Most business owners spend years building a company worth selling. What almost none of them think about until it’s too late is this: the entity type you’re operating under when you sell could cost you six figures more in taxes than it needed to. The difference between selling a C corp vs S corp is not just a legal technicality. It is one of the highest-stakes financial decisions you will ever make, and the IRS treats each exit structure in a way that produces radically different outcomes for the seller.

This guide breaks down exactly how the exit tax works for each entity, what happens in an asset sale versus a stock sale, and how to structure your exit — years in advance if necessary — to keep the maximum amount of what you built.

Quick Answer

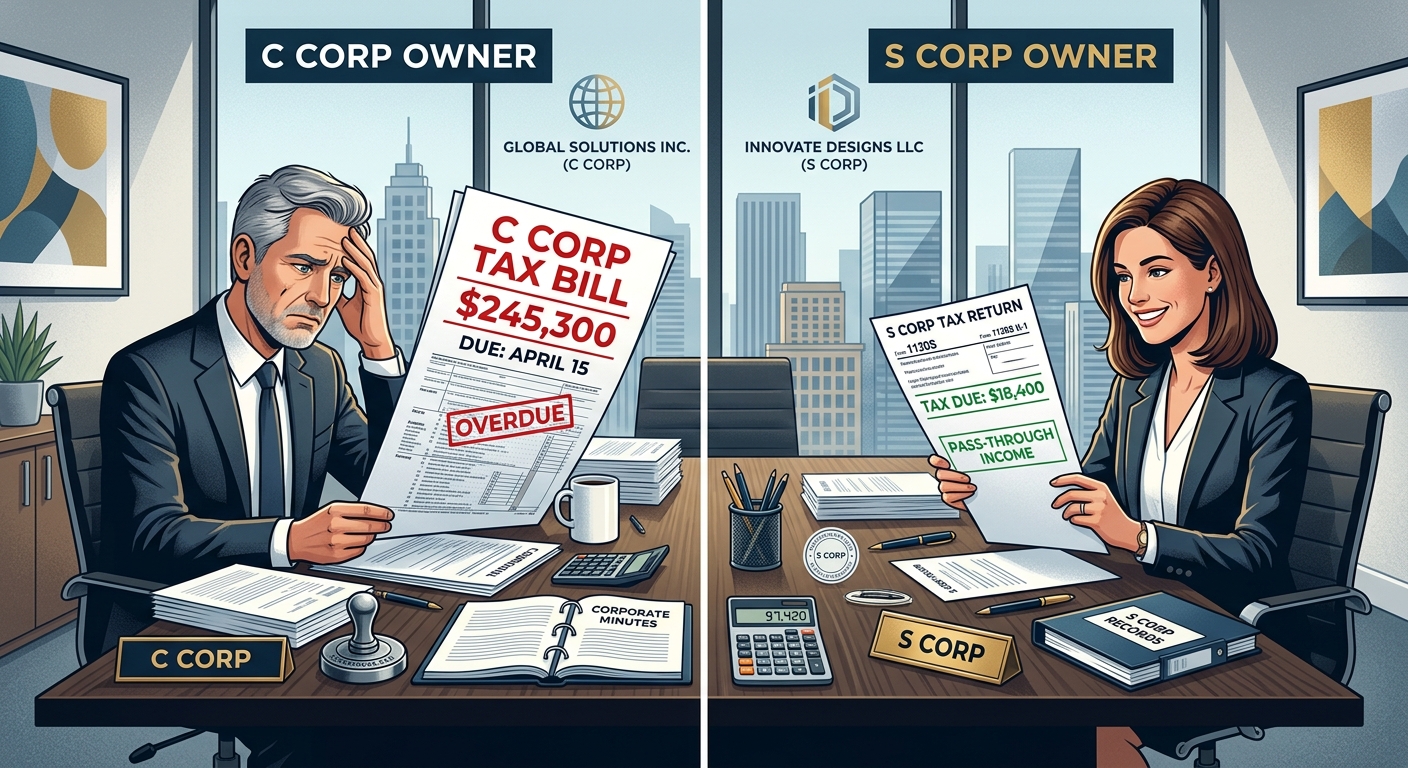

When selling a C Corp, the company pays corporate tax on asset gains, and then shareholders pay capital gains tax on the proceeds — a double taxation event that can push your effective tax rate past 50%. When selling an S Corp, gains typically flow through to shareholders once and are taxed at individual capital gains rates, which are significantly lower. The structure of your sale — asset sale versus stock sale — matters enormously in both scenarios, and the gap between them can exceed $200,000 on a $1 million transaction.

Why the Entity Type You Chose Years Ago Determines Your Exit Tax Today

The entity decision most small business owners make at formation — usually based on liability protection or simplicity — becomes one of the most consequential tax variables at the moment of exit. If you are operating as a C Corporation and a buyer wants your assets (equipment, customer lists, contracts, goodwill), the tax math becomes painful fast.

Here is what happens in a C Corp asset sale: the corporation pays federal corporate tax at 21% on the gain. Then, when the after-tax proceeds are distributed to you as a shareholder, you pay capital gains tax again — up to 23.8% including the 3.8% Net Investment Income Tax (NIIT). If you are a California resident, add the state’s 13.3% capital gains rate on top of that. You are effectively taxed twice on the same money.

An S Corporation avoids this entirely. Because S Corps are pass-through entities, the gain from an asset sale flows directly to shareholders’ individual returns. You pay capital gains tax once, at the individual rate, skipping the corporate-level layer completely. That structural difference is worth real money.

Many business owners who built their companies as C Corps do not realize the exit cost until they are sitting across from a buyer. By then, the window to restructure has usually closed. Planning this five to ten years before exit is not excessive — it is standard practice for anyone who takes their outcome seriously.

For a comprehensive look at how S Corp strategy intersects with long-term business planning, see our complete guide to S Corp tax strategy in California.

Asset Sale vs. Stock Sale: The Deal Structure That Changes Everything

Before comparing entity types head-to-head, you need to understand that the structure of the deal itself — asset sale versus stock sale — creates an entirely different tax reality, regardless of whether you are a C Corp or S Corp.

What Is an Asset Sale?

In an asset sale, the buyer purchases specific assets of the business: equipment, inventory, intellectual property, customer lists, contracts, and goodwill. The selling entity receives the purchase price, and the gain is recognized at the corporate level (for C Corps) or the shareholder level (for S Corps). Buyers almost always prefer asset sales because they get a stepped-up tax basis on the assets they acquire, which creates immediate depreciation benefits for them.

What Is a Stock Sale?

In a stock sale, the buyer purchases the shares of the corporation directly from the shareholders. The selling entity itself does not receive any proceeds — the shareholders do. This means the gain is taxed only once, at the individual shareholder level, and the buyer inherits the company’s tax basis in its assets without a step-up.

Because stock sales eliminate the corporate-level tax for C Corps, sellers strongly prefer them. But buyers resist stock sales when dealing with C Corps precisely because they get no depreciation reset on the acquired assets. This negotiation tension is where significant value is won or lost — and your exit will play out inside that tension.

How Structure and Entity Type Interact

| Scenario | C Corp Asset Sale | C Corp Stock Sale | S Corp Asset Sale | S Corp Stock Sale |

|---|---|---|---|---|

| Corporate-Level Tax | Yes — 21% federal | None | None | None |

| Shareholder-Level Tax | Yes — up to 23.8% | Yes — up to 23.8% | Yes — up to 23.8% | Yes — up to 23.8% |

| California State Tax | Up to 13.3% | Up to 13.3% | Up to 13.3% | Up to 13.3% |

| Effective Rate (CA) | 45–55%+ | Up to 37.1% | Up to 37.1% | Up to 37.1% |

| Buyer Preference | High (step-up basis) | Low | High (step-up basis) | Low |

The numbers above assume long-term capital gains treatment. Short-term gains or ordinary income recapture (such as depreciation recapture under IRC Section 1245) can push rates even higher. Every deal has a mix of asset types, and each one carries its own tax rate at the time of sale.

KDA Case Study: C Corp Owner Avoids a $178,000 Tax Penalty Through Pre-Exit Restructuring

A manufacturing business owner in the Inland Empire — operating as a C Corporation since 2009 — came to KDA in late 2023 with a letter of intent from a private equity buyer offering $2.4 million for his business assets. He was thrilled with the number. He had no idea what was about to happen to it.

After reviewing his entity structure, KDA ran the exit tax projection. In a C Corp asset sale at $2.4 million, with a cost basis of approximately $600,000, the taxable gain was $1.8 million. At 21% corporate tax, the corporation owed $378,000 in federal tax before distributing anything. The remaining $2.022 million distributed to the owner then triggered an additional $174,000+ in federal capital gains tax and NIIT, plus $189,000 in California state tax. His net after-tax proceeds: approximately $1.26 million on a $2.4 million deal — an effective tax rate of over 47%.

KDA worked with the owner and the buyer to restructure the transaction. By allocating a portion of the purchase price toward a personal non-compete agreement (taxed at ordinary income but paid directly to the individual, avoiding the corporate layer) and negotiating a partial stock sale component, KDA reduced the blended exit tax burden significantly. After restructuring, the owner netted approximately $1.44 million — an improvement of $178,000 on the same deal.

The owner’s total investment in KDA’s exit planning services was $6,200. That is a 28.7x first-year return on the tax savings alone.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

The S Corp Advantage at Exit: Why Pass-Through Structure Wins in Most Sale Scenarios

If you are operating as an S Corporation and you sell your business assets, the gain passes through to you personally. You pay federal capital gains tax (0%, 15%, or 20% depending on your income), plus the 3.8% NIIT if your income exceeds the threshold ($200,000 single / $250,000 married), plus California’s rate of up to 13.3%.

There is no corporate layer. No 21% haircut before the money even reaches you. On a $1 million asset sale with a $200,000 basis, the taxable gain is $800,000. A high-income California S Corp shareholder pays roughly $297,600 in combined federal and state taxes — leaving $702,400 net. The equivalent C Corp transaction would leave the same seller with approximately $440,000–$480,000 after double taxation. That gap is real, and it compounds as deal size grows.

Qualified Small Business Stock (QSBS) — The C Corp Exception That Changes the Calculus

There is one scenario where a C Corp exit structure can dramatically outperform an S Corp exit: when the seller qualifies for the Section 1202 Qualified Small Business Stock (QSBS) exclusion. Under IRC Section 1202, shareholders of qualified C Corporations who have held their stock for more than five years can exclude up to $10 million (or 10x their basis, whichever is greater) in capital gains from federal income tax entirely.

The QSBS exclusion does not apply to S Corp stock. This is the primary scenario where experienced founders or early investors in a qualifying C Corp should think carefully before converting to S Corp status — the five-year holding clock, once reset by a conversion, restarts. Losing QSBS eligibility on a $10 million exit is not a recoverable mistake.

To determine whether you qualify, the company must meet several criteria including being a domestic C Corporation, having gross assets under $50 million at time of issuance, operating in a qualifying trade or business (excluding professional services firms, financial firms, and hospitality), and the stock must have been acquired at original issuance. See IRS Form 8949 instructions for reporting QSBS exclusions.

Pre-Exit Planning Moves That Can Save Six Figures

The difference between a good and great exit outcome is almost always determined years before the deal closes. Here are the strategies that KDA deploys for business owners preparing to sell.

Step 1: Convert from C Corp to S Corp Early

If you are a C Corp owner and you do not qualify for QSBS, converting to S Corp status puts you on a clock. The IRS imposes a built-in gains (BIG) tax period of five years under IRC Section 1374. During that window, gains on assets that had appreciated before the conversion are still taxed at the corporate rate (21%) when sold. After five years, the BIG tax no longer applies, and you exit as a pure pass-through entity. If you are planning to sell in year six or beyond, the conversion math almost always works in your favor. The key is starting the clock as early as possible. Our entity formation services include full analysis of conversion timing and tax consequences before any restructuring takes place.

Step 2: Structure the Deal With Mixed Consideration

Not all deal components are taxed the same way. A purchase price can be allocated across tangible assets (equipment, inventory), intangible assets (goodwill, customer lists, non-compete agreements), and consulting or employment agreements. Each category carries different tax treatment for both buyer and seller. Working with a tax strategist to optimize the purchase price allocation under IRS Form 8594 can shift income between ordinary and capital gains rates — legally and with buyer cooperation.

Step 3: Time Installment Sales Strategically

If you are willing to receive proceeds over multiple years, an installment sale under IRC Section 453 allows you to spread the gain — and therefore the tax — across tax years. This can keep you below higher capital gains thresholds or NIIT triggers in any single year. For California sellers, installment sale treatment applies at the state level as well, creating potential for meaningful rate arbitrage if your income fluctuates year to year.

Step 4: Use a Charitable Remainder Trust (CRT) for High-Appreciation Businesses

A CRT allows a business owner to transfer appreciated business interests into a trust before a sale. The trust sells the business tax-deferred, invests the proceeds, and pays the owner an income stream for a defined term. At the end of the trust term, remaining assets pass to charity. The owner receives a partial charitable deduction, defers capital gains tax, and converts a lump-sum payout into a diversified income stream. This is not a strategy for every seller, but for high-net-worth business owners with significant built-in gain, the tax benefits can be substantial.

Want to estimate how much of your sale proceeds you will actually keep after taxes? Run your numbers through this small business tax calculator to get a baseline picture before your exit planning begins.

Common Mistakes Business Owners Make When Selling Their Company

Exit tax planning failures are not usually dramatic. They are quiet, expensive mistakes made by business owners who assumed someone else was handling it.

Mistake 1: Waiting Until the Letter of Intent to Call a Tax Strategist

By the time a buyer sends you a letter of intent, the deal structure is largely set. Renegotiating purchase price allocation or entity structure mid-deal is possible but costly in terms of goodwill and deal momentum. The time to engage a tax strategist is 12 to 36 months before you expect to sell — not after you have a buyer in the room.

Mistake 2: Assuming Your Accountant Will Handle It

General tax preparers handle compliance. Exit tax planning is a specialized discipline that involves deal structure, entity law, IRC Sections 1374, 338, 453, and 1202, and often coordination with your M&A attorney. If your CPA has never walked you through a built-in gains analysis or purchase price allocation strategy, you need a second opinion before signing anything.

Mistake 3: Ignoring Depreciation Recapture

If your business has significant depreciable assets — equipment, leasehold improvements, vehicles — you have likely claimed depreciation deductions over the years. When you sell those assets for more than their depreciated value, the IRS claws that benefit back through depreciation recapture under IRC Sections 1245 and 1250. This recapture is taxed as ordinary income, not capital gains, and it can surprise sellers who assumed their entire gain qualified for preferential rates.

Mistake 4: Forgetting California’s Non-Conformity Rules

California does not recognize the QSBS exclusion under IRC Section 1202. Even if you exclude $10 million from federal capital gains tax using QSBS, California will tax that same gain at its full rate — up to 13.3%. California also does not conform to certain installment sale provisions in the same way federal law does. California-based sellers need separate state-level exit tax modeling, not just a federal projection.

S Corp vs. C Corp Exit: The Decision Framework

Use this framework to determine which exit structure is working for — or against — you.

You are likely better off as an S Corp if:

- You do not qualify for QSBS (most service businesses, professional firms, and mature operating companies)

- Your buyer prefers an asset sale (most private equity and strategic buyers)

- Your business has been operating profitably and the buyer is acquiring your assets, not your stock

- You are a California resident and want to minimize the compounding effect of state plus federal plus corporate tax

- You are more than five years from your anticipated exit date and want to convert from C Corp now

You may be better off staying a C Corp if:

- You qualify for Section 1202 QSBS and have held the stock for more than five years

- You are a venture-backed or angel-funded startup with significant institutional investment

- Your buyer specifically wants a stock sale and you can negotiate the structure accordingly

- You are targeting a sale to a public company or large acquirer who can absorb the basis disadvantage

What If I Already Converted from C Corp to S Corp?

If you converted and have not yet passed the five-year built-in gains window, you are still exposed to corporate-level tax on appreciated assets that existed at the time of conversion. The built-in gains tax under IRC Section 1374 is calculated on the net unrealized built-in gain recognized during the recognition period. After the five-year window passes, you are fully in pass-through territory and the corporate-level tax no longer applies to appreciation that occurred post-conversion.

If you are inside that five-year window and expecting a sale, the planning conversation shifts. You may want to defer the sale, restructure the deal to minimize asset-level gains, or explore whether certain asset categories fall outside the BIG tax computation. This is highly fact-specific analysis that requires professional modeling — not a spreadsheet estimate.

What Happens to S Corp Basis When I Sell?

S Corp shareholders track their basis in shares annually. Basis increases with income allocations and contributions, and decreases with losses and distributions. When you sell your S Corp stock, your gain is calculated as the difference between your sales proceeds and your adjusted basis in the shares. A higher basis means a smaller taxable gain. This is one of the reasons keeping clean, accurate S Corp books every year matters even if you never plan to sell — basis tracking errors at exit can create phantom gain that costs you real money.

This information is current as of 3/23/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Book Your Exit Tax Strategy Session

If you are planning to sell your business in the next one to ten years and you have not done a formal exit tax projection, you are flying blind into the most consequential tax event of your financial life. The difference between a well-structured exit and an unplanned one is not academic — it is six figures, in cash, that you either keep or hand to the IRS unnecessarily. Book a personalized consultation with our exit planning team and walk away with a clear picture of your current exposure, your best restructuring options, and the timeline for making it happen. Click here to book your exit tax consultation now.