The One Visual That Exposes the $39,000 Gap Between S Corps and C Corps in California

Most California business owners have never seen a single S Corp C Corp infographic that breaks down where their money actually goes after the IRS and the Franchise Tax Board take their cut. They hear “21% corporate rate” from their attorney, nod along, and never realize that number is only the opening act in a five-layer tax performance that ends with nearly half their profit gone. A well-built visual comparison changes that in about 30 seconds. It turns a confusing entity decision into a clear, dollar-for-dollar reality check that reveals whether you are on the right side of a $39,000 annual gap or the wrong one.

Quick Answer

An S Corp C Corp infographic maps the five distinct tax layers that separate these two entity structures in California: federal entity tax, federal dividend double taxation, California franchise tax differentials, the QBI deduction under IRC Section 199A, and the AB 150 pass-through entity (PTE) tax election. At $200,000 in business profit, an S Corp owner in California keeps roughly $39,000 to $48,000 more per year than a C Corp owner distributing the same earnings. The visual makes the gap impossible to ignore.

What an S Corp C Corp Infographic Actually Reveals About Your Tax Bill

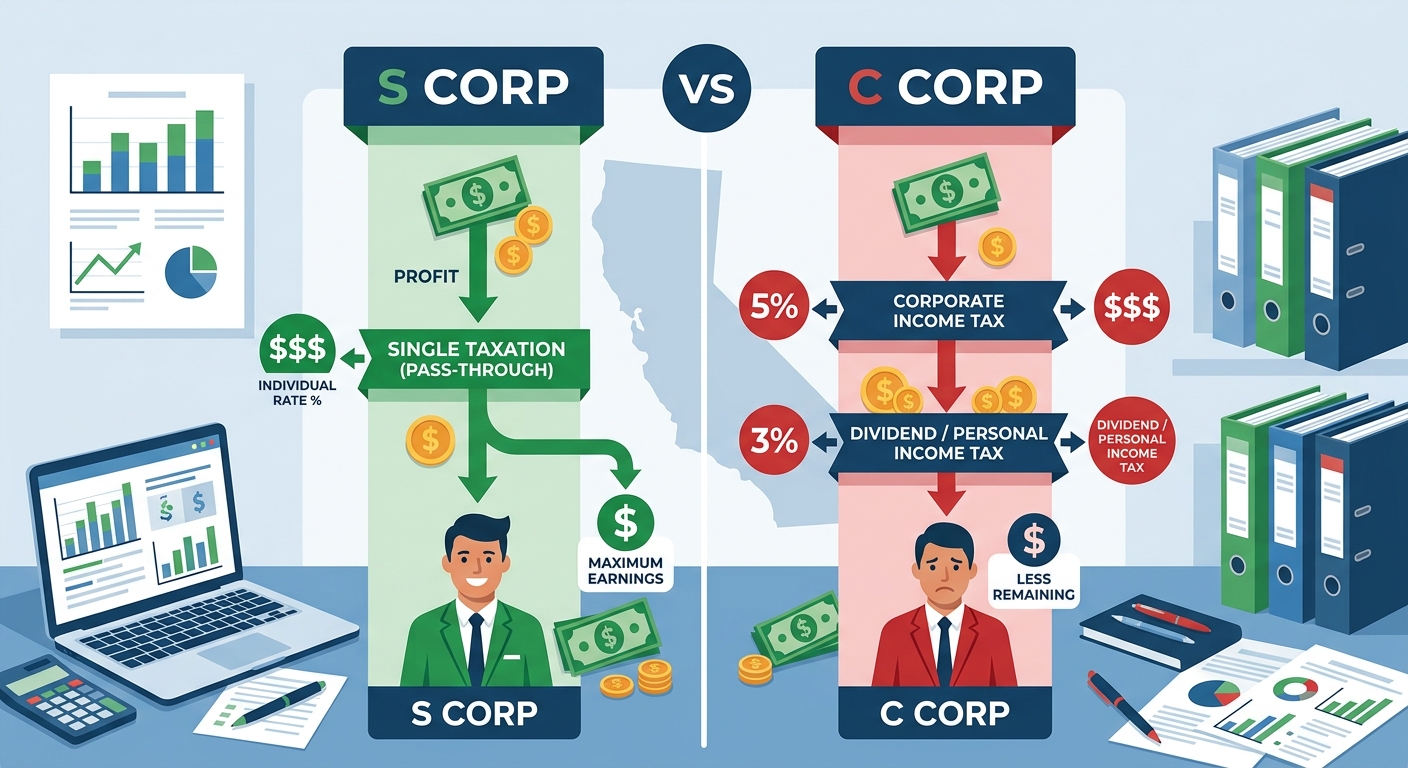

A static comparison of S Corp versus C Corp usually lists features side by side. Ownership limits, shareholder rules, stock classes. That information matters for legal structuring, but it tells you nothing about how much money you lose each year by choosing the wrong entity. A properly built S Corp C Corp infographic does something different. It traces every dollar of business profit through each tax layer and shows you exactly where the money disappears.

Layer One: Federal Entity-Level Tax

A C Corp pays a flat 21% federal corporate income tax on net profit before a single dollar reaches the owner. On $200,000 in profit, that is $42,000 gone at the entity level. An S Corp pays zero federal entity-level tax. The profit passes through to the owner’s personal return untouched. That first layer alone creates a $42,000 head start for the S Corp owner, though the math gets more nuanced once individual rates apply.

Layer Two: Federal Dividend Double Taxation

After the C Corp pays its 21% corporate tax, the remaining $158,000 gets distributed to the owner as a qualified dividend. Federal dividend tax rates range from 0% to 23.8%, including the 3.8% Net Investment Income Tax under IRC Section 1411. At the 18.8% combined rate, the owner pays another $29,704 on those dividends. That is two separate federal tax events on the same $200,000 in business profit. S Corp distributions avoid this entirely because they are not dividends. They are returns of already-taxed income.

Layer Three: California Franchise Tax Differential

California taxes C Corps at 8.84% of net income through the franchise tax. On $200,000, that is $17,680. S Corps pay just 1.5% of net income, which equals $3,000. The difference: $14,680 in state-level savings that never shows up on a basic federal comparison chart. Many business owners who operate in California miss this layer entirely because their advisor only ran the federal numbers.

Layer Four: The QBI Deduction Exclusivity

The Qualified Business Income deduction under IRC Section 199A allows S Corp owners to deduct up to 20% of qualified business income from their federal taxable income. The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, made this deduction permanent. On $200,000 in S Corp profit, the QBI deduction removes $40,000 from taxable income, saving roughly $8,800 to $14,800 in federal tax depending on the owner’s marginal rate. C Corps do not qualify for the QBI deduction. Period. This is an S Corp-exclusive benefit that widens the gap every single year.

Layer Five: AB 150 PTE Election

California’s AB 150 pass-through entity tax election allows S Corp owners to pay state income tax at the entity level and claim a dollar-for-dollar federal tax credit, effectively bypassing the $40,000 SALT deduction cap. C Corps cannot use this election. For a California S Corp owner in the top bracket, this creates an additional $2,000 to $5,000 in annual savings that a basic S Corp C Corp infographic rarely captures but that a five-layer version makes crystal clear.

The Five-Layer Tax Comparison Table Every California Owner Needs

When you stack all five layers into a single visual, the cumulative impact is staggering. Here is the breakdown at three profit levels that California business owners commonly earn. If you want to plug your own numbers in before reading further, run them through this small business tax calculator to see your estimated gap.

| Tax Layer | C Corp ($100K Profit) | S Corp ($100K Profit) | C Corp ($200K Profit) | S Corp ($200K Profit) | C Corp ($350K Profit) | S Corp ($350K Profit) |

|---|---|---|---|---|---|---|

| Federal Entity Tax (21%) | $21,000 | $0 | $42,000 | $0 | $73,500 | $0 |

| Federal Dividend Tax | $11,840 | $0 | $29,704 | $0 | $51,982 | $0 |

| CA Franchise Tax | $8,840 | $1,500 | $17,680 | $3,000 | $30,940 | $5,250 |

| QBI Deduction Savings | $0 | $4,400 | $0 | $8,800 | $0 | $14,800 |

| AB 150 PTE Savings | $0 | $1,800 | $0 | $3,200 | $0 | $4,900 |

| Annual S Corp Advantage | $17,600 | $39,287 | $64,700 | |||

That table is the S Corp C Corp infographic in data form. At $200,000 in profit, the S Corp owner keeps $39,287 more per year. Over five years, that is $196,435 in cumulative savings. No product, no investment, no side hustle delivers that kind of return with a single tax election.

For a complete walkthrough of how these layers interact under 2026 California rules, see our comprehensive S Corp tax strategy guide.

Five Costliest Mistakes That Make the Infographic Irrelevant

Knowing the five-layer gap exists does nothing if you execute the conversion incorrectly. Here are the five mistakes that wipe out the advantage your S Corp C Corp infographic just revealed.

Mistake One: Trusting the 21% Rate Without Running the Full Distribution Cycle

The 21% C Corp rate looks attractive on paper. But that number only applies to retained earnings. The moment you distribute profit as a dividend, you trigger a second layer of federal tax at up to 23.8%. Combined with California’s 8.84% franchise tax, the effective rate on distributed C Corp income exceeds 46% at the $200,000 level. A single-number comparison is not a tax strategy. It is a trap.

Mistake Two: Filing Form 2553 After the March 15 Deadline

IRS Form 2553 elects S Corp status. The deadline to file for current-year treatment is March 15. Miss it, and you remain a C Corp for the entire tax year, losing $17,600 to $64,700 depending on your profit level. Late election relief exists under Rev. Proc. 2013-30, but it requires meeting specific conditions and demonstrating reasonable cause. Do not assume the IRS will grant it.

Mistake Three: Skipping FTB Form 3560 After the Federal Election

California requires a separate S Corp election notification via FTB Form 3560. Filing Form 2553 with the IRS does not automatically update your California status. Skip this step and the FTB will continue taxing you at the 8.84% C Corp rate instead of the 1.5% S Corp rate. That is a $14,680 mistake on $200,000 in profit that many owners do not discover until they get their first California tax bill after conversion.

Mistake Four: Setting an Unreasonable Salary

S Corp owners must pay themselves a reasonable salary before taking distributions. The IRS uses Bureau of Labor Statistics data, industry comparisons, and compensation studies to evaluate what “reasonable” means. In Watson v. Commissioner, the Tax Court ruled that an accounting firm owner paying himself $24,000 on $200,000+ in firm profit set an unreasonable salary. The penalty: reclassification of distributions as wages plus back employment taxes, interest, and penalties. A reasonable salary for a $200,000 S Corp typically falls in the $75,000 to $95,000 range, depending on the industry and geography.

Mistake Five: Ignoring California Bonus Depreciation Nonconformity

The OBBBA restored 100% bonus depreciation at the federal level under IRC Section 168(k). California does not conform. Under R&TC Sections 17250 and 24356, California requires its own depreciation schedule. If you file one set of numbers for both jurisdictions, you will either overpay California or understate federal deductions. Every S Corp in California must maintain dual depreciation schedules. This is not optional. It is a compliance requirement that creates real audit exposure when ignored.

Three Narrow Scenarios Where the C Corp Wins

Honesty matters more than sales pitches. There are exactly three situations where the C Corp structure delivers a genuine advantage over the S Corp, even after factoring in all five tax layers.

Scenario One: Venture Capital Funding With a Signed Term Sheet

Venture capital investors require C Corp structure because it supports preferred stock classes, convertible notes, and complex equity arrangements. S Corps are limited to one class of stock under IRC Section 1361(b)(1)(D). If you have a signed term sheet from a VC firm, the C Corp structure is the correct choice. If you are hoping to raise VC funding someday, that is not a reason to stay in a C Corp today.

Scenario Two: QSBS Section 1202 Exclusion

Qualified Small Business Stock under IRC Section 1202 allows C Corp shareholders to exclude up to 100% of capital gains on stock held for five or more years, up to $15 million or 10x their cost basis under the new OBBBA tiered rules. This is a legitimate C Corp advantage for founders planning a major exit. However, California does not conform to the federal QSBS exclusion under R&TC Section 18152.5, meaning California will still tax the full gain at up to 13.3%.

Scenario Three: Full Earnings Retention Below $250,000

If a C Corp retains 100% of earnings and never distributes a dividend, double taxation never triggers. At the 21% corporate rate, the entity-level tax is lower than the top individual rate. However, retained earnings above $250,000 trigger the accumulated earnings tax under IRC Section 531 at an additional 20%. And the moment you distribute those retained earnings in any future year, the second layer of tax arrives. This strategy works only as long as you never need the money personally.

KDA Case Study: Sacramento Landscaping Business Owner Saves $37,400 in Year One

A landscaping company owner in Sacramento had operated as a C Corp since 2019. Annual profit averaged $215,000. His CPA filed the corporate return, paid the 21% federal rate and the 8.84% California franchise tax, and distributed the remainder as dividends. He had never seen a five-layer S Corp C Corp infographic and did not know the QBI deduction or AB 150 PTE election existed.

KDA ran a full five-layer analysis. The results showed he was overpaying by $37,400 per year. Here is what we executed:

- Filed Form 2553 for S Corp election and FTB Form 3560 for California notification

- Set a reasonable salary at $85,000 based on BLS data for landscaping business managers in the Sacramento metro area

- Activated the AB 150 PTE election to bypass the $40,000 SALT cap

- Established dual depreciation schedules for federal and California compliance

- Set up a Solo 401(k) with a $23,500 employee contribution plus 25% employer match on salary

- Eliminated $18,040 in accumulated AE&P through a final pre-conversion distribution under IRC Section 1368(c)

First-year savings: $37,400. Engagement fee: $5,200. That is a 7.2x return on investment in year one alone. Projected five-year savings: $187,000.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How to Build Your Own Five-Layer S Corp C Corp Comparison

You do not need a design degree to create a useful visual comparison. You need the right numbers and the right structure. Here is the eight-step process KDA uses to build every S Corp C Corp infographic for our California clients.

Step One: Calculate Your Annual Business Profit

Use your net income after all ordinary and necessary business expenses. This is the number that flows through to either the corporate return (C Corp) or your personal return (S Corp). Do not use gross revenue.

Step Two: Apply the 21% Federal Corporate Tax (C Corp Only)

Multiply your net profit by 0.21. That is the first-layer tax the C Corp pays before you see a dollar. Record this amount.

Step Three: Calculate Federal Dividend Tax on the Remainder

Subtract the corporate tax from your net profit. Multiply the remainder by your qualified dividend rate (15% or 18.8% including the 3.8% NIIT under IRC 1411 for high earners). This is your second-layer tax.

Step Four: Apply the California Franchise Tax Differential

For the C Corp column, multiply net profit by 8.84%. For the S Corp column, multiply by 1.5%. Record both amounts. The gap at $200,000 is $14,680.

Step Five: Calculate the QBI Deduction Benefit (S Corp Only)

Multiply your S Corp net income by 20% to find the QBI deduction amount. Then multiply that deduction by your marginal federal tax rate to find the actual tax savings. At the 24% bracket, a $40,000 QBI deduction saves $9,600. C Corps get zero.

Step Six: Estimate the AB 150 PTE Tax Credit (S Corp Only)

If your California state income tax exceeds $40,000, the AB 150 election generates additional savings by allowing entity-level state tax payments that bypass the federal SALT cap. Calculate the difference between your SALT-capped deduction and your full state tax liability. That gap is your AB 150 benefit.

Step Seven: Stack All Five Layers Into a Single Visual

Create two columns. Label one “C Corp” and the other “S Corp.” List all five tax amounts in rows. Sum each column. The difference between the two totals is your annual entity gap. At $200,000, it should land between $39,000 and $48,000 depending on your specific tax situation.

Step Eight: Project the Gap Over Five Years

Multiply your annual gap by five. Add 3% annual growth if your profit is increasing. That five-year number is what you are leaving on the table every year you stay in the wrong entity structure. At $200,000 in profit, the five-year cost of staying in a C Corp exceeds $196,000.

OBBBA Permanent Changes That Make This Visual Even More Critical in 2026

The One Big Beautiful Bill Act, signed into law on July 4, 2025, permanently locked in several provisions that expand the S Corp advantage shown in every S Corp C Corp infographic. Understanding these changes is essential for every California business owner evaluating entity formation or restructuring decisions in 2026 and beyond.

QBI Deduction Under IRC 199A: Permanent

The 20% Qualified Business Income deduction was originally set to expire after December 31, 2025 under the TCJA sunset provisions. The OBBBA made it permanent. S Corp owners below the income phase-out thresholds ($197,300 single, $394,600 married filing jointly for 2025, indexed for inflation in 2026) can deduct 20% of qualified business income from federal taxable income every year going forward. This single provision is worth $4,400 to $14,800 annually depending on profit level.

100% Bonus Depreciation Under IRC 168(k): Restored and Permanent

Bonus depreciation had been phasing down from 100% to 80% to 60%. The OBBBA restored it to 100% and made it permanent. S Corp owners can now deduct the full cost of qualifying assets in the year they are placed in service. California does not conform under R&TC Sections 17250 and 24356, so dual depreciation schedules remain mandatory.

Section 179 Expensing Limit: Raised to $2.5 Million

The OBBBA increased the Section 179 expensing limit to $2.5 million with a phase-out beginning at $4 million. This allows S Corp owners to immediately expense qualifying equipment and property improvements rather than depreciating them over multiple years.

SALT Cap at $40,000 With AB 150 Bypass

The federal state and local tax deduction cap was set at $10,000 under the TCJA. The OBBBA raised it to $40,000 but maintained the cap. California S Corp owners bypass this cap entirely through the AB 150 PTE election, which allows entity-level state tax payment with a corresponding dollar-for-dollar federal credit. C Corp owners cannot use this workaround.

Estate Tax Exemption at $15 Million Per Person

The OBBBA set the federal estate tax exemption at $15 million per individual, or $30 million per married couple with portability under IRC Section 2010(c)(4). This changes the calculus for business succession planning and generational wealth transfer, particularly for S Corp owners whose business value passes through their estate.

What If You Already Filed as a C Corp for 2026?

If you already filed your 2026 corporate return as a C Corp, you have options. The March 15, 2027 deadline for the 2027 tax year S Corp election is your next opportunity. Between now and then, consider these steps.

First, calculate your five-layer gap using the eight-step process above. If the annual advantage exceeds $15,000, the conversion is almost certainly worth pursuing. Second, evaluate your Built-In Gains tax exposure under IRC Section 1374. If your C Corp holds appreciated assets, those gains may be taxed at the entity level during the five-year recognition period after conversion. Third, clean up any accumulated earnings and profits (AE&P) under IRC Section 1368(c) before the election becomes effective. AE&P from C Corp years can contaminate S Corp distributions and create unexpected dividend treatment.

If you missed the March 15, 2026 deadline for the current year, late election relief under Rev. Proc. 2013-30 may be available if you can demonstrate reasonable cause and all shareholders consented. The IRS Palantir SNAP AI system now cross-references entity classification changes against payroll filings and distribution patterns, so incomplete filings or mismatched data will trigger review faster than in previous years.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Can an LLC Use the S Corp C Corp Infographic to Decide Its Tax Election?

Yes. An LLC can elect to be taxed as either an S Corp (Form 2553) or a C Corp (Form 8832). The five-layer visual comparison applies directly to LLCs making this election. The default LLC classification is a disregarded entity (single member) or partnership (multi-member), both of which carry self-employment tax on all net income. Electing S Corp status eliminates self-employment tax on distributions while preserving LLC liability protection.

Does California Tax S Corps and C Corps Differently Beyond the Franchise Tax?

Yes. Beyond the franchise tax differential (1.5% versus 8.84%), California does not conform to several federal provisions that benefit S Corps, including bonus depreciation under R&TC Sections 17250 and 24356 and the QSBS exclusion under R&TC Section 18152.5. California also imposes a gross receipts fee under R&TC Section 17942 that ranges from $900 to $11,790 for LLCs, though this does not apply to corporations. These differences make California-specific analysis essential for any entity comparison.

How Long Does the C Corp to S Corp Conversion Take?

The administrative process takes 30 to 60 days from start to finish. Filing Form 2553 with the IRS takes one business day. FTB Form 3560 processing takes two to four weeks. Payroll setup with reasonable salary configuration takes one to two weeks. AE&P distribution planning and execution depends on the complexity of prior C Corp earnings history. KDA typically completes the entire conversion within 45 days.

Will Converting From C Corp to S Corp Trigger an Audit?

An entity classification change does not automatically trigger an audit. However, the IRS Palantir SNAP AI system flags entity changes and cross-references them against payroll filings, distribution patterns, and income levels. Ensuring clean documentation, a reasonable salary, and consistent filing across all forms minimizes audit risk. According to IRS data, S Corps with properly documented reasonable salaries and consistent K-1 reporting face audit rates below 1%.

What Is the Minimum Profit Level Where an S Corp Makes Sense?

Most tax professionals place the breakeven point between $40,000 and $60,000 in annual net profit. Below $40,000, the cost of running payroll, maintaining dual depreciation schedules, and filing Form 1120-S may not justify the self-employment tax savings. Above $60,000, the S Corp advantage typically exceeds $5,000 annually and grows with every additional dollar of profit.

Can I Revoke My S Corp Election if It Does Not Work Out?

Yes, but the consequences are severe. Revoking S Corp status under IRC Section 1362(d)(1) triggers a five-year lockout under IRC Section 1362(g), during which you cannot re-elect S Corp status. During those five years, you lose the QBI deduction, the AB 150 PTE election, and the franchise tax differential. At $200,000 in profit, the five-year cost of revocation exceeds $196,000. Run the five-layer analysis before making any revocation decision.

This information is current as of April 28, 2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

“The IRS publishes every rule that separates S Corps from C Corps. Most business owners just never see the five layers stacked in a single visual. Once they do, the decision makes itself.”

Book Your Five-Layer Entity Analysis With KDA

If you have been operating as a C Corp in California without ever seeing a five-layer S Corp versus C Corp comparison built on your actual numbers, you are almost certainly overpaying. The gap is not theoretical. It is $17,600 to $64,700 every year, depending on your profit level. Book a personalized entity analysis with our strategy team and walk away knowing exactly where your money is going and how to redirect it. Click here to book your consultation now.