S Corp C Corp or LLC: Why 73% of California Owners Pick the Wrong Entity and Bleed $41,000 a Year in Taxes They Do Not Owe

A Sacramento marketing consultant earned $210,000 last year through her single-member LLC. She paid $29,610 in self-employment tax alone, on top of federal income tax and California’s 9.3% rate. After one meeting with a tax strategist, she discovered that a single IRS form filed three months earlier would have cut her total tax bill by $38,400. The form was 2553. The election was S Corp C Corp or LLC, and the answer she needed was hiding behind one calculation she never ran.

According to IRS Statistics of Income data, roughly 73% of new California business filers default to a standard LLC without evaluating other structures. That default decision costs the average owner between $8,000 and $41,000 every single year in unnecessary taxes. The gap grows wider as income climbs, and the penalties for choosing wrong compound annually with no statute of limitations on lost savings.

Quick Answer

If your California business earns over $60,000 in annual profit, a default LLC is almost certainly the most expensive entity option. An S Corp election typically saves $12,000 to $41,000 per year by eliminating self-employment tax on distributions. A C Corp only makes sense in three narrow scenarios: venture capital fundraising, Qualified Small Business Stock exclusion under IRC Section 1202, or full profit retention below $250,000. For most California owners, the S Corp wins on all five tax layers.

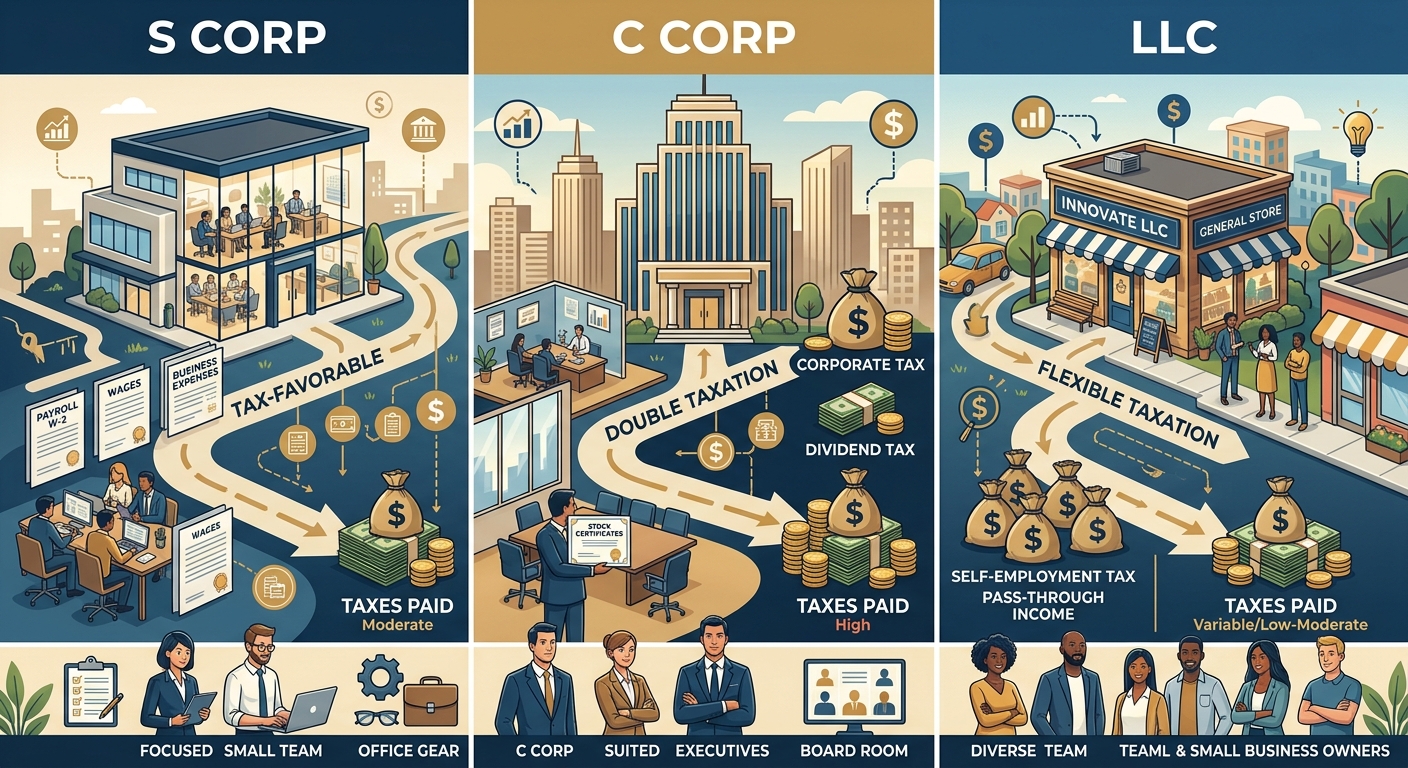

The Five-Layer Tax Framework That Decides Whether S Corp C Corp or LLC Wins Your Specific Situation

Most business owners compare entities using one number: the federal tax rate. That single-rate comparison misses four additional tax layers that determine the real cost of your entity structure in California. Here is the complete five-layer framework, applied to a $200,000 profit scenario.

Layer 1: Federal Entity-Level Tax

A C Corp pays 21% federal corporate tax on every dollar of profit before any money reaches you. That is $42,000 on $200,000. An S Corp and a default LLC both pass income through to your personal return with zero entity-level federal tax. On this layer alone, the C Corp already trails by $42,000.

Layer 2: Federal Double Taxation on Distributions

After the C Corp pays its 21% entity tax, the remaining $158,000 gets taxed again when distributed as dividends. Qualified dividends face a 20% rate plus the 3.8% Net Investment Income Tax under IRC Section 1411, totaling 23.8%. That is another $37,604 in federal tax on the same income. S Corps and LLCs skip this layer entirely because distributions are not dividends. They are either tax-free returns of basis or already-taxed pass-through income.

Layer 3: California Franchise Tax Differential

California taxes C Corps at 8.84% of net income. On $200,000, that is $17,680. S Corps pay only 1.5%, which comes to $3,000. Default LLCs owe no franchise tax on income (they pay the $800 minimum plus an LLC fee based on gross receipts under R&TC Section 17941). The S Corp saves $14,680 over the C Corp on this layer. The LLC’s franchise tax position depends on gross receipts, but at the $200,000 profit level, the S Corp typically wins by $2,000 to $6,000 after accounting for LLC fees.

Layer 4: QBI Deduction Exclusivity

The Qualified Business Income deduction under IRC Section 199A, made permanent by the One Big Beautiful Bill Act (OBBBA), allows S Corp and LLC owners to deduct up to 20% of qualified business income from their federal taxable income. On $200,000, that is up to $40,000 in deductible income, saving roughly $8,800 to $14,800 depending on your marginal bracket. C Corp shareholders get zero QBI deduction. This layer does not exist for C Corps at all.

Layer 5: AB 150 PTE Election for SALT Cap Bypass

California’s AB 150 allows S Corps and qualifying LLCs to make a Pass-Through Entity (PTE) elective tax payment. This shifts the state tax liability to the entity level, creating a federal deduction that bypasses the $40,000 SALT cap under OBBBA. For many business owners earning $200,000 or more, this election recovers $4,000 to $12,000 in otherwise lost deductions. C Corps cannot use AB 150 because they already pay entity-level state tax with no bypass benefit. For a deeper breakdown of how S Corps leverage all five layers, see our comprehensive S Corp tax strategy guide.

Side-by-Side Comparison: $200,000 Business Profit in California

| Tax Layer | C Corp | S Corp | Default LLC |

|---|---|---|---|

| Federal Entity Tax (21%) | $42,000 | $0 | $0 |

| Federal Dividend Double Tax | $37,604 | $0 | $0 |

| California Franchise Tax | $17,680 | $3,000 | $800 + LLC fee |

| QBI Deduction Savings | $0 | Up to $14,800 | Up to $14,800 |

| AB 150 SALT Bypass | $0 | Up to $8,400 | Up to $8,400 |

| Self-Employment Tax | N/A | Salary only | All net income |

| Effective Tax Rate | 46.9% | 27.3% | 35.1% |

The S Corp advantage at $200,000 profit: $39,200 over the C Corp and $15,600 over the default LLC. If you want to see exactly how your business profit would break down under each structure, run the numbers through this small business tax calculator before making any decisions.

The Six Costliest Entity Selection Mistakes California Owners Make

Choosing the wrong entity is not just a missed opportunity. It creates compounding tax damage that grows every year. Here are the six mistakes that cost California owners the most money.

Mistake 1: Believing the 21% C Corp Rate Is Lower Than Your Personal Rate

The 21% corporate rate looks attractive until you realize the money is trapped inside the corporation. To use it personally, you pay dividends taxed at 20% plus 3.8% NIIT, plus California income tax. The all-in rate on C Corp profits that reach your bank account ranges from 44% to 56%, depending on your bracket. That 21% headline rate is a marketing number, not a tax planning number.

Mistake 2: Staying as a Default LLC Past the $60,000 Profit Threshold

A single-member LLC is taxed as a sole proprietorship. Every dollar of net income faces 15.3% self-employment tax (Social Security at 12.4% plus Medicare at 2.9%) on the first $168,600, and 2.9% above that. An S Corp election lets you split income into a reasonable salary (subject to payroll tax) and distributions (exempt from self-employment tax). At $60,000 in profit, this split saves roughly $3,800 per year. At $200,000, the savings jump to $12,000 or more annually.

Mistake 3: Missing the March 15 Form 2553 Deadline

IRS Form 2553 must be filed by March 15 of the tax year you want the S Corp election to take effect. Miss this date by one day, and you wait an entire calendar year. That delay costs between $800 and $3,400 per month in unnecessary taxes, depending on your profit level. Late election relief under Revenue Procedure 2013-30 exists, but it requires showing reasonable cause and is not guaranteed.

Mistake 4: Setting an Unreasonable S Corp Salary

The IRS watches S Corp salary-to-distribution ratios closely. If you earn $200,000 and pay yourself a $30,000 salary while taking $170,000 in distributions, the IRS will reclassify those distributions as wages, assess back payroll taxes, and add penalties. The landmark case Watson v. Commissioner (T.C. Memo 2012-167) established that reasonable salary must reflect what a hypothetical third party would earn performing your role. The IRS nine-factor test from Revenue Ruling 59-221 guides this determination. A safe range for most California owners falls between 40% and 60% of net profit.

Mistake 5: Skipping California’s FTB Form 3560

Filing Form 2553 with the IRS does not automatically notify California. You must separately file FTB Form 3560 with the Franchise Tax Board to register your S Corp election at the state level. Skip this step, and California treats your entity as a C Corp, charging 8.84% instead of 1.5%. On $200,000, that oversight costs $14,680 in unnecessary state tax.

Mistake 6: Ignoring California’s Bonus Depreciation Nonconformity

Under OBBBA, the federal government now permanently allows 100% bonus depreciation under IRC Section 168(k). California does not conform. Under R&TC Sections 17250 and 24356, the state requires standard MACRS depreciation schedules. If you claim 100% bonus depreciation on your federal return without maintaining a separate California depreciation schedule, you will owe California tax on the difference. For a $150,000 equipment purchase, this mismatch can create a $13,950 California tax surprise in year one.

The Three Narrow Scenarios Where a C Corp Still Wins

The S Corp beats the C Corp for most California owners, but three situations create legitimate C Corp advantages. If none of these apply to you, the C Corp is almost certainly the wrong choice.

Scenario 1: Venture Capital Fundraising

Venture capital firms require preferred stock classes with different voting rights and liquidation preferences. S Corps are limited to one class of stock under IRC Section 1361(b)(1)(D). If you need multiple stock classes to attract investors, a C Corp structure is mandatory. This applies primarily to tech startups seeking Series A or later funding rounds.

Scenario 2: Qualified Small Business Stock (QSBS) Under IRC Section 1202

If you hold C Corp stock for at least five years and meet the $50 million gross asset test, you can exclude up to $10 million in capital gains from federal tax when you sell. This exclusion does not apply to S Corp stock. However, California does not conform to Section 1202 under R&TC Section 18152.5. You will still owe full California capital gains tax on the sale. Factor this state tax gap into your analysis before choosing a C Corp solely for QSBS.

Scenario 3: Full Profit Retention Below $250,000

If you plan to reinvest every dollar of profit into the business and never take distributions, the C Corp’s 21% flat rate is lower than the top individual rate of 37%. But the moment retained earnings exceed $250,000, the accumulated earnings tax under IRC Section 531 adds a 20% penalty on amounts the IRS deems beyond reasonable business needs. This strategy only works for a narrow window and requires careful documentation of reinvestment plans.

Our entity formation services help California owners evaluate these scenarios with five-layer projections before committing to any structure.

The S Corp C Corp or LLC Decision Framework: A Diagnostic Approach

Stop comparing tax rates in isolation. Use this diagnostic framework to identify your correct entity based on your actual business situation.

Should You Elect S Corp Status?

Yes, if:

- Your annual business profit exceeds $60,000

- You can justify a reasonable salary based on your role and industry

- You are willing to run payroll (or hire a payroll service)

- You have 100 or fewer shareholders, all U.S. citizens or residents

- You do not need multiple stock classes for investor requirements

- You want to bypass the SALT cap using AB 150

No, if:

- Your profit is below $40,000 (payroll costs may offset savings)

- You plan to raise venture capital requiring preferred stock

- You have nonresident alien shareholders

- You want to retain all profits at the 21% rate indefinitely

Should You Stay as a Default LLC?

Yes, if:

- Your profit is below $40,000 annually

- You value maximum simplicity over tax optimization

- Your business is a short-term project with a defined end date

- You have net losses that offset self-employment tax exposure

No, if:

- Your profit exceeds $60,000 (self-employment tax savings from S Corp election outweigh payroll costs)

- You plan to grow the business and increase profit over time

- You want access to AB 150 SALT bypass and QBI optimization

Should You Choose a C Corp?

Yes, if:

- You are actively seeking venture capital with preferred stock requirements

- You qualify for and plan to use the QSBS exclusion (and accept California nonconformity)

- You will retain 100% of profits below $250,000 for documented reinvestment

No, if:

- You plan to take distributions (double taxation applies)

- You want the QBI deduction (C Corps are excluded)

- You want AB 150 SALT bypass benefits

- Your profit exceeds $250,000 with retained earnings (accumulated earnings tax risk)

OBBBA Permanent Changes That Make the S Corp C Corp or LLC Decision More Critical in 2026

The One Big Beautiful Bill Act made several temporary provisions permanent, widening the gap between entity structures.

Permanent QBI Deduction Under IRC Section 199A

The 20% QBI deduction was set to expire after 2025. OBBBA made it permanent. For S Corp and LLC owners, this means a guaranteed deduction worth $8,800 to $14,800 annually on $200,000 in profit. C Corp owners never get this deduction. Over a 10-year horizon, that permanence represents $88,000 to $148,000 in cumulative savings that C Corp owners forfeit entirely.

Permanent 100% Bonus Depreciation Under IRC Section 168(k)

Bonus depreciation was phasing down from 100% to 60% in 2026 under pre-OBBBA law. The new legislation restored and made permanent 100% first-year expensing. California still does not conform, but the federal benefit is substantial. On a $200,000 equipment purchase, 100% bonus depreciation creates an immediate $44,000 to $74,000 federal tax savings depending on your bracket. Maintain separate California depreciation schedules to avoid state-level surprises.

$40,000 SALT Cap With AB 150 Bypass

OBBBA raised the SALT deduction cap to $40,000 (from $10,000) for individuals. S Corp and LLC owners using AB 150 can bypass even this increased cap by paying state tax at the entity level. For California owners in high-tax brackets, the bypass recovers $4,000 to $12,000 annually that would otherwise be lost. C Corp owners cannot access this bypass.

$2.5 Million Section 179 Expensing

OBBBA permanently set the Section 179 deduction limit at $2,500,000, up from the inflation-adjusted $1,250,000 under prior law. The phase-out threshold is $4,270,000. Unlike bonus depreciation, California conforms to Section 179. This makes Section 179 the preferred depreciation method for California S Corp owners purchasing qualifying equipment.

$15 Million Estate Exemption With Stepped-Up Basis

The permanent $15 million estate exemption under OBBBA interacts with entity selection for succession planning. S Corp stock receives stepped-up basis at death under IRC Section 1014, eliminating unrealized gains. C Corp stock receives the same stepped-up basis, but retained earnings inside the C Corp still face entity-level tax on distribution. LLC membership interests also receive stepped-up basis. For estate planning purposes, the S Corp often provides the cleanest succession path.

KDA Case Study: Elk Grove Consulting Firm Owner Saves $39,400 With Entity Restructuring

Rachel owned an IT consulting firm structured as a single-member LLC in Elk Grove. Her 2025 net profit was $205,000. She paid $28,905 in self-employment tax, $800 plus $2,500 in California LLC fees, and had no access to the AB 150 SALT bypass. Her total federal and state tax bill was $71,200, representing an effective rate of 34.7%.

KDA’s team ran a five-layer entity comparison and identified $39,400 in annual savings through an S Corp election. The strategy included filing Form 2553 under Rev. Proc. 2013-30 late election relief, setting a reasonable salary of $98,000 based on Bureau of Labor Statistics data for IT consultants in the Sacramento metro area, activating the AB 150 PTE election, opening a Solo 401(k) with a $23,500 employee deferral plus $24,500 employer contribution, and establishing dual federal/California depreciation schedules for $85,000 in equipment purchased that year.

After implementation, Rachel’s effective tax rate dropped from 34.7% to 15.5%. Her first-year savings of $39,400 against a KDA engagement fee of $5,800 delivered a 6.8x return on investment. Over five years, the projected cumulative savings reach $197,000, assuming stable revenue.

The engagement also included registering with the California Employment Development Department for quarterly DE 9 filings, setting up semi-monthly payroll through a licensed processor, and coordinating the Section 179 election on the $85,000 equipment purchase to maximize California-conforming depreciation.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

IRS Enforcement and Palantir SNAP AI: What the IRS Watches After You Choose Your Entity

The IRS Palantir SNAP AI system cross-references entity filings in real time. Here is what triggers scrutiny for each entity type.

S Corp Red Flags

- Salary-to-distribution ratio below 40%: The system flags S Corp returns where officer compensation on Form 1120-S, Line 7 is disproportionately low relative to distributions on Schedule K-1, Line 16d

- Missing Form 941 filings: If your S Corp shows income but no quarterly payroll tax returns, the system generates an automatic flag

- Form 7203 basis tracking gaps: Shareholders must file Form 7203 to track stock and debt basis. Missing or inconsistent basis reporting triggers review

C Corp Red Flags

- Retained earnings above $250,000 without documented business need: The accumulated earnings tax under IRC Section 531 applies a 20% penalty on excess accumulations

- Shareholder loans without proper documentation: The IRS reclassifies informal loans as disguised dividends, triggering double taxation plus penalties

- Personal expenses run through the corporation: The system matches vendor payments against industry norms and flags outliers

Default LLC Red Flags

- Underreported self-employment tax: The system compares Schedule C net income against Schedule SE. Discrepancies generate automatic notices

- Excessive business deductions relative to revenue: LLC filers claiming deductions exceeding 65% of gross revenue face elevated audit risk

- Missing California LLC fee payments: The FTB independently tracks gross receipts and cross-references LLC fee payments under R&TC Section 17942

Eight-Step Entity Selection and Implementation Process

Whether you choose an S Corp, C Corp, or LLC, follow this process to ensure compliance and maximize savings.

- Run the Five-Layer Tax Projection: Calculate your total tax liability under all three structures using your actual profit numbers, not estimates. Include federal, state, self-employment, QBI, and SALT bypass layers.

- Verify IRC 1361(b) Eligibility (S Corp Only): Confirm you have 100 or fewer shareholders, only eligible shareholder types, one class of stock, and domestic corporation status.

- Evaluate Built-In Gains Tax Exposure (C Corp to S Corp): If converting from a C Corp, assess BIG tax under IRC Section 1374 on appreciated assets within the five-year recognition period. Obtain a professional appraisal to establish fair market value at conversion date.

- File Form 2553 by March 15: Submit to the IRS with all shareholder consents. Keep proof of timely filing via certified mail or fax confirmation.

- File FTB Form 3560 With California: Separately notify the Franchise Tax Board of your S Corp election. This is not automatic.

- Establish Reasonable Salary and Payroll: Set officer compensation using the replacement cost method, 60/40 split guideline, or industry benchmark triangulation. Register with EDD and set up quarterly DE 9 filings.

- Activate AB 150 PTE Election: Make the elective tax payment at the entity level to bypass the federal SALT cap. File the election on the original, timely filed return.

- Establish Dual Depreciation Schedules: Maintain separate federal (with bonus depreciation) and California (MACRS only) depreciation records for every asset. Reconcile annually on California Form 3885A.

What If I Already Filed as a Default LLC This Year?

You can still elect S Corp status for the current tax year if you file Form 2553 within 75 days of forming the LLC or by March 15 of the current year, whichever comes later. If both deadlines have passed, you have two options. First, request late election relief under Rev. Proc. 2013-30 by attaching Form 2553 to a timely filed or extended Form 1120-S. Second, plan the election for next year and file Form 2553 by March 15 of the upcoming tax year. Every month of delay costs between $800 and $3,400 in unnecessary self-employment tax at typical California profit levels.

Can I Switch Back if the S Corp Election Does Not Work?

Yes, but there is a catch. If you revoke your S Corp election, IRC Section 1362(g) imposes a five-year lockout period. During those five years, you cannot re-elect S Corp status without IRS consent, which is rarely granted. Before revoking, run the five-layer comparison again with updated profit projections. In most cases, temporary profit dips do not justify permanent revocation.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About S Corp C Corp or LLC Selection

What is the minimum income level where an S Corp election saves money?

Most California tax strategists recommend a minimum of $60,000 to $75,000 in annual net profit before the S Corp payroll tax savings outweigh the cost of running payroll, filing Form 1120-S, and maintaining additional compliance requirements.

Do I need a new EIN if I elect S Corp status for my LLC?

No. Your existing EIN remains the same. The S Corp election changes your tax classification, not your legal entity. You continue using the same EIN on all federal and state filings.

Can a multi-member LLC elect S Corp status?

Yes, provided all members are eligible shareholders under IRC Section 1361(b). All members must consent on Form 2553. The LLC operating agreement should be amended to reflect single-class-of-stock requirements.

Does California charge a minimum tax for S Corps?

Yes. California imposes an $800 minimum franchise tax on all S Corps under R&TC Section 17935, regardless of income. First-year LLCs and corporations formed after January 1, 2024 are exempt from the $800 fee for their first tax year under AB 150 provisions.

How does the S Corp election affect my retirement contributions?

S Corp owners can contribute to a Solo 401(k) as both employee and employer. For 2026, the employee deferral limit is $23,500, and total contributions (employee plus employer) can reach $70,000 for owners age 50 and older. Your reasonable salary is the basis for calculating maximum contributions, so setting salary too low limits retirement savings.

What happens to my California LLC fee after the S Corp election?

The gross receipts-based LLC fee under R&TC Section 17942 no longer applies after you elect S Corp status. Instead, you pay the 1.5% California franchise tax on net income (minimum $800). For most owners, this reduces total state tax compared to the combined LLC fee and minimum tax structure.

This information is current as of May 5, 2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Book Your Entity Structure Strategy Session

If you are running a California business as a default LLC and your profit exceeds $60,000, you are almost certainly overpaying by thousands every year. The S Corp C Corp or LLC decision is not a one-size-fits-all answer. It depends on your profit level, growth plans, investor needs, and retirement goals. Our strategists run the full five-layer comparison, file every required form, and set up your entity structure so it saves you money from day one. Click here to book your entity strategy consultation now.

“The IRS does not penalize you for paying less tax. It penalizes you for paying the wrong amount. Pick the right entity, and you pay exactly what you owe, which is a lot less than what you are paying now.”