Many business owners think choosing an entity is just a box to check when they file paperwork with the state. In reality, that one decision can lock in thousands of dollars of extra tax every year or protect you when something goes wrong. If you do not really understand the core business entity definition you selected, you are betting your wallet and your personal assets on guesswork.

Quick Answer

In plain English, a business entity is the legal wrapper around your business. It determines how you pay tax, who is liable if something goes wrong, and what rules you must follow. For most small owners, the real choice is between staying a sole proprietor, forming an LLC, or layering in S corporation or C corporation tax treatment on top. The right move depends on profit level, risk, and long term goals.

Why Your Business Entity Definition Matters More Than You Think

At a high level, your entity affects three levers: how your income is taxed, how much of your personal stuff is exposed in a lawsuit, and how flexible things are when you add partners or investors. Missing those levers is why so many owners overpay and feel trapped later.

For example, a consultant in California making $180,000 of net profit as a sole proprietor might pay self employment tax on the entire amount. If that same activity were structured through an LLC that elects S corporation status, a well designed salary and distribution mix could cut payroll tax by $8,000 to $12,000 a year, while still staying inside IRS rules about reasonable compensation. Getting the business entity definition right is not theory; it is real cash flow.

From an IRS standpoint, the default tax treatment for an LLC is set out across multiple resources, including IRS Publication 334 for small businesses and IRS Publication 583 on starting a business. Those publications explain how the IRS views different entity types and what filings go with each.

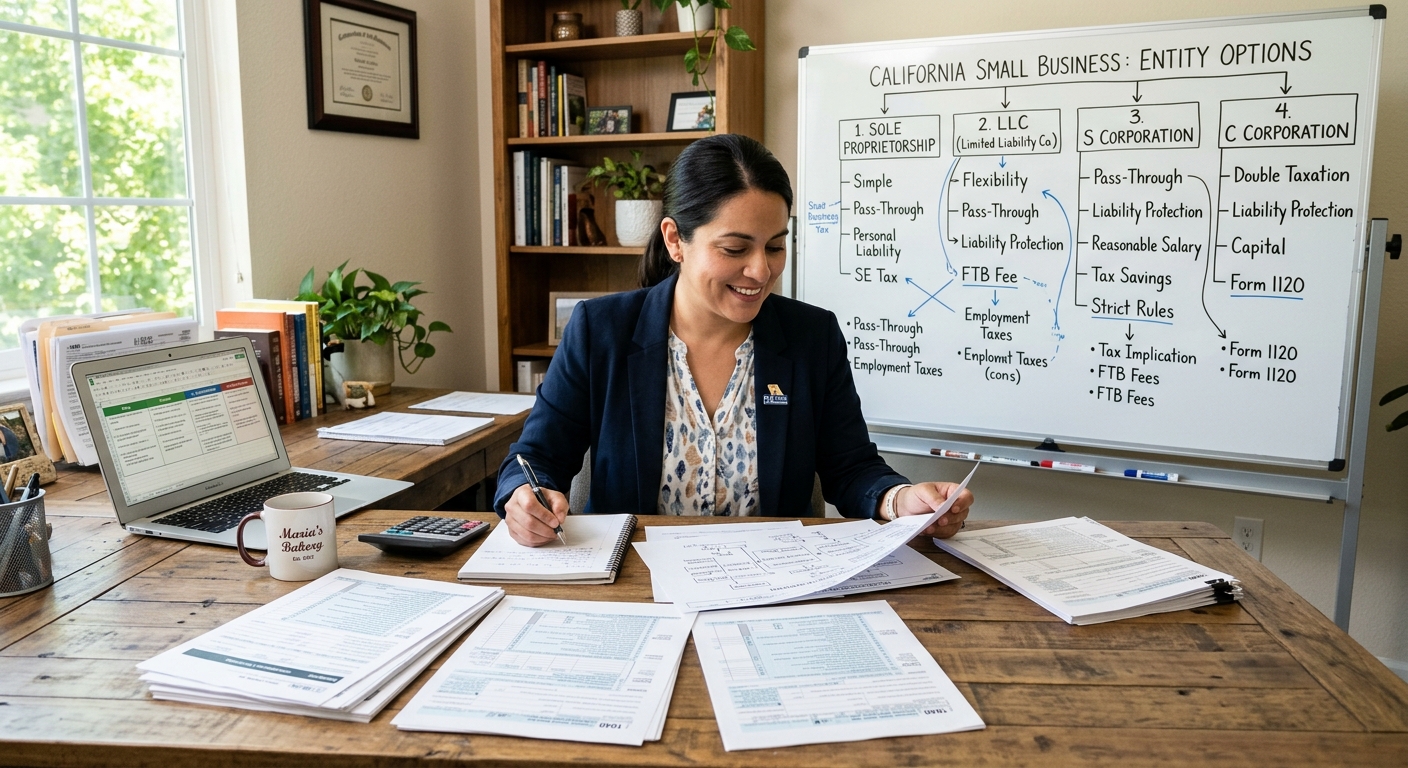

Breaking Down Each Common Business Entity Definition

Let us translate the main options into plain English and real numbers, starting with the ones most new owners default into by accident rather than strategy.

Sole Proprietor The Accidental Default

If you freelance on a 1099, drive Uber on the side, or sell on Etsy under your own name without forming anything with the state, you are a sole proprietor. There is no separate legal shell. You report income and expenses on Schedule C of your Form 1040, and you pay both income tax and self employment tax on your net profit.

Say you earn $90,000 in gross revenue from 1099 consulting and have $20,000 in legitimate expenses. Your $70,000 profit is subject to income tax based on your bracket plus roughly 15.3 percent self employment tax. That self employment component alone is about $10,710. There is no split between wages and dividends to soften that load like there can be in an S corporation.

Beyond the tax bill, every contract you sign and every mistake made in the business is tied back to you personally. If something goes sideways, creditors can potentially chase your personal bank account, your car, and even your home equity, depending on state rules.

Single Member LLC A Liability Shell, Same Default Tax

A limited liability company, or LLC, formed with one owner is called a single member LLC. From a legal standpoint, it puts a fence around your business activities. If you maintain that fence properly, the goal is that a lawsuit or unpaid vendor claim hits the LLC instead of your personal assets.

From a federal tax standpoint though, the default business entity definition for a single member LLC is a disregarded entity. That means the IRS pretends the LLC does not exist for income tax and still has you file a Schedule C. For tax, you look exactly like a sole proprietor until you affirmatively file forms to change that.

This is where many business owners leave money on the table. They form the LLC for liability reasons and assume the tax savings just show up. They do not. To change the tax treatment, you have to make an S corporation election or choose C corporation status. That decision is where strategic planning matters.

When owners are ready to reevaluate their structure, a smart move is to sit down with a firm that lives and breathes tax strategy, not just form filing. Solid support often starts with a review of your books and compliance, which is why pairing your entity work with strong bookkeeping and payroll services is so critical. Clean numbers are the only way to model which entity choice actually saves you tax.

Multi Member LLC and Partnerships Shared Profits, Shared Issues

Once you add a second owner, your LLC is treated as a partnership by default for federal tax purposes. The IRS expects a partnership return on Form 1065 and Schedule K 1s to flow profit and loss shares out to each partner.

Here, the business entity definition has to be backed up by math. You and your partner should have an operating agreement that spells out capital contributions, profit splits, and what happens if someone leaves. Ignoring that is how you end up arguing about who owes tax on income they never saw in cash because it got reinvested.

From a tax perspective, active partners generally owe self employment tax on their share of ordinary business income. In a profitable professional services firm where each of two partners nets $150,000, that self employment layer alone can run close to $23,000 per partner. Carefully planned S corporation elections or management company structures might reduce that burden, but those moves need to be engineered to align with IRS guidance in areas like partnership taxation.

S Corporation A Tax Election, Not a Separate Legal Entity

An S corporation is not a different kind of company at the state level. It is a tax election layered on top of either a corporation or an LLC that meets certain criteria. The IRS rules for S corporations live in the Internal Revenue Code and are summarized in instructions for Form 2553.

The main attraction is how it treats profit. Owners who work in the business must take a reasonable salary that is subject to payroll taxes. Profit above that salary can be distributed as S corporation income that is not hit with self employment tax. That arbitrage is where the savings come from.

Take a California marketing agency that nets $220,000 after expenses with one owner operator. As a Schedule C filer, the entire $220,000 is subject to self employment tax, roughly $33,660 on top of income tax. If that same activity runs through an S corporation, and the owner pays themselves a salary of $120,000 with $100,000 left as S corporation profit, self employment type taxes hit only the salary portion. That can reduce the combined payroll tax bill by around $14,000 annually, assuming the salary level can be justified under IRS reasonable compensation standards.

More advanced owners in California often benefit from understanding how S corporation design fits within the broader context of state and federal planning. For a deeper walkthrough focused entirely on S corporations, see KDA’s comprehensive S corporation tax strategy guide at this detailed S corporation resource.

C Corporation Growth Friendly, But With Double Tax

The C corporation is the classic corporate structure for startups and companies planning to raise outside capital. It files its own corporate return, usually on Form 1120, and pays corporate level income tax. When it later distributes after tax profits as dividends, shareholders pay tax again on those dividends, which is why people refer to double taxation.

For a small closely held consulting or real estate firm throwing off steady profit, that double tax can be painful. For a fast growth startup in Silicon Valley chasing venture capital and potentially qualifying for Section 1202 qualified small business stock treatment, the C corporation’s definition looks much more attractive.

KDA Case Study Business Entity Redesign for a Consultant

Consider Maria, a 38 year old marketing consultant in Los Angeles who started as a sole proprietor taking 1099 work from three tech companies. In 2023, she grossed $260,000 and netted about $200,000 after expenses. She filed as a sole proprietor and was shocked by the combined income and self employment tax bill north of $70,000.

In early 2024, she came to KDA after hearing that an S corporation might help but having no clear picture of the real numbers or how her current business entity definition was working. Our team reviewed her books, rebuilt her chart of accounts, and walked through entity options. We formed a California LLC and filed Form 2553 to have it taxed as an S corporation effective January 1, 2024.

We set her salary at $120,000 based on industry data and her role, with the remaining projected $100,000 treated as S corporation profit. Once we ran the tax model, the shift cut her self employment style taxes by roughly $13,500 for the year. After including the California franchise tax and modest additional payroll service costs, her net first year savings were just over $10,000. Our total advisory and compliance fee package for the restructure and ongoing support was $3,500, yielding roughly a 2.8x first year return on investment before any future year compounding.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

What the IRS Cares About With Any Business Entity Definition

No matter which path you choose, the IRS is checking three things: are you filing the right forms, are you paying roughly the right amount of tax for that structure, and can you back up your numbers with documentation. Entity choice changes the forms and deadlines, but not the basic expectations.

For instance, a Schedule C filer must keep records of income and expenses and follow the rules in IRS Publication 535 on business expenses. An S corporation owner must be able to justify that their salary meets reasonable compensation standards so the government is not losing payroll tax on underpaid wages. A partnership must issue timely Schedule K 1s so each partner reports their share of income accurately.

California adds an extra wrinkle through its annual franchise tax obligations for most entities. LLCs and corporations face both flat fees and sometimes gross receipts based fees through the Franchise Tax Board in addition to federal requirements. That is one of many reasons serious owners in the state often need support beyond generic national tax software.

How To Decide Which Entity Fits Your Situation

Instead of letting the state default or a low cost incorporation website pick for you, treat entity choice like a serious design decision. Work backward from your real numbers and your risk profile.

Step One Quantify Your Current Position

Start with your last full year of income and expense data. If you do not have clean books, get that fixed. Net profit is the core number a strategist needs to evaluate entity choices. A W 2 employee with a tiny side hustle might stick with sole proprietor treatment until their Schedule C profit consistently exceeds $30,000 to $40,000. A full time 1099 consultant clearing $120,000 of net income should be modeling S corporation scenarios.

As your income grows and your operations become more complex, plain bookkeeping spreadsheets stop being enough. This is when working with a firm that offers integrated accounting and advisory, such as KDA’s tax planning services, helps you make decisions based on accurate, timely numbers instead of guesses.

Step Two Clarify Your Risk and Liability Profile

If you are giving advice, handling client funds, or running crews on job sites, your liability risk is different from someone selling digital templates. Even if you are not ready for S corporation planning, moving from sole proprietor to LLC status can be an important risk management step.

However, legal protection only works if you respect the entity boundaries. That means separate bank accounts, proper contracts in the company name, and not commingling business and personal funds. Courts can pierce the corporate veil when owners treat the entity as a personal piggy bank, effectively undoing the protection they thought they had.

Step Three Match Profit Level to Entity Strategy

As a rough rule of thumb, S corporation planning usually starts to make sense once consistent net profit from the business exceeds about $60,000 to $80,000, especially for service businesses where most value comes from the owner’s time. Below that level, the payroll overhead and extra compliance cost can outweigh the savings.

By contrast, a C corporation strategy might be better suited for a business that intends to reinvest profit for many years, issue stock options, or pursue investors. There, the short term double tax can be outweighed by qualified small business stock benefits or strategic exit planning.

Common Mistakes That Break an Otherwise Good Entity Strategy

Even with the right high level business entity definition, owners often undercut themselves with sloppy execution. The IRS does not care what you meant to do if the paperwork and bank statements tell a different story.

Red Flag Alert Ignoring Reasonable Compensation in S Corporations

The classic S corporation mistake is paying the owner a token salary, such as $30,000, while distributing $170,000 in profit. That might look great on paper in terms of payroll tax savings, but it practically invites scrutiny. IRS guidance, including audit results shared in various internal memoranda, makes clear that underpaying wages can trigger reclassification of distributions as wages plus penalties and interest.

Red Flag Alert Treating Personal Spending as Business Deductions

Another common trap is treating the LLC or corporation as a magic write off machine. Personal groceries, family vacations, and non business vehicle use pushed through the entity do not become deductible just because the bank account name changed. The rules in IRS Publication 535 apply regardless of entity type. Crossing that line is how otherwise successful owners end up with painful audits.

Red Flag Alert Missing Elections and Deadlines

S corporation status requires timely filing of Form 2553. Partnership and corporate returns have different deadlines than individual returns, and late filing penalties can rack up quickly if you forget to file a business return separate from your personal Form 1040. For the 2025 tax year, these deadlines and penalty structures are outlined on the IRS filing page and in the instructions for each form.

What If You Chose the Wrong Entity Years Ago

Many people realize late that they picked their structure without really understanding the underlying business entity definition. Fortunately, you are usually not stuck forever. The law allows for tax elections to be made late in some circumstances, restructures to new entities, and even tax free reorganizations if moves are planned carefully.

For example, an LLC taxed as a partnership can convert to an S corporation in the eyes of the IRS by filing Form 2553 and sometimes Form 8832, if done before specific deadlines. In certain cases, it can make sense to form a new corporation and spin assets into it under rules designed to avoid immediate tax on the transfer. These are the kinds of projects that should be run through scenario models first so you know both the tax impact and the legal steps involved.

Will Changing Your Entity Trigger an Audit

Adjusting your entity type by itself is not an automatic audit trigger. The IRS expects businesses to evolve. What gets attention is inconsistent reporting, missing forms, and aggressive positions that are not supported by documentation.

If you move from a Schedule C to an S corporation, expect the government to notice changes in self employment tax. They see the drop in payroll tax as you shift profit to S corporation distributions. That is why file quality skyrockets in importance after an election. Clean payroll reports, sensible salary levels, and books that match your returns reduce the risk that your return looks like the kind of file the IRS would use as an enforcement example.

Fast Tax Fact How to Think About Entities as a California Owner

Here is a simple mental model for California based owners deciding how to interact with the maze of entity choices and state fees:

- If you are testing a side hustle under $20,000 of profit, stay simple, keep clean records, and revisit later.

- If you are over $50,000 to $60,000 of consistent net profit and your work carries liability risk, an LLC with a possible S corporation election should be on the table.

- If you are building a company for outside capital and stock based compensation, getting C corporation and qualified small business stock planning right can be worth seven figures at exit.

In every scenario, the definitions on paper are only as strong as the way you run the entity in real life. Bank accounts, contracts, payroll, and tax filings all have to reflect the structure you claim to have.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

FAQs on Business Entity Choices

What is the simplest definition of a business entity

At its core, a business entity is the legal and tax identity under which your business operates. It tells the state and the IRS who is responsible for debts, who gets sued if something goes wrong, and how profit is taxed. Sole proprietors use their personal identity, while LLCs and corporations create a separate identity with its own obligations.

Can I change my entity later if I start as a sole proprietor

Yes. You can move from sole proprietor to LLC, and from there potentially elect S corporation or C corporation status. The key is timing and planning. Some elections must be made within specific windows to apply for a given tax year. Others may trigger tax consequences if assets have appreciated. That is why mapping out the steps with someone who lives inside these rules matters more than just filing another online form.

Does every small business owner need an LLC or corporation

No. If your side business is small, low risk, and not producing meaningful profit yet, the added cost and complexity of an entity might not be worth it today. That said, the moment you are signing real contracts, dealing with larger amounts of money, or taking on any kind of operational risk, revisiting your structure is smart risk management, not just a tax move.

How does California’s franchise tax affect entity choice

California charges most LLCs and corporations an annual franchise tax, often starting at a minimum of a few hundred dollars, plus additional fees tied to income level. Those state costs need to be weighed against any federal and state tax savings an S corporation or C corporation strategy might create. An entity that makes sense in a no income tax state can pencil out very differently once the Franchise Tax Board enters the picture.

Will forming an LLC or corporation automatically reduce my taxes

No. Forming an entity changes your legal wrapper, not your tax bill by itself. The savings show up only when the structure allows you to change how income flows to you, how payroll is handled, or how deductions are tracked. That requires a deliberate design, not just filing articles with the Secretary of State.

Book Your Tax Strategy Session

This information is current as of 6/17/2026. Tax laws change frequently. Verify updates with the IRS or FTB if you are reading this later.

If you are not confident that your current structure matches your real profit level and risk, it is time to revisit your entity decision. A focused strategy session can reveal whether a different business entity definition would keep more money in your pocket while tightening your liability protection. Click here to book your consultation now.