The Missing Tax Form That Could Trigger an IRS Audit

You pulled $3,000 from your HSA last year to cover medical bills. Fast forward to tax season, and you’re staring at a 1040 wondering why the IRS is asking about distributions you don’t remember reporting. Here’s the truth most taxpayers miss: every dollar you withdraw from a Health Savings Account generates a paper trail, and if you don’t report it correctly, you could face penalties that wipe out years of tax savings.

The IRS doesn’t just trust that your HSA withdrawals were for qualified medical expenses. They require documentation through Form 1099-SA, and if you don’t know how to get a 1099 SA or what to do with it once you have it, you’re setting yourself up for an expensive mistake.

Quick Answer: What Is Form 1099-SA and How Do You Get It?

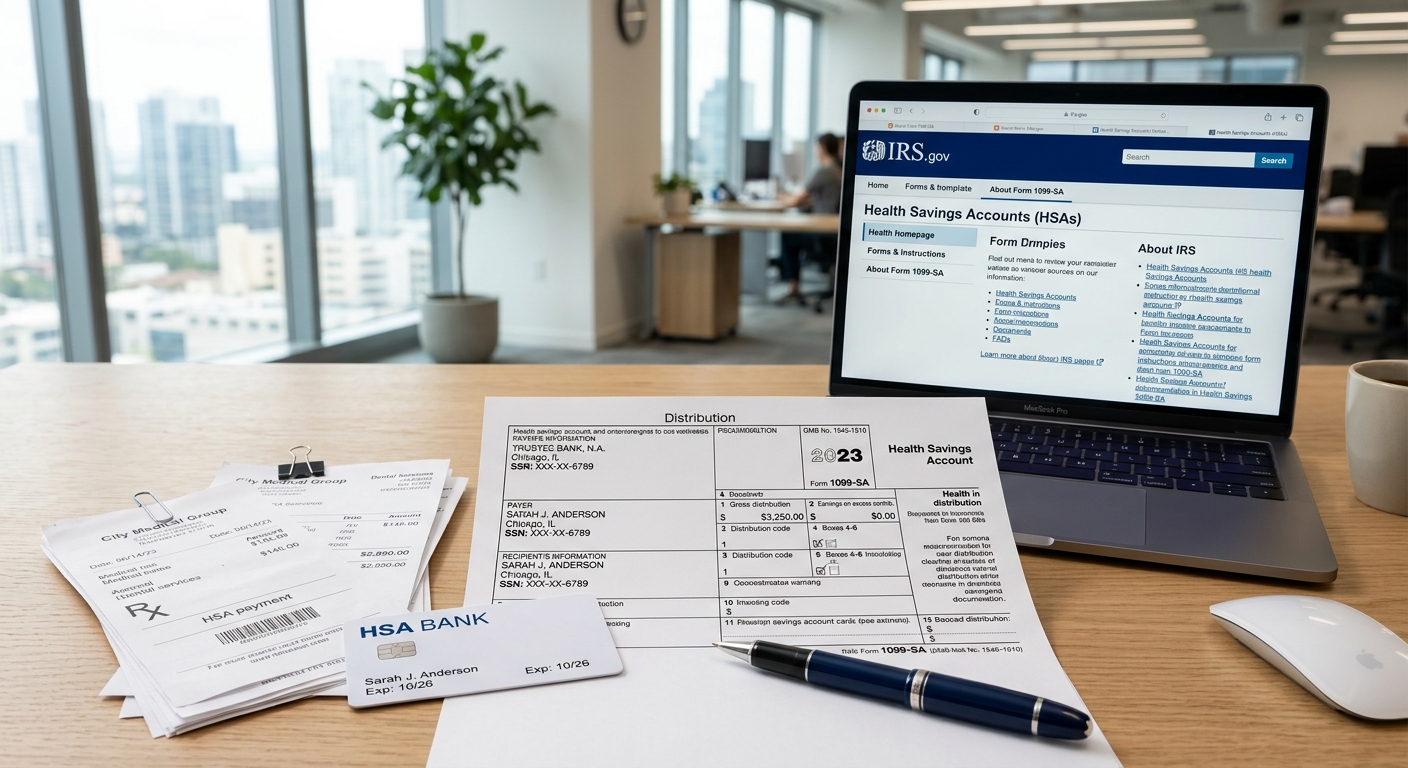

Form 1099-SA is an IRS tax document that reports distributions from your Health Savings Account, Archer MSA, or Medicare Advantage MSA. Your HSA administrator (bank, credit union, or benefits provider) is required to send you this form by January 31st if you took any distributions during the previous tax year. You’ll receive it automatically by mail or through your online account portal, and you must use the information on this form to accurately report HSA withdrawals on your tax return using Form 8889.

Why Form 1099-SA Matters More Than You Think

Here’s what happens when you withdraw money from an HSA: your administrator reports that distribution directly to the IRS using Form 1099-SA. The IRS then matches that report against your tax return. If the numbers don’t align, or if you fail to report the distribution altogether, you trigger an automatic mismatch notice (CP2000) that can lead to penalties, interest, and a potential audit.

For 2026, HSA contribution limits increased to $4,400 for individuals and $8,750 for families, with an additional $1,000 catch-up contribution allowed for those 55 and older. These higher limits mean more taxpayers are using HSAs strategically, but they also mean more potential for costly reporting errors if you don’t understand the 1099-SA process.

The Three-Way Tax Trap

Most taxpayers don’t realize that HSA money gets taxed THREE different ways if you mess up:

- Ordinary income tax on non-qualified distributions (your full marginal rate)

- 20% additional penalty if you’re under 65 and use HSA funds for non-medical expenses

- Interest and accuracy penalties from the IRS if you fail to report distributions correctly

A $5,000 non-qualified withdrawal at a 24% tax bracket costs you $1,200 in income tax, plus $1,000 in penalties, plus potential IRS interest. That’s $2,200+ in avoidable costs because of a missing or misreported 1099-SA.

How to Get Your 1099-SA: Step-by-Step Process

Getting your Form 1099-SA isn’t complicated, but timing and method matter. Here’s exactly how the process works:

Step 1: Identify Your HSA Administrator

Your HSA administrator is the financial institution that holds your account. Common providers include:

- Fidelity HSA

- HealthEquity

- Optum Bank

- HSA Bank

- Lively

- Bank of America HSA

Check your HSA debit card or login portal to confirm who manages your account. This is who will issue your 1099-SA.

Step 2: Understand the January 31st Deadline

By law, your HSA administrator must send Form 1099-SA by January 31st following any year in which you took distributions. If you took money out of your HSA in 2025, you should receive your 1099-SA by January 31, 2026.

The form will be mailed to your address on file OR made available electronically if you opted into paperless delivery.

Step 3: Access Your Form Online or by Mail

Option A: Online Portal Access

- Log into your HSA provider’s website or mobile app

- Navigate to “Tax Documents,” “Tax Forms,” or “Year-End Statements”

- Download your 1099-SA as a PDF (usually available by mid-January)

- Save a digital copy for your records

Option B: Postal Mail

If you haven’t opted into electronic delivery, your administrator will mail a paper copy to your address on file. This typically arrives between January 20-31.

Step 4: Verify Your Information Immediately

When you receive your 1099-SA, check these critical fields:

- Box 1 (Gross Distribution): Total amount withdrawn from your HSA during the year

- Box 2 (Earnings on Excess Contributions): Usually blank unless you over-contributed

- Box 3 (Distribution Code): Code 1 = Normal distribution; Code 2 = Excess contribution; etc.

- Box 4 (FMV on Date of Death): Only applies if account holder died

- Your Name, Address, SSN: Must match your tax return exactly

If any information is wrong, contact your HSA administrator immediately. Corrections can take 2-4 weeks, and you cannot file your tax return accurately without the correct 1099-SA data.

Step 5: What to Do If You Don’t Receive Your 1099-SA

If February 15th arrives and you still don’t have your form:

- Check your online account first (most providers post forms before mailing)

- Verify your mailing address with your HSA administrator

- Call customer service and request a duplicate copy

- Download from the portal if available electronically

Don’t wait until April to track this down. The IRS requires you to report HSA distributions whether you have the form or not, so delaying puts you at risk of filing errors.

Understanding What’s on Your 1099-SA (And What It Means for Your Taxes)

Form 1099-SA contains critical data you’ll need to transfer to Form 8889 (the HSA tax reporting form). Here’s how to read each section:

Box 1: Gross Distribution

This is the total dollar amount you withdrew from your HSA during the tax year. It includes:

- Debit card purchases at pharmacies and doctor’s offices

- Reimbursements you requested for out-of-pocket medical expenses

- Cash withdrawals (even if you later used them for medical costs)

- Any mistaken or non-qualified distributions

Example: Maria withdrew $2,800 for dental work, $1,200 for prescriptions, and accidentally used her HSA debit card for $150 in groceries. Her Box 1 shows $4,150 total distribution.

Box 3: Distribution Code

This single-digit code tells the IRS what type of distribution occurred:

- Code 1: Normal distribution (most common)

- Code 2: Excess contribution distribution

- Code 3: Disability distribution

- Code 4: Death distribution (beneficiary receiving funds)

- Code 5: Prohibited transaction

- Code 6: Corrections of administrative errors

Most taxpayers will see Code 1. If you see Code 5 (prohibited transaction), consult a tax professional immediately as your entire HSA may lose its tax-advantaged status.

How to Report Your 1099-SA on Your Tax Return

Receiving the 1099-SA is only half the battle. You must correctly report it on your tax return using Form 8889: Health Savings Accounts. Here’s the exact process:

Form 8889 Reporting Requirements

Part II: HSA Distributions

- Line 14a: Enter the total distribution amount from 1099-SA Box 1

- Line 14b: Enter the amount you used for qualified medical expenses (requires documentation)

- Line 14c: Subtract Line 14b from 14a (this is your taxable distribution)

- Line 17: Calculate the 20% additional tax if applicable

The critical question: How do you prove qualified medical expenses?

Documentation You Need to Keep

The IRS doesn’t require you to submit receipts with your return, but you must keep them for at least 3 years in case of audit. Acceptable documentation includes:

- Itemized receipts from medical providers (not just credit card statements)

- Explanation of Benefits (EOB) forms from your insurance

- Prescription labels and pharmacy receipts

- Mileage logs for medical travel (67 cents per mile in 2026)

- Invoices for qualifying equipment (blood pressure monitors, diabetic supplies, etc.)

Red Flag Alert: Generic receipts that say “medical services” without itemization won’t hold up in an audit. You need specific dates, provider names, and service descriptions.

Common Mistakes That Trigger IRS Notices

Mistake 1: Not Reporting the 1099-SA at All

Some taxpayers assume that if they used HSA money for medical expenses, they don’t need to report anything. Wrong. The IRS receives a copy of your 1099-SA and expects to see those distributions on your Form 8889. Failing to file Form 8889 when you have distributions is an automatic red flag.

Mistake 2: Claiming All Distributions as Qualified Without Proof

Just because you withdrew $5,000 doesn’t mean you can claim all $5,000 as qualified expenses without documentation. If you withdrew funds but didn’t spend them on qualified medical expenses in the same year, you owe tax and penalties.

Mistake 3: Mixing Personal and Medical Expenses

Using your HSA debit card for non-medical purchases (even accidentally) creates a taxable event. Some taxpayers don’t realize that using an HSA card at Target for both prescriptions and groceries in one transaction requires them to separate qualified from non-qualified amounts.

Mistake 4: Forgetting State Tax Implications

California-Specific Alert: California does NOT recognize HSAs for state tax purposes. While your HSA contributions are federally tax-deductible, California requires you to add them back as income on your state return. This means:

- Federal return: HSA contributions reduce taxable income

- California return: Add HSA contributions back on Schedule CA (540)

- Distributions: California taxes you on earnings that grew in the HSA

For California residents, maintaining separate federal and state HSA tracking is essential to avoid overpayment or underpayment penalties.

What Happens If You Lost Your Receipts?

You withdrew $3,500 from your HSA in 2025 for medical expenses, but you can’t find all the receipts. What now?

Reconstruction Strategies

- Request EOBs from your insurance company (usually available for 2-3 years)

- Contact medical providers directly for duplicate itemized statements

- Review your HSA transaction history (often shows merchant names and dates)

- Check credit card statements to identify medical vendors, then request receipts

- Use prescription history from your pharmacy (CVS, Walgreens keep multi-year records)

If you absolutely cannot document the full amount, you must report the undocumented portion as taxable income on Line 14c of Form 8889 and pay the applicable tax and 20% penalty.

Pro Tip: Many HSA administrators offer receipt storage tools within their platforms. Upload receipts immediately after each medical purchase to avoid this problem in future years.

Special Situations and Edge Cases

What If You Changed HSA Providers Mid-Year?

If you transferred your HSA from one bank to another, you may receive multiple 1099-SA forms. A proper trustee-to-trustee transfer should NOT generate a taxable distribution, but errors happen.

Verification checklist:

- Confirm transfer was completed as trustee-to-trustee (not a withdrawal and redeposit)

- Ensure your old provider coded the transfer correctly on their 1099-SA

- Report the rollover on Form 8889, Part I, Line 10

- Keep transfer documentation for 7 years

What If You’re Over 65?

Once you turn 65, the 20% penalty for non-qualified distributions disappears. You can use HSA funds for anything (groceries, travel, living expenses), but you’ll still owe ordinary income tax on non-medical withdrawals.

This makes HSAs an excellent supplemental retirement account for high-income earners. You get the deduction going in, tax-free growth, and penalty-free access after 65 even for non-medical uses.

What If You Over-Contributed?

If you contributed more than the annual limit ($4,400 individual / $8,750 family for 2026), you face a 6% excise tax on the excess amount every year it remains in the account.

Your options:

- Withdraw the excess plus earnings before your tax deadline (including extensions)

- Apply the excess toward next year’s contribution limit

- File Form 5329 to report and pay the 6% penalty

If you withdraw excess contributions before the deadline, your HSA administrator will send you a 1099-SA with Code 2 in Box 3.

KDA Case Study: Self-Employed Consultant

Marcus, a 42-year-old self-employed technology consultant earning $125,000 annually, switched to a high-deductible health plan in 2025 to open an HSA. He contributed the maximum $4,400 and withdrew $3,200 throughout the year for dental work, prescriptions, and chiropractor visits.

When January 2026 arrived, Marcus couldn’t find his 1099-SA and had lost most of his medical receipts. He called KDA in a panic, worried about missing the filing deadline.

What KDA Did:

- Helped Marcus retrieve his 1099-SA electronically through his HSA provider portal

- Reconstructed $2,850 in qualified expenses using insurance EOBs and pharmacy records

- Properly reported $350 as a non-qualified distribution (couldn’t document it)

- Filed Form 8889 accurately, avoiding IRS mismatch notices

- Set up a receipt tracking system for future years

Tax Result: Marcus paid $84 in tax plus $70 in penalties on the $350 undocumented distribution, but avoided a potential audit and thousands in penalties if he’d failed to report the 1099-SA entirely. Total KDA fee: $450. Total avoided penalties: estimated $1,200-$2,000.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How to Avoid 1099-SA Problems in Future Years

Create a Year-Round Documentation System

Don’t wait until tax season to organize your HSA records. Implement these habits:

- Photograph receipts immediately using your smartphone

- Upload to your HSA provider’s platform or use a dedicated folder (Google Drive, Dropbox)

- Label files clearly: “2026-03-15_Dentist_$450.pdf”

- Keep a simple spreadsheet tracking date, provider, amount, and purpose

- Reconcile quarterly instead of waiting until year-end

Opt Into Electronic Delivery

Paper forms get lost, delayed, or sent to old addresses. Most HSA providers allow you to opt into electronic tax document delivery, which means:

- Earlier access (often 1-2 weeks before mailing)

- No risk of postal delays

- Easy storage and retrieval

- Environmental benefits

Log into your HSA account settings and enable “Electronic Tax Documents” or “Paperless Tax Forms” now.

Understand Qualified Medical Expenses

Not all health-related expenses qualify for tax-free HSA withdrawals. Here’s what’s allowed versus what triggers taxes:

Qualified Expenses (Tax-Free):

- Doctor and dentist visits

- Prescription medications

- Medical equipment (crutches, blood pressure monitors)

- Vision care (eye exams, glasses, contacts, LASIK)

- Mental health services (therapy, psychiatrist visits)

- Chiropractic and acupuncture

- Lab fees and diagnostic tests

- Ambulance and hospital services

Non-Qualified Expenses (Taxable + 20% Penalty):

- Gym memberships (unless prescribed for specific medical condition)

- Vitamins and supplements (unless prescribed)

- Cosmetic procedures (unless medically necessary)

- Over-the-counter medications without prescription

- Health club dues

- Insurance premiums (except COBRA, long-term care, and Medicare in some cases)

When in doubt, check IRS Publication 502 for the complete list of qualified medical expenses.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About Form 1099-SA

Do I Need a 1099-SA If I Only Made Contributions and No Withdrawals?

No. Form 1099-SA only reports distributions (money coming OUT of your HSA). If you didn’t take any withdrawals during the year, you won’t receive a 1099-SA. However, you’ll still receive Form 5498-SA, which reports your contributions.

What’s the Difference Between Form 1099-SA and Form 5498-SA?

Form 1099-SA reports distributions (withdrawals) and arrives by January 31st. Form 5498-SA reports contributions and arrives by May 31st. You need the 1099-SA to file your tax return, but the 5498-SA comes after most people have already filed (it’s informational only).

Can I File My Tax Return Before Receiving My 1099-SA?

Technically yes, but it’s risky. You can check your HSA account’s online transaction history to see your total distributions for the year and report that amount on Form 8889. However, if the official 1099-SA later shows a different number, you’ll need to file an amended return. Best practice: wait for the actual form.

What If My 1099-SA Shows the Wrong Amount?

Contact your HSA administrator immediately and request a corrected 1099-SA (called a 1099-SA-C). Do not file your tax return with incorrect information. The correction process typically takes 2-4 weeks, and you may need to file for an extension if it delays your filing.

Do I Still Need to Report My 1099-SA If All Distributions Were for Qualified Medical Expenses?

Yes. Even if 100% of your distributions were for qualified medical expenses and you owe no tax, you still must file Form 8889 with your tax return to report the distributions. The IRS matches your 1099-SA against your return and will send you a CP2000 notice if they don’t see the corresponding Form 8889.

California-Specific Considerations

California taxpayers face unique HSA reporting requirements that can create confusion and double-taxation if not handled correctly.

California Does Not Conform to Federal HSA Rules

While HSAs are tax-advantaged at the federal level, California treats them as regular taxable accounts. This means:

- Contributions: NOT deductible on California state return

- Earnings: Subject to California state tax as they accumulate

- Distributions: Partially taxable to the extent of earnings

How to Report HSAs on California Form 540

- Schedule CA, Line 8: Add back your HSA contribution deduction from federal return

- Schedule CA, Part II: Report HSA distributions and calculate California-specific taxable amount

- Form 3849: May be required if you have significant HSA earnings

Many tax software programs don’t handle California HSA adjustments correctly, leading to overpayment or underpayment. If your HSA has grown significantly, professional tax preparation is worth the investment.

This information is current as of 4/24/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Advanced HSA Tax Strategies for High Earners

If you’re using your HSA strategically, understanding Form 1099-SA becomes even more critical as you optimize for long-term wealth building.

The “Stealth IRA” Strategy

Many high-income taxpayers use HSAs as supplemental retirement accounts by:

- Contributing the maximum each year ($4,400 individual / $8,750 family for 2026)

- Paying medical expenses out-of-pocket instead of withdrawing from the HSA

- Investing HSA funds in mutual funds or ETFs for tax-free growth

- Saving receipts for decades

- Withdrawing tax-free reimbursements in retirement (no statute of limitations)

Example: Sarah contributes $8,750 annually to her family HSA from age 35-65 (30 years). She pays $50,000 in medical expenses out-of-pocket during that time but never withdraws from the HSA. At 7% average annual return, her HSA grows to approximately $875,000. She can withdraw the original $50,000 in medical expenses tax-free anytime, and the remaining balance grows tax-free until withdrawal for medical expenses or penalty-free withdrawal after age 65.

This strategy requires meticulous record-keeping of all medical receipts and zero 1099-SA forms until retirement, when you’ll receive multiple forms for strategic withdrawals.

Spousal HSA Coordination

Married couples with family HSA coverage can split contributions between two HSAs (one per spouse) even though only one can contribute the family maximum. This creates estate planning advantages and separate 1099-SA reporting:

- Each spouse receives their own 1099-SA for their account’s distributions

- Allows for separate investment strategies and risk tolerance

- Provides beneficiary flexibility if one spouse passes away

- Simplifies Medicare transition planning (one spouse on Medicare, one not)

When to Hire Professional Help

You should consult a tax professional if:

- You have unexplained amounts on your 1099-SA

- You changed HSA providers mid-year

- You’re a California resident with significant HSA earnings

- You withdrew HSA funds for non-qualified expenses and aren’t sure how to report them

- You received a CP2000 notice from the IRS about HSA distributions

- You’re using advanced HSA strategies like the “Stealth IRA” approach

- You have multiple 1099-SA forms from different years or accounts

The cost of professional tax preparation (typically $450-$1,200 for HSA-related issues) is minor compared to the penalties, interest, and audit costs of getting it wrong.

Book Your HSA Tax Strategy Session

If you’re confused about how to get a 1099 SA, how to report it correctly, or whether your HSA withdrawals will trigger taxes and penalties, don’t guess. One mistake on Form 8889 can cost you thousands in unnecessary taxes and IRS penalties. Our team specializes in HSA compliance for self-employed professionals, high-income earners, and California residents facing complex state reporting requirements. Click here to book your consultation now and get clear answers before you file.