Every April, millions of taxpayers hand the IRS more money than they legally owe. The reason is almost never fraud or complexity. It is one overlooked decision made in a hurry: choosing the wrong deduction method. Understanding the difference between itemized deductions and standard deductions is the single fastest way to stop leaving money on the table, and yet the majority of filers pick their method by default instead of by math.

Here is the uncomfortable truth. Software will often nudge you toward whichever answer is faster to process, not whichever answer saves you the most. And the tax code changed enough over the past several years that old assumptions no longer hold. A strategy that made sense in 2017 may cost you thousands today. Let’s fix that.

Quick Answer

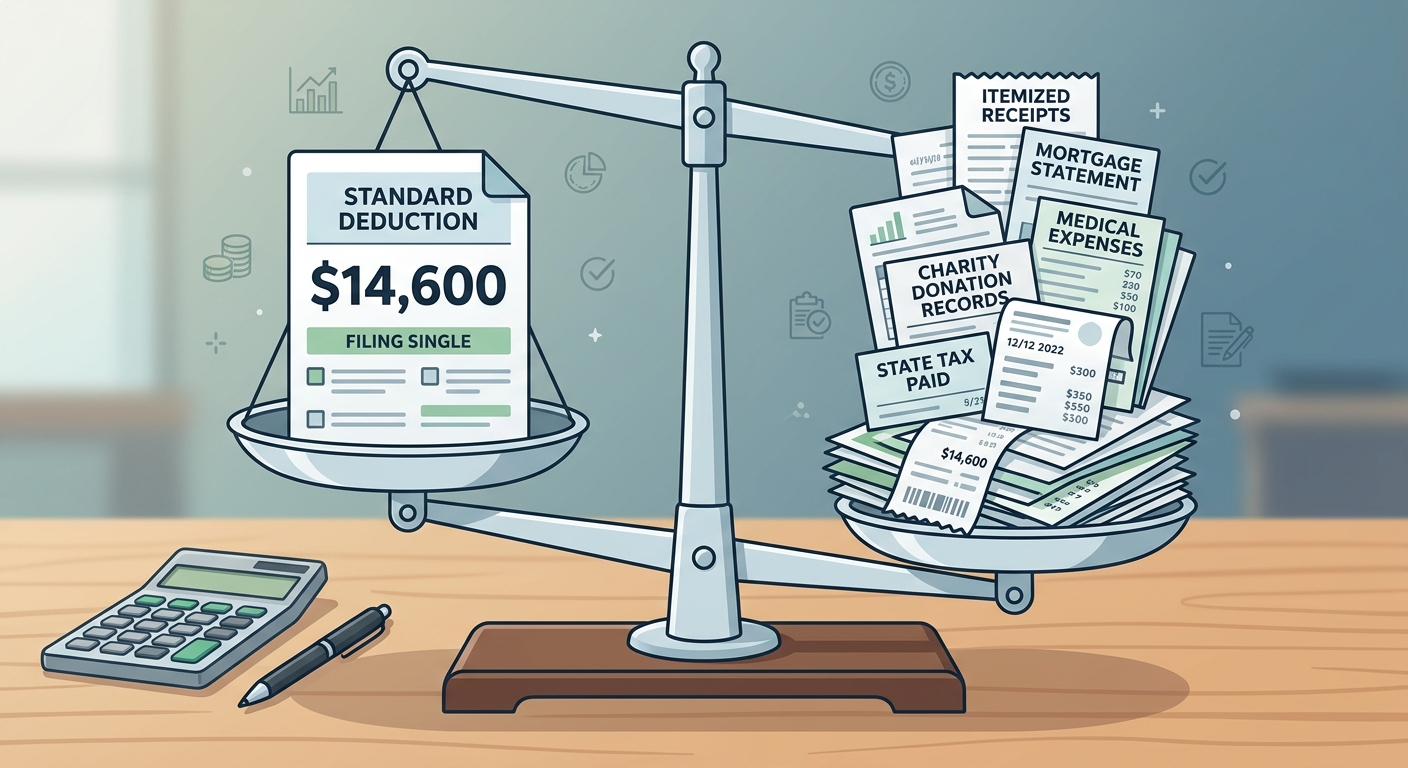

The difference between itemized deductions and standard deductions comes down to this: the standard deduction is a fixed dollar amount the IRS lets you subtract from your income with zero paperwork, while itemized deductions require you to add up specific qualifying expenses such as mortgage interest, state taxes, and charitable gifts. You take whichever number is larger. For tax year 2025, the standard deduction is $15,000 for single filers and $30,000 for married couples filing jointly. If your itemized expenses beat that number, you itemize. If they don’t, you take the standard.

This information is current as of 7/12/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

What Is a Deduction, and Why Does the Choice Matter?

A deduction is an amount subtracted from your gross income before your tax is calculated. It lowers your taxable income, which lowers the tax you owe. It is not a dollar-for-dollar credit. If you are in the 22 percent bracket, a $1,000 deduction saves you roughly $220, not $1,000. That distinction trips up a lot of people, so keep it front of mind.

Every taxpayer gets to choose one of two roads. The first road is the standard deduction, a flat amount set by Congress that anyone can claim without justification. The second road is itemizing, where you list out individual expenses that the tax code specifically allows. You cannot use both. You pick the road that produces the bigger deduction, and therefore the smaller tax bill.

Why does this matter so much? Because the gap between the two can be enormous. A homeowner in California with a large mortgage and high property taxes might have $42,000 in itemized deductions. If that person mistakenly takes the $30,000 standard deduction, they just threw away $12,000 in deductions. At a 24 percent marginal rate, that is roughly $2,880 in real cash handed to the government for no reason.

The Core Distinction in Plain English

Think of it like a coupon at checkout. The standard deduction is a store-wide coupon everyone gets automatically at the register, no receipts needed. Itemizing is like clipping individual coupons for each product in your cart. Sometimes the store-wide coupon is bigger. Sometimes your stack of individual coupons wins. You would never use the smaller one on purpose, but that is exactly what happens when people file on autopilot.

Standard Deduction: The Simple Path Most People Take

The standard deduction is the government’s way of simplifying tax filing for the majority of households. You claim it, you move on, no records required. Roughly 90 percent of filers now take the standard deduction, largely because the amount was nearly doubled by the Tax Cuts and Jobs Act starting in 2018 and has been adjusted upward for inflation each year since.

For tax year 2025, the amounts are as follows. Single filers and those married filing separately claim $15,000. Heads of household claim $22,500. Married couples filing jointly claim $30,000. Taxpayers who are 65 or older, or blind, get an additional amount stacked on top. For 2025, that extra amount is $1,600 per condition for married filers and $2,000 for single or head-of-household filers.

Who Should Default to the Standard Deduction?

Yes, take the standard deduction, if:

- You rent your home and have no mortgage interest to deduct

- Your state and local taxes plus charitable gifts fall well under $15,000 (single) or $30,000 (married)

- You had no large medical expenses or casualty losses during the year

- You want the simplest possible return with no receipt tracking

Take Marcus, a 29-year-old W-2 software engineer renting an apartment in San Jose. He donates $2,000 to charity and pays $9,000 in California state income tax withholding. His potential itemized total is around $11,000, well below the $15,000 standard deduction. Marcus takes the standard deduction and saves himself hours of record-keeping while capturing the bigger write-off. For high-income W-2 earners like Marcus who want to dig into overlooked opportunities, our resources for engineers and tech professionals cover strategies beyond the basic deduction choice.

Pro Tip: The standard deduction requires zero documentation. There is nothing to prove, nothing to save, and nothing to defend in an audit. That simplicity has real value if your itemized total would only barely edge past the standard amount.

Itemized Deductions: When Listing Expenses Wins

Itemizing means reporting your qualifying expenses on Schedule A of Form 1040. You only benefit from itemizing when the sum of these expenses exceeds your standard deduction. The most common categories that push people over the threshold are homeowners with mortgages, residents of high-tax states, and people with significant medical bills or charitable giving.

Here are the major itemizable categories and their current limits. Understanding each one is the key to knowing whether itemizing is worth it for your situation.

State and Local Taxes (SALT)

You can deduct state income taxes (or sales taxes, whichever is larger) plus property taxes. However, this category is capped. Through 2025, the SALT deduction is limited to $10,000 per return ($5,000 if married filing separately). This cap hits high-tax states like California especially hard, since many homeowners blow past $10,000 in property and income taxes alone.

Mortgage Interest

Interest paid on mortgage debt used to buy, build, or improve your home is deductible on loans up to $750,000 (for mortgages taken after December 15, 2017). This is usually the single largest itemized deduction for homeowners. Your lender sends you Form 1098 each January showing the exact interest you paid. If you are weighing a home purchase or refinance, run the numbers through this mortgage interest calculator to see the deduction impact before you commit.

Charitable Contributions

Cash and property donations to qualified organizations are deductible, generally up to 60 percent of your adjusted gross income for cash gifts. Keep written acknowledgment for any single donation of $250 or more. Donations of appreciated stock held over a year are especially powerful, since you deduct full market value and skip the capital gains tax.

Medical and Dental Expenses

You can deduct unreimbursed medical expenses that exceed 7.5 percent of your adjusted gross income. If your AGI is $80,000, only medical costs above $6,000 count. This threshold is high, so it usually only matters in a year with surgery, long-term care, or major dental work.

KDA Case Study: The Real Estate Investor Who Almost Overpaid

Diane, a 54-year-old real estate investor in Sacramento, came to KDA convinced she should take the standard deduction because her prior accountant had done so for two straight years. Her reasoning was that the standard deduction had gotten so large it “always wins.” She owned her primary residence with a $610,000 mortgage and paid substantial California income tax on her rental portfolio.

When our team pulled her documents, the picture was clear. She had $24,000 in mortgage interest from Form 1098, the full $10,000 SALT cap, and $9,500 in documented charitable contributions to her church and a local shelter. That totaled $43,500 in itemized deductions against a $30,000 standard deduction for her married-filing-jointly status. Her previous filings had cost her the difference.

We amended her prior two returns and corrected the current one. The recovered deductions of $13,500 per year, at her 24 percent marginal rate, translated to roughly $3,240 in tax savings annually, plus refunds on the amended returns totaling $6,480. Her total first-year benefit was close to $9,720. She paid KDA $3,200 for the strategy work and amendments, producing a first-year return of just over 3x. Real estate investors juggling rentals and a primary home almost always benefit from a professional second look, which is why our real estate investor tax services start with a full deduction audit.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Standard vs Itemized: A Side-by-Side Comparison

Sometimes the clearest way to grasp the difference between itemized deductions and standard deductions is to see them lined up next to each other. Use this table as a quick diagnostic.

| Factor | Standard Deduction | Itemized Deductions |

|---|---|---|

| Paperwork | None required | Receipts and records needed |

| Amount (2025, single) | Fixed $15,000 | Varies by actual expenses |

| Best for | Renters, low expenses | Homeowners, high-tax states |

| Audit exposure | Very low | Higher, records matter |

| IRS form used | None extra | Schedule A |

| Time to prepare | Minutes | Hours |

The math is simple once your numbers are gathered. Add up every itemizable expense. If the total beats your standard deduction, itemize. If it doesn’t, take the standard. There is no partial credit and no combining the two. Solid year-round tax planning services make this calculation effortless because your records stay organized from January forward instead of being reconstructed in a panic each April.

Red Flag Alert: The Mistakes That Cost People Thousands

Red Flag Alert: The most expensive mistake is assuming the standard deduction always wins because it is “so big now.” That assumption is exactly why homeowners in high-tax states overpay. If you own property with a mortgage in California, New York, or New Jersey, you should run the itemized math every single year before defaulting to the standard amount.

A second common error is failing to keep documentation for itemized deductions. If you itemize and get audited, the IRS wants proof. No receipt, no deduction. That means bank statements, canceled checks, Form 1098, written charity acknowledgments, and mileage logs where relevant. The deduction is only as strong as the paper trail behind it.

A third mistake is forgetting that married couples filing separately must both use the same method. If one spouse itemizes, the other cannot take the standard deduction, even if it would help them. This trap catches couples who file separately for student loan or income-based reasons without coordinating their deduction strategy.

The Bunching Strategy Competitors Rarely Mention

Here is an advanced move that sits right on the line between the two methods. If your itemized deductions land just below the standard deduction most years, you can “bunch” two years of charitable giving and elective expenses into a single tax year. You itemize big in year one, then take the standard deduction in year two. Over a two-year window, you capture more total deductions than you would by taking the standard amount both years.

Consider Robert and Lena, a married couple who normally give $8,000 to charity annually and have $22,000 in other itemizable expenses. That is $30,000 per year, exactly matching the standard deduction, so itemizing gives them no benefit. By donating $16,000 in one year through a donor-advised fund and $0 the next, their year-one itemized total hits $38,000 while year two they take the $30,000 standard. Across two years they deduct $68,000 instead of $60,000, an extra $8,000 in deductions worth roughly $1,760 at their bracket.

How to Decide Which Method to Use

Making the right call is a five-minute exercise if you have your documents ready. Follow these steps and you will never overpay from a bad default again.

5 Steps to Choose the Right Deduction Method

- Gather your Form 1098: Pull the mortgage interest statement your lender mailed in January. This is usually your biggest itemized number.

- Total your state and local taxes: Add state income tax withheld plus property taxes, then cap the combined figure at $10,000.

- Add charitable and medical: Sum documented charitable gifts and any medical costs above 7.5 percent of your AGI.

- Compare to your standard deduction: Match your filing status against the 2025 standard amounts ($15,000 single, $30,000 joint, $22,500 head of household).

- Take the larger number: Whichever total is higher becomes your deduction. If itemized wins, file Schedule A.

Key Takeaway: The entire decision rests on one comparison. If your itemized expenses exceed your standard deduction by even one dollar, itemizing saves you money. Never guess; always run the two numbers side by side.

California-Specific Considerations

California adds a wrinkle that catches many taxpayers off guard. The state does not follow federal deduction amounts. For 2025, California’s standard deduction is far smaller than the federal figure, roughly $5,540 for single filers and $11,080 for married couples filing jointly. That means a taxpayer might take the standard deduction on their federal return but come out ahead itemizing on their California return, or vice versa.

Even more important, California does not impose the federal $10,000 SALT cap on its own return. So while your property and income taxes are limited to $10,000 federally, California lets you deduct more of them at the state level. This mismatch means the smart move is often to itemize on your California return even when you take the standard deduction federally. Coordinating the two returns is where a lot of self-prepared filers leave money behind.

The Franchise Tax Board treats documentation seriously, and the state has grown more aggressive on residency and deduction audits. A recent California Office of Tax Appeals ruling reminded taxpayers that the burden of proof sits squarely on them. If you claim it, you must be able to prove it. Keep your California records as clean as your federal ones.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Can I switch between itemized and standard deductions from year to year?

Yes. There is no requirement to use the same method every year. Your circumstances change, and so should your choice. A year with a home purchase, a big medical event, or a large charitable gift might tip you into itemizing when you normally take the standard deduction. Reassess annually.

What happens if I itemize but cannot find my receipts in an audit?

The IRS can disallow any itemized deduction you cannot substantiate, and you would owe the additional tax plus interest and potential penalties. This is why documentation matters so much when you itemize. The standard deduction carries no such risk because it requires no proof. When in doubt, keep every receipt, statement, and acknowledgment for at least three years.

Does taking the standard deduction mean I lose all my write-offs?

No. Certain valuable deductions live “above the line” and are available whether you itemize or not. These include contributions to a traditional IRA, student loan interest, health savings account contributions, and the self-employment tax deduction. So even a standard-deduction filer can still capture significant tax breaks separately.

I’m self-employed. Does the deduction choice affect my business write-offs?

Not at all. Business expenses are deducted on Schedule C entirely separately from the standard versus itemized decision, which only concerns your personal deductions. A freelancer deducts their home office, equipment, and mileage on Schedule C, then still chooses between standard and itemized for personal items like mortgage interest and charity.

The bottom line is refreshingly simple: run both numbers every year, keep your records tight, and never let filing software make a five-figure decision for you on autopilot.

Book Your Tax Strategy Session

If you have been defaulting to one deduction method without running the math, there is a real chance you have been overpaying for years. Our team will pull your documents, compare both methods across your federal and California returns, and recover every dollar you are legally owed. Stop guessing and start keeping what is yours. Click here to book your consultation now.