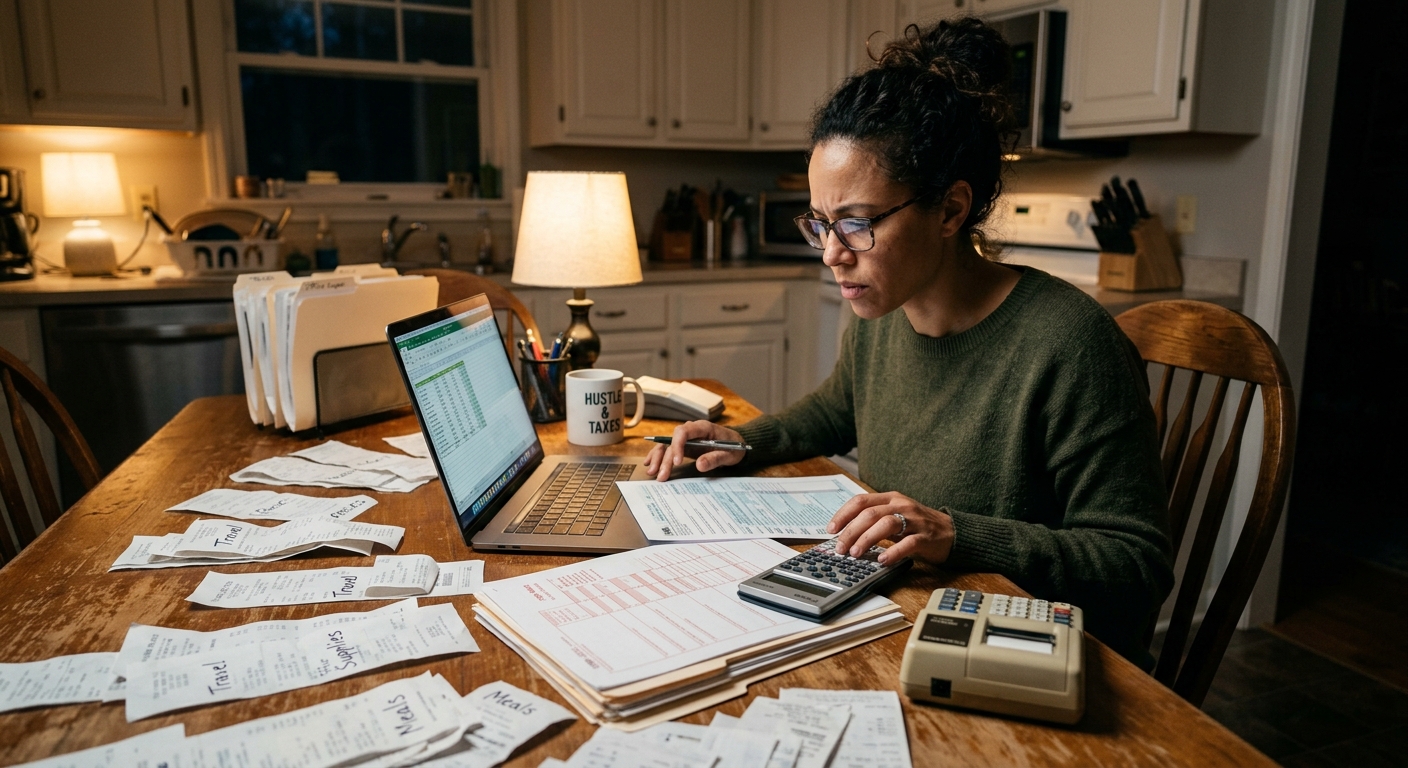

Most 1099 contractors assume they will get crushed at tax time because they do not have an employer withholding taxes or setting up benefits. That belief is exactly why many self-employed people quietly overpay the IRS by five figures every decade. The rules for independent contractors are different from W2 employees, but that difference can be turned into a serious advantage if you know how to use business deductions aggressively and correctly.

Fast Tax Fact: A self-employed professional with $120,000 of 1099 income who tracks and claims strong deductions can easily cut their tax bill by $8,000 to $15,000 per year, depending on their state and situation. This is not about games or gray areas. It is about using the rules that already exist in the tax code and backing them up with clean documentation.

how can i maximize deductions for 1099 income is really the wrong question. The better question is, “Which expenses do I already have that the IRS will legally let me move from my personal life into my business column?” Once you see your finances through that lens, every major spending category gets re-evaluated for deduction potential.

Quick Answer

If you earn money as a 1099 contractor, freelancer, or solo business owner, you maximize deductions by treating your work like a real business. That means opening a separate bank account, tracking every business related expense, learning the rules for categories like home office, vehicle use, equipment, and subcontractors, and filing a complete Schedule C with your Form 1040. According to IRS Publication 535, any expense that is ordinary and necessary for your trade or business is potentially deductible as long as you can document it.

This information is current as of 6/10/2026. Tax laws change frequently. Verify updates with the IRS or your state tax authority if you are reading this later.

Understanding 1099 Income And Why It Is Taxed Differently

When you receive a Form 1099 NEC or 1099 K, the IRS treats you as self employed. Instead of having Social Security and Medicare taxes withheld by an employer, you pay self employment tax on your net profit. Net profit is your 1099 income minus your deductible business expenses, reported on Schedule C and carried to Schedule SE.

For 2025 federal returns, self employment tax is still effectively 15.3 percent on the first portion of net earnings, with the Social Security piece capped at an annual wage base and the Medicare portion continuing beyond that. You also owe regular income tax on those same profits. This is why strong deductions matter so much. Every dollar you can legitimately move into the expense column often saves you somewhere between 25 and 40 cents when you add federal income tax, self employment tax, and possibly state income tax.

Think of it this way. If you are in a combined 30 percent tax bracket and you identify an extra $10,000 of legitimate deductions, you reduce your tax bill by roughly $3,000. For a California contractor paying both federal and state, that same $10,000 might save closer to $3,500 or more.

Core Categories To Focus On When You Want To Maximize Deductions

Instead of trying to remember a random list of write offs, build deductions around how your business actually operates. Most profitable 1099 contractors share a few big expense buckets that drive most of the tax savings.

Home Office And Workspace Costs

If you regularly and exclusively use part of your home for business, you may qualify for the home office deduction. The IRS explains the rules in Publication 587. The space can be a spare bedroom, a dedicated area in your living room, or a separate structure like a converted garage, as long as you meet the exclusive use and regular use tests.

There are two main methods.

- Simplified method. You deduct $5 per square foot of qualified space, up to 300 square feet, for a maximum of $1,500.

- Actual expense method. You calculate the percentage of your home used for business and apply that percentage to eligible costs such as rent, mortgage interest, property tax, utilities, insurance, and certain repairs.

Example. Ana is a graphic designer with $95,000 of 1099 income. She uses a 200 square foot room in a 1,000 square foot condo purely for work. That is 20 percent of her home. Her annual eligible costs total $30,000 between rent, utilities, insurance, and property tax. Under the actual expense method, she can deduct $6,000 as a home office expense. At a combined 32 percent tax rate, that single decision saves her about $1,920 in tax.

Red Flag Alert: If your “home office” is clearly a shared family space and you are deducting half your house, you are inviting questions. The test is exclusive and regular business use. Respect that line and you can take this deduction with confidence.

Vehicle And Mileage Deductions

Driving for business is another major opportunity. You can generally deduct either the standard mileage rate or actual vehicle expenses as long as you track your business use separately from personal miles. IRS guidance for both methods is summarized in Publication 463.

With the standard mileage method, you multiply your business miles by the IRS mileage rate for the year and add qualifying parking and tolls. With the actual expense method, you track fuel, repairs, insurance, registration, lease payments, and depreciation, then multiply total costs by your business use percentage.

Example. Malik is a mobile notary in Los Angeles who drove 14,000 miles last year, of which 11,000 were for client visits. If the standard mileage rate is 67 cents per mile, his mileage deduction is 11,000 x 0.67, or $7,370. At a 30 percent combined tax rate, that is a $2,211 tax reduction by itself.

Pro Tip: If your vehicle use is heavy and the car is newer, the actual expense method can sometimes produce a larger deduction, especially when first year depreciation or Section 179 expensing applies. You can explore the impact on your overall bill with a small business tax calculator that models net profit and estimated tax based on your deductible expenses.

Equipment, Software, And Supplies

Laptops, cameras, tools, phones, printers, and specialized gear are often fully deductible. Under rules described in Publication 946, you can usually deduct the full cost in the year you place the item in service using Section 179 or bonus depreciation, subject to limits, instead of depreciating it slowly.

Example. A self employed videographer spends $6,000 on a new camera body and lenses, $2,000 on a computer upgrade, and $1,200 on editing software subscriptions. That $9,200 can generally be deducted in the year of purchase. At a 30 percent combined rate, that is roughly $2,760 back in tax savings.

Do not overlook recurring software costs. Cloud storage, design tools, customer relationship management platforms, scheduling apps, and tax software are usually fully deductible business expenses when used for your work.

Subcontractors And Outsourced Help

If you pay others to help deliver your work, those payments can be deducted as contract labor. This might include a virtual assistant, editor, bookkeeper, or another specialist. You generally need to issue a Form 1099 NEC to contractors you pay $600 or more in a year. The expense itself belongs on Schedule C, and the 1099 reporting keeps things clean in case of an IRS question.

An online consultant who pays a part time assistant $12,000 per year may reduce tax by $3,000 to $4,000 depending on bracket and state. That is on top of the time they get back to grow revenue.

KDA Case Study: 1099 Consultant Turns Chaos Into Tax Savings

Laura is a self employed marketing consultant in California earning about $180,000 per year in mixed 1099 NEC and 1099 K income from various platforms. For years she filed returns using only basic expenses she could remember, usually claiming around $18,000 in deductions. Her effective federal and state tax bill hovered near $60,000, and she felt like she could never catch up on savings.

When she came to KDA, we rebuilt her books from bank and credit card feeds, separated personal and business transactions, and restructured her categories. We captured a realistic home office deduction, fully documented 9,000 business miles, added equipment and software that had never been claimed, and correctly reported $24,000 of contractor payments. Her legitimate deductions jumped from $18,000 to just over $54,000.

The result. That $36,000 deduction increase cut her combined federal and California bill by roughly $11,000 for that year alone. Our fee for the clean up work and ongoing advisory package was just under $3,500, so Laura saw more than a three to one first year return and moved into a proactive planning relationship instead of scrambling every April.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Business Structure, Bookkeeping, And Why They Matter For Deductions

Many contractors focus on individual write offs but ignore the structure and systems that make those write offs defensible. This is where working with experienced business owners as a peer group, not just as an accountant, becomes valuable.

Separate Accounts And Clean Records

From the IRS perspective, sloppy records are one of the fastest ways to lose deductions in an audit. Publication 583 covers recordkeeping requirements for small businesses. The practical version is simple. Use a separate business bank account and credit card, never mix personal and business spending intentionally, and keep digital copies of receipts for anything that looks even slightly unusual.

Clean bookkeeping is not just about audit defense. When your books are current, it is much easier to see which expenses are growing, which clients are actually profitable, and where cash is going. Strong books support stronger tax planning and better business decisions. If you are not ready to hire an internal bookkeeper, modern bookkeeping and payroll services can give you CFO level clarity at a fraction of the cost.

Entity Choice And The Potential For Additional Savings

Some 1099 contractors stay sole proprietors for simplicity. Others eventually move into an LLC or elect S corporation status when profits justify the extra complexity. While entity choice is a separate decision, it affects how you take deductions and how you pay yourself. For example, an S corporation can potentially reduce self employment tax by splitting profit between salary and distributions, but it also adds payroll requirements and reasonable compensation rules.

If you are consistently netting over $80,000 to $100,000 from 1099 income, it is usually worth having a strategist model different structures for you. The difference between staying Schedule C and shifting to a well run S corporation structure can easily be $6,000 to $15,000 per year in combined federal and state savings, but only if payroll, bookkeeping, and documentation are dialed in.

Advanced Strategies Many 1099 Contractors Overlook

Once you are comfortable with core write offs, there are more sophisticated strategies that can move real money over a decade. These usually require coordination between tax planning, bookkeeping, and in some cases retirement or legal advisors.

Retirement Contributions As A Tax Lever

Self employed individuals often have access to more powerful retirement plans than W2 employees. Options include SEP IRAs, Solo 401k plans, and defined benefit plans for very high earners. Contributions are generally deductible against your business income, reducing both income and self employment tax in many cases.

Example. A 1099 software engineer with $210,000 in net profit establishes a Solo 401k. Between the employee deferral and employer profit sharing component, they contribute $50,000 for the year. At a 35 percent combined tax rate, that one move saves $17,500 in current year tax while accelerating retirement savings. IRS rules for these arrangements live in several places, including one participant 401k guidance.

Health Insurance And HSA Opportunities

If you pay for your own health insurance, you may qualify to deduct premiums as an adjustment to income, separate from itemized medical deductions. In addition, if you are covered by a high deductible health plan, you can contribute to a Health Savings Account. HSA contributions are deductible, grow tax deferred, and can be withdrawn tax free for qualified medical expenses.

Example. A married 1099 contractor family contributes $8,300 to an HSA for the tax year. In a 28 percent combined bracket, that adjusts their tax down by about $2,324, and the funds stay available for future medical needs.

Qualified Business Income Deduction

The Qualified Business Income deduction, often just called the 20 percent pass through deduction, can be a major benefit for profitable 1099 businesses. In simple terms, many self employed taxpayers can deduct up to 20 percent of their qualified business income on top of their normal business expenses, subject to income thresholds and limitations described in IRS QBI guidance.

For example, if you have $120,000 of Schedule C profit and qualify fully for the 20 percent deduction, that is another $24,000 off your taxable income. At a 24 percent federal bracket, the QBI deduction alone could be saving you around $5,760 in federal income tax, not counting state effects. The catch is that high income, certain service businesses, and low wage situations can reduce or eliminate the deduction, so planning matters.

Why Most Business Owners Miss These Deductions

The tax code is written in a way that rewards proactive behavior and punishes guesswork. Most self employed people fall into one of three traps.

- They wait until March or April and try to reconstruct a full year of expenses from memory.

- They do not know which expenses are allowed, so they play it too safe and only claim the obvious items.

- They rely on basic software without feeding it complete, categorized data.

From the IRS side, under claimed deductions are not a problem. There is no penalty for paying more tax than you owe. That is why there is very little public education on strategies that would reduce your bill. The burden is on you and your advisory team to learn the rules and apply them.

Red Flag Alert: Over claiming is just as dangerous. If you start pushing personal lifestyle costs like family vacations, personal meals, or your entire home internet bill into your business without clear business justification, you increase your audit risk. The standard is still ordinary and necessary for your trade or business, and you should be able to explain every large or unusual line item calmly if asked.

What If I Did Not Track Anything Last Year

A common fear for new 1099 earners is that they have already “blown it” because they did not track receipts from day one. In practice, you usually have more salvageable data than you think.

Bank and credit card statements can be pulled into bookkeeping software and categorized after the fact. Calendar entries and email history can help you reconstruct mileage and trip purpose. Phone and internet bills can be split between business and personal use based on realistic percentages. While it is always better to build systems early, it is rarely too late to improve a return before filing.

If you already filed a weak return for a prior year, you may be able to amend it using Form 1040 X and a corrected Schedule C if you discover substantial missed deductions. There is a statute of limitations on refunds, so this is an area where timing and professional guidance matter.

Will Taking Strong Deductions Trigger An Audit

Strong deductions that are fully documented do not automatically cause problems. The IRS is far more interested in patterns that suggest unreported income, fake businesses, or deduction categories that are wildly out of proportion to the industry standard. You can review small business guidance in the Small Business and Self Employed Tax Center to see how the agency frames these issues.

In fact, having clean books, separate accounts, and clearly labeled categories is one of the best risk reducers you can have. When your tax preparer or strategist can print a profit and loss statement that ties directly to your bank feeds and receipts, it sends a very different message than a handwritten summary that says “travel, $18,000.”

Bottom Line

The real answer to how can i maximize deductions for 1099 income is that you treat your self employment like a business from day one. You build systems for tracking expenses, you learn the core rules around home office, vehicles, equipment, contractors, retirement contributions, and health costs, and you partner with professionals who understand 1099 realities rather than just W2 checklists.

Over a decade, a contractor who consistently captures an extra $20,000 per year in legitimate deductions versus a peer who does not is likely to keep $60,000 to $80,000 more in after tax cash, depending on their bracket and state. That difference alone can fund retirement accounts, emergency reserves, or the down payment on a rental property.

Key Takeaway: The IRS is not hiding these write offs. They are published in plain view across publications like Publication 535, but nobody is going to apply them for you automatically. That is your job, and the job of the team you choose to advise you.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Book Your Tax Strategy Session

If you are earning serious 1099 income and suspect you are leaving money on the table, do not wait for another high tax bill to confirm it. Book a focused strategy session with our team, bring your last return and a few months of bank statements, and we will show you exactly where stronger deductions and better structure could reduce your bill while keeping you firmly within IRS rules. Click here to book your consultation now.

The IRS is not hiding these write offs you just were not taught how to find them.