What Is Form 1099-SA and Why Does It Matter?

You opened a Health Savings Account to save on taxes and build a cushion for medical expenses. Then tax season arrives, and you receive Form 1099-SA in the mail. Most people assume HSA withdrawals are always tax-free. That assumption costs thousands of taxpayers every year when they misreport distributions or miss the IRS red flags entirely.

Form 1099-SA reports distributions from your HSA, Archer MSA, or Medicare Advantage MSA. The IRS uses this form to track whether you spent the money on qualified medical expenses or took a non-qualified distribution that triggers taxes and penalties. If you withdrew $5,000 from your HSA but spent only $3,200 on qualified expenses, you owe ordinary income tax on the $1,800 difference, plus a 20% penalty if you’re under 65.

Quick Answer

Form 1099-SA is an IRS tax form that reports distributions from your Health Savings Account, Archer MSA, or Medicare Advantage MSA. You receive this form if you withdrew money during the tax year. The form itself does not determine your tax liability; what matters is whether you used the funds for IRS-qualified medical expenses. Non-qualified withdrawals are taxable as ordinary income and subject to a 20% penalty unless you’re 65 or older, disabled, or deceased.

Understanding the Boxes on Form 1099-SA

Form 1099-SA contains critical information the IRS uses to verify your HSA activity. Misreading a single box can trigger an audit notice or cause you to overpay taxes. Here’s what each section tells you and the IRS.

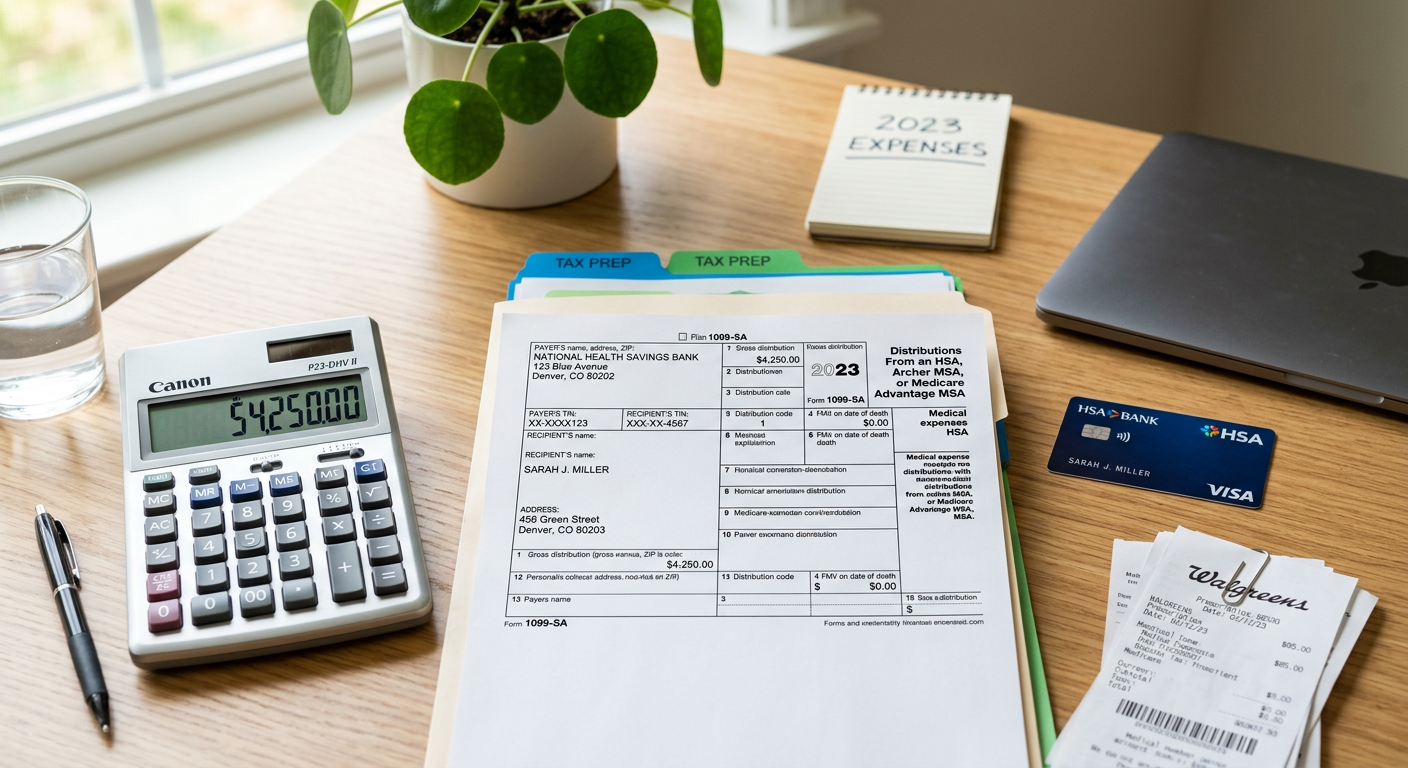

Box 1: Gross Distribution

This is the total amount you withdrew from your HSA during the tax year. If you took multiple withdrawals, they’re all added together in Box 1. The IRS receives a copy of your 1099-SA showing this exact number. Your job is to prove on Form 8889 that you spent this amount on qualified medical expenses.

Box 2: Earnings on Excess Contributions

If you over-contributed to your HSA and withdrew the excess along with any earnings, those earnings appear here. These are always taxable, even if the original contribution was corrected before the tax deadline. This is a common mistake for taxpayers who change employers mid-year or miscalculate family vs. individual contribution limits.

Box 3: Distribution Code

This single-digit code tells the IRS what type of account the distribution came from. Code 1 means HSA, Code 2 means Archer MSA, and Code 3 means Medicare Advantage MSA. Most taxpayers will see Code 1. If you see Code 2 or 3 and don’t recognize the account type, contact your HSA administrator immediately because this could indicate reporting errors.

Box 4: Fair Market Value (FMV) on Date of Death

This box is only filled in if the account holder died and the distribution represents the account’s value at death. For beneficiaries, this number determines the taxable amount. If you inherited an HSA and see this box filled in, consult a tax professional because inherited HSA rules differ dramatically depending on whether you’re a spouse or non-spouse beneficiary.

Who Receives Form 1099-SA and When?

HSA custodians and trustees must send you Form 1099-SA by January 31 if you took any distribution during the previous tax year. They also send a copy to the IRS. This means the IRS already knows how much you withdrew before you even file your return.

You’ll receive a 1099-SA if you withdrew funds for any reason: medical expenses, accidental withdrawals, reimbursements for past expenses, or even mistaken debits. The form does not distinguish between qualified and non-qualified uses. That determination happens on Form 8889, which you file with your tax return.

What If You Don’t Receive a 1099-SA?

If you took a distribution but didn’t receive a 1099-SA by mid-February, contact your HSA administrator. Do not assume the IRS won’t know about the withdrawal. HSA custodians are required to file the form with the IRS even if they fail to send you a copy. Filing without the form can result in processing delays, notices, or audits down the line.

How Form 1099-SA Affects Your Tax Return

Receiving a 1099-SA does not automatically create a tax liability. The form is informational. Your tax situation depends entirely on how you used the money. The IRS cross-references your 1099-SA against Form 8889, where you report HSA contributions, distributions, and qualified medical expenses.

Qualified Medical Expenses: The Safe Zone

If you spent every dollar from your HSA on IRS-qualified medical expenses, you owe no tax and no penalty. Qualified expenses include doctor visits, prescriptions, dental care, vision care, mental health services, and dozens of other categories defined in IRS Publication 502. You do not need to attach receipts to your return, but you must keep documentation for at least three years in case of an audit.

Example: Marcus, a 1099 consultant, withdrew $4,200 from his HSA to cover his family’s dental work and prescription medications. He received Form 1099-SA showing $4,200 in Box 1. On Form 8889, he reported the distribution and confirmed he spent it all on qualified expenses. Result: $0 tax, $0 penalty.

Non-Qualified Distributions: The Tax Trap

If you withdrew HSA funds for non-medical purposes, the IRS treats the distribution as taxable income. You report it as “other income” on your tax return. If you’re under 65, you also owe a 20% additional tax (penalty) on the non-qualified amount.

Example: Sarah, age 42, accidentally used her HSA debit card to pay for groceries totaling $350. She realized the mistake but didn’t return the funds. At tax time, she reported the $350 as a non-qualified distribution. She owed ordinary income tax (22% bracket = $77) plus a 20% penalty ($70), for a total tax hit of $147 on a $350 mistake.

Over-Age-65 Exception

Once you turn 65, the 20% penalty disappears. Non-qualified withdrawals are still taxable as ordinary income, but there’s no additional penalty. This makes your HSA function similarly to a traditional IRA after age 65, giving you penalty-free access to funds for any purpose.

Common Mistakes Taxpayers Make with Form 1099-SA

The IRS processes millions of 1099-SA forms each year, and a significant percentage trigger notices because taxpayers misunderstand the rules or make filing errors. Here are the mistakes that cost people the most money.

Red Flag Alert: Not Filing Form 8889

If you receive a 1099-SA, you must file Form 8889 with your tax return, even if your distribution was 100% for qualified expenses. Skipping Form 8889 is the single most common HSA mistake. The IRS computer sees a 1099-SA with no corresponding Form 8889 and assumes the entire distribution is taxable. You’ll receive a CP2000 notice proposing taxes and penalties on the full amount.

Red Flag Alert: Using Current-Year Expenses to Justify Prior-Year Withdrawals

You can only use HSA funds tax-free for expenses incurred after your HSA was established. If you opened your HSA in July 2025 but withdrew money in November 2025 to reimburse yourself for medical bills from March 2025, the March expenses don’t qualify. The expense must occur on or after the HSA establishment date.

Red Flag Alert: Counting Insurance Premiums as Qualified Expenses

Most health insurance premiums are not qualified HSA expenses. The IRS allows HSA funds for premiums only in specific situations: COBRA continuation coverage, health insurance while receiving unemployment benefits, long-term care insurance (subject to age-based limits), and Medicare premiums (but not Medigap). Paying your employer-sponsored health insurance premium with HSA funds is a non-qualified distribution.

Red Flag Alert: Withdrawing for Non-Spouse, Non-Dependent Family Members

You can use your HSA to pay qualified medical expenses for yourself, your spouse, and your tax dependents. You cannot use it tax-free for adult children who aren’t your dependents, parents you don’t claim as dependents, or domestic partners. These withdrawals are non-qualified and taxable.

Step-by-Step: How to Report Form 1099-SA on Your Tax Return

Properly reporting your HSA distribution requires coordinating Form 1099-SA with Form 8889. Follow these steps to avoid IRS notices and ensure accurate reporting.

Step 1: Gather Your Documentation

Before you start your tax return, collect Form 1099-SA from your HSA custodian, receipts or explanations of benefits (EOBs) for all medical expenses you paid during the year, and records of any HSA contributions you made (reported on Form W-2 Box 12 Code W for employer contributions, or your own records for personal contributions).

Step 2: Complete Form 8889 Part II

Part II of Form 8889 deals with distributions. Enter the gross distribution amount from Form 1099-SA Box 1 on Line 14a. Then calculate your qualified medical expenses on Line 14b. Qualified expenses are those you paid using HSA funds during the tax year for expenses incurred after your HSA was established.

If Line 14a (distribution) equals Line 14b (qualified expenses), you owe no tax. If Line 14a is greater than Line 14b, the difference flows to Line 16 as a taxable distribution.

Step 3: Report Taxable Distributions on Form 1040

If you have a taxable distribution (Form 8889 Line 16 shows an amount), you report it as “other income” on Schedule 1 Line 8z, which flows to Form 1040. You’ll also owe the 20% additional tax on Line 17b of Form 8889 if you’re under 65 and don’t qualify for an exception (disability or death).

Step 4: Attach Form 8889 to Your Return

Form 8889 must be filed with your Form 1040. If you’re e-filing, your tax software automatically includes it. If you’re paper filing, attach it behind your Form 1040 and schedules. Keep your receipts and documentation at home; do not mail them to the IRS unless specifically requested during an audit.

Step 5: Verify Before You File

Before submitting your return, double-check that the Box 1 amount from Form 1099-SA matches Line 14a on Form 8889. Mismatches are a red flag for IRS processing systems. Also confirm your qualified expenses are realistic and match the distribution amount if you’re claiming zero taxable income from the HSA.

What Qualifies as a Medical Expense for HSA Purposes?

The IRS defines qualified medical expenses in Publication 502. The list is extensive but includes specific exclusions that surprise many taxpayers. Understanding these rules prevents costly mistakes and penalties.

Qualified Expenses Include:

- Doctor, dentist, and specialist visits (co-pays and out-of-pocket costs)

- Prescription medications and insulin

- Hospital services and surgery

- Mental health counseling and psychiatric care

- Chiropractic care and physical therapy

- Vision exams, glasses, contact lenses, and LASIK surgery

- Orthodontics and dental work not covered by insurance

- Hearing aids and batteries

- Medical equipment like crutches, wheelchairs, and blood pressure monitors

- Lab fees and diagnostic tests

Non-Qualified Expenses Include:

- Over-the-counter medications without a prescription (with limited exceptions for items like insulin and certain COVID-related products)

- Cosmetic procedures (unless medically necessary)

- Health club or gym memberships (even if recommended by a doctor)

- Most health insurance premiums (exceptions noted earlier)

- Vitamins and supplements (unless prescribed for a specific medical condition)

- Non-prescription sunglasses or reading glasses bought at a retail store without a prescription

Pro Tip: If your doctor writes a letter of medical necessity for a specific treatment or product, it may qualify as a medical expense even if it’s not explicitly listed in Publication 502. Keep the letter with your tax records in case of an audit.

KDA Case Study: Self-Employed Consultant

Jamie, a 38-year-old self-employed marketing consultant earning $92,000 annually, opened an HSA in 2025 after switching to a high-deductible health plan. She contributed $4,300 during the year and withdrew $3,100 to cover dental surgery, vision care, and physical therapy for a running injury. In January 2026, she received Form 1099-SA showing the $3,100 distribution.

Jamie’s tax preparer confirmed all expenses were qualified and properly documented. On Form 8889, they reported the $3,100 distribution and matched it with $3,100 in qualified medical expenses. Result: $0 taxable distribution, $0 penalty. Jamie also deducted her full $4,300 HSA contribution on Form 1040 Line 13, saving approximately $1,161 in federal taxes (27% marginal bracket) plus $650 in self-employment tax savings.

Total first-year tax benefit: $1,811. Jamie paid $600 for professional tax preparation and planning. First-year ROI: 3.0x.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Special Situations and Edge Cases

HSA rules contain nuances that catch taxpayers off-guard. Here are the scenarios that don’t fit the standard playbook.

When You Change Jobs Mid-Year

If you leave a job with HSA coverage and your new employer doesn’t offer a high-deductible health plan, you can still use your existing HSA funds tax-free. However, you cannot make new contributions unless you’re covered by an HDHP. The 1099-SA you receive will show distributions regardless of your employment status. Report them the same way on Form 8889.

When You Inherit an HSA

If you inherit an HSA from a non-spouse, the account ceases to be an HSA on the date of death. The fair market value becomes taxable income to you in the year of death. The custodian reports this on Form 1099-SA with Box 4 completed. If you’re the spouse beneficiary, you can treat the HSA as your own and avoid immediate taxation.

When You Over-Contribute and Withdraw the Excess

Excess contributions create a 6% excise tax for each year the excess remains in your HSA. If you catch the mistake before the tax deadline (including extensions), you can withdraw the excess contribution plus any earnings. The earnings are taxable and appear in Form 1099-SA Box 2. The original excess contribution is not taxable when withdrawn, but you must report it correctly on Form 8889 and Form 5329.

When You Use HSA Funds for Medicare Premiums

Once you enroll in Medicare, you can use HSA funds to pay Medicare Part A, Part B, Part D, and Medicare Advantage premiums tax-free. However, Medigap (Medicare Supplement) premiums are not qualified expenses. The 1099-SA won’t differentiate; you’ll need to separate qualified from non-qualified premium payments on Form 8889.

California-Specific Considerations for HSA Holders

California does not conform to federal HSA rules. While the federal government allows tax-free contributions and distributions for qualified medical expenses, California treats HSAs like regular taxable accounts.

On your California state return, you must add back any HSA deduction you claimed on your federal return. You also report HSA earnings as taxable income each year. However, California does not tax qualified HSA distributions. When you receive Form 1099-SA, the distribution is not taxable on your California return as long as you used it for qualified medical expenses.

This creates a reporting mismatch. You lose the upfront deduction California taxpayers enjoy at the federal level, but you avoid state tax on the back end when you take distributions. For high-income California taxpayers in the 9.3% or higher state brackets, this quirk reduces the overall tax advantage of HSAs compared to residents of conforming states.

How the IRS Catches HSA Reporting Errors

The IRS uses automated matching programs to compare the 1099-SA your custodian files against your Form 8889. If there’s a discrepancy or missing form, you’ll receive a CP2000 notice proposing additional tax and penalties.

Here’s what triggers scrutiny: receiving a 1099-SA but not filing Form 8889, reporting a distribution on Form 8889 that doesn’t match the 1099-SA amount, claiming qualified expenses that seem unrealistically high compared to your distribution, or taking distributions in years when you had no HDHP coverage and likely no new qualified expenses.

The IRS does not require you to submit receipts with your return, but auditors can request documentation during an examination. If you can’t substantiate your claimed qualified expenses, the IRS will reclassify the distribution as taxable and apply the 20% penalty if you’re under 65.

What to Do If You Made a Mistake

If you realize after filing that you misreported your 1099-SA or incorrectly calculated qualified expenses, file an amended return using Form 1040-X. Attach a corrected Form 8889 and include a detailed explanation of the error.

If you mistakenly took a non-qualified distribution and want to correct it, you can deposit the money back into your HSA within 60 days and treat it as a rollover contribution. However, you’re allowed only one HSA rollover per 12-month period. If you’ve already done a rollover, redepositing the funds won’t fix the tax issue.

For excess contribution mistakes, withdraw the excess and earnings before your tax filing deadline (including extensions) to avoid the 6% excise tax. The custodian will issue a corrected or additional 1099-SA showing the earnings portion, which you report as taxable income.

Form 1099-SA vs. Form 5498-SA: What’s the Difference?

Taxpayers often confuse these two forms because they both relate to HSAs. Form 1099-SA reports distributions (money you took out). Form 5498-SA reports contributions (money you or your employer put in) and year-end account balances. You receive Form 5498-SA in May, after the tax filing deadline, because it includes contributions made through the April deadline for the prior tax year.

You need Form 1099-SA to complete your tax return. You typically don’t need Form 5498-SA to file because you should already know how much you contributed. However, keep Form 5498-SA for your records as proof of contributions in case of an audit.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Do I Need to Report My 1099-SA If I Only Used the Money for Medical Expenses?

Yes. Even if 100% of your distribution went to qualified medical expenses and you owe no tax, you must file Form 8889 with your return. The IRS uses Form 8889 to verify that the distribution shown on your 1099-SA was used correctly. Failing to file Form 8889 will result in a CP2000 notice.

What If My HSA Custodian Made an Error on Form 1099-SA?

Contact your HSA administrator immediately and request a corrected 1099-SA. Custodians can issue a corrected form (marked “Corrected” in the top right corner) and send it to you and the IRS. Do not file your return using incorrect information. Wait for the corrected form to avoid mismatches and notices.

Can I Use My HSA for My Adult Child’s Medical Bills?

Only if your adult child qualifies as your tax dependent. If your child is over 19 (or 24 if a full-time student) and you don’t provide more than half their support, they’re not your dependent. Using HSA funds for their medical expenses would be a non-qualified distribution subject to tax and penalty.

What Happens If I Forgot to Keep Receipts?

The IRS requires you to substantiate qualified medical expenses if audited. If you don’t have receipts, request itemized statements from your health providers, copies of explanations of benefits (EOBs) from your insurance company, or credit card statements showing payments to medical providers. Reconstruction is harder than keeping records, but it’s possible if you act quickly.

Can I Reimburse Myself Years Later for Old Medical Expenses?

Yes, as long as the expense was incurred after your HSA was established and you haven’t already reimbursed yourself or deducted it. Many taxpayers keep a running log of unreimbursed qualified expenses and withdraw from their HSA years later. This is legal, but you must maintain documentation showing the date of service and proof you didn’t claim the expense elsewhere. When you take the distribution, you’ll receive a 1099-SA and report it on Form 8889 as a qualified distribution.

Does Form 1099-SA Affect My Financial Aid or Medicaid Eligibility?

HSA distributions used for qualified medical expenses are not counted as income for financial aid (FAFSA) purposes. However, non-qualified distributions increase your adjusted gross income, which can affect aid calculations. For Medicaid, HSA distributions generally don’t count as income if used for medical expenses, but state rules vary. Consult your state Medicaid agency if you’re close to income thresholds.

Pro Tips for Managing Your HSA and Form 1099-SA

Keep digital copies of all receipts and EOBs in a dedicated folder labeled by tax year. Snap photos with your phone immediately after medical appointments and store them in a cloud folder. This creates an audit-proof trail without the hassle of paper filing systems.

Track your HSA withdrawals in a spreadsheet with columns for date, amount, provider, and purpose. Cross-reference this log against your 1099-SA at year-end to catch discrepancies early.

If you’re close to age 65, consider delaying non-urgent medical expenses until after your birthday to avoid the 20% penalty if you accidentally take a non-qualified distribution.

Use your HSA strategically by paying out-of-pocket for small medical expenses and letting your HSA grow tax-free. Save the receipts and reimburse yourself years later when you need cash. This maximizes the investment growth within the account.

Review your HDHP coverage at year-end. If you lose HDHP eligibility mid-year, you can’t contribute for months you’re not covered. This affects your annual contribution limit and requires careful calculation on Form 8889.

Book Your HSA Tax Strategy Session

If you received Form 1099-SA and you’re unsure whether you’ve reported it correctly, or if you want to maximize the tax advantages of your Health Savings Account without risking IRS penalties, we can help. Our team specializes in self-employed tax strategies, including HSA optimization for 1099 contractors and small business owners. Don’t let a small reporting error cost you thousands in taxes and penalties. Book your personalized tax consultation now and get the clarity and confidence you need this tax season.

This information is current as of 3/14/2026. Tax laws change frequently. Verify updates with the IRS if reading this later.