Here is a number that stops most investors cold: the difference between selling an asset on day 364 versus day 366 can cost you thousands of dollars in taxes on the exact same profit. Same stock, same gain, two days apart, wildly different tax bill. This is the heart of the short term vs long term gain question, and it is one of the most expensive mistakes taxpayers make without ever realizing it.

Most people think capital gains are capital gains. The IRS does not see it that way. When you understand how holding periods work, you gain a lever that can shave your tax rate nearly in half. When you ignore it, you hand the government money you never had to pay. This guide breaks down exactly how the rules work, who they affect, and how to time your sales so the tax code works for you instead of against you.

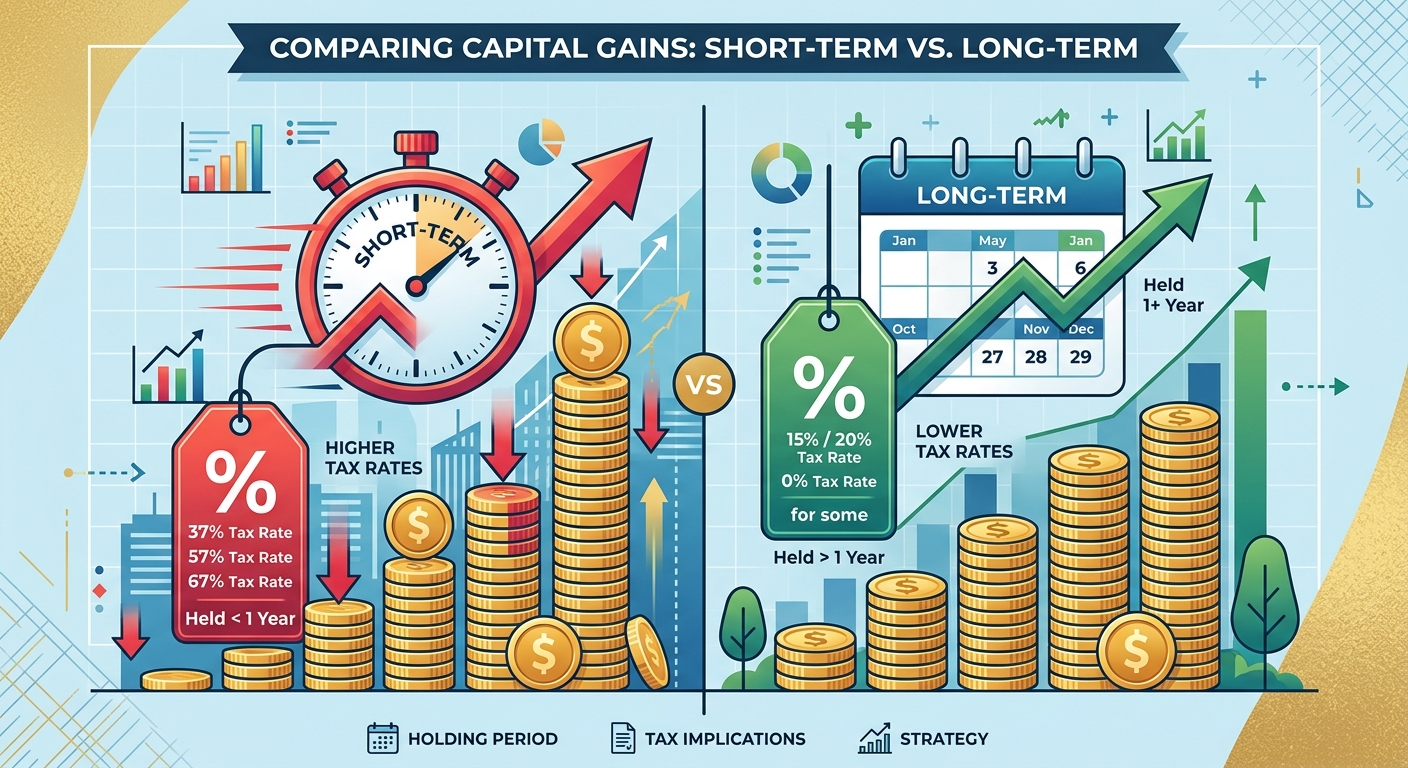

Quick Answer: Short Term vs Long Term Gain

A short term vs long term gain distinction comes down to how long you held the asset before selling it. Hold an asset for one year or less, and any profit is a short-term capital gain taxed at your ordinary income tax rate, which can reach 37 percent federally. Hold it for more than one year, and it becomes a long-term capital gain taxed at 0, 15, or 20 percent depending on your income. That single day past the one-year mark can cut your tax rate dramatically.

Key Takeaway: The magic threshold is one year and one day. Cross it, and you unlock preferential long-term rates that are often less than half the short-term rate.

What Is a Capital Gain, and Why Does the Holding Period Matter?

A capital gain is the profit you earn when you sell a capital asset for more than you paid for it. A capital asset includes stocks, bonds, mutual funds, real estate, cryptocurrency, collectibles, and even a business you own. Your gain is the difference between your sale price and your cost basis, which is generally what you originally paid plus certain adjustments.

The holding period is the clock that determines your tax rate. It starts the day after you acquire the asset and runs through the day you sell it. The IRS uses this window to sort every gain into one of two buckets. That sorting decision is worth real money, because the two buckets are taxed under completely different systems.

Short-Term Capital Gains Explained

A short-term capital gain results from selling an asset you held for one year or less. The IRS treats this profit exactly like your paycheck. It gets stacked on top of your wages and other income, then taxed at your marginal ordinary income rate. For 2026, those brackets climb from 10 percent all the way to 37 percent for high earners.

Here is the plain-English version. If you are a business owner in the 32 percent bracket and you flip a stock for a $20,000 profit after eight months, you owe roughly $6,400 in federal tax on that gain. The IRS does not give you any break for the profit being an investment. It is treated the same as if you earned it working.

Long-Term Capital Gains Explained

A long-term capital gain results from selling an asset you held for more than one year. This profit enjoys a special, lower set of tax rates: 0 percent, 15 percent, or 20 percent for 2026, depending on your taxable income. Most middle and upper-middle income taxpayers land in the 15 percent bracket.

Take that same $20,000 profit. If you had simply waited past the one-year mark before selling, you would likely pay 15 percent, or $3,000, instead of $6,400. That is $3,400 saved on one transaction just by watching the calendar. Multiply that across a portfolio and the numbers become impossible to ignore.

Short Term vs Long Term Gain: Side-by-Side Comparison

Sometimes the clearest way to understand the difference is to see it laid out directly. The table below shows how the two categories stack up on the factors that matter most to your wallet.

| Factor | Short-Term Gain | Long-Term Gain |

|---|---|---|

| Holding period | One year or less | More than one year |

| Federal tax rate | 10% to 37% | 0%, 15%, or 20% |

| Taxed as | Ordinary income | Preferential rate |

| Net Investment Income Tax | May apply (3.8%) | May apply (3.8%) |

| California treatment | Up to 13.3% state | Up to 13.3% state |

Notice the California row. The Golden State does not offer any preferential rate for long-term gains. California taxes all capital gains as ordinary income at rates up to 13.3 percent. So while your federal savings can be dramatic, California residents still owe full state tax on both types of gain. This is a critical detail that national blogs routinely ignore. If you want to model your combined federal and state exposure before you sell, run the numbers through a capital gains tax calculator to see the real after-tax result.

Understanding this distinction is a foundational piece of any smart tax strategy. For a broader view of how gains fit into a full-year plan, our California business owner tax strategy hub walks through how timing decisions like this connect to entity structure, retirement planning, and year-end moves.

KDA Case Study: The Impatient Real Estate Investor

Marcus, a 44-year-old real estate investor in Sacramento, came to KDA after a costly lesson. He had purchased a rental duplex and, after 10 months, received a strong cash offer he could not resist. He sold and pocketed a $95,000 gain. Because he held the property for less than a year, the entire profit was taxed as a short-term gain at his 35 percent federal rate, plus 9.3 percent California tax. His combined bill on that sale exceeded $42,000.

When Marcus brought us his next deal, we built a holding-period strategy into his plan from the start. On a second property with a projected $110,000 gain, we mapped out the exact date he would cross the one-year threshold and advised him to structure the sale just past it. By simply waiting an additional seven weeks, his federal rate dropped from 35 percent to 20 percent. That timing move saved him roughly $16,500 in federal tax on a single transaction.

Marcus paid KDA $4,200 for the planning engagement that covered this deal plus his broader depreciation and entity strategy. The holding-period timing alone returned $16,500, a 3.9x first-year return on the fee, before counting the additional savings from his other strategies. The lesson was simple: patience, applied deliberately, is one of the cheapest tax strategies available.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Five Strategies to Manage Short Term vs Long Term Gain Timing

Knowing the rules is only half the battle. The real value comes from applying them deliberately. Here are five concrete strategies to keep more of your investment profits.

1. Watch the Calendar Before You Sell

The single most powerful move is also the simplest. Before you sell any appreciated asset, check the exact date you acquired it. If you are within a few weeks of the one-year mark, the tax savings from waiting almost always outweigh the risk of a modest price drop. A W-2 employee with company stock sitting at an $8,000 gain could save around $1,900 just by holding past the anniversary date.

Pro Tip: Your brokerage statement lists your acquisition date and holding period status. Never sell a near-anniversary position without confirming which side of the line you are on.

2. Harvest Losses to Offset Gains

Tax-loss harvesting means selling investments that have dropped in value to generate capital losses. Those losses first offset gains of the same type, then the other type, and finally up to $3,000 of ordinary income per year. If you have a large short-term gain, selling a losing position in the same year can neutralize part of that high-taxed profit.

Imagine a self-employed consultant with a $15,000 short-term gain and a stock down $10,000. Selling the loser wipes out $10,000 of the gain, leaving only $5,000 taxed at ordinary rates. At a 32 percent bracket, that is roughly $3,200 in tax avoided in a single year.

3. Match Gains and Losses Strategically

The IRS nets your gains and losses in a specific order. Short-term losses offset short-term gains first, and long-term losses offset long-term gains first. Understanding this netting order lets you plan which positions to sell and when. Getting this wrong can leave your high-rate short-term gains fully exposed while your losses uselessly offset already-low long-term gains.

This is where working with a professional pays off. Our tax planning services help investors sequence sales across a tax year so losses land where they save the most tax, not where they happen by accident.

4. Use Retirement Accounts to Sidestep the Question Entirely

Assets held inside a 401(k), traditional IRA, or Roth IRA are not subject to capital gains tax when you trade within the account. You can sell a stock after two months inside an IRA and owe zero capital gains tax that year. For active traders, holding volatile positions inside tax-advantaged accounts eliminates the short term vs long term gain problem altogether.

5. Time Sales Around Your Income Year

Because long-term rates depend on your taxable income, a low-income year can be a golden window. If your business had a slow year or you took a sabbatical, you might fall into the 0 percent long-term capital gains bracket. In 2026, married couples filing jointly with taxable income under roughly $96,700 pay 0 percent on long-term gains. Selling appreciated assets in a low-income year can mean paying literally nothing in federal capital gains tax.

Red Flag Alert: The Most Common Capital Gains Mistakes

Red Flag Alert: The costliest error is selling just before the one-year mark by accident. Investors get spooked by a dip or excited by an offer and sell at day 350, unaware that 15 more days would have cut their tax rate in half. Always confirm your holding period before pulling the trigger on a sale.

A second frequent mistake is forgetting about the wash sale rule. If you sell a security at a loss and buy the same or a substantially identical security within 30 days before or after, the IRS disallows your loss. This trips up investors trying to harvest losses while staying in a position. The disallowed loss gets added to the basis of the replacement shares, so it is not lost forever, but it does not help you this year.

A third mistake is ignoring the Net Investment Income Tax. Higher earners face an additional 3.8 percent tax on investment income, including capital gains, once modified adjusted gross income exceeds $200,000 for single filers or $250,000 for joint filers. This surtax applies to both short-term and long-term gains and often catches high-net-worth taxpayers off guard.

Special Situations and Edge Cases Most Guides Skip

Inherited Assets Get a Stepped-Up Basis

When you inherit an asset, its cost basis usually resets to the fair market value on the date of death. This is called a stepped-up basis. On top of that, inherited assets are automatically treated as long-term, no matter how long you actually hold them before selling. This is a powerful estate planning tool that can erase decades of built-in gain.

Gifted Assets Carry the Original Holding Period

If someone gifts you an appreciated asset, you generally inherit their cost basis and their holding period. So if your parent held a stock for five years and gifts it to you, then you sell it after two months, it still qualifies as a long-term gain. This carryover rule surprises many taxpayers.

Collectibles Face a Higher Long-Term Rate

Not all long-term gains get the friendly 15 or 20 percent rate. Collectibles such as art, coins, precious metals, and certain physical assets are taxed at a maximum long-term rate of 28 percent. Investors in gold or fine art need to plan around this higher ceiling.

Cryptocurrency Follows the Same Rules

The IRS treats cryptocurrency as property, so the same short term vs long term gain framework applies. Trade Bitcoin after six months and you owe ordinary rates. Hold it past a year and you unlock preferential rates. Crypto investors who trade frequently often generate huge short-term tax bills without realizing it. For detailed rules, review IRS Publication 544, which covers sales and dispositions of assets.

What Happens If You Report This Wrong?

Capital gains are reported on Form 8949 and summarized on Schedule D of your Form 1040. If you misclassify a short-term gain as long-term to claim the lower rate, you are underreporting tax. The IRS receives a copy of your brokerage 1099-B, which lists the acquisition and sale dates, so the agency can easily catch a mismatch.

Underreporting can trigger an accuracy-related penalty of 20 percent of the underpaid tax, plus interest. In more serious cases involving intentional misreporting, penalties climb higher. According to IRS data, mismatches between reported income and third-party documents like the 1099-B are among the most common triggers for automated notices. The lesson is to report holding periods accurately and let legitimate timing strategies, not misclassification, drive your savings.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

How exactly do I count my holding period?

Your holding period begins the day after you acquire the asset and includes the day you sell it. To qualify as long-term, you must sell after holding for more than one full year. That means one year and one day. If you bought on March 15, you must sell on or after March 16 of the following year to get long-term treatment.

Are capital gains taxes different in California?

Yes, and this matters greatly for California residents. California does not offer any reduced rate for long-term gains. The state taxes all capital gains as ordinary income at rates reaching 13.3 percent. So your federal savings from long-term treatment do not carry over to your state return. This information is current as of 7/13/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Can capital losses reduce my regular income?

Yes. After your losses offset your gains, you can use up to $3,000 of net capital loss per year to reduce your ordinary income, or $1,500 if married filing separately. Any excess loss carries forward to future tax years indefinitely until it is used up. This carryforward can be a valuable asset in high-gain years down the road.

The Bottom Line on Timing Your Gains

The tax code rewards patience in a very literal way. The line between a short-term and long-term gain is measured in days, but the financial impact is measured in thousands of dollars. Understanding the short term vs long term gain distinction is one of the highest-return pieces of knowledge any investor can carry, because it costs nothing to apply and can permanently lower your tax bill.

Whether you are a W-2 employee sitting on company stock, a business owner sold on an acquisition, or a real estate investor timing a property sale, the same principle applies. Know your holding period, plan your sales, and let the calendar do some of the heavy lifting on your tax bill. Here is the one-liner worth remembering: in the world of capital gains, one extra day can be worth more than any hot stock tip.

Book Your Tax Strategy Session

If you are holding appreciated assets and unsure whether selling now or waiting could save you thousands, do not guess. Our strategy team maps out the exact timing, netting, and harvesting moves that fit your income and goals so you never overpay on a gain again. Click here to book your consultation now.