Most LLC owners hear that S corporations save taxes and C corporations are for big companies, then stop there. That shallow understanding is exactly how profitable businesses drift into the wrong structure and quietly bleed five or even six figures in avoidable tax over a decade.

This article is for the owner who wants a clear, numbers based way to evaluate the difference between an s corp and a c corp llc in 2025 and beyond, especially if you are in California or another high tax state.

Quick Answer

An LLC can choose to be taxed as an S corporation or a C corporation, and that choice controls how profits are taxed, who pays self employment tax, how dividends work, and whether you face double taxation. S corporation status usually fits profitable owner operated businesses that want to reduce self employment tax, while C corporation status can make sense for companies reinvesting heavily, bringing in outside investors, or planning a sale with stock based exits. The wrong choice can easily cost $10,000 to $50,000 over a few years.

This information is current as of 5/16/2026. Tax laws change often, so confirm details with the IRS or a qualified advisor if you are reading this later.

How LLC Tax Status Really Works

Before comparing S and C treatment, you need to understand how the IRS sees your LLC. An LLC is a legal wrapper under state law, not a tax category by itself. For federal taxes, the IRS looks through the LLC and treats it as one of three things by default:

- Single member LLC treated as a sole proprietorship reported on Schedule C

- Multi member LLC treated as a partnership filed on Form 1065

- LLC that elects corporate treatment using Form 8832, then possibly S status using Form 2553

Corporation status changes how profits move to you, what payroll looks like, and which returns you file. The main IRS guidance for corporations is in IRS Publication 542, while rules on business expenses live in IRS Publication 535. S corporation elections use Form 2553 instructions.

If you are already running payroll or you plan to build a team, you are squarely in the group that needs to weigh S corporation and C corporation options, not just default to a simple LLC.

Core Tax Difference Between S Corp and C Corp For An LLC

At the heart of the decision is one question: Do you want profits taxed once at your personal rates, or are you willing to accept two layers of tax in exchange for other benefits? That is the structural difference between an s corp and a c corp llc.

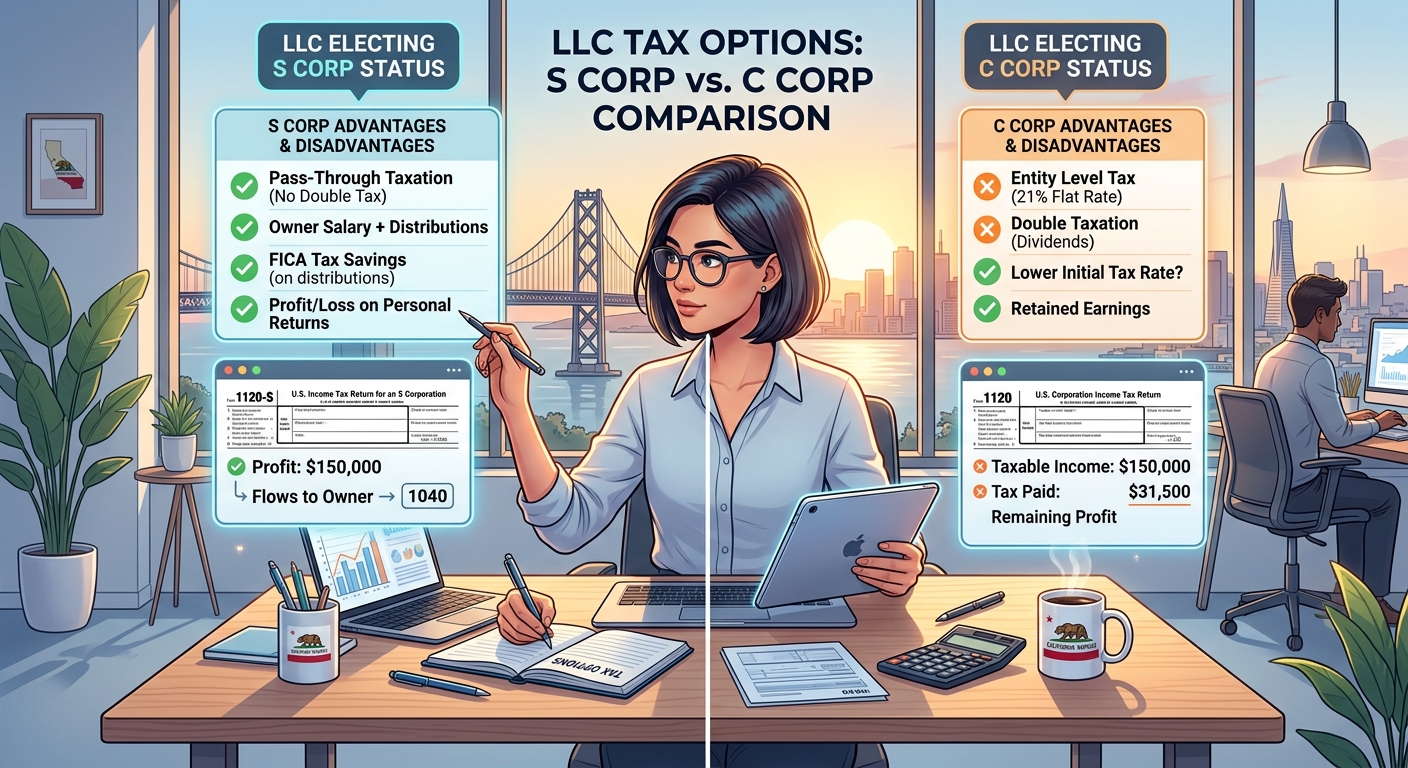

Single Level Taxation With S Corporation Status

An S corporation is a pass through entity. The company files an informational return on Form 1120 S and issues Schedule K 1s to shareholders. All profits or losses pass straight to your personal return, whether or not you distribute cash.

Key effects for a typical LLC owner:

- You must pay yourself a reasonable W 2 salary subject to payroll taxes

- Profit above that salary usually passes through as distributions not subject to self employment tax

- You may qualify for the Qualified Business Income deduction of up to 20 percent of business profit if you meet the rules in Section 199A (see IRS QBI guidance)

- No corporate level federal income tax on S corporation profits in most situations

For a California LLC that elects S status, there is also a 1.5 percent California S corporation franchise tax on net income with an $800 minimum, as outlined by the Franchise Tax Board. That is on top of your personal California tax.

Double Taxation With C Corporation Status

A C corporation is a separate taxpayer. The business files Form 1120 and pays its own federal income tax. If it distributes after tax profits to you as dividends, those dividends are taxed again on your personal return.

Key effects for that same LLC if it elects to be taxed as a C corporation:

- Corporate profits are taxed at a flat 21 percent federal rate

- Dividend payouts to individual shareholders are taxed again at qualified dividend rates, often 15 to 20 percent plus potential 3.8 percent net investment income tax

- Owner wages are deductible to the corporation, just like any other employee

- Losses stay inside the C corporation and generally cannot offset your personal income

The phrase double taxation is accurate. Profit can be taxed once at the corporate level and a second time when you take it out as dividends or if you sell shares and recognize gain.

Why Profit Level Drives The Better Choice

To see how this plays out, consider an LLC with $200,000 of net profit before owner compensation in 2025.

- If you stay a default LLC taxed as a sole proprietorship, all $200,000 is subject to income tax and roughly 15.3 percent self employment tax on most of it

- If you elect S status and pay yourself, say, $100,000 in W 2 wages and take $100,000 as profit distributions, only the wage portion is hit with Social Security and Medicare payroll tax

- If you elect C status, you pay yourself wages and leave some profit in the corporation or pay it out as dividends

At that level of profit, a well structured S corporation often wins on total tax for an owner operator who is actively working in the business.

KDA Case Study: LLC Owner Chooses The Right Tax Status

Consider Maria, who runs a marketing agency as a California LLC. In 2023 she netted $220,000 on a Schedule C and paid over $32,000 in self employment tax alone, on top of income tax. She came to KDA frustrated that she always owed a large balance in April even though she made quarterly payments.

We modeled three options for 2024 and 2025: staying a Schedule C, electing S corporation status, and electing to have the LLC taxed as a C corporation. Under the S structure, we set a defensible W 2 salary of $110,000 based on market pay for a creative director and let the remaining profit flow through as distributions. We also identified another $18,000 of legitimate business expenses under the guidance of IRS Publication 535 on business expenses.

Under the C corporation model, the entity tax at 21 percent plus California corporate tax eroded much of the benefit, and dividends to Maria would be taxed again. The numbers were clear. Compared with staying a Schedule C, the S corporation structure for her LLC reduced self employment and payroll related taxes by about $9,800 in the first year and around $11,200 in the second year as profit grew. After payroll and bookkeeping costs, her net savings were approximately $7,000 per year.

That is the practical power of understanding the structural differences instead of defaulting to the simplest option. Small changes in salary, distributions, and entity type create large changes in long term tax drag.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

When An LLC Taxed As S Corp Makes The Most Sense

Most profitable, owner operated businesses between roughly $80,000 and $600,000 of annual net income should at least evaluate electing S status. Here is why.

Self Employment Tax Savings

When your LLC is taxed as a sole proprietorship or partnership, the entire net profit is generally subject to self employment tax. At $150,000 of net income, that is roughly $18,000 to $20,000 in Social Security and Medicare tax.

By contrast, an LLC that elects S corporation status splits that income into wages and profit distributions. The wages are subject to payroll tax, but the distributions are not. Suppose you earn $180,000 from your consulting business:

- Default LLC: most or all $180,000 hit with self employment tax

- S corporation: $100,000 salary plus $80,000 distributions, payroll tax only on the salary

That one structural move can cut your self employment tax by $8,000 to $10,000 per year at that income level.

If you want a sense of how your total federal tax changes when you move income between salary and distributions, plug your numbers into a solid small business tax calculator to see how different profit and wage mixes change your total bill.

Qualified Business Income Deduction

S corporation pass through profit can qualify for the Qualified Business Income deduction, which is up to 20 percent of eligible profit for many owners under Income thresholds, subject to the detailed rules in Section 199A and discussed in IRS guidance. That deduction is not available for wage income. Structuring your compensation so that a portion of profit shows up as pass through income instead of wages can increase the deduction amount if you are under the phaseout ranges.

Reasonable Compensation Is Not Optional

There is a trap here. The IRS expects S corporation owners who materially participate to pay themselves reasonable compensation for their work before taking large distributions. If you set your own salary at $30,000 while taking $200,000 of distributions, you are waving a red flag.

IRS enforcement on S corporation reasonable comp is guided by case law and internal guidance, and audits often reclassify distributions as wages, adding payroll tax and penalties. The safe approach is to document salary decisions using salary surveys and job descriptions and treat yourself like you would treat a non owner executive.

Why S Corps Often Fit 1099 And Professional Owners

Freelancers, consultants, creatives, and solo professional practices are often ideal S corporation candidates once net income clears roughly $80,000. Many of these owners think in terms of hourly rates or project fees, not entity tax treatment. For those profiles, the difference between an s corp and a c corp llc shows up directly in the owner’s personal cash flow because nearly all economic value flows to one or two active owners.

At that stage, working with an advisor who understands entity mechanics is more important than shopping for the cheapest tax prep. KDA’s team frequently helps self employed business owners restructure their LLCs and salary setups as part of a broader plan, not as a one off election.

When An LLC Taxed As C Corp Deserves A Look

C corporations get a bad reputation among small business owners because of double taxation. That is justified for many lifestyle businesses, but in some specific situations an LLC taxed as a C corporation can be the better fit.

Reinvesting Most Profits In The Business

If your growth strategy requires heavy reinvestment in staff, technology, or inventory, you may not be taking large dividends anyway. In that case, paying tax at the 21 percent federal corporate rate and keeping profits inside the entity can be efficient, especially if your personal marginal rate is significantly higher than 24 percent.

Consider a real estate technology startup in California structured as an LLC that elects corporate status. The company earns $800,000 in profit but reinvests most of it. As a C corporation, it pays 21 percent federal on that $800,000 and California corporate tax, but shareholders do not recognize income until dividends or a liquidity event. If owners are in the 35 percent or 37 percent individual bracket, that deferral and rate arbitrage can matter.

Outside Investors And Different Share Classes

S corporations are highly restricted when it comes to shareholders and stock types. They are limited to:

- 100 shareholders or fewer

- Only certain types of shareholders, such as individuals who are U.S. persons and certain trusts

- One class of stock as to economic rights, though voting rights can differ

That makes S corporations a poor fit when you plan to bring in larger investors, issue preferred shares, or use warrants and complex equity. A C corporation structure, which your LLC can elect, supports common and multiple classes of preferred stock and almost any investor type, which is why venture backed companies standardize on C corporations.

Planning For Sale Or Qualified Small Business Stock

C corporation status opens the door to potential Qualified Small Business Stock benefits for C corporations meeting Section 1202’s requirements. If your company can qualify, shareholders may be able to exclude a sizeable portion of capital gain on sale, in some cases up to the greater of $10 million or ten times basis. Those rules are complex and subject to strict limitations, so this is not something to DIY, but it illustrates that the tradeoff between double taxation and other benefits is not always straightforward.

How C Corporation Elections Work For LLCs

For an LLC to be taxed as a C corporation, you use Form 8832 to elect to be classified as an association taxable as a corporation. If you then want S corporation status, you file Form 2553 as well. The timing and effective date of these elections drive which year the change takes effect. Late election relief may be available under IRS procedures in some cases.

Because 2025 and 2026 guidance on corporate tax topics continues to evolve, the IRS has programs, described in recent revenue procedures and discussed in sources like corporate ruling updates, to obtain advance clarity on certain complex corporate transactions. While that is beyond what most small LLC owners need, it is another reminder that entity choices are long term tax decisions, not one page forms to sign without analysis.

Common Mistakes That Trigger Problems

Many owners focus solely on headline tax savings and ignore practical issues that cause audits, penalties, or missed opportunities. Here are patterns we see repeatedly.

Ignoring State Level Taxes And Fees

California imposes additional taxes and fees on corporations and LLCs beyond federal treatment. For example, an S corporation owes a 1.5 percent franchise tax on its net income with an $800 minimum, while LLCs taxed as partnerships or disregarded entities pay an annual fee based on gross receipts plus the same $800 minimum franchise tax.

Other states have their own quirks, from franchise taxes based on net worth to gross receipts taxes that apply regardless of profit. If you do business in multiple states, you may also face foreign qualification and multi state filing.

This is one reason many growth focused LLC owners end up working with firms that provide ongoing tax planning services rather than just filing help. State and local rules can erode the benefit of a federal strategy if they are not factored in.

Electing S Status Too Early Or Too Late

If you elect S corporation status for an LLC that nets $30,000 of profit, you add payroll costs, extra tax filings, and complexity for very little savings. On the other hand, if you wait until you are making $250,000 to even ask the question, you likely donated tens of thousands to the government unnecessarily in the years before the election.

The election itself has timing rules. In general, to have S status effective for the full tax year, you must file Form 2553 no later than two months and 15 days after the beginning of the tax year, though there are late election relief procedures described in IRS guidance. Missing that window can lock you into a less efficient structure for an additional year.

Mismatching Entity Type With Exit Strategy

If you expect to hold your business indefinitely and extract most value as annual cash flow, S status often aligns best because it keeps taxation simple and tied to your personal return. If you are building something designed to raise capital and sell to a larger buyer, C corporation treatment and thoughtful stock planning might save more tax on the exit than you give up in interim dividends.

The right decision requires modeling all three phases: growth, extraction of profits, and sale or wind down. That modeling is where many business owners either guess or lean on surface level articles, instead of getting scenario driven analysis from a specialized advisor.

What If You Chose The Wrong Status Already

Many clients come to KDA after operating for years under a structure that no longer fits their reality. The good news is that the IRS does allow changes, though not always without friction.

Changing From C Corporation To S Corporation

If your LLC has already elected C corporation status and you now want pass through S treatment, you can file Form 2553 to elect S status if you are an eligible corporation. However, the transition has traps, including built in gains tax on certain appreciated assets if they are sold within a recognition period after the election.

You also need unanimous consent from all shareholders for the S election, and you must ensure you meet shareholder and single class of stock requirements. This is not just a checkbox exercise.

Changing From S Corporation To C Corporation

Going the other direction is usually simpler procedurally but can have longer term consequences. Terminating an S election can happen voluntarily by filing a statement, or automatically if you violate S rules. Once terminated, there are waiting period rules before you can reelect S status without IRS consent, and there may be earnings and profits complications that affect distributions.

Because of these complexities, any move to change the fundamental tax character of your LLC should be modeled with three to five year projections, not just this year’s tax bill.

Will Choosing S Or C Corporation Status Trigger An Audit

Electing S or C status itself does not automatically trigger an audit, but certain behaviors within those structures raise your risk.

Red Flag Alert: Extreme Owner Compensation Patterns

In the S corporation context, the most common audit issue is unreasonable compensation. If you pay yourself a $30,000 salary on $400,000 of profit distributions, you are a tempting target. In a C corporation, the inverse problem exists; if owner salaries are far above market, the IRS can argue that excessive compensation is disguised dividends and disallow deductions.

Grounding your salary decisions in real market data, documenting your role, and revisiting compensation annually is one of the simplest ways to keep your risk manageable.

Red Flag Alert: Sloppy Documentation And Commingling

Regardless of structure, commingling personal and business funds, missing minutes when required, or ignoring basic corporate formalities can weaken your liability protection and draw scrutiny. Keep clean books, separate accounts, and formal records. If your entity is large or complex enough, consider outsourcing bookkeeping and payroll to professionals who work with bookkeeping and payroll systems every day.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

FAQs About S Corp Versus C Corp Choices For LLCs

Is it better to start as an LLC then elect S or C later

For many small business owners, yes. Forming as an LLC at the state level gives you flexibility. You can start with default taxation while profits are modest, then elect S corporation status once income reliably justifies the shift. If you later grow into a structure where C corporation benefits matter, you can elect corporate treatment and adjust from there, subject to the rules discussed above.

Can a single member LLC be taxed as a C corporation directly

Yes. A single member LLC can file Form 8832 to elect to be taxed as a corporation, and then either remain a C corporation or file Form 2553 to elect S status if it qualifies. There is no requirement to have multiple members to choose corporate tax treatment.

Does the choice change how I pay myself

Absolutely. Under default LLC taxation, you generally take draws and pay self employment tax on profit. Under S or C status, you become an employee of your own company, receive W 2 wages, and potentially also receive distributions or dividends. That change affects everything from retirement plan options to how lenders view your income.

What about high net worth investors or multiple businesses

For high net worth owners who hold multiple companies or complex investment structures, the difference between an s corp and a c corp llc sits inside a broader architecture. It may involve holding companies, management entities, or separate real estate LLCs. Those situations almost always benefit from bespoke planning with a firm that offers deeper premium advisory services to coordinate across entities and tax years.

Bottom Line For LLC Owners Weighing S Versus C Status

Your LLC’s tax status is one of the few levers that can change your after tax income by five figures without changing your pricing, your clients, or your workload. For an owner operated business between roughly $80,000 and $600,000 of profit, S corporation status for the LLC is often the default candidate because it balances self employment tax savings, simplicity, and eligibility for the Qualified Business Income deduction.

C corporation treatment for an LLC, on the other hand, is a specialized tool for businesses that plan to raise outside capital, reinvest most profits, or pursue stock based exits where concepts like Qualified Small Business Stock matter. In those cases, accepting double taxation on some profits can be worth the structural and planning advantages.

What you cannot afford is a casual, one size fits all answer. The right choice depends on your profit level, growth plans, state tax exposure, and exit expectations. The nuance inside the difference between an s corp and a c corp llc only shows up when you run the math over several years and coordinate with your personal return.

Book Your Entity Strategy Session

If you are not sure whether your current LLC structure is costing you avoidable tax every year, it is time to find out. In a focused strategy session, our team will review your existing entity, run S corporation and C corporation scenarios with real numbers, and outline a step by step plan to implement changes safely if they make sense. Click here to book your consultation now.

The IRS is not hiding these entity tax rules. You were simply never taught how to use them to your advantage.

For a deeper dive into S corporation planning in California, explore our comprehensive S corporation strategy guide once you have clarity on whether S status fits your LLC.