Your LLC Already Has Two Tax Elections Sitting on the Table. One of Them Costs You $41,300 More Per Year.

Most California LLC owners never file a single tax election form. They register their LLC with the Secretary of State, get an EIN, open a business bank account, and start working. That is exactly how they end up overpaying the IRS by five figures every single year. The difference between S Corp and C Corp for my LLC is not a trivia question. It is the most consequential tax decision a California business owner will make, and getting it wrong at $200,000 in annual profit means handing the government an extra $41,300 that could have stayed in your pocket.

Here is the reality: your LLC is not a tax classification. It is a legal wrapper. The IRS does not care what your state filing says. What the IRS cares about is how you elect to be taxed, and you have three choices: default (disregarded entity or partnership), S Corp, or C Corp. Two of those choices create radically different tax outcomes, and most LLC owners never bother to compare them.

Quick Answer: What Is the Difference Between S Corp and C Corp for My LLC?

An LLC taxed as an S Corp passes all profit through to your personal return, where you pay tax once. An LLC taxed as a C Corp pays tax at the corporate level first (21% federal), then you pay tax again when you pull money out as dividends. For a California LLC owner earning $200,000 in profit, the S Corp election saves roughly $41,300 per year compared to the C Corp election. The gap widens as income grows, and it narrows only in a few specific, uncommon scenarios.

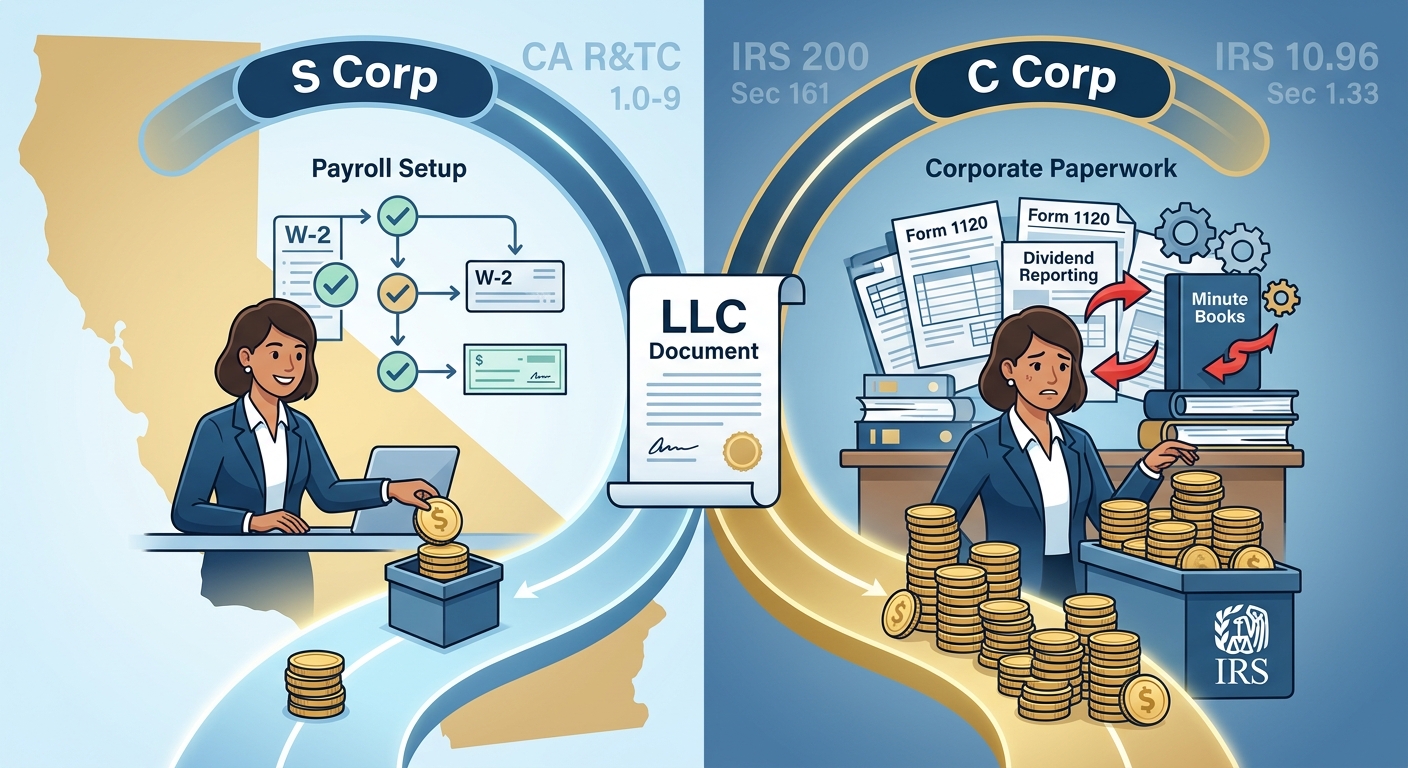

How the Five-Layer California Tax Gap Works Between S Corp and C Corp for Your LLC

When people talk about the difference between S Corp and C Corp for my LLC, they usually stop at one number: the 21% federal corporate rate. That is a fraction of the real story. In California, there are five distinct tax layers that separate these two elections, and every one of them matters.

Layer 1: Federal Entity-Level Tax

A C Corp pays a flat 21% federal income tax on all profit before any money reaches you. An S Corp pays zero at the entity level. On $200,000 in profit, that is $42,000 out the door before you see a dime with the C Corp election. With the S Corp election, every dollar flows directly to your personal return.

Layer 2: Federal Double Taxation on Dividends

After the C Corp pays its 21%, the remaining $158,000 gets taxed again when distributed to you as dividends. Qualified dividends face a 20% rate for high earners, plus the 3.8% Net Investment Income Tax (NIIT) under IRC Section 1411. That is an additional $37,564 on those distributions. The S Corp has no second layer because profits are not “distributed” in the tax sense; they flow through once.

Layer 3: California Franchise Tax Differential

California taxes C Corps at 8.84% on net income. S Corps pay just 1.5%, with a minimum of $800. On $200,000 in profit, the C Corp owes $17,680 to the Franchise Tax Board (FTB). The S Corp owes $3,000. That is a $14,680 state-level gap before you even factor in personal income tax. Many business owners in California overlook this layer entirely because they focus only on the federal picture.

Layer 4: QBI Deduction Exclusivity

The Qualified Business Income (QBI) deduction under IRC Section 199A, now made permanent by the One Big Beautiful Bill Act (OBBBA), lets S Corp owners deduct up to 20% of their qualified business income from taxable income. At $200,000 in profit with a reasonable salary of $95,000, the QBI deduction on the remaining $105,000 saves roughly $6,300 in federal tax. C Corp owners get zero QBI deduction. This benefit only exists for pass-through entities.

Layer 5: AB 150 Pass-Through Entity Tax Election

California’s AB 150 allows S Corps (and other pass-through entities) to pay state income tax at the entity level, generating a dollar-for-dollar federal tax credit that effectively bypasses the $40,000 SALT deduction cap (raised from $10,000 under OBBBA). For a California S Corp owner, this can save an additional $3,000 to $8,000 annually depending on income. C Corps cannot use this election because they are not pass-through entities. For a deep dive into every S Corp strategy layer, read our comprehensive guide to S Corp tax strategy in California.

The Combined Five-Layer Tax Comparison

| Tax Layer | C Corp LLC ($200K Profit) | S Corp LLC ($200K Profit) |

|---|---|---|

| Federal Entity Tax | $42,000 (21%) | $0 |

| Federal Dividend / Pass-Through Tax | $37,564 (on $158K) | $28,440 (personal rate on $200K) |

| California Franchise Tax | $17,680 (8.84%) | $3,000 (1.5%) |

| QBI Deduction Savings | $0 | -$6,300 |

| AB 150 SALT Bypass Savings | $0 | -$4,200 |

| Total Effective Tax | $97,244 (48.6%) | $55,940 (28.0%) |

| Annual S Corp Advantage | $41,304 | |

That $41,304 gap is not theoretical. It shows up every year you remain in the wrong election. Over five years, you are looking at $206,520 in unnecessary taxes.

Five Costliest Mistakes LLC Owners Make When Choosing Between S Corp and C Corp

Understanding the difference between S Corp and C Corp for my LLC is one thing. Avoiding the traps that erase your savings is another. These five mistakes cost California LLC owners the most money.

Mistake 1: Falling for the 21% Rate Illusion

The C Corp’s 21% federal rate looks attractive on paper. But it is only the first layer. After California’s 8.84% franchise tax and federal dividend taxation, the effective rate on $200,000 in profit exceeds 48%. The S Corp’s single-layer taxation with QBI and AB 150 benefits delivers an effective rate near 28%. If someone tells you the C Corp rate is lower, they are only showing you one-fifth of the picture.

Mistake 2: Missing the March 15 Form 2553 Deadline

To elect S Corp status for your LLC, you must file IRS Form 2553 by March 15 of the tax year you want the election to take effect. Miss that date and you wait an entire year, which at $200,000 profit means losing $41,300 in savings. Late election relief exists under Revenue Procedure 2013-30, but it requires a reasonable cause statement and is not guaranteed. Do not rely on it.

Mistake 3: Skipping FTB Form 3560

California does not automatically honor your federal S Corp election. You must separately file FTB Form 3560 with the Franchise Tax Board. Skip this form and California treats your LLC as a C Corp for state purposes, which means you pay the 8.84% rate instead of 1.5%. That single missed form costs $14,680 per year on $200,000 in profit. KDA’s entity formation services handle both federal and California filings to make sure nothing slips through the cracks.

Mistake 4: Setting an Unreasonable Salary

If you elect S Corp status, the IRS requires you to pay yourself a “reasonable salary” before taking distributions. Set it too low and the IRS reclassifies your distributions as wages under Watson v. Commissioner (T.C. Memo 2012-167), triggering back payroll taxes, penalties, and interest. Set it too high and you wipe out the payroll tax savings that make the S Corp valuable. The IRS uses a nine-factor test from Revenue Ruling 59-221 to evaluate reasonableness. At $200,000 in profit, a defensible salary typically falls between $85,000 and $110,000 depending on your industry and role.

Mistake 5: Ignoring California Bonus Depreciation Nonconformity

Under OBBBA, federal bonus depreciation is now permanently set at 100% under IRC Section 168(k). California does not conform. Under R&TC Sections 17250 and 24356, the state disallows bonus depreciation entirely. If you claim $150,000 in bonus depreciation on your federal return but forget to add it back on your California return, the FTB will come knocking. Every S Corp and C Corp LLC in California must maintain dual depreciation schedules, one for federal and one for state.

KDA Case Study: Sacramento Marketing Consultant Saves $39,800 After S Corp Election

Daniela ran a digital marketing consultancy through a single-member LLC in Sacramento. For three years, she reported $205,000 in annual profit on Schedule C, paying self-employment tax on every dollar. She assumed her LLC was “already taxed as a business” and never filed any election form. Her total annual tax burden exceeded $72,000.

KDA reviewed her situation and identified three immediate problems. First, she was paying 15.3% self-employment tax on all $205,000 because her LLC was a disregarded entity. Second, she had no QBI deduction optimization because her salary-equivalent was effectively her entire profit. Third, she was missing the AB 150 PTE election entirely.

We filed Form 2553 under late election relief via Rev. Proc. 2013-30, submitted FTB Form 3560, established a reasonable salary of $98,000 based on industry benchmarks, activated the AB 150 PTE election, and set up a Solo 401(k) to shelter an additional $23,500 in pre-tax contributions. Her first-year tax bill dropped from $72,000 to $32,200, a savings of $39,800. The engagement cost $5,800, delivering a 6.9x return on investment in year one. Over five years, projected savings total $199,000.

Want to see how much you could save? Plug your business profit into this small business tax calculator to estimate your tax under different entity elections.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Three Narrow Scenarios Where the C Corp Election Might Win

The S Corp election wins for the vast majority of California LLC owners. But the difference between S Corp and C Corp for my LLC is not always one-sided. Here are three situations where the C Corp election may make sense.

Scenario 1: Venture Capital Funding

S Corps are limited to one class of stock under IRC Section 1361(b)(1)(D). If you plan to raise venture capital, investors typically require preferred stock with different rights, which disqualifies you from S Corp status. If VC funding is a near-term goal, the C Corp election preserves your ability to issue multiple stock classes.

Scenario 2: Qualified Small Business Stock (QSBS) Under Section 1202

IRC Section 1202 allows C Corp shareholders to exclude up to $10 million in capital gains (or 10x their basis) when selling QSBS held for five or more years. This is a powerful exit strategy. However, California does not conform to Section 1202 under R&TC Section 18152.5, so the state-level benefit is zero. The federal savings can still be substantial for founders planning a large exit, but you must weigh this against years of double taxation while operating.

Scenario 3: Full Earnings Retention Below the $250,000 Threshold

If your LLC retains all profits for reinvestment and never distributes dividends, the C Corp’s 21% flat rate can be lower than individual rates for high earners. The catch: retained earnings above $250,000 trigger the Accumulated Earnings Tax under IRC Section 531 at 20%, which eliminates the advantage. This only works if you genuinely reinvest every dollar and keep the balance below the threshold.

Eight Steps to Elect S Corp Status for Your California LLC

If the S Corp election makes sense for your LLC, here is the exact process, step by step.

Step 1: Verify IRC 1361(b) Eligibility

Confirm your LLC meets all S Corp requirements: 100 or fewer shareholders, only individuals (or certain trusts and estates) as members, no nonresident alien members, one class of ownership interest, and domestic organization. Most single-member and spousal LLCs qualify automatically.

Step 2: Evaluate Built-In Gains Exposure

If your LLC was previously taxed as a C Corp, appreciated assets trigger the Built-In Gains (BIG) tax under IRC Section 1374 for five years after conversion. Get a professional appraisal of all assets on the conversion date to establish fair market value baselines.

Step 3: Clean Up Accumulated Earnings and Profits

If your LLC has C Corp history, any accumulated earnings and profits (AE&P) under IRC Section 1368(c) create a ticking time bomb. Excess passive investment income on top of AE&P can terminate your S Corp election under IRC Section 1362(d)(3). Distribute all AE&P before or immediately after the election takes effect.

Step 4: File IRS Form 2553 by March 15

Submit Form 2553 to the IRS. All members must sign. For new LLCs, you have 75 days from formation to file. For existing LLCs, file by March 15 for current-year effect. Keep a copy of the IRS acceptance letter in your permanent records.

Step 5: File FTB Form 3560 with California

Within one month of filing Form 2553 (or by the due date of your first S Corp return), file Form 3560 with the California Franchise Tax Board. This is a separate requirement that does not happen automatically.

Step 6: Establish Reasonable Salary and Payroll

Set up payroll for the owner-employee. Use the three-method benchmark approach: replacement cost analysis, 60/40 salary-to-distribution ratio, and industry wage data from the Bureau of Labor Statistics. Register with the California Employment Development Department (EDD) for state payroll taxes, including SDI at 1.1%.

Step 7: Activate the AB 150 PTE Election

File the AB 150 pass-through entity tax election with the FTB. This allows your S Corp to pay California income tax at the entity level, generating a federal tax credit that bypasses the $40,000 SALT cap. The election must be made annually.

Step 8: Set Up Dual Depreciation Schedules

Because California does not conform to federal bonus depreciation under R&TC Sections 17250 and 24356, maintain separate depreciation schedules for federal (using 100% bonus depreciation under IRC 168(k) where applicable) and California (using MACRS without bonus). Use Section 179 expensing up to $2,500,000 (now permanent under OBBBA) where it benefits both returns.

OBBBA Permanent Changes That Widen the S Corp Advantage in 2026

The One Big Beautiful Bill Act made several provisions permanent that were previously set to expire, and every one of them tilts the scale further toward the S Corp election for California LLC owners.

Permanent QBI Deduction Under IRC 199A

The 20% QBI deduction was originally set to expire after 2025. OBBBA made it permanent, which means S Corp LLC owners can deduct up to 20% of qualified business income from taxable income every year going forward. C Corps do not qualify. At $200,000 in profit with a $95,000 salary, the annual QBI savings exceed $6,300.

Permanent 100% Bonus Depreciation

Federal bonus depreciation under IRC 168(k) is now permanently fixed at 100%, reversing the phase-down that was scheduled. For S Corp LLC owners who purchase equipment, vehicles, or other qualifying property, this means a full first-year write-off on the federal return. Remember: California still does not conform, so you need that dual schedule.

$40,000 SALT Cap with AB 150 Bypass

OBBBA raised the SALT deduction cap from $10,000 to $40,000, but California S Corp owners can bypass even this higher cap through the AB 150 PTE election. C Corps cannot use this workaround, which means their owners face the full SALT limitation on personal returns.

$15 Million Estate Tax Exemption

The increased estate tax exemption, now at approximately $15 million per individual, combined with stepped-up basis, makes the S Corp’s pass-through structure more valuable for succession planning. S Corp shares receive a full basis step-up at death. C Corp shares also receive a step-up, but the underlying corporate assets do not, creating a built-in gain that can haunt the next generation.

How the IRS Monitors Your LLC Tax Election

The IRS Palantir SNAP AI system cross-references multiple data sources to flag inconsistencies in LLC tax elections. Here is what triggers an audit.

Salary-to-Distribution Ratio Flags

If your Form 1120-S shows officer compensation of $40,000 but distributions of $160,000, the IRS algorithm flags the return for reasonable salary review. The system compares your reported salary against industry benchmarks, geographic data, and your own historical compensation patterns.

Missing 941 Filings After S Corp Election

Once you elect S Corp status, the IRS expects quarterly Form 941 payroll tax filings. If the system detects an active S Corp election but zero 941 filings, it triggers an automatic compliance notice. This is one of the most common post-election mistakes.

Form 7203 Basis Tracking

S Corp shareholders must file Form 7203 to track their stock and debt basis. If your distributions exceed your basis, the excess is taxable as capital gains. The IRS now cross-references Form 7203 against K-1 distributions and Form 1040 reporting to catch mismatches.

Entity Reclassification Detection

For LLC owners who elected C Corp status, the IRS monitors whether the election is being maintained consistently. Filing Form 1120 one year and then switching to Form 1120-S without a proper Form 2553 on file triggers an immediate review.

Should You Elect S Corp or C Corp for Your LLC? A Decision Framework

Use this framework to determine which election fits your California LLC.

Elect S Corp if:

- Your annual LLC profit exceeds $60,000

- You want to minimize self-employment and payroll taxes

- You plan to take most profits as distributions

- You have no plans to raise venture capital

- You want access to the QBI deduction and AB 150 PTE election

- You have 100 or fewer members, all U.S. individuals or qualifying trusts

Elect C Corp if:

- You are actively seeking VC funding requiring preferred stock classes

- You qualify for QSBS Section 1202 and plan a large exit in 5+ years

- You will retain all earnings below $250,000 for reinvestment with zero distributions

- You need multiple classes of ownership interests

Stay as Default LLC if:

- Your profit is below $40,000 annually

- You have significant net losses to carry forward

- You want maximum simplicity and minimal compliance obligations

What If I Already Elected C Corp and Want to Switch?

If your LLC is currently taxed as a C Corp and you want to change to S Corp, you can do so by filing Form 2553 by March 15 of the desired effective year. Be aware of two critical traps. First, the five-year Built-In Gains recognition period under IRC 1374 applies to any appreciated assets at the time of conversion. Second, any accumulated earnings and profits from your C Corp years must be distributed or managed carefully to avoid the passive investment income termination risk under IRC 1375 and 1362(d)(3). Also note the five-year lockout rule under IRC 1362(g): if you revoke your S Corp election, you cannot re-elect for five tax years without IRS consent.

What If I Miss the March 15 Deadline?

Late election relief under Revenue Procedure 2013-30 is available if you meet specific conditions: the LLC intended to be classified as an S Corp from the requested effective date, the only reason for the late filing was that Form 2553 was not timely submitted, and you have reasonable cause. You must file within 3 years and 75 days of the intended effective date. Attach a statement explaining the reasonable cause to your Form 2553, and write “FILED PURSUANT TO REV. PROC. 2013-30” at the top. This is not a guaranteed fix, but the IRS approves the majority of good-faith late filings.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Can a single-member LLC elect S Corp status?

Yes. A single-member LLC can elect S Corp status by filing Form 2553. The LLC will be treated as a corporation for federal tax purposes and then taxed under Subchapter S. You must run payroll and pay yourself a reasonable salary.

Do I need a new EIN if I change my LLC’s tax election?

No. Your LLC keeps the same EIN regardless of whether you elect S Corp or C Corp taxation. The EIN is tied to the legal entity, not the tax classification.

What is the minimum income to make the S Corp election worthwhile?

Generally, $60,000 to $75,000 in annual profit is the break-even point. Below that, the compliance costs of running payroll, filing Form 1120-S, and maintaining payroll tax accounts may exceed the tax savings.

Does California automatically recognize my federal S Corp election?

No. You must separately file FTB Form 3560 with the California Franchise Tax Board. Without this form, California taxes your LLC as a C Corp at the 8.84% rate instead of the 1.5% S Corp rate.

Can I have my LLC taxed as an S Corp and still keep LLC liability protection?

Yes. The tax election does not change your legal structure. Your LLC retains all the liability protection of a limited liability company. The S Corp election only changes how the IRS and FTB tax your income.

What happens if the IRS rejects my S Corp election?

If your Form 2553 is rejected, your LLC remains in its prior tax status (default or C Corp). Common rejection reasons include ineligible shareholders, late filing without proper relief, or missing signatures. You will receive IRS Letter 385C or 386C explaining the rejection. Fix the issue and refile.

This information is current as of May 4, 2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Book Your LLC Tax Election Strategy Session

If you own a California LLC and you are not sure whether the S Corp or C Corp election is costing you or saving you money, stop guessing. The difference between S Corp and C Corp for my LLC is not something you figure out from a blog post alone. It takes a five-layer projection built on your actual numbers. Book a personalized consultation with our strategy team, and we will run your specific profit, salary, and distribution scenario through all five California tax layers so you can see exactly where you stand. Click here to book your consultation now.