Most small business owners form an LLC and assume they are set. The reality is that how that LLC is taxed can swing your annual tax bill by five figures. If you are earning real profit but have never compared an LLC taxed as an S corporation to an LLC taxed as a C corporation, you are almost certainly leaving money on the table.

Quick Answer

The short version is this. A default single member LLC is taxed like a sole proprietorship and pays full self employment tax on all profit. An LLC electing S corporation status can cut self employment tax by splitting profit between reasonable salary and distributions. An LLC electing C corporation status faces double taxation but can sometimes help high income owners who plan to reinvest profits long term. Choosing correctly is worth thousands per year once profit crosses roughly $60,000.

How LLC Tax Status Really Works

Before comparing flavors of LLC taxation, you need to understand what the IRS actually sees when it looks at your entity. From the IRS perspective, an LLC is a legal wrapper formed under state law, not a federal tax category. The tax treatment flows from elections you do or do not file with the IRS.

Default Treatment If You Do Nothing

If you create a single member LLC and never file any tax elections, the IRS treats it as a disregarded entity. In plain English, this means the LLC does not file its own federal income tax return. All income and expenses land directly on your individual return on Schedule C attached to Form 1040. You pay both income tax and the full 15.3 percent self employment tax on your net profit, subject to Social Security wage limits. See the rules in IRS Publication 334.

For a multi member LLC with no elections, the default is partnership taxation. The LLC files Form 1065, issues K 1s to each partner, and the partners report their share of income on their individual returns. Much of that income is still subject to self employment tax under the guidance in IRS Publication 541.

How S Corporation Status Enters the Picture

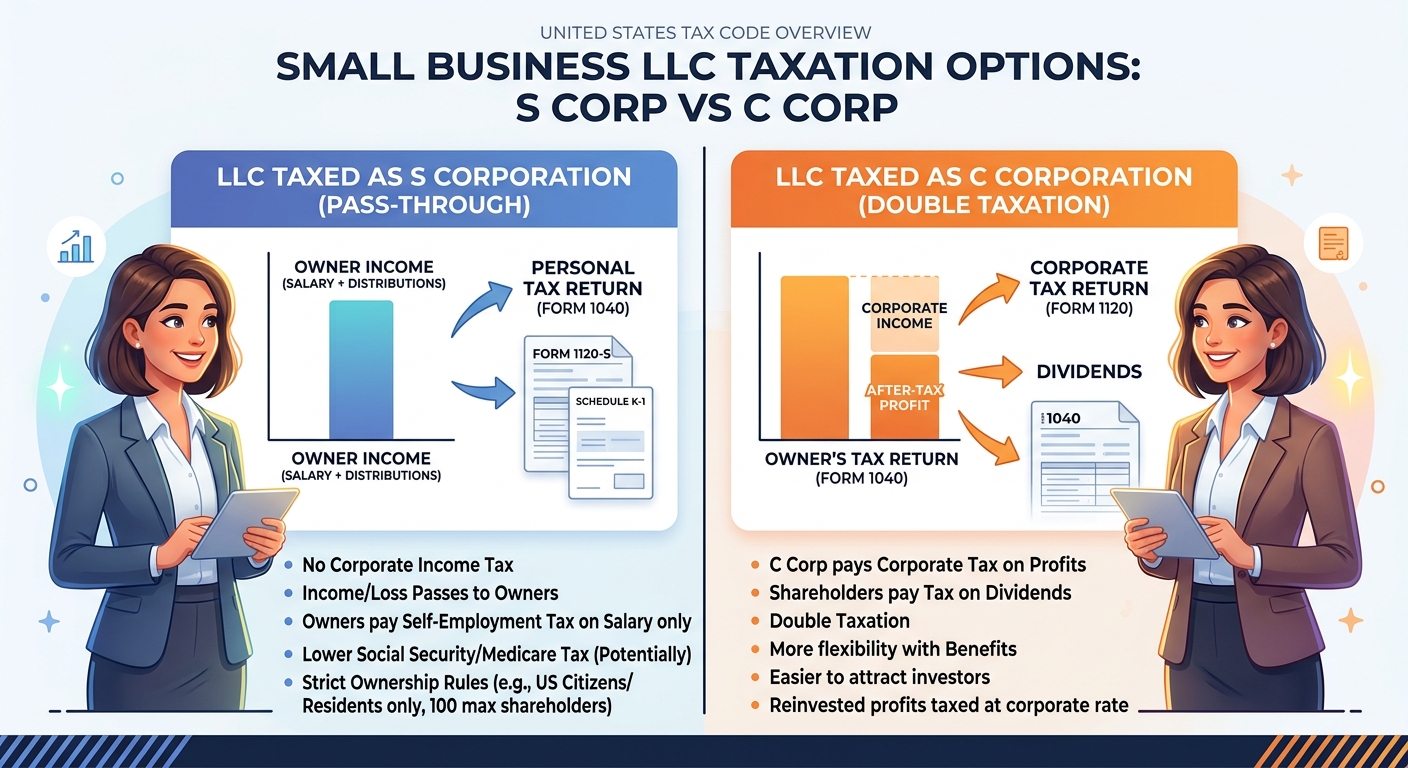

An LLC can be taxed as an S corporation by filing Form 2553 with the IRS. An S corporation is a pass through entity. The business usually files Form 1120 S and issues K 1s to shareholders. Profits pass through to the owners but are not automatically hit with self employment tax. Instead, owners working in the business must be paid a reasonable W 2 salary, which is subject to payroll taxes. Remaining profit can be distributed free of self employment tax.

For a profitable service business that has outgrown the side hustle phase, this split between salary and distributions is where a great deal of the tax savings hides. Many self employed professionals make the mistake of staying in sole proprietor mode far too long.

How C Corporation Status Works For an LLC

An LLC can also elect to be treated as a C corporation by filing Form 8832. In that case the business files Form 1120 and pays corporate income tax, currently at a flat 21 percent at the federal level. When profits are then distributed to you as dividends, you pay tax again at your individual rate. This is the classic double taxation scenario described in IRS Publication 542.

Despite that double layer of tax, a C corporation can make sense for certain high income owners who want to leave cash in the company for growth or who plan to use fringe benefits aggressively. The key is to understand the tradeoffs clearly before making the election.

Comparing LLC Tax Paths With Real Numbers

To see how the choice plays out, let us walk through a simple but realistic example. Suppose you run a consulting business that nets $160,000 after expenses. You are the only owner. The work is full time, and there is no other income. We will compare the three main paths.

Scenario 1 Default Single Member LLC

As a default LLC, all $160,000 flows to Schedule C. Ignoring itemized deductions and focusing just on federal tax for illustration, here is the rough outline.

- Self employment tax of 15.3 percent applies to the first $160,000 of net earnings, but Social Security tax only applies up to the wage base. For simplicity, assume about $20,000 of self employment tax after the deduction allowed on Schedule 1.

- Income tax is layered on top according to the individual brackets for the current year, as explained in IRS Publication 17.

On this income level, it is common to see a combined federal liability in the $45,000 to $50,000 range for someone filing single, depending on deductions and credits.

Scenario 2 LLC Taxed as S Corporation

Now assume the same $160,000 profit inside an LLC that has elected S corporation status. You have to set a reasonable salary based on what the market pays for someone doing your role. After reviewing local data and job postings, you and your advisor settle on a $90,000 W 2 wage. The remaining $70,000 is S corporation profit passed through on a K 1.

Here is how the taxes shift.

- Payroll taxes apply on the $90,000 salary, split between employer and employee sides. Combined, this is roughly $13,770, with half deductible to the business. You have removed $70,000 from the self employment tax base.

- The $70,000 of pass through profit is still subject to income tax but not to Social Security or Medicare payroll tax, assuming you have already maxed those through salary.

The result is a self employment and payroll tax savings of roughly $7,000 to $9,000 per year compared to the default LLC, before considering the extra cost of payroll and S corporation compliance. For many owners in the $120,000 to $300,000 profit range, that spread is worth the added structure.

If you want a big picture view of how structure and income level affect your total federal bill, test different scenarios with a small business tax calculator and then compare against real projections from your advisor.

Scenario 3 LLC Taxed as C Corporation

Finally, picture the same business as an LLC that filed Form 8832 to be treated as a C corporation. The company earns $160,000 before any owner compensation. Suppose you take a salary of $110,000 and leave $50,000 in the company this year to fund growth.

- The company deducts your $110,000 salary, leaving $50,000 of corporate profit taxed at 21 percent, or $10,500 in corporate tax.

- You pay individual income tax on the $110,000 of W 2 wages, plus payroll taxes as with the S corporation salary. If you later distribute the after tax retained earnings as dividends, you will pay dividend tax as well.

In this income range, the C corporation path rarely beats the S corporation path once you factor in that second layer of dividend tax. Where it sometimes makes sense is for very high income owners who want to cap corporate level tax at 21 percent and leave significant profit inside the company for many years.

When S Corporation Status Usually Wins

Once your business profit consistently sits above roughly $60,000 to $80,000 and you are actually working in the business, S corporation taxation tends to be the best balance of savings and complexity for most active owners. It keeps the pass through flexibility while cutting self employment tax without triggering double taxation. For many business owners, the savings easily cover the cost of payroll and bookkeeping support.

If you want a deeper dive on salary, distributions, and California considerations, review the S corporation strategies explained in this comprehensive S corporation tax guide and then tailor that framework to your own numbers.

Key Differences Between LLC Taxed as S Corporation and C Corporation

At the headline level, an LLC electing S corporation status focuses on reducing self employment tax for active owners while keeping a single layer of income tax. An LLC electing C corporation status accepts potential double taxation in exchange for flexibility in corporate level planning and benefits. Choosing between the two should be a strategic decision, not an accident based on whatever form someone filed years ago.

Self Employment Tax vs Double Taxation

The first question to answer is whether self employment tax is the real pain point or whether double taxation is the bigger threat. Many 1099 earners and small service firms are crushed by self employment tax. For them, relieving that pressure using salary plus distributions in an S corporation is usually more powerful than chasing the 21 percent corporate rate.

By contrast, a high net worth owner with seven figure profits who plans to retain earnings in the business may care more about locking in that flat corporate rate and using strategies like fringe benefits to extract value. For that persona, the double taxation risk can be managed with careful dividend planning, redemptions, and eventual exit strategies.

Reasonable Salary Rules in an S Corporation

The heart of the S corporation strategy is the reasonable salary requirement. The IRS expects you to pay yourself market based wages for the work you actually do before taking large distributions. There is no fixed formula in the Code, but audits and court cases show that the IRS will reclassify distributions as wages if salary is unreasonably low. See the discussion of officer compensation in Instructions for Form 1120 S.

Setting salary correctly is where many DIY S corporation setups go wrong. Underpay yourself and you risk back payroll taxes, penalties, and interest if the IRS challenges your return. Overpay yourself and you give back much of the tax benefit. This is one of the main reasons our tax planning services spend so much time on compensation modeling before locking in elections.

Fringe Benefits and Retained Earnings in a C Corporation

C corporations have access to certain fringe benefits in a cleaner way than S corporations in some cases. For example, some health and welfare benefits work more smoothly when the owner is also a W 2 employee of a C corporation, especially when nonowner employees are involved. In addition, C corporations can accumulate earnings for business needs, though very large accumulations may trigger the accumulated earnings tax.

A C corporation also defines clear boundaries between business and personal cash. If you plan to sell the business or bring in outside investors, the C corporation format is often more familiar to institutional capital. For passive investors and capital partners, especially those profiled on our capital partner services page, this clarity can be valuable.

KDA Case Study: Consultant Restructures LLC to Cut Self Employment Tax

A California based marketing consultant, earning about $190,000 in net profit through a single member LLC, came to KDA after a painful April tax bill. For several years she reported everything on Schedule C and paid full self employment tax. Her effective federal tax load, including self employment tax, hovered around $60,000 per year.

We reviewed her entity structure and quickly concluded that staying in default LLC status made little sense at her income level. After a detailed reasonable salary study based on regional pay data for similar roles, we recommended electing S corporation status and setting her W 2 salary at $105,000, with the remaining profit treated as pass through distributions.

We also implemented proper payroll, quarterly reasonable compensation reviews, and a bookkeeping system that clearly tracked officer wages versus distributions. In the first full year after restructuring, her combined payroll and income tax bill dropped by just over $9,400 compared to the prior year on nearly identical gross revenue. Our advisory fee for the planning, election filings, and first year monitoring was about $3,000, giving her more than a three to one first year return on investment, with similar savings expected each year going forward.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

What Most Owners Get Wrong About LLC and S Corporation Elections

The most common mistake is assuming that forming an LLC automatically locks in tax benefits. The state paperwork makes you legally separate from your business, but it does nothing by itself to reduce self employment tax or manage double taxation. The second mistake is making an S corporation election too early or without a compensation plan. If your business is still losing money or only generating $30,000 of profit, the extra overhead may erase any savings.

Red Flag Alert Choosing C Corporation Status Just for the 21 Percent Rate

Many owners hear about the 21 percent corporate tax rate and assume a C corporation must be the cheapest option. That ignores the fact that you will eventually need to pull money out of the company. Once you add qualified dividend tax or additional wages on top of corporate tax, your real blended rate can easily exceed what you would have paid sticking with an S corporation or even a default LLC in some cases.

Another trap is forgetting state taxes. California, for instance, imposes its own franchise tax on corporations and also charges an annual LLC fee based on gross receipts. You need to blend federal and state numbers to see the real picture.

Missing Deadlines and Late Elections

S corporation and C corporation elections are not automatic. Form 2553 for S status generally needs to be filed within two months and fifteen days after the beginning of the tax year you want it to apply to, although late election relief is sometimes available. Form 8832 has its own timing rules for entity classification changes. The IRS explains these rules in Instructions for Form 2553 and Instructions for Form 8832.

Owners frequently discover the power of S corporation savings during tax preparation, after the ideal election window has passed. While relief is possible, it requires additional statements and sometimes professional help. Getting ahead of these deadlines through proactive planning is far cheaper than trying to unwind mistakes later.

How to Decide Between S Corporation and C Corporation Treatment

With the big picture laid out, it is time to apply a simple decision framework. The goal is not to turn you into a technician but to give you a clear path to an informed yes or no.

Step 1 Clarify Your Profit Level and Growth Path

First, look at your last two or three years of net profit and your realistic forecast for the next one to two years. If your business has not yet cleared at least $60,000 in consistent annual profit, the S corporation structure may be premature. The payroll costs, extra tax filings, and bookkeeping expectations are too heavy for early stage ventures without stable earnings.

If profit is consistently above that threshold and trending up, an S corporation analysis becomes more compelling. At that stage an experienced advisor can model different salary and distribution mixes to see how much self employment tax you could credibly shave off under reasonable compensation standards.

Step 2 Decide How Soon You Need the Cash

The second question is your cash need. S corporation structures are typically best when you plan to take most profit out of the business annually to support your household. C corporation structures become more interesting when you are comfortable leaving significant cash in the company for years to fund expansion, hire teams, or pursue acquisitions.

If you are running a lifestyle consulting practice or a small professional firm, chances are you sit in the first camp. If you are building a scalable product business, a technology company, or a capital heavy venture, the second camp deserves more attention.

Step 3 Look at Future Exit and Investor Needs

Finally, think about your likely exit strategy. S corporations work well for owner operated businesses that will eventually be sold as asset deals or transferred gradually. C corporations often align better with outside investors, stock option plans, and potential stock sales. Certain tax benefits, such as the qualified small business stock exclusion under Section 1202, are only available in C corporation structures when strict conditions are met.

These strategic questions are why serious owners work with advisors who look beyond the current year tax return. Our premium advisory services are built around multi year planning, not just compliance.

Will Changing Your LLC Tax Status Trigger an Audit

Many owners worry that switching from default LLC taxation to S corporation status or even C corporation status will automatically put them on an IRS audit list. There is no rule that says the act of filing Form 2553 or Form 8832 triggers scrutiny. The risk comes from what you do after the election.

The main audit trigger in S corporations is unreasonably low officer compensation combined with large distributions. The IRS explicitly calls this issue out in its guidance to examiners. If you treat yourself as making $30,000 on payroll while pulling $200,000 of distributions in a service business, you are asking to be challenged.

For C corporations, the exam risk often revolves around unreasonable compensation in the opposite direction. If you try to zero out corporate profit each year with giant salaries or bonuses to avoid corporate tax, the IRS can recharacterize part of that pay as nondeductible dividends.

Pro Tip Use Clearly Documented Compensation Policies

The best defense is a written compensation policy tied to market data, revisited annually, and implemented through clean payroll records. Documenting how you arrived at your salary figures, and keeping that file with your corporate records, goes a long way in showing that you acted in good faith.

Common Questions About LLC Tax Elections

Can I Switch From S Corporation Treatment Back to Default LLC Taxation

Yes, but not casually. Once you elect S corporation status, there are timing restrictions on terminating that election and rules around when you can make a new one. In addition, unwinding S corporation status can have tax consequences if the company holds appreciated assets or has built in gains. Any move to change status should be modeled carefully in advance.

What If My Income Drops After I Elect S Corporation Status

If profits fall below the level where S corporation savings outweigh the extra overhead, you can adjust your salary downward within reasonable bounds and reassess. If the downturn looks long term, it may make sense to consider revoking the S election, but you want professional advice before pulling that trigger.

Can a Real Estate Investor Benefit From S Corporation or C Corporation Status

Generally, long term rental real estate is better held in LLCs taxed as partnerships or disregarded entities, not S corporations or C corporations, because of how losses, depreciation, and the qualified business income deduction operate. For those holding multiple properties or larger portfolios, specialized structures and planning are available through our real estate tax preparation services tailored to landlords and investors.

Bottom Line and Next Steps

Choosing how your LLC is taxed is not a checkbox decision to hand off to incorporation websites or do it yourself software. The spread between a default LLC and an S corporation election can easily reach $10,000 per year for a single owner business in the six figure profit range. The wrong C corporation election can create long term double taxation traps that are far more expensive to unwind than they were to set up.

This information is current as of 5/18/2026. Tax laws change frequently. Verify updates with the IRS or your state tax authority if you are reading this at a later date, and review primary sources like IRS Publication 334, Publication 541, and the instructions for Forms 2553 and 8832 for the latest details.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Book Your Entity Tax Strategy Session

If you suspect your current LLC setup is costing you unnecessary tax, it is time to run real numbers and choose a structure that fits your income, goals, and risk tolerance. Our team specializes in modeling S corporation and C corporation options for consultants, creatives, professional firms, and investors so you can see your next three to five years on paper before filing a single election. Book a consultation today and walk away with a clear, customized entity tax plan instead of another surprise bill next April.

The IRS is not hiding these savings. Most owners simply were never taught how to align their LLC tax status with the way they actually earn and keep money.

Direct link to this blog post will be provided once published on the KDA site.