainment subject to IRS limitations.

A consultant working from home with a dedicated 200-square-foot home office in a 2,000-square-foot home can deduct 10% of mortgage interest, property taxes, utilities, insurance, and maintenance as business expenses. On a home with $24,000 in annual qualified expenses, that’s a $2,400 deduction, saving approximately $576 in California taxes at a 9.3% marginal rate plus federal tax savings.

Special Situations: Part-Year Residents and Non-Residents

Part-Year California Residents

If you moved into or out of California during 2026, you’re considered a part-year resident. You’ll pay California income tax only on income earned while you were a California resident, plus any California-source income earned after you left.

California-source income includes wages for services performed in California, rental income from California properties, and business income from a California business location. If you moved from California to Texas in June 2026, you’ll pay California tax on January through June wages, plus any ongoing California rental income for the full year.

Non-Residents with California-Source Income

Non-residents pay California income tax only on income earned from California sources. If you live in Nevada but perform consulting work for a California client, you owe California income tax on that consulting income even though you’re not a California resident.

You’ll file California Form 540NR and report only your California-source income. You’ll also claim a credit on your Nevada return, though Nevada has no state income tax, so the California tax becomes an unavoidable cost of earning California-based income.

What Happens If You Miss This?

Failing to file a California tax return when you have California-source income triggers FTB enforcement. The Franchise Tax Board can assess taxes, penalties of 25% of unpaid tax, and interest compounding daily. If you earned $75,000 in California-source income as a non-resident and never filed, you could owe $7,000 in taxes, $1,750 in penalties, and $1,200 in interest after two years, totaling nearly $10,000.

KDA Case Study: Small Business Owner

Marcus operated a digital marketing agency as a sole proprietorship, earning $180,000 in annual profit. He paid approximately $16,740 in California income tax at an effective rate of 9.3%, plus $27,540 in federal self-employment tax, totaling $44,280 in combined federal and state taxes before federal income tax.

KDA helped Marcus elect S Corp status and implement reasonable salary compensation of $85,000 with $95,000 in distributions. We set up payroll processing to ensure compliance and established a SEP IRA allowing him to contribute $36,000 annually.

Results: Marcus now pays California income tax on $144,000 ($180,000 minus $36,000 SEP contribution), saving $3,708 in California taxes annually. He eliminated $14,535 in self-employment tax on the $95,000 distribution portion. Combined federal and state savings totaled $21,600 in the first year.

Marcus paid $4,200 for S Corp election, payroll setup, and ongoing tax planning. His first-year ROI was 5.1x, with recurring annual savings of $18,000+ in future years.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

California-Specific Considerations

The California Minimum Franchise Tax

California imposes an $800 annual minimum franchise tax on most LLCs and corporations, regardless of whether the business is profitable. This tax is due even if your business operates at a loss. New LLCs receive a one-year exemption for their first tax year, but the $800 tax applies starting in year two.

If you’re deciding between a sole proprietorship and an LLC, factor in this $800 annual cost. For businesses earning under $50,000 annually, the liability protection of an LLC may not justify the minimum tax expense.

California Does Not Tax Social Security Benefits

Unlike federal tax law, California does not tax Social Security retirement benefits. If you receive $30,000 in Social Security benefits and $50,000 in other retirement income, you’ll pay California income tax only on the $50,000, while the federal government may tax up to 85% of your Social Security benefits depending on your combined income.

California Mental Health Services Tax

California imposes an additional 1% tax on taxable income exceeding $1 million for individuals and $1.25 million for married couples filing jointly. This Mental Health Services Tax applies on top of the regular 13.3% top income tax rate, creating an effective top rate of 14.3% for the highest earners.

If you earn $1.5 million as a single filer, you’ll pay 13.3% on income between $698,272 and $1,000,000, then 14.3% on income exceeding $1,000,000. The additional 1% on $500,000 equals $5,000 in extra California tax annually.

Common Mistakes California Taxpayers Make

Red Flag Alert: Assuming California Conforms to All Federal Tax Law

California maintains numerous differences from federal tax treatment. Bonus depreciation, Section 179 expense limits, and certain federal credits don’t apply to California returns. Taxpayers who assume federal and California returns match often underpay California taxes and face FTB notices demanding additional payment plus penalties.

Always complete Schedule CA (540) to reconcile federal and California differences. This schedule adds back or subtracts amounts that California treats differently, ensuring your California taxable income is calculated correctly.

Red Flag Alert: Ignoring Estimated Tax Payment Requirements

California requires quarterly estimated tax payments if you expect to owe more than $500 in taxes after withholding and credits. Missing estimated payments triggers underpayment penalties even if you pay the full balance when you file your return.

For 2026, estimated tax payments are due April 15, June 16, September 15, and January 15, 2027. If you owe $8,000 annually, you should pay approximately $2,000 per quarter to avoid penalties.

Red Flag Alert: Claiming Nonresident Status While Maintaining California Ties

California uses a facts-and-circumstances test to determine residency. Simply spending more than half the year outside California doesn’t automatically make you a non-resident. If you maintain a California home, driver’s license, voter registration, or professional licenses, the FTB may challenge your non-resident status.

The FTB aggressively audits taxpayers who claim non-resident status after leaving California. If you’re reclassified as a resident, you’ll owe California tax on worldwide income, not just California-source income, resulting in tens of thousands in additional tax for high earners.

How to Calculate Your Effective California Tax Rate

Your effective California tax rate represents the percentage of total income you actually pay in California taxes. This differs from your marginal rate, which is the rate you pay on your last dollar of income.

To calculate your effective rate: Divide your total California income tax by your total income. If you earned $150,000 and paid $10,200 in California income tax, your effective rate is 6.8% ($10,200 divided by $150,000).

Your marginal rate, however, is 9.3% because additional income falls into the 9.3% bracket. This marginal rate determines how valuable deductions and credits are for you. A $10,000 deduction saves you $930 in California taxes at a 9.3% marginal rate, plus federal tax savings.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About California Income Tax Rates

Does California Tax Unemployment Benefits?

Yes. California treats unemployment compensation as taxable income, just like the federal government. If you received $15,000 in unemployment benefits during 2026, you’ll include that amount as income on your California return and pay tax at your marginal rate.

Does California Tax Remote Work Income If I Work for a California Company?

It depends on where you physically perform the work. If you live and work remotely from Arizona for a California-based employer, you generally do not owe California income tax on that income. You’ll pay Arizona income tax instead. However, California may tax income from stock options, restricted stock units, or deferred compensation if it relates to work performed in California before you relocated.

Can I Reduce My California Tax by Moving to Another State?

Yes, but only if you successfully establish residency in another state and sever California residency. This requires more than spending time elsewhere. You must move your domicile, meaning you establish a permanent home in the new state, register to vote there, obtain a driver’s license, close California bank accounts, and demonstrate clear intent to remain in the new state indefinitely.

California will continue taxing you as a resident until you prove you’ve genuinely relocated. The FTB presumes you remain a California resident if you maintain significant contacts with the state.

Book Your Tax Strategy Session

California’s progressive income tax system creates substantial planning opportunities for business owners and high earners who understand how to navigate both state and federal rules. If you’re unsure whether your entity structure, deduction strategy, or residency status is costing you thousands annually, let’s fix that. Book a personalized consultation with our strategy team and get clear, compliant, and confident. Click here to book your consultation now.

This information is current as of 5/25/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.