Meta description: How s corp stock differs from c corp can change your tax bill, control, and exit value. Learn the real traps and the clean fixes California owners use.

Most owners think “stock is stock.” It isn’t. The way how s corp stock differs from c corp shows up in real life is not a legal trivia question, it is a money question. It changes who can invest, how you split profits, what happens when you sell, and how painful your California compliance becomes.

If you are building a business you want to fund, transfer to family, or sell, your stock structure is either a tool or a trap. Pick the wrong structure and you can accidentally disqualify an S election, trigger a built-in gains problem later, or create a shareholder agreement that cannot do what you need it to do.

Quick answer: what changes when stock is S Corp vs C Corp?

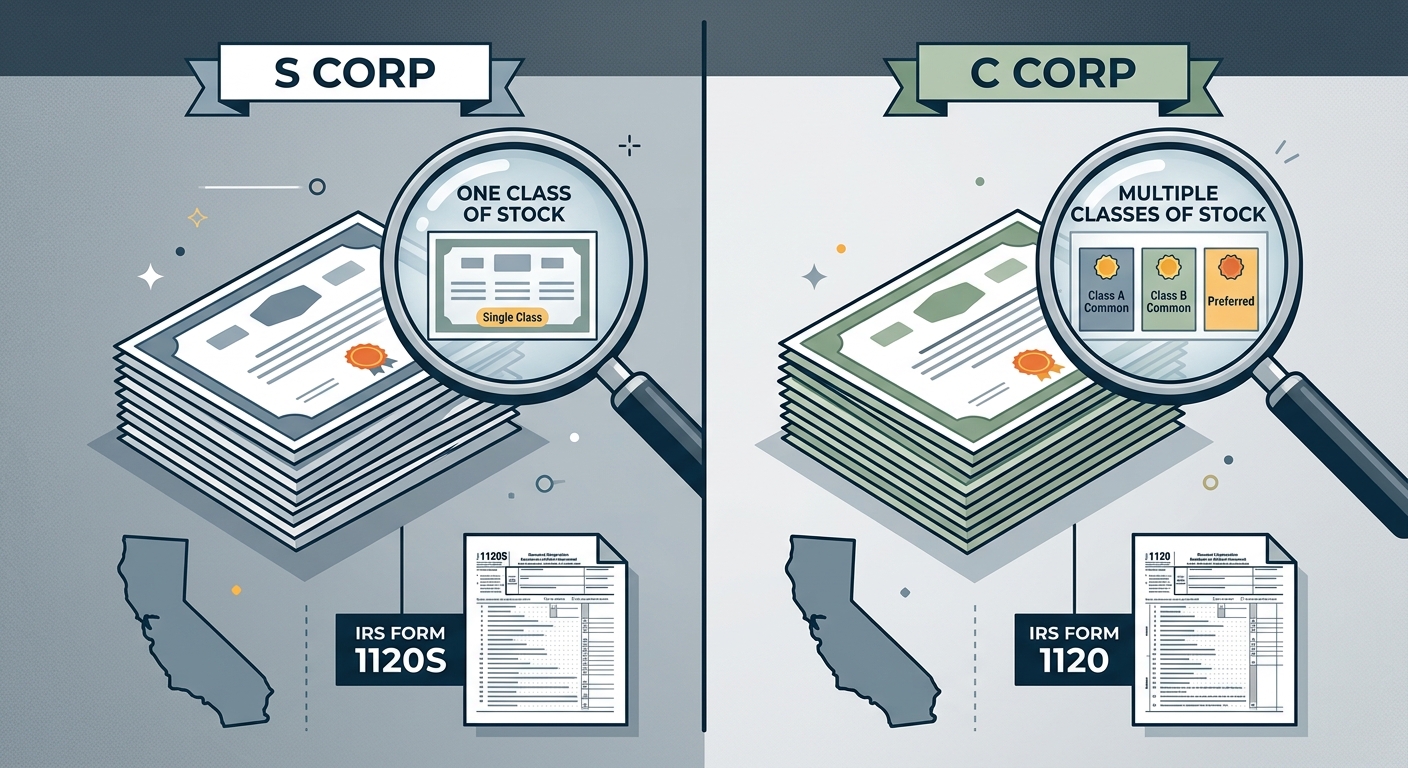

How s corp stock differs from c corp comes down to flexibility. An S Corp is generally limited to one class of stock (in plain English: you cannot create different economic deals across shareholders), has tighter shareholder eligibility rules, and pushes income through to owners’ personal tax returns. A C Corp can issue multiple classes of stock, bring in more types of investors, and pays its own federal corporate income tax, with owners taxed again on dividends.

This information is current as of 5/7/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

What “one class of stock” actually means (and why it breaks deals)

The biggest practical difference in how s corp stock differs from c corp is the “one class of stock” rule. People hear that and assume it means “only common stock.” Not exactly. An S Corp can have voting and nonvoting shares, but it generally cannot have shares with different distribution or liquidation rights.

Plain English definition

One class of stock means every share must have the same economic rights. If you own 10% of the shares, you must receive 10% of distributions, and you must be allocated 10% of profits and losses (subject to your basis and other pass-through rules). You cannot write a custom deal that gives one investor a preferred return, guaranteed distributions, or a liquidation preference that changes the economics.

What breaks the S Corp rule in the real world

- Investor prefers a preferred return: “I get my money back first, then we split.” That is a second economic class in substance.

- Founder wants to split cash differently than ownership: Common in spouses, partners, and family businesses. S Corp does not tolerate disproportionate distributions.

- Debt that acts like equity: A shareholder note with payment terms tied to profits can be treated as a second class. The regulations focus on whether an instrument creates different distribution rights.

Why this matters for California owners

If you are raising capital, acquiring another business, or issuing equity compensation, the one-class rule is where deals die. A California owner often wants flexibility for a key hire or a capital partner. That is exactly where a C Corp is structurally easier.

Key takeaway: When how s corp stock differs from c corp is mainly about “one class,” it means you can’t customize who gets what cash and when. If your plan requires custom economics, don’t force an S Corp to pretend it is a VC-ready structure.

Who can own the stock: eligibility rules that quietly kill S status

The next major point in how s corp stock differs from c corp is who is allowed to be a shareholder. A C Corp can generally have any number and type of shareholders (subject to securities laws). An S Corp cannot.

S Corp shareholder eligibility in plain English

Under the S Corp rules, shareholders are generally limited to individuals who are U.S. citizens or residents, certain estates, and certain trusts. Partnerships and corporations generally cannot own S Corp shares, and nonresident aliens are not allowed. The rules are in the Internal Revenue Code section on S corporation definitions (see IRC Section 1361).

Common California scenarios that trigger eligibility landmines

- Bringing in an LLC as an investor: Many investors and operators hold interests through LLCs. That typically does not work for S Corp ownership.

- Foreign spouse or parent: A nonresident alien shareholder can terminate S status. If your family is international, this is a serious planning point.

- Trust planning gone wrong: Trusts can be eligible, but only certain types and often with elections and timing rules.

What if you already have an S Corp and discover an ineligible owner?

If an ineligible shareholder is admitted, the S election can terminate. The fix may involve unwinding transfers, making trust elections, or seeking relief. This is not the kind of issue you want to “DIY” at year-end.

For owners who need proactive structuring and annual compliance guardrails, our entity formation services are built to keep your ownership documents and tax posture aligned, not just “filed.”

Key takeaway: A huge part of how s corp stock differs from c corp is shareholder eligibility. S Corps are picky. C Corps are not.

Where the tax pain shows up: dividends, distributions, and double taxation

Owners often focus on tax rates without understanding where the tax is actually triggered. That is a mistake. The tax engine is different, and it is one of the most expensive parts of how s corp stock differs from c corp.

C Corp tax flow: two layers when money leaves the company

A C Corp generally pays federal corporate income tax on its profits. If it distributes profits to shareholders as dividends, shareholders pay tax again on those dividends. That is the “double tax” everyone talks about. Dividends can also be subject to the Net Investment Income Tax in some cases (see IRS instructions for Form 8960).

Example: $300,000 of profit and $200,000 distributed

- Company earns $300,000.

- Company pays federal corporate tax at 21%: $63,000 (ignoring state for the moment).

- Company distributes $200,000 as dividends.

- Shareholder pays dividend tax (qualified dividends rates plus potential NIIT depending on facts).

Depending on your income level and California tax bracket, that second layer is not small.

S Corp tax flow: generally one layer, but payroll matters

An S Corp generally does not pay federal income tax at the entity level. Instead, profit flows through on a Schedule K-1 to shareholders, and they pay tax on their personal returns. Distributions are generally not subject to payroll tax, but shareholder-employees must take reasonable compensation for services. The payroll mechanics are governed by IRS employment tax rules (see IRS Publication 15).

Example: $300,000 of profit with $140,000 salary

- Owner runs payroll: $140,000 W-2.

- Remaining profit passes through: $160,000 on K-1.

- Payroll taxes apply to the W-2, not the distributions.

What this means for different taxpayer personas

- 1099 consultant with $220,000 net income: An S Corp can reduce self-employment tax exposure by splitting salary and distributions, if the salary is defensible.

- High-growth tech startup: A C Corp might make more sense if you need institutional investment and equity incentives that do not fit S Corp constraints.

- W-2 earner with a side LLC: S Corp savings can still be real, but only once profits are high enough to justify payroll and compliance.

Pro Tip: If you keep mixing up marginal tax rate with effective tax rate, use a tool before you assume a structure is “cheaper.” You can estimate overall federal exposure with this federal tax calculator.

Key takeaway: When people debate how s corp stock differs from c corp, they often miss where the second tax layer really hits: dividends for C Corps and payroll compliance for S Corps.

The control and governance differences investors actually care about

Stock differences are not only tax differences. If you want outside money, you need to understand the governance story behind how s corp stock differs from c corp.

C Corp: designed for outside capital

- Multiple classes: Preferred stock with liquidation preferences is standard.

- Option plans: Equity compensation is cleaner in a C Corp.

- Investor familiarity: Many institutional investors require a C Corp for legal and tax reasons.

S Corp: designed for closely held operating businesses

- Simple cap table: Works well for 1 to a handful of owners.

- Pass-through economics: Owners are taxed on profits whether or not cash is distributed, so distributions often need to cover tax bills.

- Less flexibility: Agreements must respect one-class economics.

California-specific friction: payroll and compliance cadence

California adds its own reality. A California S Corp has payroll filings, potential EDD registration, and the 1.5% franchise tax (minimum $800). A C Corp has its own California corporate tax regime. The structure you pick changes the compliance load and the “mistake surface area.” If you want a full strategic map of the S Corp landscape, see our comprehensive S Corp tax guide for California.

Key takeaway: The investor-ready side of how s corp stock differs from c corp is about flexibility in governance and economics, not just taxes.

Special situations and edge cases competitors gloss over

Most content on how s corp stock differs from c corp stops at the obvious. Here are the situations that create expensive surprises.

Edge case 1: You want disproportionate cash splits (family, partners, sweat equity)

If one partner is funding and another is operating, you may want different cash splits than ownership. In an LLC taxed as a partnership, you can often structure special allocations (with complex rules). In an S Corp, you cannot. If your business model needs custom economics, forcing an S Corp can create constant compliance stress and legal workarounds that do not hold up.

Edge case 2: Trust and estate planning, especially in California

If you expect to transfer ownership into trusts, you must plan for shareholder eligibility and elections. That planning is part corporate law, part tax compliance. If you ignore it, you can terminate S status at the worst time, like during a sale.

Edge case 3: You are planning an exit within 3 to 5 years

Buyers often prefer asset deals, sellers prefer stock deals, and the entity structure changes how the tax hits. A C Corp stock sale can be attractive for some reasons, but the double-tax trap can show up if you end up in an asset sale. Meanwhile, S Corp shareholders can often get a single layer of tax on gain, but the transaction structure matters.

Edge case 4: Multi-state expansion and nexus

If you operate in multiple states, you can create filing obligations and apportionment issues. The pass-through versus entity-level tax picture gets more complicated. Do not assume “S Corp always saves taxes” without running the multi-state math.

Key takeaway: The important part of how s corp stock differs from c corp is how it behaves under stress: new investors, trust transfers, and exits.

Common mistake that triggers expensive cleanup: DIY stock documents

This is the cleanest way to create a disaster: you form an entity online, download a generic set of bylaws, issue stock in a spreadsheet, and then “decide later” what the equity means. Then you try to file an S election, bring in an investor, or sign a buy-sell agreement. Everything breaks.

Red Flag Alert: “We’ll just do preferred returns in an S Corp”

If your agreement effectively gives someone a different right to distributions, you can violate the one-class rule. That can terminate S status retroactively. Retroactive tax changes are where penalties, interest, and amended returns stack up fast.

Red Flag Alert: admitting an ineligible shareholder

Admitting a nonresident alien or an entity shareholder into an S Corp is one of the fastest ways to terminate the election. Owners do this unintentionally when they transfer shares into an LLC for “asset protection” or into a trust without checking eligibility.

How to avoid it: a simple document-first workflow

- Define the endgame: lifestyle cash flow business, investor-backed growth, or sale in 3-7 years.

- Map ownership needs: equal splits or custom economics.

- Choose the entity tax posture: S Corp election or C Corp taxation.

- Draft documents that match tax rules: bylaws, shareholder agreement, stock ledger, equity comp plan.

- Set compliance cadence: payroll, estimated taxes, and California filings.

Key takeaway: The stock structure issues inside how s corp stock differs from c corp are usually created by documents that don’t match the tax election.

KDA Case Study: Business Owner Avoids a Broken S Election Before a $1.8M Sale

Jared owned a California-based software services firm doing about $950,000 in revenue with roughly $320,000 in annual profit. He had formed a corporation online years ago and had always heard “S Corp is cheaper,” so he filed an S election and moved on. The problem surfaced when a buyer offered $1.8M and wanted to review his cap table and shareholder agreement.

His documents included a side letter promising a former partner a preferred cash payout until a “capital balance” was repaid. In plain English, he had accidentally created second-class economics while operating as an S Corp. The buyer’s counsel flagged it immediately, and Jared was staring at a delayed closing plus the possibility that his S election could be challenged.

KDA rebuilt the ownership documentation to align with S Corp one-class requirements, cleaned up the side letter into a compliant debt agreement, and coordinated with his attorney so the deal terms stayed intact. We also ran an exit-tax model to show the difference between stock vs asset treatment under both S Corp and C Corp assumptions. The result: Jared preserved the S posture, avoided a reclassification fight, and kept the closing on schedule. Estimated tax avoided from “worst-case” restructuring: $46,000 in combined federal and California impact. Jared paid $6,500 for the advisory and cleanup work, generating a 7.1x first-year return when measured against avoided tax and deal delay costs.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

So which one should you choose in 2026? A decision framework

If you only remember one thing about how s corp stock differs from c corp, remember this: S Corp stock is built for simplicity and pass-through taxation, while C Corp stock is built for flexible economics and outside investment.

Choose an S Corp structure when

- You want a closely held operating business with simple ownership splits.

- You expect consistent profits and want pass-through treatment.

- You can run payroll and defend reasonable compensation.

- You do not need preferred returns or multiple classes of equity.

Choose a C Corp structure when

- You want to raise money from funds or complex investors.

- You need multiple classes of stock, preferred terms, or complex equity incentives.

- You plan to retain earnings for growth (and understand the accumulated earnings rules and planning needs).

What if you are an LLC today?

Many California owners start as LLCs and later elect S status once profits justify it. If you are self-employed or operating a small company, you will get more value by modeling the real cash flows and compliance costs first. If you are a founder chasing funding, a C Corp might be the right starting point even if it is not the lowest-tax option early on.

If you are a self-employed operator trying to decide what structure fits your income, risk, and growth plan, start with the guidance for business owners who need tax strategy that matches the way their company actually runs.

Key takeaway: Your “best” choice is the one that matches your cap table reality. That is the real lesson in how s corp stock differs from c corp.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

FAQ: fast answers owners ask after reading this

Can an S Corp have preferred stock?

Generally no, not if “preferred” changes distribution or liquidation rights. S Corps can have voting and nonvoting shares, but they cannot have separate economic classes without risking the election.

Can I bring in an LLC or a corporation as an investor in my S Corp?

Usually no. That is one reason businesses that want outside capital often move to C Corp structures.

If my S Corp makes money but doesn’t distribute cash, do I still pay tax?

Often yes. Pass-through income can be taxable to you even if cash is retained in the business. That is why many S Corps plan distributions to cover owners’ tax liabilities.

Do California rules change the stock differences?

The core stock rules are federal, but California taxes and compliance can change the practical cost of running each structure. California also has minimum taxes and different entity tax rates depending on the entity type.

Does “one class of stock” mean I can’t do equity compensation?

You can do equity compensation, but you have to design it so it does not create a second class of stock. Many complex incentive designs are easier in a C Corp.

Will changing from C Corp to S Corp fix this?

It can, but conversions have timing and tax traps. If you are considering a change, do it with a full model of shareholder eligibility, built-in gains risk, and your cap table.

Book Your Tax Strategy Session

If your shareholder structure is starting to feel like a legal puzzle and you are not sure whether you are accidentally violating S Corp rules, let’s clean it up before it costs you a deal or a tax year. Book a strategy session and we’ll map your ownership, tax posture, and next 12 months of compliance into a plan you can run. Click here to book your consultation now.

Mic drop: The IRS isn’t hiding the rules on stock classes, most owners just wait until an investor or buyer forces them to learn them.

Direct link to this blog: https://kdainc.com/how-s-corp-stock-differs-from-c-corp-the-control-tax-traps-california-owners-miss/