What Is Modified AGI and Why Does It Control Your Tax Benefits?

You filed your taxes, saw a number labeled “Adjusted Gross Income” on Line 11 of your 1040, and assumed that was the end of it. Then the IRS denied your Roth IRA contribution. Or your child tax credit got phased out. Or you discovered you don’t qualify for the Premium Tax Credit you were counting on. The reason? A number that doesn’t appear anywhere on your tax return: your Modified Adjusted Gross Income (MAGI).

Here’s the frustrating truth: how is modified agi calculated determines whether you get thousands in tax breaks or get shut out completely. And most taxpayers don’t learn this until it’s too late to fix it.

Quick Answer

Modified Adjusted Gross Income (MAGI) is your Adjusted Gross Income (AGI) with certain deductions added back. The IRS uses MAGI to determine eligibility for tax credits, deductions, and retirement account contributions. The specific calculation varies depending on which tax benefit you’re trying to claim, but it typically involves adding back items like foreign earned income exclusion, student loan interest deduction, IRA contributions, and passive losses.

Understanding the Foundation: What Is AGI?

Before you can understand Modified AGI, you need to grasp what Adjusted Gross Income actually is. Your AGI is your total income minus specific “above-the-line” deductions. Think of it as your gross income after the IRS lets you subtract certain expenses but before you claim the standard or itemized deduction.

Your AGI calculation starts with all your income sources:

- W-2 wages and salaries

- 1099 self-employment income

- Interest and dividend income

- Capital gains from investments

- Rental real estate income (Schedule E)

- Business income (Schedule C)

- Retirement account distributions

- Unemployment compensation

From this total, you subtract above-the-line deductions (also called adjustments to income), which include:

- Traditional IRA contributions (up to $7,000 for 2026, or $8,000 if age 50+)

- Self-employment tax deduction (50% of SE tax paid)

- Self-employed health insurance premiums

- Student loan interest (up to $2,500)

- HSA contributions

- Educator expenses

- Alimony paid (for divorces finalized before 2019)

The result is your AGI, which appears on Form 1040, Line 11. But this number is just the starting point for calculating MAGI.

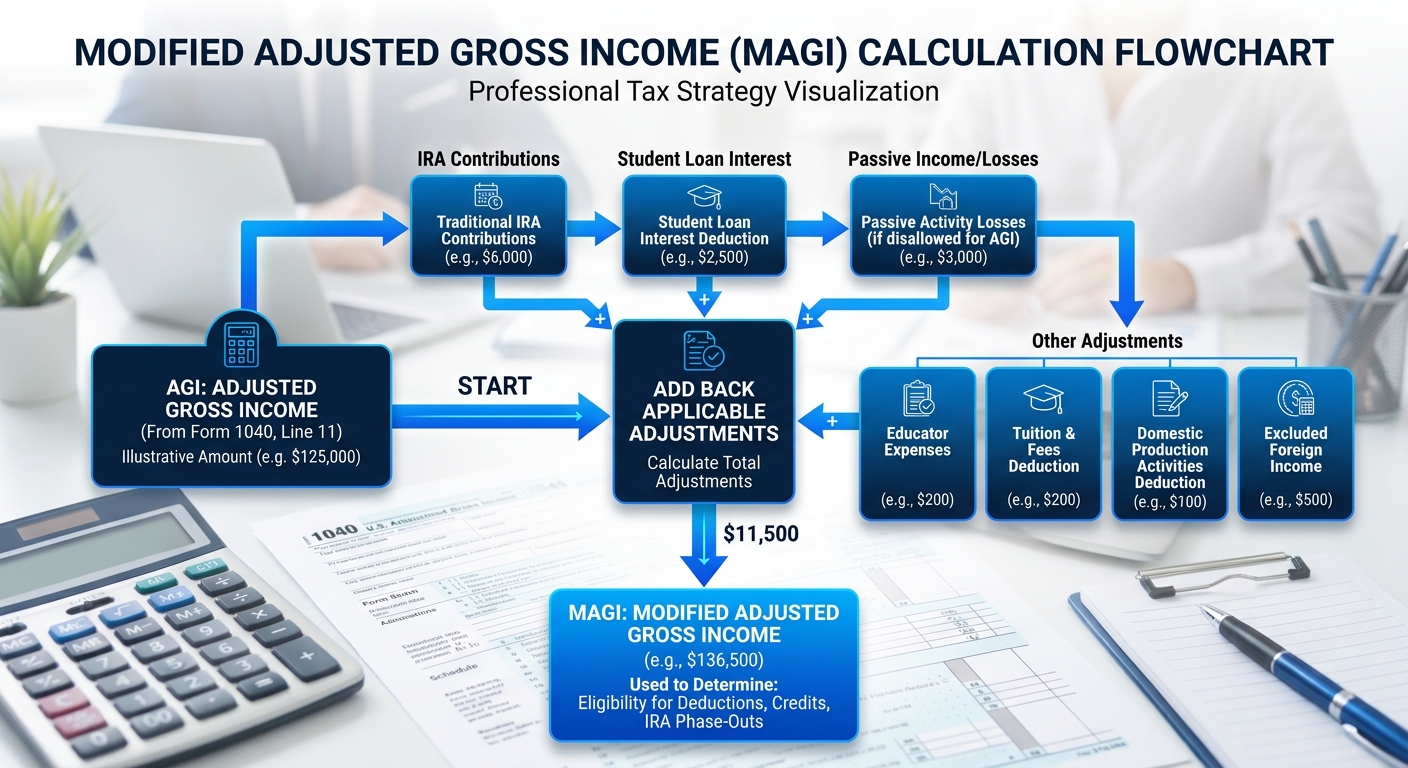

How Is Modified AGI Calculated? The Core Formula

Here’s where it gets complicated: there isn’t one universal MAGI calculation. The IRS uses different versions of MAGI for different tax benefits. However, the general concept remains consistent across all calculations.

The Basic MAGI Formula

MAGI = AGI + Add-Backs

The “add-backs” are specific deductions you took when calculating your AGI that the IRS wants to add back in for purposes of determining eligibility for certain tax benefits. The most common add-backs include:

- Traditional IRA deduction

- Student loan interest deduction

- Tuition and fees deduction (if applicable)

- Foreign earned income exclusion

- Foreign housing exclusion or deduction

- Excluded savings bond interest used for education

- Excluded employer adoption benefits

- Passive income or loss from rental real estate

- Half of self-employment tax

Step-by-Step: Calculating MAGI for Roth IRA Eligibility

Let’s walk through a real-world example. Sarah is a 1099 marketing consultant in San Diego who wants to contribute to a Roth IRA for 2026.

Step 1: Calculate Total Income

- 1099 consulting income: $95,000

- Interest income: $800

- Total income: $95,800

Step 2: Subtract Above-the-Line Deductions

- Self-employment tax deduction: $6,713

- Self-employed health insurance: $8,400

- SEP IRA contribution: $14,250

- Total adjustments: $29,363

Step 3: Calculate AGI

- $95,800 – $29,363 = $66,437 AGI

Step 4: Add Back Specific Items for Roth MAGI

For Roth IRA purposes, the IRS requires adding back any traditional IRA deduction (Sarah used a SEP IRA, so no add-back needed here), and certain exclusions. In Sarah’s case:

- AGI: $66,437

- Add-backs: $0 (no traditional IRA deduction or foreign income)

- Roth IRA MAGI: $66,437

Since Sarah’s MAGI is below the 2026 Roth IRA phase-out threshold ($146,000 for single filers), she can make the full $7,000 contribution. If her MAGI had been between $146,000 and $161,000, her contribution would be partially phased out. Above $161,000, she’d be completely ineligible.

Different MAGI Calculations for Different Tax Benefits

One of the most confusing aspects of MAGI is that the calculation changes depending on what you’re trying to claim. Here’s how how is modified agi calculated varies for major tax benefits:

MAGI for Roth IRA Contributions

Start with AGI and add back:

- Traditional IRA deduction

- Student loan interest deduction

- Tuition and fees deduction

- Foreign earned income exclusion

- Foreign housing exclusion

- Excluded savings bond interest

- Excluded employer adoption benefits

2026 Phase-Out Ranges:

- Single filers: $146,000 – $161,000

- Married filing jointly: $230,000 – $240,000

MAGI for Premium Tax Credit (ACA Subsidies)

Start with AGI and add back:

- Tax-exempt interest

- Non-taxable Social Security benefits

- Excluded foreign income

For the Premium Tax Credit, your MAGI must fall between 100% and 400% of the Federal Poverty Level. For a family of four in 2026, that’s roughly $31,200 to $124,800. If your MAGI exceeds these thresholds, you lose the subsidy entirely, which can mean $8,000+ in additional health insurance costs.

MAGI for Child Tax Credit

The Child Tax Credit begins phasing out at:

- $200,000 MAGI for single filers

- $400,000 MAGI for married filing jointly

For this credit, MAGI equals your AGI plus any foreign earned income exclusion and foreign housing exclusion. The credit reduces by $50 for each $1,000 (or fraction thereof) above the threshold.

MAGI for Deducting Traditional IRA Contributions

If you or your spouse are covered by a workplace retirement plan, your ability to deduct traditional IRA contributions phases out based on MAGI. For this purpose, MAGI is your AGI before subtracting the IRA deduction, plus certain exclusions.

2026 Phase-Out Ranges (if covered by workplace plan):

- Single filers: $77,000 – $87,000

- Married filing jointly: $123,000 – $143,000

MAGI for Medicare Part B and Part D Premiums (IRMAA)

High-income Medicare beneficiaries pay Income-Related Monthly Adjustment Amounts (IRMAA) based on their MAGI from two years prior. For your 2026 premiums, Medicare looks at your 2024 tax return.

For IRMAA purposes, MAGI equals your AGI plus tax-exempt interest income. The surcharges begin at $106,000 for single filers and $212,000 for joint filers, with additional tiers up to $500,000+.

Many retirees don’t realize that a one-time spike in income (like selling a rental property or taking a large IRA distribution) can trigger IRMAA surcharges costing $3,000+ annually for two years.

KDA Case Study: Real Estate Investor

Marcus, a 42-year-old real estate investor in Oakland, came to KDA after the IRS disallowed his $25,000 passive loss deduction from his rental properties. His W-2 income from his tech job was $135,000, and he reported $32,000 in rental losses across three properties.

The problem? Marcus’s MAGI exceeded the $100,000 threshold where passive loss deductions begin phasing out. By the time his MAGI hit $150,000, the entire $25,000 special allowance was gone.

What KDA Did:

We restructured Marcus’s tax strategy to reduce his MAGI below the critical $100,000 threshold:

- Maximized his 401(k) contribution from $15,000 to $23,500 (the 2026 limit)

- Set up a Health Savings Account and contributed the family maximum of $8,550

- Implemented a home office deduction for his side consulting work, creating $6,200 in additional above-the-line deductions

Results:

- Previous MAGI: $135,000

- New MAGI: $96,750

- Unlocked $25,000 passive loss deduction

- Tax savings in first year: $8,900

- Our fee: $3,000

- First-year ROI: 2.9x

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Why MAGI Matters More Than AGI for Tax Planning

Your AGI determines your standard or itemized deduction limitations and appears on your tax return. But your MAGI operates behind the scenes, controlling access to dozens of valuable tax benefits without ever appearing as a line item on Form 1040.

This creates a planning problem: most tax software calculates these limits automatically, but by the time you’re filing your return, it’s too late to do anything about it. Strategic tax planning requires understanding how is modified agi calculated for your specific situation and making proactive moves throughout the year.

Consider working with our tax planning team to develop a year-round MAGI management strategy tailored to your financial goals.

Common Mistakes That Inflate Your MAGI

Red Flag Alert: Ignoring the Two-Year IRMAA Lookback

Retirees often trigger massive Medicare premium increases by forgetting that IRMAA calculations use your MAGI from two years earlier. If you sell a business or rental property in 2026, your 2028 Medicare premiums could increase by $3,000+ annually. Strategic timing of major income events can save thousands over retirement.

Red Flag Alert: Mixing Up Roth Conversion MAGI

Many taxpayers assume Roth conversions don’t affect MAGI calculations. Wrong. A Roth conversion increases your AGI (and therefore your MAGI) for that year, potentially disqualifying you from credits and deductions you were counting on. A $50,000 Roth conversion could cost you the Premium Tax Credit worth $8,000, turning a smart move into a $8,000 mistake.

Red Flag Alert: Passive Loss Phase-Out Cliff

The passive loss special allowance doesn’t phase out gradually. It drops by $0.50 for every dollar of MAGI over $100,000. If your MAGI is $149,999, you can deduct $1. At $150,000, you get nothing. Being $1 over the threshold costs you up to $25,000 in deductions. A $500 HSA contribution could save you $8,750 in taxes by keeping you under the cliff.

Pro Tip: Time Capital Gains to Manage MAGI

Capital gains from selling stocks or real estate increase your AGI and MAGI. If you’re close to a phase-out threshold, consider spreading sales across multiple tax years. Selling $100,000 in appreciated stock in one year might push you over the Roth IRA limit. Selling $50,000 in 2026 and $50,000 in 2027 keeps both years’ MAGI under the threshold, preserving $14,000 in Roth contributions ($7,000 × 2 years).

Proactive Strategies to Lower Your MAGI

Since MAGI controls access to valuable tax benefits, reducing it becomes a high-leverage tax planning strategy. Here are the most effective approaches:

Maximize Retirement Contributions

401(k) and 403(b) contributions reduce your AGI dollar-for-dollar (and therefore your MAGI). For 2026:

- Standard contribution limit: $23,500

- Age 50+ catch-up: Additional $7,500

- Total possible: $31,000

If you’re self-employed, a Solo 401(k) or SEP IRA offers even larger deductions (up to $69,000 for 2026, or $76,500 if age 50+).

Fund a Health Savings Account

HSA contributions are above-the-line deductions that reduce both AGI and MAGI. 2026 limits:

- Self-only coverage: $4,300

- Family coverage: $8,550

- Age 55+ catch-up: Additional $1,000

HSAs offer triple tax benefits: deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. For high-MAGI taxpayers, the MAGI reduction can unlock thousands in additional tax benefits.

Defer Income When Possible

If you’re a business owner or 1099 contractor, timing when you receive income can shift it between tax years. Strategies include:

- Delaying December invoicing until January (moves income to next year)

- Using a fiscal year accounting method (if eligible)

- Deferring bonuses or distributions to the following tax year

Accelerate Deductions

Above-the-line deductions reduce MAGI. Consider:

- Making January’s mortgage payment in December (if you itemize and pay points)

- Prepaying state estimated tax payments (subject to $10,000 SALT cap)

- Accelerating business expenses into the current year

- Making charitable contributions through a donor-advised fund

How MAGI Affects California Taxpayers Specifically

California uses federal AGI as the starting point for state tax calculations but makes its own adjustments. Understanding how is modified agi calculated at the federal level is crucial because many California tax credits and benefits tier off your federal MAGI.

For example, California’s Earned Income Tax Credit (CalEITC) uses federal MAGI thresholds. The California Premium Assistance Subsidy for health insurance also relies on federal MAGI calculations. If your federal MAGI is too high, you lose both the federal Premium Tax Credit and California’s additional subsidy.

California residents also face unique planning challenges:

- High state income taxes (up to 13.3%) make MAGI management even more valuable

- Capital gains from stock options and RSUs (common in tech) can spike MAGI unexpectedly

- Rental property income is significant in expensive markets like SF and LA, triggering passive loss limitations

For detailed California-specific tax strategies, see our California Business Owner Tax Strategy Hub.

Special Situations and Edge Cases

What Happens If You’re Just Over the MAGI Threshold?

Being $1 over a hard MAGI threshold can cost you thousands. For example, exceeding the Roth IRA MAGI limit by $1 means your contribution is an “excess contribution” subject to a 6% penalty annually until corrected. That’s $420 per year on a $7,000 contribution.

If you discover you’re over the threshold after making a contribution, you have until the tax filing deadline (including extensions) to withdraw the excess contribution plus any earnings to avoid the penalty.

How Does MAGI Work for Married Couples Filing Separately?

Married Filing Separately (MFS) taxpayers face the harshest MAGI thresholds. For example:

- Roth IRA contributions phase out between $0 and $10,000 MAGI (yes, zero)

- Traditional IRA deduction phases out starting at just $0 MAGI if either spouse is covered by a workplace plan

- Most education credits are unavailable regardless of income

The IRS designed these rules to prevent high-income married couples from gaming the system by filing separately.

Do IRA Distributions Count Toward MAGI?

Yes. Traditional IRA and 401(k) distributions are included in your AGI (and therefore your MAGI). This creates a trap for retirees who take large distributions without considering the impact on Medicare premiums, the taxation of Social Security benefits, and other MAGI-based calculations.

Roth IRA qualified distributions, however, are tax-free and don’t increase your MAGI, which is one reason Roth conversions during lower-income years can be so valuable.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Is MAGI the Same as Taxable Income?

No. Taxable income is your AGI minus either the standard deduction ($14,600 for single filers in 2026) or itemized deductions. MAGI is usually higher than your AGI because it adds certain deductions back. The hierarchy is typically: MAGI > AGI > Taxable Income.

Where Do I Find My MAGI on My Tax Return?

You don’t. MAGI doesn’t appear as a line item on Form 1040. You must calculate it manually based on which tax benefit you’re evaluating. Start with your AGI (Line 11 of Form 1040) and add back the specific items required for that particular MAGI calculation.

Can I Lower My MAGI After the Tax Year Ends?

Your options are limited but not zero. You can make deductible IRA contributions until the tax filing deadline (April 15, 2027, for tax year 2026). You can also make HSA contributions for the prior year up until the filing deadline. However, most strategies require action during the tax year itself.

Does Social Security Income Count Toward MAGI?

It depends on the calculation. For most MAGI purposes (like Roth IRA eligibility), only taxable Social Security benefits are included in your AGI and therefore your MAGI. For the Premium Tax Credit calculation, tax-exempt Social Security is added back into MAGI. For IRMAA calculations, Social Security is already in your AGI, so it counts toward the MAGI threshold.

The Bottom Line: MAGI Controls Your Tax Planning Opportunities

Understanding how is modified agi calculated is essential for anyone trying to maximize Roth IRA contributions, claim education credits, qualify for healthcare subsidies, or deduct passive real estate losses. The calculation varies by tax benefit, but the principle remains the same: MAGI is your AGI with certain deductions added back.

The taxpayers who save the most aren’t the ones who find clever deductions after the year ends. They’re the ones who understand their MAGI thresholds in advance and make strategic moves throughout the year to stay under them.

Key Takeaway: Every dollar you reduce your MAGI can unlock multiple tax benefits simultaneously. A $10,000 increase in your 401(k) contribution doesn’t just save you $2,200 in federal tax (at the 22% bracket). It could also preserve a $7,000 Roth IRA contribution, maintain a $2,000 Child Tax Credit, or unlock a $25,000 passive loss deduction. The compounding effect makes MAGI management one of the highest-ROI tax strategies available.

Ready to Take Control of Your MAGI?

Most taxpayers discover their MAGI problems when it’s too late to fix them. You’re reading about your disallowed Roth contribution in a CP2000 notice, or you’re watching your Premium Tax Credit evaporate because you earned $1,000 too much. By then, the tax year is over and your options are limited.

The alternative? Work with a tax strategist who monitors your MAGI year-round and helps you make adjustments before December 31. Whether you’re a W-2 employee trying to maximize Roth contributions, a business owner managing passive rental losses, or a retiree trying to avoid IRMAA surcharges, proactive MAGI planning saves thousands.

Stop leaving tax benefits on the table because you didn’t know how the calculation worked. Book your personalized tax strategy session now and let’s build a MAGI management plan that protects your eligibility for every credit and deduction you deserve.

This information is current as of 4/10/2026. Tax laws change frequently. Verify updates with the IRS or a qualified tax professional if reading this later.