If you are netting solid profit in your business and still filing everything on a sole proprietor return, you may be quietly overpaying self employment tax every single year. Many owners stick with Schedule C out of habit or fear of payroll, and by the time they ask for help, they have lost tens of thousands of dollars they can never recover. Thinking strategically about a schedule c to s corp move is often the fastest way to cut your tax bill without cutting your lifestyle.

Quick Answer

When your business profit is consistently above roughly 60,000 dollars per year, staying on Schedule C often means paying more in self employment tax than necessary. An S Corporation lets you split profit between W 2 wages and owner distributions. Only the wage portion is subject to Social Security and Medicare tax. If you pick a reasonable salary, run real payroll, and follow the rules, that split can legally save many California owners 5,000 dollars to 15,000 dollars per year in federal and state taxes.

This information is current as of 6/12/2026. Rules can change, so confirm details with the IRS, the California Franchise Tax Board, or a qualified advisor before you act.

When Staying on Schedule C Starts Costing You Real Money

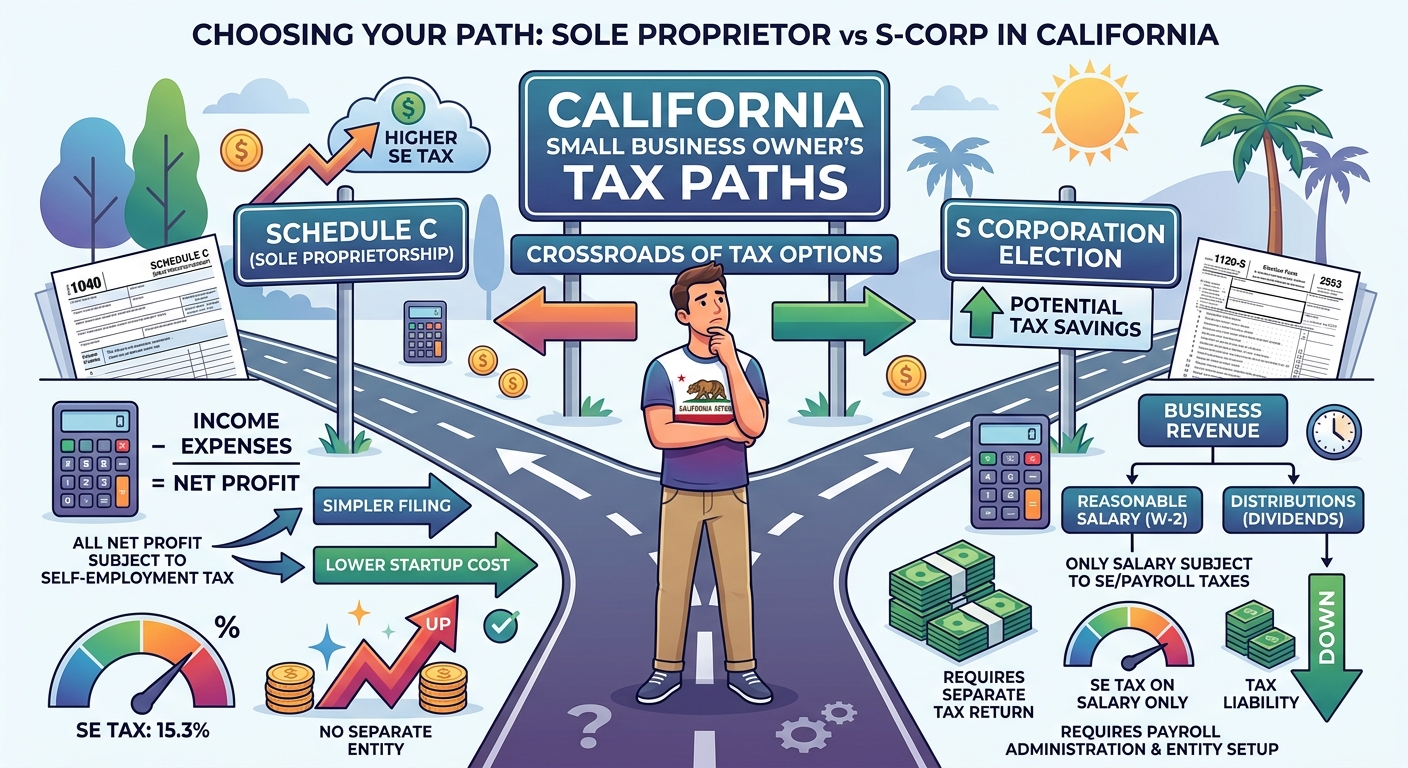

Schedule C is the default for most freelancers, solo consultants, and new side hustles. You report your business income and expenses on a single form, attach it to your Form 1040, and pay income tax plus self employment tax on the net profit. The simplicity works when profit is small. It turns into a problem once profit grows.

Self employment tax is 15.3 percent on the first Social Security wage base amount of combined wages and self employment income, then 2.9 percent Medicare tax above that, plus an extra 0.9 percent Medicare surtax once you pass certain thresholds. The IRS explains this in its self employment tax guidance. On a 100,000 dollar Schedule C profit, you can easily see 15,000 dollars or more in self employment tax on top of regular income tax.

Many business owners accept that bill as the cost of doing business because no one has walked them through the alternatives. Once you understand how an S Corp works, it becomes clear why running a mature six figure business on pure Schedule C is rarely the most tax efficient choice.

Here is a simple comparison for a California owner with 120,000 dollars of net profit, no employees, and no other income. Numbers are rounded to keep the concepts clear.

- Schedule C sole proprietor 120,000 dollars profit taxed as self employment income. Self employment tax roughly 18,000 dollars. Income tax calculated on full 120,000 dollars, with some deduction for half of the self employment tax under IRS Publication 535.

- S Corporation Same 120,000 dollars of economic profit inside the corporation. Owner takes 70,000 dollars as W 2 salary and 50,000 dollars as profit distribution. Payroll taxes apply only to the 70,000 dollars of wages. Self employment tax disappears on the 50,000 dollars distribution portion.

The result in this simplified scenario is often a savings in the range of 7,000 dollars to 10,000 dollars per year once you factor in payroll costs and California S Corp franchise tax. The exact number depends on your bracket, deductions, and how cleanly your books are kept, but the direction is usually the same. As profit climbs, the tax advantage of the S Corp structure grows.

Step by Step Your Schedule C to S Corp Transition

Moving your reporting from Schedule C to an S Corporation is not just checking a box. It is a legal and tax process that has to be sequenced correctly so the IRS recognizes the new structure. At a high level, you are creating a separate entity, electing S Corp status, and then paying yourself partly as an employee and partly as an owner.

Here is how a clean transition usually looks for a California based owner.

- Form a legal entity with your state. Most small operators choose a California LLC or corporation, depending on liability and long term plans. The state filing creates a legal shell that can then elect S status.

- Obtain an EIN for the new entity. You use the IRS online EIN application and keep the confirmation letter. This EIN becomes the identification number for payroll and corporate returns.

- File Form 2553 to elect S Corporation status. This is the actual S election. The IRS describes how and when to file in its Form 2553 instructions. Missing the deadline can cause a full year of lost savings.

- Set up real payroll for yourself as an employee. You run W 2 wages, withhold taxes, and file required payroll returns as described in IRS Publication 15. Payroll is not optional for S Corp owners who are active in the business.

- Move your business activity out of Schedule C. New income and expenses flow through the S Corp books. At tax time, the business files Form 1120 S, and you receive a Schedule K 1 that feeds into your personal return.

Our entity formation services handle this sequencing so you do not stumble over timing rules or miss critical forms. We also coordinate with ongoing bookkeeping so that the first S Corp year is clean instead of chaotic.

For a fuller walkthrough of salary, distributions, and California specific rules, review our complete S Corp tax strategy guide for California once you finish this article.

KDA Case Study: California Consultant Cuts Self Employment Tax

Consider Lisa, a marketing consultant in Los Angeles. For three years she operated as a sole proprietor, filing on Schedule C with profit in the 130,000 dollar range. She had no employees and minimal overhead. Her CPA kept telling her that her tax bill was normal. Lisa suspected something was off when friends with similar income were paying far less in total tax.

When she came to KDA, we rebuilt her numbers and ran a detailed schedule c to s corp comparison. On Schedule C she was paying close to 20,000 dollars a year in self employment tax alone. After reviewing her role, we set a reasonable S Corp salary of 80,000 dollars and treated the remaining 50,000 dollars as distributions. We also cleaned up her expense tracking using guidance from IRS Publication 334, which covers small business record keeping.

In the first full S Corp year, Lisa saved about 9,200 dollars in combined federal and California tax after factoring in payroll costs and the 800 dollar California minimum franchise tax. Our fee for the entity formation, S election, and first year advisory work was roughly 3,500 dollars. That is a first year return on investment of more than 2.5 times, with similar savings expected going forward as long as her profit stays in the same range.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How to Decide If Schedule C or S Corp Fits You This Year

The right choice is not only about saving tax on paper. You have to weigh the savings against new costs, complexity, and your growth plans. Here is a practical way to think about it.

| Factor | Schedule C | S Corporation |

|---|---|---|

| Typical use | Side hustles, early stage freelancers, low profit years | Established businesses with steady profit |

| Self employment tax | Applies to all net profit | Applies only to salary portion |

| Admin and compliance | One personal return with Schedule C | Corporate return, payroll, extra filings |

| Best profit range | Under about 60,000 dollars | Usually above 60,000 dollars and especially above 100,000 dollars |

| California costs | No S Corp franchise tax | 800 dollars minimum franchise tax plus 1.5 percent S Corp tax on net income |

Red Flag Alert If your profit is under 40,000 dollars most years, forcing an S Corp for the sake of having a corporation can backfire. The California franchise tax and payroll costs can easily eat up any self employment tax savings. In that range, it is often better to optimize deductions on Schedule C and wait until your numbers justify a change.

Pro Tip Before you choose a structure, run your last year s numbers through a scenario tool like a small business tax calculator. Seeing the side by side impact of payroll tax, California S Corp tax, and your own bracket makes the decision far more objective.

The decision line is rarely a hard cutoff. A stable 80,000 dollar profit in a low overhead consulting practice is a stronger candidate for an S Corp than a volatile 90,000 dollar profit from a seasonal business. That is why we treat each schedule c to s corp analysis as a custom calculation rather than a rule of thumb.

Common Mistakes That Trigger IRS Problems With S Corps

S Corporations are a powerful planning tool, but they are also a favorite audit target when owners abuse the reasonable compensation requirement. The IRS expects shareholder employees who perform substantial services to pay themselves a market based salary. Take too little salary and the savings can disappear in penalties and back payroll taxes.

Here are mistakes we see repeatedly when owners attempt a do it yourself schedule c to s corp conversion.

- Paying no salary at all. Treating every dollar as a distribution is a direct invitation for the IRS to reclassify income and assess back tax. IRS examiners are trained to look for this pattern.

- Setting a token salary. Paying yourself 20,000 dollars in wages on a 200,000 dollar profit is rarely defensible. The IRS will ask what someone in your role would be paid on the open market and compare it to your numbers.

- Ignoring payroll filings. Once you elect S status, you must handle quarterly payroll returns, year end W 2s, and payroll deposits. Publication 15 and related guidance from the IRS describe these in detail.

- Continuing to use Schedule C. Some owners forget to shut down their old Schedule C reporting after the S election and accidentally double report income or mix pre and post election activity.

According to IRS enforcement data, payroll and employment tax issues are a major driver of small business audits each year. The safest approach is to document how you chose your salary, keep support for your numbers, and work with a firm that has defended S Corp positions before.

What If You Are Late On Your S Corp Election

Many owners hear about S Corps a year or two after they should have switched and assume it is too late. The IRS does offer late election relief in certain cases when you can show reasonable cause and consistent treatment as an S Corp. The details are technical, and the cost benefit needs to be modeled carefully.

If your business has been profitable for several years on Schedule C and you only now understand the schedule c to s corp opportunity, it may still be possible to salvage part of the savings. That decision turns on specific facts, your bookkeeping quality, and your tolerance for dealing with IRS correspondence. This is not something to attempt casually with a generic form letter.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About Moving From Schedule C to S Corp

Will this change how I pay estimated taxes

Yes. As a Schedule C filer you usually pay quarterly estimated tax based on expected net profit. Once you move to an S Corp, part of your tax is covered through payroll withholding on your salary, and the rest is paid through estimates on the K 1 income. The total tax can drop if the structure is set up correctly, but you still need a payment plan that keeps you out of underpayment penalties.

Does the S Corp affect my Qualified Business Income deduction

The Qualified Business Income deduction, often called the QBI deduction, is available to many pass through owners, including S Corp shareholders, subject to wage and income limitations. For high earning professionals in fields like law and medicine, the deduction can phase out. The way you split salary and distributions inside an S Corp can either support or limit your QBI benefit. This is another reason to model the schedule c to s corp move before you file the election.

Can real estate investors use the same strategy

Pure rental income that belongs on Schedule E is usually not a fit for S Corporation treatment, and putting appreciating real estate inside an S Corp can create exit tax headaches. However, active flippers and real estate agents sometimes benefit from S Corps if they have substantial earned income. The key is to separate long term assets from short term commission or flip income and then evaluate structure with that clarity.

What does California add on top of federal rules

California respects the federal S election but adds its own tax layer. S Corporations pay the annual 800 dollar minimum franchise tax plus 1.5 percent of net income as an entity level tax. Shareholders then report their K 1 income on their California Form 540. The state level cost eats into some of the self employment tax savings, which is why we rarely recommend an S Corp at very low profit levels. For the right profit band, particularly above 100,000 dollars, the math still comes out in favor of the S Corp in most cases.

Book Your Tax Strategy Session

If your business profit has outgrown Schedule C, staying put can quietly drain five figures from your net worth over the next few years. A targeted schedule c to s corp review models your actual numbers, tests different salary levels, and quantifies the impact of California taxes so you can choose with confidence instead of guesswork. Our team builds and defends S Corp structures daily, which means you get strategy and execution, not just theory.

If you are unsure whether your current setup is costing you unnecessary self employment tax, let us run the numbers with you and map out a cleaner structure. Book a personalized consultation with our strategy team and get clear, compliant, and confident about your next move. Click here to book your consultation now.