This blog post explores **s corp to c corp conversion aaa** and what it really means for business owners who are trying to clean up years of tax decisions without accidentally lighting a match to their after tax cash. If you own an S corporation that has grown, added investors, or is running into the limitations of pass through status, the idea of flipping to a C corporation is going to show up in conversations with attorneys, bankers, or potential buyers.

Quick Answer

Switching from an S corporation to a C corporation is legally simple but tax heavy. You need to understand how your accumulated adjustments account, or AAA, interacts with retained earnings, distributions, and future double taxation. Done correctly with a plan, you can unlock growth, clean up your balance sheet, and still extract old S corp profits at favorable tax rates. Done blindly, you can trap hundreds of thousands of dollars of previously taxed income inside a C corporation and pay tax on it twice.

Why Owners Consider S Corp To C Corp Conversion

Most owners do not wake up one morning and decide to abandon S status for fun. The pressure usually comes from one of five directions:

- Outside investors who only invest in C corporations

- Plans to issue stock options or multiple share classes

- Bank or lender covenants that push toward C corp financial reporting

- Desire to retain earnings at the corporate level for expansion

- Mistaken belief that C corp tax rates are always lower

Each of those reasons may be valid, but each has a different tax footprint. For example, a professional services firm in California netting $600,000 per year may think the flat 21 percent federal C corp rate looks attractive compared to the top individual bracket. That same owner is often ignoring the second layer of tax when profits are paid out as dividends, plus the 1.5 percent California franchise tax on C corps compared with the minimum tax on S corps.

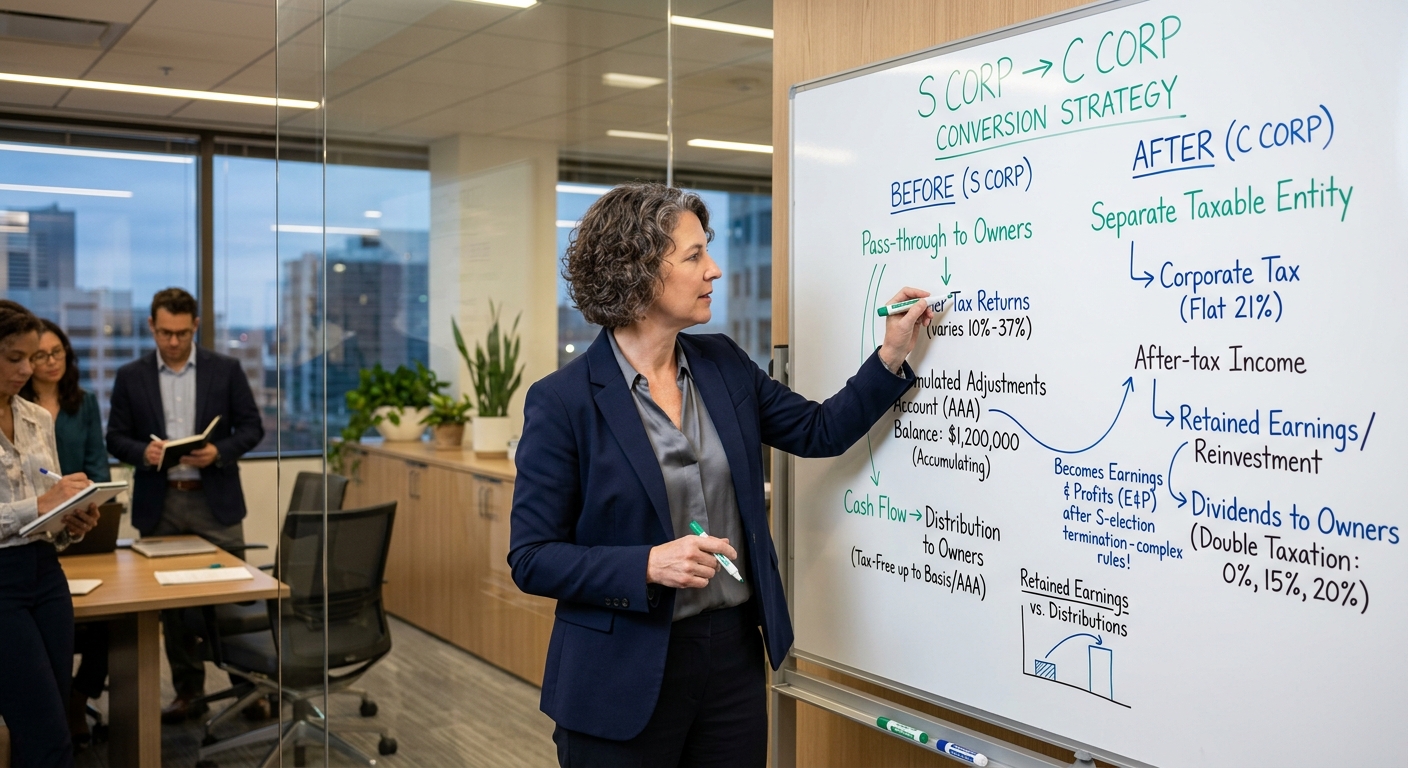

How AAA Fits Into The Picture

The accumulated adjustments account tracks the S corporation earnings that have already been taxed to shareholders but have not yet been distributed. In plain English, AAA is your running total of profits that you have already paid tax on personally. As long as the corporation is an S corp, you can usually distribute those dollars without paying another layer of federal income tax, subject to basis rules and other limits. When you convert to a C corporation, that safety valve begins to close.

Federal Versus California Consequences

At the federal level, S corporations are governed by Subchapter S of the Internal Revenue Code, and C corps fall under Subchapter C. IRS guidance for C corporations appears in resources like IRS Publication 542, while S elections are made using Form 2553. California follows federal entity elections but inserts its own franchise tax structure, and many business owners underestimate the combined state plus federal burden after a conversion.

How S Corp To C Corp Conversion Actually Works

Mechanically, revoking S status is not complicated. Strategically, it is.

Step 1: Revoke The S Election

To terminate S status, shareholders file a written revocation with the IRS Service Center where the original S election was filed. The revocation needs signatures from shareholders owning more than 50 percent of the shares. If filed by the 15th day of the third month of the tax year, it is effective on the first day of that year. Otherwise, it is effective the following year. After revocation, the entity files Form 1120, the C corporation return, instead of Form 1120S.

Step 2: Identify Your AAA And Other Equity Layers

Before you pull the plug, you need a clear picture of the equity section of your balance sheet. That means separately calculating:

- Paid in capital and additional paid in capital

- Accumulated adjustments account

- Other adjustments account if applicable

- Accumulated earnings and profits from any prior C corp years

Your CPA should reconcile AAA under the rules in the Form 1120S instructions. If you have $750,000 sitting in AAA and $50,000 of accumulated C corp earnings and profits, the ordering rules for distributions before and after conversion matter a lot.

Step 3: Model Distributions Before And After Conversion

Owners often focus on the tax rate of the entity and ignore the path of cash to their personal returns. That is where AAA is powerful. While you are still an S corporation, distributions generally come out of AAA first. If shareholder stock basis is high enough, those distributions are typically non taxable returns of already taxed income.

Imagine your S corporation in California has three equal shareholders and $900,000 of AAA. You are thinking about converting to a C corporation on January 1 of next year. Before doing that, you model a $600,000 distribution this year, or $200,000 per shareholder. If each shareholder has sufficient basis, that distribution may be federal income tax free, and California will not tax it again either because it reflects income already reported in past years.

If you skip the planning and convert immediately, you can still access AAA after conversion under special ordering rules, but if you do not track and document it correctly, those same distributions can be mischaracterized as taxable dividends from C corp earnings and profits. That is the core risk behind any s corp to c corp conversion aaa discussion.

Step 4: Address Built In Gains And Asset Appreciation

When a C corporation elects S status, the built in gains tax under section 1374 can create a corporate level tax on certain appreciated assets sold within a recognition period. When you move the other way, from S to C, you do not trigger built in gains tax the same way, but you do need to be mindful of the embedded appreciation in your assets and how the future sale will be taxed. After conversion, asset sales reside fully inside a C corporation, meaning the gain is taxed at the corporate level and then potentially again when proceeds are distributed.

Common Mistakes That Destroy AAA Value

From a strategist perspective, the biggest risk is not the act of revoking S status. It is mismanaging AAA before and after the switch.

Treating AAA As A Line Item Instead Of A Planning Tool

AAA is not just an accounting tally. It represents dollars you can usually pull from the corporation without a second federal tax hit. When owners rush into a C corp conversion because an investor or attorney demands it, they often leave that reservoir untouched. If you have $1,000,000 in AAA and you move to C status with no plan, you may end up paying 21 percent corporate tax on future earnings and then dividend rates when you finally distribute cash, while a large portion of that cash could have come out previously with no additional federal income tax.

Ignoring Reasonable Compensation And Payroll Taxes

Some owners believe they can shift from S to C, pay themselves entirely in dividends, and avoid payroll taxes. That is not how the IRS views it. Whether you operate as an S corp or a C corp, paying shareholder employees zero salary while issuing large distributions is a red flag. IRS guidance on corporate compensation appears in places like IRS Publication 535, which discusses reasonable compensation and deductible business expenses. In practice, you need a salary that aligns with market data before you think about dividends or large AAA distributions.

Letting State Taxes Sneak Up On You

For California based corporations, the move from S to C amplifies the importance of state tax modeling. C corporations pay 8.84 percent California tax on net income, while S corporations generally pay 1.5 percent on net income, with shareholders paying tax on their share at individual rates. When you combine that with the federal changes, the net difference can be tens of thousands per year on a business clearing $500,000 in profit. That is why serious planning often includes professional tax planning services instead of generic spreadsheet math.

Red Flag Alert: Will This Trigger An Audit

The IRS does not automatically audit a company because it revokes S status. Audits are triggered by mismatches, inconsistent reporting, and aggressive positions without support. With that said, there are a few patterns that invite scrutiny around a s corp to c corp conversion aaa plan.

Large Distributions In The Final S Year

Pulling a seven figure distribution in the last S year and claiming it is entirely from AAA is legitimate only if the math and documentation support it. Your stock basis must be high enough to absorb the distribution, and prior year income and distributions must reconcile under the AAA rules in the Form 1120S instructions. If the numbers are sloppy, expect questions.

Inconsistent shareholder basis schedules

The IRS knows that many small corporations do not maintain proper basis schedules. If you claim that a $400,000 distribution is tax free because of AAA, you must be ready to prove that basis. That means tracking contributions, income, losses, and prior distributions at the shareholder level every year.

What If You Already Misreported Distributions

If you have been treating every distribution as tax free without understanding AAA or basis, you may already have exposure. Cleaning that up should be part of the conversion project. Amended returns, corrected K 1s, and better documentation may reduce penalties and make the future C corp returns less risky.

KDA Case Study: California S Corp Owner Restructures For Investor Round

Consider Maria, who owns a marketing agency in Los Angeles taxed as an S corporation. Her firm nets about $750,000 per year, and over ten years she has built up $1.2 million in AAA and solid shareholder basis. A venture backed fund wants to invest and insists on a C corporation structure so it can receive preferred shares and standard venture protections. Maria is tempted to file the revocation notice immediately to close the deal.

KDA stepped in before she signed. First, we rebuilt ten years of AAA and basis schedules to confirm that $1.2 million figure. We then designed a pre conversion distribution plan that pulled $800,000 out to Maria in the last S year, documented as a return of already taxed income. Because her basis supported it, that distribution did not create additional federal income tax. We also modeled compensation as a C corp owner, setting a reasonable salary of $240,000 and projected dividend patterns to satisfy both Maria and the investors.

After conversion, Maria still had $400,000 of AAA available under the post termination rules, but the bulk of her already taxed S corp profits had been extracted at favorable rates. In the first two years, we estimate she avoided roughly $140,000 in combined federal and California taxes compared to a no plan conversion. The investors still received the C corporation structure they wanted, and Maria kept more of the cash she had already earned. Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How AAA Distributions Work After Conversion

One of the most misunderstood areas is what happens to AAA once you are officially a C corporation. Many owners think AAA disappears on the effective date of the revocation. It does not. Instead, special ordering rules apply to distributions in post termination years.

The Post Termination Transition Period

For a limited period after S status ends, usually one year, the corporation can still treat certain distributions as coming from AAA first, before earnings and profits, if specific conditions are met. That window is called the post termination transition period. If you do not know it exists, you will not use it, and your accountant may default to dividend treatment out of C corp earnings and profits.

Ordering Rules And Elections

Distributions in the post termination transition period follow ordering rules that consider AAA, accumulated earnings and profits, and other accounts. In some situations, you can even elect to treat distributions as coming out of earnings and profits first to preserve AAA for later or for different shareholders. These elections are technical and require close reading of the code and regulations, but they are powerful levers when structured alongside investor requirements and buyout terms.

Practical Example

Suppose your corporation converts to C status on January 1 and has:

- $600,000 in AAA

- $100,000 in accumulated earnings and profits

- $300,000 of current year C corp earnings

During the post termination transition period, the corporation distributes $500,000. If structured correctly, much of that distribution can still be treated as coming from AAA and thus non taxable to the extent of shareholder basis, rather than fully taxed as dividends. That difference can easily be six figures for high income shareholders in California once you stack federal and state dividend taxes.

What If You Decide To Go Back To S Status

Owners sometimes discover that C status is less attractive than it looked on paper. Maybe profits fall, investor plans change, or the second layer of tax bites harder than expected. The code does allow a corporation to reelect S status after a period, but it is not as simple as toggling a switch.

The Five Year Waiting Rule

Generally, once a corporation revokes S status, it cannot reelect S for five tax years without IRS consent. That means a hasty decision today can lock you into C corp treatment for half a decade. During that period, all earnings are taxed at corporate rates and then again on distribution, with no fresh AAA building up.

Impact On Future AAA

If you eventually reelect S status, you start building a new AAA from the date of the election. The old AAA and earnings and profits accounts still matter, but you are effectively running two sets of histories. Getting those wrong on future distributions can lead to messy audits years down the line.

Will S Corp To C Corp Conversion Lower Your Taxes

For some businesses, yes. For many, no. The only intelligent answer comes from modeling your specific facts.

Who Might Benefit

- Companies planning to reinvest profits for many years without large shareholder distributions

- Businesses targeting institutional or foreign investors limited to C corps

- High growth startups where qualified small business stock rules and long term exit planning matter more than short term cash

A technology founder in San Diego projecting $2 million in annual profits that will largely stay inside the company might accept the corporate tax rate and double tax risk in exchange for investor capital and potential section 1202 benefits at exit. Even in that situation, it is vital to understand how pre conversion AAA, if any, will be used or effectively abandoned.

Who Usually Does Not Benefit

- Professional service firms distributing most profits annually

- Closely held family businesses with no outside investors on the horizon

- Owners who rely on distributions for personal living expenses

If your S corporation in California distributes $400,000 each year to the shareholder group and you expect that pattern to continue, voluntarily inviting double taxation rarely makes sense. For many self employed professionals, it is better to refine S corp salary, retirement plans, and fringe benefit strategies than to jump into C corp territory. Those questions are at the heart of what we tackle in our broader S corporation tax strategy guide for California owners.

What About Basis, Debt, And Losses

AAA is not the only technical piece that matters during a s corp to c corp conversion aaa review. Shareholder basis, corporate level debt, and suspended losses also deserve attention.

Basis And Suspended Losses

In an S corporation, your ability to deduct losses is limited by your stock and debt basis. If you have suspended losses because basis was insufficient in prior years, revoking S status does not magically free those up. In fact, you may forever lose the ability to use them if you are not careful about final year planning. Clarifying basis before conversion can create room for more AAA distributions or final year loss utilization.

Corporate Debt And Guarantees

Many small S corporations rely on shareholder guarantees or loans to support bank financing. Those arrangements affect basis and loss limits. After converting to a C corporation, basis rules do not work the same way on the shareholder side, but the old history still matters for how distributions and redemptions are taxed. Cleaning up intercompany loans and documenting guarantees before conversion reduces future confusion.

Pro Tip

Before you sign a revocation letter, have a strategist walk you through a side by side comparison using your real numbers. That means modeling three to five years of projected profit, salary, distributions, and entity level taxes under both S and C status, with AAA planning built into the S side. The tax delta often surprises owners who were told that a flat corporate rate automatically wins.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About S To C Conversion And AAA

Will I owe tax when I convert from S to C

The act of revoking S status itself does not usually trigger a separate federal tax. The real tax consequences show up in how you handle distributions, built in gains, and earnings before and after conversion. Large final year distributions from AAA can be tax efficient if basis and documentation support them, but every situation is different.

Does AAA disappear when I become a C corporation

No. AAA carries over, and during the post termination transition period you can still use it to support more favorable distribution treatment. After that window, AAA does not grow further, and the presence of earnings and profits complicates the ordering. That is why detailed schedules matter.

Can I convert mid year

Yes, but mid year conversions are more complex because you split the year between S and C status and file short period returns. Income, deductions, and distributions must be allocated correctly between the S period and C period. That often increases professional fees and audit risk without adding much benefit compared with timing the conversion at year start.

Is a C corp always bad for small California businesses

No. For some companies, especially those with scalable products, venture ambitions, and long reinvestment horizons, C status is the right tool. The mistake is assuming that the statutory 21 percent corporate rate tells the whole story. When you add California, payroll, and second layer taxes, the effective rate gap versus an optimized S corp can shrink or even reverse.

Bottom Line

If you are even casually considering a s corp to c corp conversion aaa strategy, you are in territory where rules, elections, and timing decisions can easily move six figures on a three to five year horizon. The conversion itself may be a single letter to the IRS, but the run up and the aftermath are where money is made or lost. You need a plan for AAA, basis, compensation, state taxes, and investor realities before you change anything on paper.

Book Your Tax Strategy Session

If you want to know whether an S to C conversion will actually save or cost you money, and how to harvest your AAA safely before or after a change, it is time to get a customized model instead of guesses. Book a personalized consultation with our strategy team and walk away with a clear, written game plan for your entity structure in California. Click here to book your consultation now.

This information is current as of 7/14/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.