Many business owners only realize they picked the wrong corporation type when they see a surprise tax bill. By then, they have already paid thousands of dollars they did not need to pay and changing course is slower and more painful than choosing correctly up front.

If you are trying to understand the difference between and s corp and a c corp, you are already ahead of most owners. Getting this call right can mean a five figure swing in lifetime tax paid for a single business.

Fast Tax Fact

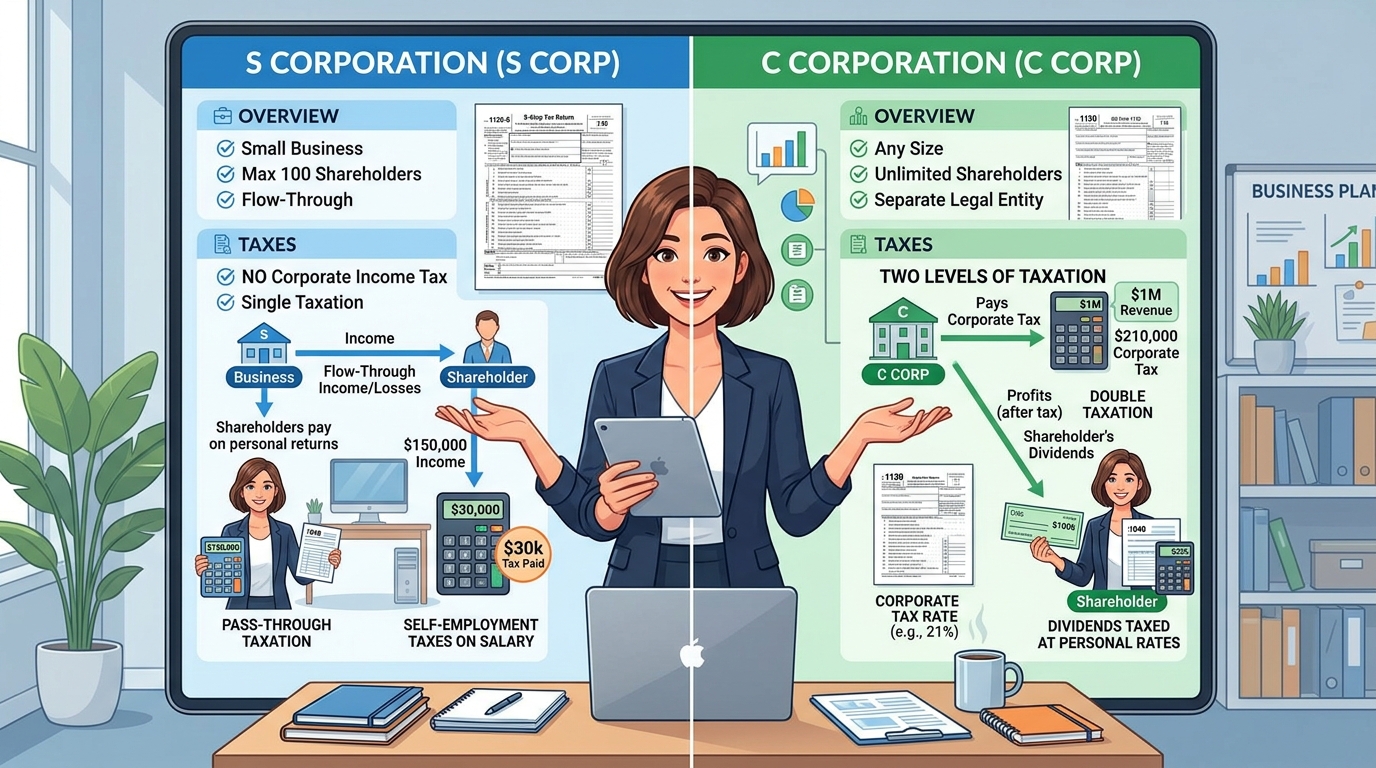

Here is the short version. A C corporation pays corporate income tax on its profits, then shareholders pay tax again on dividends they receive. An S corporation is generally a pass through entity, so profits flow directly to the owners personal returns without a corporate level tax. That single feature is why S corporations often win for closely held businesses, but the details matter.

Quick Answer: The Practical Difference Between an S Corp and a C Corp

The practical difference is how profits are taxed and how flexible you want to be. A C corporation files Form 1120, pays its own federal income tax at a flat rate, and then distributes after tax profits as dividends which shareholders report and pay tax on again. An S corporation files Form 1120 S, usually pays no federal income tax itself, and passes profits through to owners who report everything on their personal returns.

For many small business owners in California, S corporation status reduces overall tax by cutting self employment tax on a portion of profits and avoiding double taxation. For high growth companies planning outside investors or an eventual sale of stock, the C corporation structure often fits better even if the near term tax bill is higher.

How S Corp And C Corp Taxation Actually Works

Think of the tax system as a series of buckets. The first bucket is the business itself. The second bucket is you as the owner. S corporations and C corporations simply fill those buckets in different ways.

C Corporation Taxation

A C corporation is a separate taxpayer. It earns revenue, deducts expenses, and pays tax on its net income at the corporate rate. As of the 2025 and 2026 tax years, that federal rate is a flat 21 percent. The rules for C corporations are detailed in IRS Publication 542.

Example. A marketing agency formed as a C corporation earns $400,000 in profit before the owners take anything out. The company pays $84,000 in federal corporate tax (21 percent of $400,000). The owners decide to distribute $200,000 as dividends. Those dividends show up on the owners personal returns and might be taxed at, say, 15 percent. That is another $30,000 of tax at the shareholder level, bringing the combined federal bill on that $400,000 to roughly $114,000 before any state tax.

S Corporation Taxation

An S corporation is generally treated as a pass through entity. The company itself usually does not pay federal income tax. Instead, it files an informational return and sends each shareholder a Schedule K 1 showing their share of income, deductions, and credits. Owners then report those amounts on their own returns. For a deep dive into how S corporations work, KDA has a full guide at this S corporation tax strategy resource.

Now consider the same $400,000 of profit in an S corporation owned by one person. That owner must take a reasonable salary for the work they perform, which is subject to payroll tax just like any W 2 job. Say a reasonable salary here is $140,000. Payroll taxes apply on that $140,000, but the remaining $260,000 is distributed as S corporation profit not subject to self employment tax. All $400,000 still faces income tax, but avoiding payroll tax on $260,000 can easily save more than $20,000 per year for a single owner.

Why This Matters For Different Taxpayer Types

W 2 employees with side businesses, 1099 contractors, LLC owners, and real estate investors all have different pressure points. For many active business owners, the S corporation is attractive because it allows a mix of W 2 wages and pass through profit, giving more control over payroll tax exposure and retirement plan contributions. For real estate holding entities or companies expecting a venture capital raise, the C corporation may make more sense despite double taxation.

Ownership, Investors, And Who Can Use Each Type

Taxation is only part of the difference between and s corp and a c corp. The law restricts who can own an S corporation. A C corporation has far fewer limits.

Ownership Rules For S Corporations

Under Internal Revenue Code rules and summarized in IRS S corporation guidance, an S corporation must meet these conditions.

- No more than 100 shareholders

- All shareholders must be individuals, certain trusts, or estates. No partnerships, corporations, or nonresident aliens

- Only one class of stock, though voting rights can differ

- Must be a domestic corporation

These restrictions can be deal breakers if you plan to admit investors that are funds, foreign persons, or other corporations. If your long term plan includes institutional capital, the C corporation structure almost always works better.

Ownership Rules For C Corporations

C corporations do not carry those S corporation restrictions. They can have unlimited shareholders, multiple classes of stock, and foreign investors. This flexibility is why nearly every large public company in the United States is a C corporation.

If you are a founder seeking venture capital or planning to grant stock options to attract senior talent, you will likely face pressure from lawyers and investors to organize as a C corporation from day one or to convert before a serious round of funding.

Reasonable Salary Versus Dividends

Another key difference between and s corp and a c corp is how money gets from the company to you and how the IRS expects that flow to look.

Reasonable Compensation In S Corporations

The IRS expects any S corporation owner who works in the business to take a reasonable salary for the services they perform before taking profit distributions. That salary is subject to payroll tax. The term reasonable is not defined by a fixed formula, but IRS examiners look at industry norms, duties, time spent, and what you would have to pay someone else to do your job. There is guidance scattered across IRS rulings and fact sheets.

Example. A consultant runs an S corporation that nets $220,000 before paying the owner. After reviewing market data, $120,000 is defensible as reasonable compensation. The owner pays themselves $120,000 as W 2 wages and takes the remaining $100,000 as a distribution. Roughly speaking, that $100,000 avoids the 15.3 percent combined Social Security and Medicare tax that would otherwise apply if all income were Schedule C self employment income. That alone can save about $15,300 in payroll tax each year.

Dividends And Compensation In C Corporations

C corporation owners who work in the business also take salaries like any other employee. Those wages are deductible to the corporation and subject to payroll tax. Profits left after salary and other expenses face corporate income tax. Any further cash the corporation distributes is usually in the form of dividends which are not deductible by the company, but may qualify for reduced tax rates to individual shareholders.

The IRS can also challenge unreasonably high salaries in C corporations, arguing that what is labeled salary is really a disguised dividend meant to strip profits out of the company and avoid dividend tax. This is almost the mirror image of the reasonable salary issue on the S corporation side.

KDA Case Study: Solo Consultant Switches To S Corporation

A San Diego based marketing consultant, filing as a sole proprietor, had roughly $260,000 of net income in 2024 reported on Schedule C. Between federal and state income taxes and self employment tax, their effective total tax rate on that income was over 38 percent. They came to KDA frustrated that every additional dollar they earned seemed to disappear into tax.

We restructured the practice as an S corporation. For 2025, the business continued to earn around $260,000. Based on industry compensation data and the consultant s actual workload, we set a salary of $135,000. The S corporation paid payroll taxes on that salary and then distributed the remaining $125,000 as S corporation profit.

By avoiding self employment tax on $125,000 and optimizing deductions around a more formal payroll, the client saved just over $18,000 in combined payroll and income taxes in the first full year. Our total fee for the entity planning, S corporation election, and first year corporate and personal tax filings was about $4,800, producing a first year return on investment near 3.8 times.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

When A C Corporation Might Still Be Better

With all the emphasis on pass through taxation, some owners forget that C corporations come with unique planning opportunities. For the right taxpayer, the double taxation bite can be managed or even outweighed by other benefits.

Qualified Small Business Stock

Section 1202 of the Internal Revenue Code allows certain shareholders of qualified small business stock to exclude a large portion, potentially up to 100 percent, of the gain on sale if they meet holding period and other requirements. This benefit is only available for C corporation stock that meets QSBS rules. For founders planning a sizable exit in the future, this one provision can dwarf the annual tax savings of an S corporation in the early years.

Retained Earnings For Growth

A C corporation can retain after tax earnings without forcing income recognition on shareholders. That can be handy for capital intensive businesses planning large expansions or equipment purchases. While S corporations can also leave cash inside the company s bank account, the tax on those profits still passes through to owners each year whether they take distributions or not.

For a fast growing multi location business expecting to roll profits directly back into operations and eventually seek institutional investors, the C corporation may be the cleaner long term structure even if the 21 percent corporate tax seems painful at first.

Common Mistakes That Trigger IRS Problems

Once you know the difference between and s corp and a c corp, the next risk is implementing the choice sloppily. The IRS does not need exotic schemes to assess penalties; basic errors are enough.

Missing The S Corporation Election

To be treated as an S corporation for federal tax purposes, you must file Form 2553 and meet eligibility rules. Many owners form an LLC with their state, assume they now have the tax treatment they want, and never file the election. For federal purposes, that default LLC with a single owner is a disregarded entity taxed as a sole proprietorship, not an S corporation. Multi member LLCs default to partnership tax treatment.

There are late election relief procedures, but they require specific representations and can be stressful. The IRS explains these options in the Form 2553 instructions and related revenue procedures.

Unbalanced Salary And Distribution Mix

On the S corporation side, owners often chase minimal payroll to maximize pass through profit. That might feel good in the short term because payroll tax bills drop. It also paints a target on your return. If your company nets $500,000 and you pay yourself only $40,000 in wages, an IRS examiner will likely argue that your salary is not remotely reasonable.

C corporation owners face the opposite risk if they crank salary up to strip out all profit and avoid dividend treatment. Aggressive strategies on either side can end with reclassification of payments, back taxes, penalties, and interest.

Poor Bookkeeping And Documentation

Both S corporations and C corporations demand disciplined bookkeeping. Sloppy records make it hard to justify your salary decisions, support deductions, or show that you met S corporation eligibility requirements during an audit. Working with professional bookkeeping and payroll support is often the cheapest insurance policy against preventable IRS issues.

Pro Tip: Run The Numbers Before You Choose

Choosing between corporate types is not a gut decision. It s a math problem. Before filing any elections, model at least three years of projected income, salary, and distributions under both S corporation and C corporation tax treatment. Factor in your state taxes as well, especially if you are in California where franchise taxes and S corporation fees change the calculus.

For many active business owners, running those scenarios shows that S corporation status reduces overall tax, especially once income climbs above roughly $80,000 to $100,000 of net profit. For businesses aiming at outside investment, the long term leverage of C corporation stock often wins, but you should see that in black and white before you commit.

What If You Are Already Operating As The Wrong Type

Plenty of successful businesses discover years later that their original choice no longer fits. The tax code provides some flexibility for changing course, but the rules differ depending on which way you are moving.

Converting From C Corporation To S Corporation

A C corporation can elect S status for a future tax year by filing Form 2553 and meeting the usual eligibility criteria. There are special rules about built in gains tax if the corporation holds appreciated assets at the time of conversion. That built in gains tax can apply if you sell or dispose of those assets within a specified recognition period. Planning around this requires a careful review of your balance sheet and growth plans.

Converting From S Corporation To C Corporation

An S corporation can revoke its election or automatically lose it by violating eligibility rules. Once that happens, the company is taxed as a C corporation going forward. There are restrictions on making a new S election for a period of time after a revocation. Shareholders also need planning around accumulated adjustments accounts and how post termination distributions will be taxed.

These conversions are not just check the box exercises. They reshape how your profits are taxed for years. If you have more than a few thousand dollars at stake, you want a tax professional steering this process, not just a form filing service.

Will This Trigger An Audit

Forming an S corporation or C corporation by itself does not put you on an IRS hit list. What draws scrutiny are mismatches and extremes. A pattern of very low owner salaries in S corporations with high profits is one classic trigger. Wildly fluctuating compensation or giant year end bonuses in C corporations that wipe out profits can also raise questions.

Keeping your compensation in line with industry data, maintaining clean books, and documenting how you arrived at key decisions goes a long way. When your situation is unusual, being proactive with explanations in your workpapers and return disclosures helps your position if the IRS ever asks questions.

Bottom Line

The real difference between and s corp and a c corp is not just in IRS forms and code sections. It shows up in how much of your profit you keep after tax, how flexible you are in bringing in investors, and how simple or complex your ongoing compliance will be.

If you are a solo 1099 consultant netting $150,000, an S corporation paired with disciplined salary planning might save you $10,000 to $20,000 per year versus staying a sole proprietor or default LLC. If you are building a high growth software platform targeting outside investors, the C corporation is usually the more strategic choice even if the annual tax bill looks higher in the short run.

This information is current as of 6/19/2026. Tax laws change frequently. Verify updates with the IRS or your tax professional if you are reading this later.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Book Your Tax Strategy Session

If you are not sure whether S corporation or C corporation treatment is costing you money today or limiting your future options, now is the time to get clarity. KDA specializes in matching real world business models to the right tax structure, then building a plan to minimize tax within the rules. Click here to book your consultation now.