Many S corporation owners assume that if they ever switch to C corporation status, their accumulated tax benefits will simply follow them. The reality around the accumulated adjustments account is harsher. If you mishandle that balance when your S corporation becomes a C corporation, you can lock away years of previously taxed earnings and potentially create double taxation you never planned for.

For owners with meaningful profits, the **s-corp conversion to c-corp distribute out aaa balance** question is not academic. It is a six and sometimes seven figure decision that sits at the intersection of entity choice, shareholder basis, and distribution ordering rules. Getting it right can be the difference between pulling cash out at effectively zero additional federal tax or paying a second layer of tax at C corporation and dividend rates later.

Quick answer

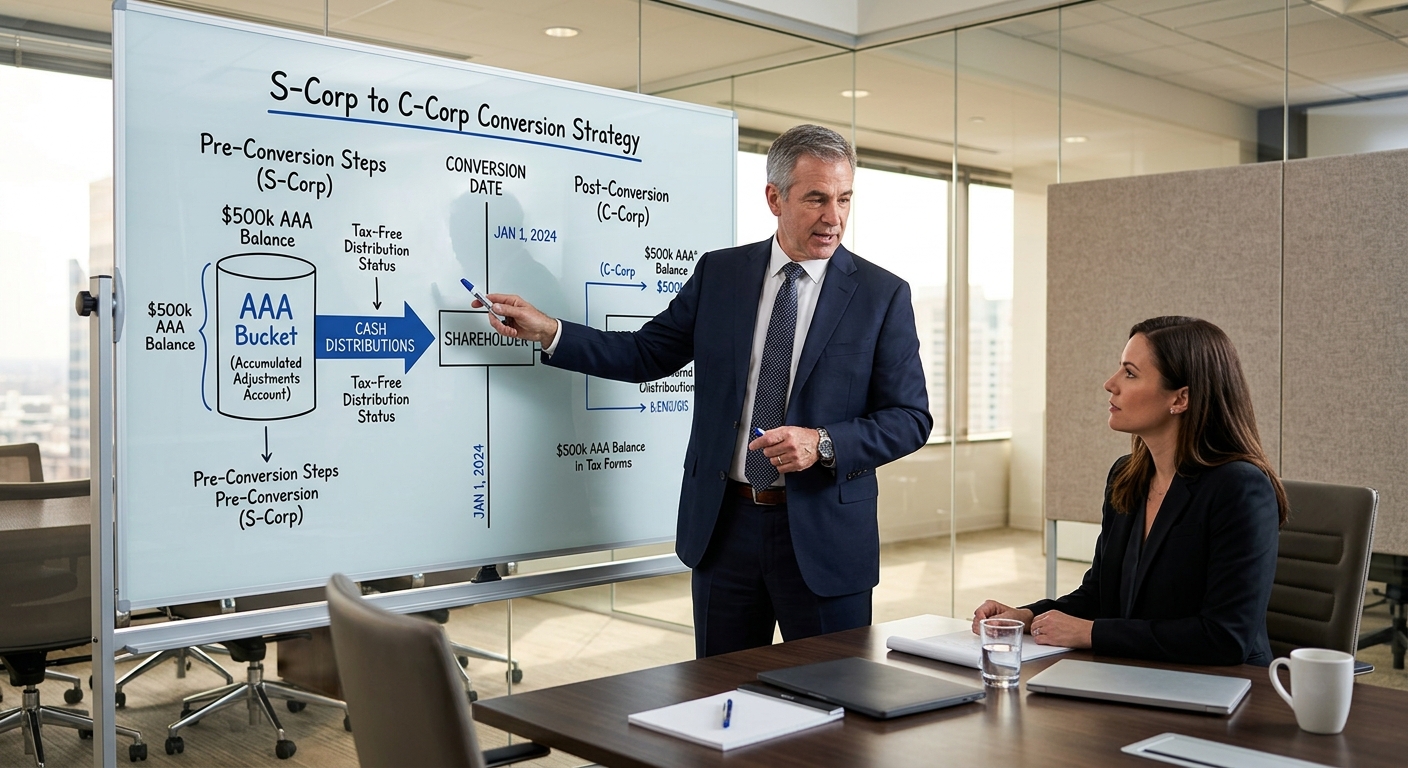

In plain English, when an S corporation with a positive accumulated adjustments account (AAA) converts to a C corporation, you generally want to distribute as much of that AAA as you can while the company is still an S corporation. Distributions from AAA, to the extent of a shareholder’s stock basis, typically come out tax free because the income was already taxed on prior S corporation returns. If you leave AAA trapped in the entity at the moment of conversion, it becomes part of the C corporation earnings and profits stack and future cash withdrawals are exposed to dividend treatment and possible double tax. The planning window is the tax year before and the short year including the revocation date, and it requires careful coordination with the S corporation distribution ordering rules in IRS Form 1120-S instructions and the underlying statutes.

How the AAA balance really works when your S corporation converts

Before you can design a smart path from S status to C status, you need a working understanding of the accumulated adjustments account. AAA is a corporate level tracking account that measures the portion of S corporation earnings that have already been taxed to shareholders but not yet distributed. Think of it as the pool that allows you to pull money out without triggering tax a second time, as long as each owner has enough stock basis to absorb the distributions.

AAA is not the same as retained earnings under GAAP, and it is not the same as your cash balance. You can have a positive AAA with very little cash on hand, or you can have a negative AAA in a business that is cash rich. The account is adjusted annually by S corporation income, losses, separately stated items, and prior year distributions under the ordering rules described in IRS Publication 542 and related guidance. For a multi shareholder business, AAA is tracked at the entity level, while stock basis is tracked for each owner individually.

When you plan a s-corp conversion to c-corp distribute out aaa balance strategy, the mechanics matter. In the year you revoke S status, you effectively have two short tax years. The first short year ends the day before the revocation is effective and is treated as an S year. The second short year begins on the revocation date and is treated as a C year. AAA is computed and distributions are tested under S rules in that first short year. Once you cross into the second short year, distributions begin to look like C corporation dividends to the extent of earnings and profits.

That timing split creates the window for owners to deliberately drain AAA while the S rules still apply. Done correctly, this process lets you harvest tax free returns of previously taxed S income, rather than leaving those dollars to become part of C corporation earnings.

Why owners consider converting despite AAA complications

It is fair to ask why any rational owner with a large AAA would voluntarily abandon S corporation status. There are several common drivers. A frequent one is the need to raise institutional equity. Venture funds, private equity sponsors, and some strategic buyers prefer or require C corporation stock due to investor eligibility rules and structural preferences. Another is the desire to accumulate earnings for a large reinvestment or acquisition where C corporation rates and reinvestment mechanics can be more attractive.

For some high growth companies in California and other high tax states, the C corporation framework can also interact more efficiently with state level apportionment and credit regimes, particularly where multiple entities and jurisdictions are involved. Finally, certain exit strategies such as qualifying for federal small business stock exclusions under Section 1202 usually require C corporation status and specific holding period rules. All of these can outweigh the annual pass through tax simplicity that made the S election appealing in the first place.

The challenge is that if you pursue these goals while ignoring the s-corp conversion to c-corp distribute out aaa balance mechanics, you can burn a hole in your long term tax picture. Owners often focus on the capital gain they hope to realize in a future stock sale but fail to evaluate the immediate cash they could extract on a tax efficient basis before making the switch.

Designing a pre conversion distribution plan

The practical question is how to structure distributions so you maximize the use of AAA while still honoring the S corporation rules that protect you from reclassification or audit trouble. The starting point is a detailed reconciliation of AAA and each shareholder’s basis. That usually means reconstructing several years of K 1 activity, capital contribution history, prior distributions, and any built in gains tax adjustments under Section 1374. Many closely held companies discover gaps or errors in that history, so a cleanup phase is sometimes necessary before you even consider writing checks.

Once you have a defensible AAA calculation, you can layer in cash flow realities. Suppose a consulting S corporation has three equal owners, $1.2 million of AAA, and $800,000 of cash that is not needed for working capital. All three owners have stock basis greater than $400,000. If the company distributes the full $800,000 before revoking the S election, each owner receives about $266,667. That distribution reduces AAA by the same amount and is generally treated as a tax free return of basis, since the earnings were already picked up on prior S returns.

If, by contrast, the company converts first and then pays that same $800,000 during a C year, the tax result looks very different. If the business is profitable, those dollars are likely paid out of C corporation earnings and profits. Each owner is now staring at dividend income taxed at their individual qualified dividend rate on top of any corporate level tax. With a 21 percent federal corporate rate and a 15 to 20 percent dividend rate stacked on high income individuals, the effective combined tax cost can approach or exceed 40 percent.

In some cases, distributing the entire AAA balance is not realistic because the business needs to retain a significant portion of its cash. That is where a more nuanced s-corp conversion to c-corp distribute out aaa balance strategy comes in. You might elect to distribute only the portion of AAA that can be funded from excess working capital while planning to use future profits to rebuild capital post conversion. The key is that the decision is deliberate rather than accidental.

What happens to AAA if you do nothing

Owners often ask whether AAA simply disappears on the effective date of C status, or whether it sits in a special bucket that can be accessed later. Under the general rules, once S status terminates, the AAA account is no longer relevant for distribution ordering. From that date forward, distributions are governed by C corporation earnings and profits concepts. There is no favored layer of S era earnings that you can reach into later and pull out tax free as if the S election still existed.

To make the point concrete, imagine a manufacturing S corporation with $2 million of AAA and $500,000 of other C corporation earnings and profits from a prior C period. If the business pays no distributions before converting, and then later issues a $1 million dividend while it is a C corporation, shareholders will report that amount as dividend income to the extent of cumulative earnings and profits. The historical AAA will not shield them. The tax cost of inaction can easily run into the hundreds of thousands of dollars for mid sized privately held companies and far more for larger ones.

There are narrow exceptions and transition rules in the Code for corporations that oscillate between S and C status, but they are tightly constrained and rarely justify relying on inaction as a primary strategy. The safer and more controllable route is to deliberately plan any s-corp conversion to c-corp distribute out aaa balance approach in advance so that you have clear documentation around timing, amounts, and shareholder level consequences.

KDA case study: business owner cleans up AAA before a growth round

Consider a three owner California software development firm that has operated as an S corporation for a decade. The business reports stable profits in the $1.5 to $2 million range and has accumulated an AAA balance of roughly $3.8 million. The company is preparing to raise $10 million from an institutional investor who requires a clean C corporation structure at closing.

When the owners came to our team, they were planning to simply file the revocation, flip to C status, and let the cash stay in the entity to impress investors with a strong balance sheet. We walked them through the mathematics of a more deliberate s-corp conversion to c-corp distribute out aaa balance plan. After reconstructing shareholder basis and confirming that each founder had sufficient basis to absorb large distributions, we recommended a pre closing distribution of $2.4 million paid equally to the three owners.

Because the distribution was made in the S short year and was covered by both AAA and basis, it was largely tax free to the owners at the time they received it. At their combined marginal rates, that effectively avoided more than $800,000 of future dividend level tax they would have incurred if the same dollars had been paid out post conversion. They still closed their round on schedule, the investor received C corporation stock as requested, and the company rebuilt working capital with fresh equity capital rather than old retained earnings.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Key red flags and common mistakes around AAA at conversion

One of the biggest errors we see is assuming that book retained earnings and AAA are interchangeable. If your internal financials show $5 million of retained earnings and your tax workpapers show $2 million of AAA, you do not have $5 million of S corporation earnings to distribute with pass through treatment. Over distributions that exceed AAA and stock basis can become taxable capital gains or be recharacterized as wages or loans if the IRS is not persuaded by your documentation.

Another recurring mistake is ignoring shareholder level basis disparities. If one founder has repeatedly advanced loans to the corporation or left earnings in the business while others have taken distributions, that founder may have a much higher basis cushion. In a pre conversion drain down of AAA, that disparity can be used strategically. You might direct a larger share of distributions toward the high basis shareholder to minimize overall tax cost and later rebalance economics through stock recapitalizations or side agreements, as long as you preserve the single class of stock requirement prior to revocation.

Red flag alert: large distributions close to the revocation date with thin or incomplete AAA and basis workpapers can invite scrutiny. If the IRS examines the short S year and finds that you misapplied the ordering rules or failed to consider prior year adjustments, they can reclassify some or all of the payments as taxable dividends or wages. Solid schedules that reconcile AAA, earnings and profits, and each owner’s basis year by year are your best defense.

How this planning interacts with shareholder level tax projections

The math around s-corp conversion to c-corp distribute out aaa balance strategy is not only a corporate exercise. It also lives on the shareholders’ individual returns. Even if a distribution is technically tax free as a return of basis, it can interact with other items on the return such as passive activity losses, net investment income tax thresholds, and state level surtaxes.

For example, a high income shareholder in California who receives a $700,000 tax free distribution shortly before conversion might then decide to reinvest a portion into a real estate partnership that generates passive losses. Understanding how that capital move affects their overall tax picture requires an integrated view across entities. Our tax planning services often layer this entity level work with personal return modeling to avoid surprise results in April.

If you are an owner operator rather than a passive investor, there are payroll and reasonable compensation issues to keep aligned as well. The IRS expects S corporation owners who work in the business to receive reasonable salaries before taking large distributions. When those distributions spike in the final S short year, your compensation policies should be reviewed to make sure they continue to make sense and do not invite a reclassification argument that turns tax favored AAA distributions into wage income subject to employment taxes.

Where this fits for different taxpayer personas

For W 2 employees who hold minority stakes in S corporations, the s-corp conversion to c-corp distribute out aaa balance issue usually arises when a company approaches an IPO or large private equity recapitalization. In those cases, the distribution decisions may be largely controlled by a board, but understanding the AAA mechanics can still help you assess the after tax impact of liquidity events.

For 1099 contractors who have built their practice inside a wholly owned S corporation, the conversion conversation is less common but can come up if they bring in outside capital or aim to roll into a larger corporate platform. For these owners, the dollar amounts may be smaller, but the relative impact of a poorly planned conversion can still be significant, often absorbing a full year or more of take home profits.

For established business owners running multi owner S corporations, AAA management is a core governance topic rather than a one time decision. The board should periodically review whether the company is deliberately building AAA as a future distribution pool or whether a move toward C status is likely in the medium term, which could change the incentive to distribute more aggressively today.

Real estate investors sometimes operate rental portfolios through S corporations, although LLCs taxed as partnerships are usually more flexible. Where they do, the AAA issues discussed here can intersect with large depreciation driven losses and timing differences in ways that require custom modeling.

Modeling the numbers: how much tax is really at stake

To make this strategy concrete, it helps to model side by side outcomes. Consider an S corporation with $4 million of AAA, all of which is supported by shareholder basis. The owners are evaluating whether to distribute $3 million before conversion or leave those funds in the entity and distribute them later as a C corporation dividend.

Scenario one: the company distributes $3 million in the final S short year, with each of three equal owners receiving $1 million. The distributions are covered by AAA and basis, so they are treated as tax free returns of capital. There is no immediate federal income tax. The owners simply reduce their stock basis by $1 million each.

Scenario two: the owners convert to C status without any pre conversion distributions and later pay the same $3 million as a C corporation dividend funded out of taxable earnings. Assuming a 21 percent federal corporate rate and a 20 percent individual dividend rate at the shareholder level, the combined federal tax cost on those earnings can be roughly $1.02 million. That is more than one third of the cash flow lost to tax cost simply because the timing and characterization were left to default treatment.

For owners who want to quantify similar planning opportunities in their own situation, running numbers through a structured model helps. It is the same logic behind using a small business tax calculator when you are evaluating alternative entity scenarios or cash distribution policies.

Practical steps to execute a clean conversion

Once your team decides that the strategic reasons for becoming a C corporation outweigh continuing as an S corporation, the execution process should be handled with the same seriousness as any major transaction. The first step is to map the revocation date relative to your fiscal year and any planned cash movements. Most owners align the effective date with the start of a month or quarter, but the tax law looks to specific calendar dates, not business cycles.

Next, coordinate with your advisors to build a written plan describing the intended s-corp conversion to c-corp distribute out aaa balance approach. That plan usually covers the target AAA distribution amount, the anticipated dates of distribution, and the expected shareholder level consequences. It also should address how reasonable compensation will be maintained in the final S short year and how any shareholder loans or prior C corporation earnings will be treated.

From there, your tax team will prepare the final S corporation return on Form 1120 S for the short year, including the necessary schedules to support AAA and basis balances. An S revocation statement will be filed with the IRS, and state level elections or notifications may be required depending on your jurisdiction. In California, coordination with the Franchise Tax Board is essential so that entity classification and estimated payment expectations remain aligned. For complex or high dollar situations, some owners also engage premium advisory services that integrate tax, legal, and transaction advisory workstreams.

Will this draw extra IRS attention

Any time a closely held business pays large distributions in proximity to a significant tax election change, owners worry about audit risk. The IRS does not automatically view a well documented s-corp conversion to c-corp distribute out aaa balance strategy as abusive. In fact, the distribution ordering rules and AAA regulations are designed with this pattern in mind. Problems arise when documentation is weak, economic arrangements look inconsistent with the single class of stock requirement, or distributions are coupled with aggressive loss allocations that lack economic substance.

Red flag alert: if your AAA and basis workpapers exist only as rough spreadsheet sketches or are reconstructed hastily in the weeks before conversion, you are creating risk. Clean, year by year reconciliations that tie to filed K 1s and prior tax returns are what convince an agent that your approach is grounded in the Code, not opportunistic guesswork.

According to IRS statistical data, small business and pass through entity examinations remain a relatively small percentage of total filings, but when they do occur, distribution classifications are a common focus area. Solid preparation on the AAA question does not eliminate audit risk, but it does sharply improve your odds of a favorable outcome and a faster resolution if your file is selected for review.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently asked questions

Can we partially drain AAA and still benefit

Yes. You do not need to zero out AAA for this planning to add value. Even a partial pre conversion distribution that harvests, say, half of the available AAA can dramatically reduce future dividend exposure. The right mix depends on cash needs, lender covenants, and investor expectations.

What if some shareholders do not want cash now

In multi owner situations, it is common for some shareholders to prefer retaining capital in the business while others want liquidity. As long as you maintain a single class of stock before revocation, you generally need to pay pro rata distributions. That said, shareholders who receive cash can contribute a portion back via new paid in capital mechanics if they choose, effectively re investing on an after tax basis.

Does AAA matter if my S corporation has losses

If your S corporation has an overall deficit in AAA at the time of conversion, there is no positive pool of previously taxed earnings to harvest. In that scenario, the focus shifts toward basis utilization and loss carryforwards rather than pre conversion distributions. The s-corp conversion to c-corp distribute out aaa balance question is most powerful when historical profits have built up a strong AAA.

Is there ever a reason not to distribute AAA before conversion

Yes. Cash flow constraints, lender covenants, or investor negotiations may make large pre conversion distributions impractical. There can also be situations where the owners’ personal tax positions favor deferral or where maintaining a thicker balance sheet is strategically more valuable than the immediate tax savings. The point is not that you must always drain AAA but that you should make the choice intentionally with full information.

Bottom line and next steps

If you are even considering a move from S status to C status in the next two to three years, do not wait until the revocation paperwork is on your desk to think about AAA. A disciplined s-corp conversion to c-corp distribute out aaa balance strategy can convert years of already taxed S corporation income into tax efficient shareholder liquidity and prevent those dollars from being swept into the C corporation earnings and profits stack.

This information is current as of 5/22/2026. Tax laws change frequently. Verify updates with the IRS or your state tax authority if you are reading this at a later date, and remember that California rules often layer on top of federal law in ways that deserve separate attention.

Book your tax strategy session

If you are unsure how much AAA is sitting on your S corporation’s books or what a future conversion could cost you in real dollars, it is time to get clarity. Our team regularly helps owners model s-corp conversion to c-corp distribute out aaa balance outcomes, structure pre conversion distributions, and coordinate with legal counsel and investors so that tax strategy supports your growth plans instead of fighting them. Click here to book your consultation now.

The IRS is not hiding these rules; most owners simply have not been shown how to use them before it is too late.