Quick Answer

Your tax bracket for 2026 as a single filer determines the rate applied to your top dollar of income, not your entire paycheck. The IRS uses seven progressive brackets ranging from 10% to 37%, with each bracket taxing only the income that falls within its specific range. For example, if you earn $60,000 as a single filer in 2026, you’re in the 22% bracket, but your actual tax burden is calculated across multiple tiers. Understanding which bracket you fall into and how marginal tax rates work can save you thousands through strategic income timing, deduction planning, and entity structuring.

What Is a Tax Bracket and Why Does It Matter in 2026?

A tax bracket is an income range taxed at a specific marginal rate under the federal progressive tax system. The U.S. uses seven brackets for 2026: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Your bracket tells you the rate on your last dollar earned, not the rate on all your income.

Here’s what taxpayers get wrong: If you’re in the 22% bracket, that doesn’t mean 22% of your entire income goes to the IRS. Instead, the first portion of your income is taxed at 10%, the next chunk at 12%, and only the income above a certain threshold hits 22%.

This matters because one extra dollar of income can’t push your entire paycheck into a higher rate. But crossing a bracket threshold can trigger phase-outs for deductions, credits, and tax planning opportunities. Understanding your actual bracket versus your effective tax rate is the first step to proactive tax strategy.

How the 2026 Federal Tax Brackets Work for Single Filers

The IRS adjusts tax brackets annually for inflation. For 2026, the Net Investment Income Tax (NIIT) remains a 3.8% surtax on certain passive income when modified adjusted gross income exceeds $200,000 for single filers. This threshold hasn’t changed, but the bracket structures underneath it have shifted slightly based on inflation adjustments.

While the IRS has released preliminary guidance on certain provisions like the “no tax on tips” deduction (up to $25,000 for eligible workers in tax years 2025-2028), the core bracket system remains consistent. Single filers face the same seven-tier structure, but the income ranges within each bracket expand slightly to account for cost-of-living increases.

For example, a software engineer earning $95,000 in 2026 will see their income taxed across four brackets: 10% on the first $11,600, 12% on income from $11,601 to $47,150, 22% on income from $47,151 to $100,525, and their remaining income taxed at 22%. Their marginal bracket is 22%, but their effective tax rate hovers around 16-17% after accounting for the standard deduction.

What Changed for 2026: New Rules and Adjustments

The biggest federal tax development for 2026 involves the finalized “no tax on tips” provision under the One Big Beautiful Bill Act (OBBBA). Workers in tipping occupations can now deduct up to $25,000 in qualified tips from taxable income. The IRS released final regulations clarifying that tips must be voluntary payments from customers and tied to occupations that customarily received tips before December 31, 2024.

This provision doesn’t change the bracket structure itself, but it does lower taxable income for qualifying workers. A bartender earning $70,000 ($50,000 base + $20,000 tips) can now deduct the full $20,000 in tips, reducing their taxable income to $50,000 and dropping them from the 22% bracket into the 12% bracket on most of their income.

Additionally, California has continued to adjust its state tax brackets independently. While federal brackets are inflation-adjusted, California enacted a high-earners income tax in 2026, affecting taxpayers with income exceeding $1 million. Single filers in California now face both federal bracket calculations and separate state bracket considerations.

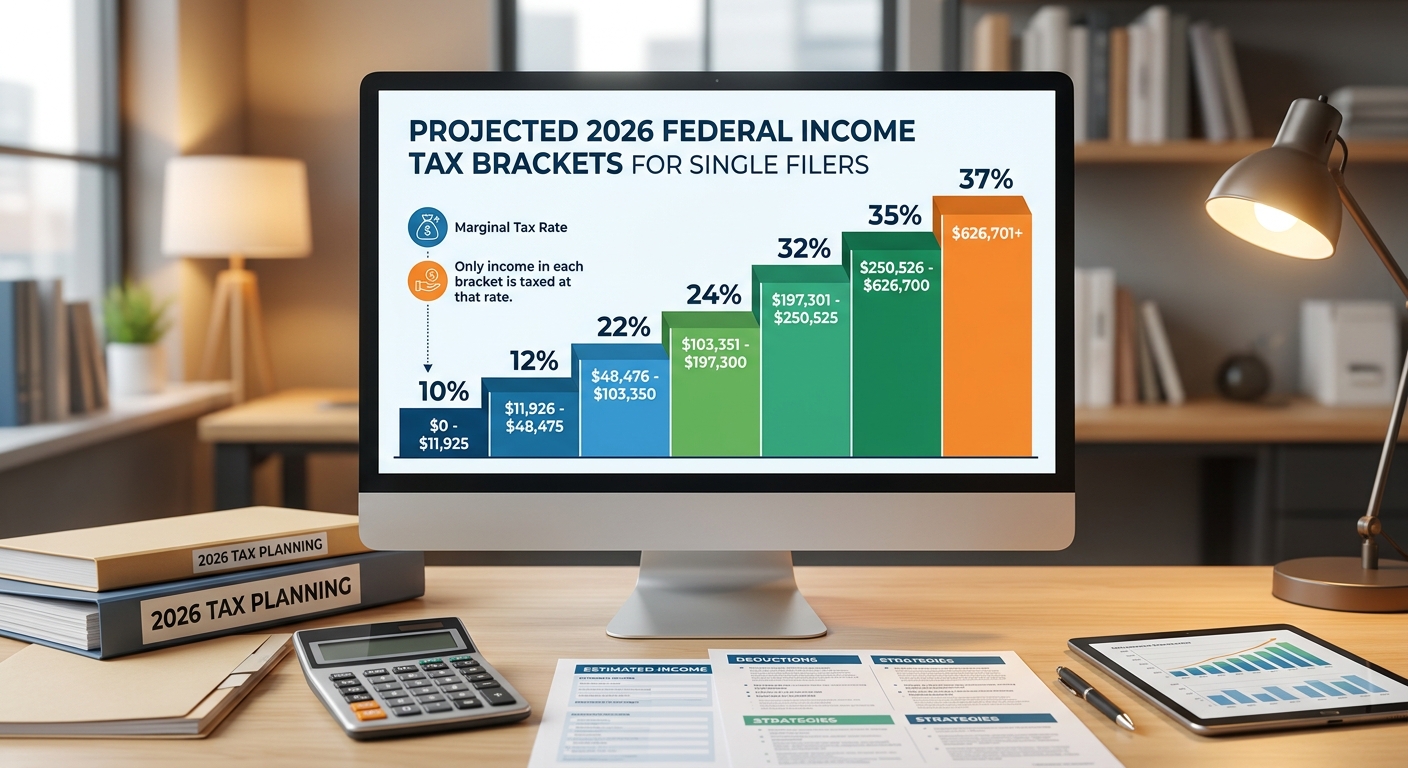

The 2026 Tax Bracket Breakdown for Single Filers

Here’s how the progressive system stacks your income across multiple tiers. Each bracket applies only to the income that falls within its range, not to your total earnings.

10% Bracket: $0 to $11,600

Every single filer starts here. The first $11,600 you earn is taxed at 10%, resulting in $1,160 in federal tax on that portion. This bracket captures entry-level earners, part-time workers, and anyone with minimal taxable income after deductions.

Example: A college student working part-time earns $18,000 in 2026. After taking the standard deduction of $14,600, their taxable income is $3,400. All $3,400 is taxed at 10%, resulting in $340 in federal tax.

12% Bracket: $11,601 to $47,150

Income between $11,601 and $47,150 is taxed at 12%. Most W-2 employees, gig workers, and small business owners with moderate income land here. This bracket captures approximately 60% of single filers.

Example: A graphic designer earning $45,000 pays $1,160 on the first $11,600, then 12% on the remaining $33,400 ($4,008), for a total federal tax of $5,168 before credits or additional deductions.

22% Bracket: $47,151 to $100,525

This is the “sweet spot” where tax planning becomes essential. Income from $47,151 to $100,525 is taxed at 22%. Many professionals, dual-income households (when filing separately), and growing business owners occupy this range.

Example: A project manager earning $85,000 pays $1,160 on the first tier, $4,266 on the second tier, and $8,333 on the $37,850 that falls into the 22% bracket, totaling $13,759 before any deductions or credits.

24% Bracket: $100,526 to $191,950

Once you cross $100,525, the next chunk of income is taxed at 24%. This bracket includes mid-career professionals, successful consultants, and small business owners with solid profit margins.

Example: A software developer earning $150,000 pays cumulative tax on the lower brackets plus 24% on the $49,475 between $100,526 and $150,000, adding $11,874 to their total federal tax liability.

32% Bracket: $191,951 to $243,725

High earners start feeling the pinch here. Income from $191,951 to $243,725 is taxed at 32%. This bracket includes senior managers, equity partners, and individuals with significant investment income.

At this level, the 3.8% Net Investment Income Tax (NIIT) also kicks in for passive income if your modified adjusted gross income exceeds $200,000. You’re now managing both marginal bracket rates and additional surtaxes.

35% Bracket: $243,726 to $609,350

Income between $243,726 and $609,350 is taxed at 35%. This bracket captures high-net-worth individuals, executives with stock compensation, and business owners with seven-figure revenues.

Example: An executive earning $400,000 faces 35% on the $156,624 between $243,726 and $400,000, adding $54,818 to their cumulative federal tax bill. At this income level, entity structuring (S Corp vs. LLC) and retirement contributions become critical tax-saving tools.

37% Bracket: $609,351 and Above

The top federal bracket applies to income exceeding $609,350. Only about 1% of single filers reach this level. At this point, every additional dollar earned is taxed at 37% federally, plus state tax (up to 13.3% in California), plus the 3.8% NIIT on investment income.

Example: A private equity partner earning $1.2 million pays 37% on the $590,650 above the threshold, resulting in $218,540 just from this top bracket, before accounting for lower bracket taxes, state obligations, and surtaxes.

Marginal Rate vs. Effective Tax Rate: The Math That Saves You Money

Your marginal tax rate is the percentage applied to your last dollar of income. Your effective tax rate is the total tax you pay divided by your total income. Confusing these two costs taxpayers thousands in unnecessary panic and poor planning.

Let’s break it down with real numbers. Suppose you’re a single filer earning $90,000 in 2026. Your marginal bracket is 22%, but your effective rate is much lower.

Here’s the calculation:

- First $11,600 taxed at 10% = $1,160

- Next $35,550 ($11,601 to $47,150) taxed at 12% = $4,266

- Next $42,850 ($47,151 to $90,000) taxed at 22% = $9,427

- Total federal tax: $14,853

- Effective tax rate: $14,853 ÷ $90,000 = 16.5%

You’re in the 22% bracket, but you’re only paying an effective rate of 16.5%. This distinction matters when evaluating whether to accelerate income, defer compensation, or convert business entities.

Why This Matters for Strategy

If your employer offers a $10,000 year-end bonus, that bonus isn’t taxed at your full marginal rate in isolation. It stacks on top of your existing income. If you’re already at $90,000, the bonus pushes $10,000 into the 22% bracket, costing you $2,200 in additional federal tax (plus payroll taxes if it’s W-2 income).

But if you contribute $10,000 to a traditional 401(k) instead, you avoid that $2,200 tax hit entirely and reduce your current taxable income. That’s a guaranteed 22% return on the contribution in tax savings alone.

Red Flag Alert: Common Tax Bracket Mistakes That Cost You

Taxpayers make predictable errors every year when it comes to understanding brackets. Here are the most expensive ones:

Mistake 1: Turning Down a Raise to “Avoid a Higher Bracket”

This myth refuses to die. Some workers decline raises or overtime because they think more income will push them into a higher bracket and leave them worse off. That’s mathematically impossible under a progressive system.

Only the income above the bracket threshold is taxed at the higher rate. If you earn one extra dollar that pushes you from the 12% bracket into the 22% bracket, only that one dollar is taxed at 22%. The rest of your income is still taxed at the lower rates.

Example: You earn $47,000 and get a $5,000 raise, bringing you to $52,000. The first $47,150 is taxed at 10% and 12% as before. Only the $4,850 above that threshold is taxed at 22%, costing you an extra $1,067 in federal tax. You still take home $3,933 more after tax. Turning down the raise would be financial malpractice.

Mistake 2: Ignoring the Standard Deduction

The standard deduction for single filers in 2026 is $14,600. This amount is subtracted from your gross income before calculating taxable income. If you earn $60,000 but take the standard deduction, your taxable income drops to $45,400, keeping you firmly in the 12% bracket instead of crossing into 22%.

Many taxpayers calculate their bracket based on gross income instead of taxable income, leading to unnecessary stress and poor planning decisions.

Mistake 3: Forgetting About Phase-Outs and Surtaxes

Certain tax benefits phase out as income rises, creating “hidden” marginal rates. The Net Investment Income Tax adds 3.8% to passive income for single filers earning above $200,000. Student loan interest deductions phase out starting at $85,000. The Earned Income Tax Credit disappears entirely for single filers without children earning above $18,591.

A single filer earning $199,000 who gets a $10,000 raise to $209,000 doesn’t just pay 32% federal tax on that extra income. They also trigger the 3.8% NIIT on investment income, creating an effective marginal rate near 36% on certain dollars.

How to Use Your Tax Bracket to Plan Smarter in 2026

Once you know your bracket, you can make tactical decisions that reduce your tax bill legally and aggressively. Here are the highest-impact strategies for single filers in 2026.

Strategy 1: Maximize Retirement Contributions to Drop a Bracket

Traditional 401(k) and IRA contributions reduce your taxable income dollar-for-dollar. If you’re earning $105,000 and sitting just inside the 24% bracket, contributing $19,500 to a 401(k) drops your taxable income to $85,500, pulling you back into the 22% bracket and saving you $4,290 in federal tax (22% of $19,500).

For 2026, the 401(k) contribution limit is $23,000 for workers under 50, and $30,500 for those 50 and older. If your employer offers a match, you’re leaving free money on the table by not contributing enough to claim it.

Strategy 2: Timing Income and Deductions Around Bracket Edges

If you’re a consultant or freelancer with control over when you invoice clients, consider deferring $10,000 of income from December 2026 to January 2027 if you’re close to a bracket threshold. That $10,000 might be taxed at 22% in 2026 but only 12% in 2027 if you expect lower income next year.

Conversely, if you expect higher income in 2027, accelerate deductions into 2026. Prepay your January mortgage, make a charitable contribution before December 31, or buy business equipment to claim Section 179 depreciation.

Strategy 3: Split Income Through Entity Structuring

If you’re self-employed and earning $120,000 through a Schedule C sole proprietorship, you’re paying 24% federal tax plus 15.3% self-employment tax on most of that income. Electing S Corp status allows you to split income into salary and distributions.

You might pay yourself a reasonable salary of $60,000 (subject to payroll tax) and take $60,000 as a distribution (not subject to self-employment tax). That saves you roughly $9,180 annually in self-employment tax alone (15.3% on $60,000). You also gain more control over bracket management by adjusting salary versus distribution ratios year to year.

Need help optimizing your business structure? Our entity formation services can walk you through S Corp elections, reasonable salary calculations, and payroll setup.

Strategy 4: Leverage the New “No Tax on Tips” Deduction

If you work in a tipping occupation (servers, bartenders, hairstylists, delivery drivers, bellhops, or even certain influencers), the new IRS rules allow you to deduct up to $25,000 in qualified tips from taxable income for tax years 2025 through 2028.

This isn’t a credit. It’s a direct reduction of taxable income. A server earning $55,000 ($35,000 base + $20,000 tips) can deduct the full $20,000 in tips, reducing taxable income to $35,000. After the standard deduction, their taxable income drops to $20,400, keeping them in the 12% bracket and saving them $4,400 in federal tax compared to a scenario where tips were fully taxable.

The IRS finalized these rules in April 2026, so ensure your 2025 tax return reflects this deduction if you qualify. Tips must be reported by your employer or documented if you’re self-employed.

KDA Case Study: Single Filer W-2 Professional

Jessica is a 34-year-old marketing manager earning $110,000 annually as a W-2 employee in Sacramento. She came to KDA in early 2026 because she was frustrated with her tax bill and had heard about strategies to reduce taxable income but didn’t know where to start.

Her situation: Jessica was in the 24% federal bracket with a taxable income of $95,400 after the standard deduction. She wasn’t contributing to her employer’s 401(k) because she thought she needed the cash flow. She had $15,000 in savings sitting in a checking account earning no interest, and she paid $23,400 in federal tax for 2025.

What KDA did: We reviewed her income, bracket positioning, and available deductions. We identified three immediate moves:

- Max out her 401(k) at $23,000 for 2026, reducing taxable income from $110,000 to $87,000

- Open a Health Savings Account (HSA) and contribute $4,150 (2026 limit for single filers), further reducing taxable income to $82,850

- Shift $5,000 into a traditional IRA for an additional deduction, dropping taxable income to $77,850

Tax savings result: Jessica’s taxable income fell from $95,400 to $63,250 after applying all deductions. She dropped from the 24% bracket into the 22% bracket. Her federal tax bill for 2026 came in at $9,485, compared to the $23,400 she paid the prior year. That’s a savings of $13,915.

What she paid: Jessica paid $2,800 for KDA’s tax planning and preparation services.

ROI: She saved $13,915 in the first year while paying $2,800 for our help. That’s a 4.9x first-year return, and the savings continue every year she maintains these contributions.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Special Situations: When Your Bracket Gets Complicated

Not every taxpayer fits the standard single filer profile. Here are edge cases that require extra attention:

Part-Year Residents and Multi-State Income

If you moved from Texas (no state income tax) to California in July 2026, you’ll file a part-year resident return in California. Your federal bracket is calculated on total income, but California only taxes income earned while you were a resident. This can create planning opportunities if you accelerate income while still in Texas or defer California-source income into 2027.

Self-Employed with Irregular Income

Freelancers and consultants often see income swings of $50,000 or more year to year. If you earned $150,000 in 2025 but expect only $80,000 in 2026, consider making a large traditional IRA contribution in 2025 to reduce tax at the 24% rate, then contribute to a Roth IRA in 2026 when your bracket is lower at 22%.

This bracket arbitrage can save $2,000+ annually by timing contributions to years when the tax benefit is highest.

High Earners with Investment Income

If you’re a single filer earning $250,000 with $40,000 in investment income (dividends, capital gains, rental income), you’ll face the 3.8% Net Investment Income Tax on that $40,000 because your modified adjusted gross income exceeds $200,000. Your effective marginal rate on that investment income is 35% federal + 3.8% NIIT + state tax (potentially 13.3% in California) = over 52%.

Strategies to consider: Harvest capital losses to offset gains, defer income into a Qualified Opportunity Zone investment, or shift investment assets into tax-deferred accounts.

California-Specific Considerations for 2026

California doesn’t follow federal tax brackets. The state has its own progressive system with rates ranging from 1% to 13.3%. For 2026, California enacted additional high-earners income tax provisions affecting residents with income over $1 million.

Single filers in California face a combined marginal rate of up to 50.3% (37% federal + 13.3% state) at the highest income levels, before accounting for the 3.8% NIIT. This makes income timing, entity selection, and retirement contributions even more valuable.

California also doesn’t conform to all federal tax law changes automatically. For instance, while the federal “no tax on tips” deduction is available for 2026, California has not adopted this provision. That means a server in Los Angeles can deduct $25,000 in tips federally but still owes California state tax on that income.

Additionally, California offers its own Working Families Tax Credit (WFTC), which expanded in 2026. Single filers without children can now claim the credit if they’re 18 or older (previously 25 or older), and income thresholds have increased. This state credit doesn’t affect your federal bracket, but it reduces your California tax liability and should be claimed on your state return.

What Happens If You Miss This? The Cost of Ignoring Bracket Planning

Failing to plan around your tax bracket results in measurable, recurring losses. If you’re in the 22% bracket and skip a $10,000 401(k) contribution, you pay an extra $2,200 in federal tax that year. Over 10 years, that’s $22,000 in lost tax savings, not counting the compound growth you missed inside the retirement account.

Ignoring bracket positioning also costs you during major financial events. Selling a rental property without considering a 1031 exchange, taking an inheritance without understanding step-up basis, or converting traditional IRA funds to Roth without bracket analysis can trigger five-figure tax mistakes.

The IRS won’t remind you of missed opportunities. They’ll gladly accept your overpayment and move on. Proactive bracket planning ensures you pay only what you legally owe and not a dollar more.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Can I Drop Into a Lower Bracket by Increasing My 401(k) Contribution?

Yes. Traditional 401(k) contributions reduce your taxable income dollar-for-dollar. If you’re earning $105,000 and contribute $10,000 to a 401(k), your taxable income drops to $95,000. That can pull you from the 24% bracket back into the 22% bracket, saving you $2,200 in federal tax on that $10,000 contribution alone.

Do Capital Gains Count Toward My Tax Bracket?

Long-term capital gains (assets held over one year) are taxed at preferential rates of 0%, 15%, or 20%, depending on your taxable income. However, capital gains do add to your total income, which can push your ordinary income into a higher bracket and trigger the 3.8% Net Investment Income Tax if your modified adjusted gross income exceeds $200,000 as a single filer.

How Do I Know If I Should File as Single or Head of Household?

You qualify for Head of Household status if you’re unmarried, paid more than half the cost of maintaining a home, and have a qualifying dependent living with you for more than half the year. Head of Household filers get a higher standard deduction ($21,900 in 2026 vs. $14,600 for single filers) and wider tax brackets, which can save $1,500-$3,000 annually. If you qualify, always file as Head of Household.

Bottom Line: Your Bracket Is a Tool, Not a Trap

Your tax bracket for 2026 as a single filer isn’t something to fear. It’s a tool for decision-making. Once you understand how marginal rates work, the difference between marginal and effective tax rates, and where your income sits within the seven-tier federal system, you can make strategic moves that reduce your tax bill by thousands.

Max out retirement accounts, time income and deductions around bracket edges, leverage entity structuring if you’re self-employed, and claim every deduction available under the new IRS rules. The taxpayers who win aren’t the ones who earn the most. They’re the ones who plan the smartest.

This information is current as of 4/16/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Stop Guessing and Start Saving on Your Taxes

If you’re tired of overpaying because you don’t know which bracket strategies apply to your situation, it’s time to get professional help. Our team specializes in helping single filers, business owners, and high earners reduce their tax bills through aggressive, legal planning. Book your personalized tax strategy session now and find out exactly how much you’re leaving on the table.