Most business owners who form an LLC think they’re making a smart move. And they’re right — forming an LLC beats operating as a sole proprietor every time. But here’s the part nobody explains: staying as a default LLC when you’re earning real profit is often the most expensive tax decision a business owner makes. The difference between LLC and S Corp isn’t just a legal technicality. It’s a gap that can mean $10,000 to $25,000 in avoidable taxes every single year.

This guide breaks down exactly what separates an LLC from an S Corp, what that difference costs you in real dollars, and how California business owners can use a single IRS election to close the gap — without changing who owns the business or how it operates day-to-day.

Quick Answer: What Is the Core Difference Between LLC and S Corp?

An LLC (Limited Liability Company) is a legal entity structure that protects your personal assets from business liabilities. An S Corp (S Corporation) is a tax election — not a separate business structure — that changes how the IRS taxes your business income. You can be both simultaneously: an LLC taxed as an S Corp is one of the most common and effective tax strategies for small business owners in the United States.

The critical difference comes down to self-employment tax. As a default LLC, every dollar of net profit is subject to the 15.3% self-employment tax (SE tax) — which covers Social Security and Medicare. That rate applies on top of your federal and California income tax. As an S Corp, only your salary is subject to payroll taxes. The remaining profit passes through as a distribution, bypassing SE tax entirely. On $150,000 in profit, that distinction can be worth more than $15,000 per year.

How Self-Employment Tax Creates the Gap

To understand the financial stakes, let’s walk through what a default single-member LLC actually costs versus what an S Corp costs on the same income.

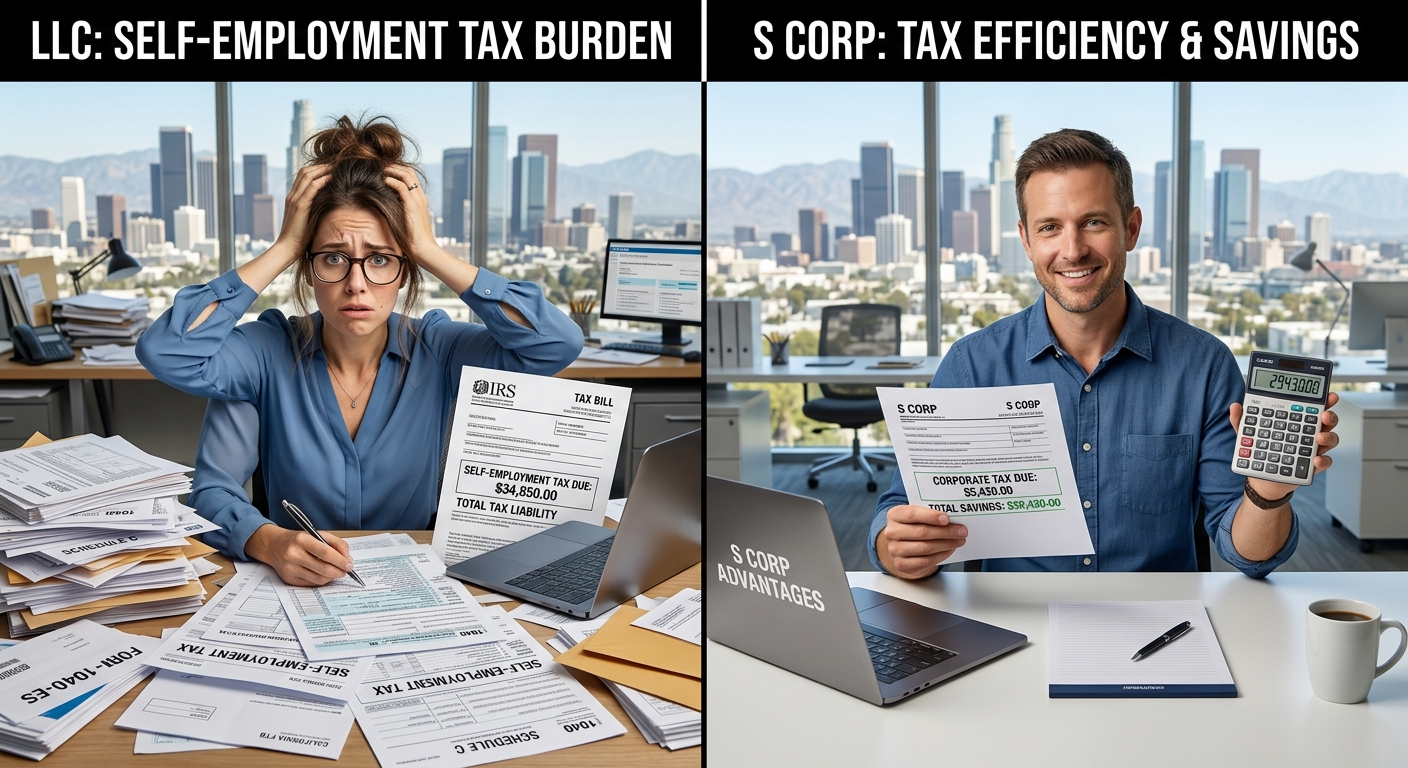

Default LLC: The Full SE Tax Burden

Imagine Marcus, a San Diego IT consultant who brings in $150,000 in net profit through his LLC. As a default LLC (sole proprietor for tax purposes), Marcus owes:

- Self-employment tax: 15.3% on the first $168,600 of net earnings = approximately $22,950

- Deductible SE tax: He deducts half of that ($11,475), reducing taxable income slightly

- Federal income tax: Based on adjusted income of ~$138,525, roughly $22,500

- California income tax: Approximately $9,200 at state rates

Total federal and state tax burden: approximately $54,650 on $150,000 in profit. Effective rate: 36.4%.

S Corp Election: The Salary-Plus-Distribution Split

Now assume Marcus elects S Corp status and sets a reasonable salary of $65,000. The remaining $85,000 passes through as a distribution, with no SE tax.

- Payroll taxes on $65,000 salary: ~$9,945 (employer + employee FICA)

- Federal income tax: Approximately $20,800 (with QBI deduction on the distribution)

- California income tax + 1.5% franchise tax: Approximately $11,400

Total burden: approximately $42,145. That’s a savings of $12,505 in year one — and that’s before layering in a retirement plan or health insurance deduction.

Want to run your own numbers first? Use this small business tax calculator to estimate your current tax load and see what an S Corp election could save you.

Why Most LLC Owners Don’t Make the Switch

Three myths keep profitable LLC owners paying unnecessary taxes year after year.

Myth 1: “I Can’t Be an LLC and an S Corp at the Same Time”

Wrong. The IRS allows an LLC to elect S Corp tax treatment by filing Form 2553. Your LLC remains intact at the state level — you keep your operating agreement, your liability protection, and your membership structure. The only thing that changes is how the IRS taxes your income. This is the single most common entity optimization move for small business owners earning $60,000 or more in annual profit.

Myth 2: “The Paperwork and Cost Isn’t Worth It”

The administrative requirements for an S Corp are real: you need to run payroll, file a separate 1120-S tax return, and maintain shareholder basis records. In California, you’ll also owe the 1.5% franchise tax (minimum $800) on net income. For many business owners earning $80,000 or more in net profit, these costs represent a fraction of the tax savings. A $3,000 annual bookkeeping and payroll cost against $12,000 to $18,000 in tax savings is a 4x to 6x return on investment.

Myth 3: “The IRS Will Flag a Low Salary as a Red Flag”

The IRS does scrutinize “unreasonably low” S Corp salaries. But the standard is “reasonable compensation” for the services you perform — not a salary equal to your entire profit. For most knowledge workers, service professionals, and consultants, a salary set at 40% to 60% of net profit is defensible. Document your reasoning using published salary data for your role (the Bureau of Labor Statistics is a solid reference), and the IRS has no legitimate basis to challenge it.

For a comprehensive breakdown of S Corp salary rules, entity election timing, and California-specific compliance, see our complete guide to S Corp tax strategy in California.

The QBI Deduction: Why S Corps Hold a Second Advantage

Under the Tax Cuts and Jobs Act (TCJA) — made permanent by the One Big Beautiful Bill Act (OBBBA) — qualifying business owners can deduct up to 20% of their qualified business income (QBI). This deduction applies to pass-through income from S Corps, partnerships, and sole proprietors.

Here’s why S Corps often extract more value from QBI:

- The QBI deduction applies to the distribution portion of S Corp income (the part not subject to payroll taxes)

- By paying yourself a reasonable salary and maximizing the distribution, you increase the base on which QBI is calculated

- The deduction phases out at higher income levels ($197,300 for single filers in 2025), but proper salary structuring keeps more income in the deductible zone

For Marcus in our example, the $85,000 distribution generates a $17,000 QBI deduction at the 20% rate. That deduction reduces his taxable income by $17,000, worth approximately $3,740 in additional federal tax savings at a 22% marginal rate. Combined with the SE tax elimination, the total first-year benefit exceeds $16,000.

What If My Business Is a Specified Service Trade or Business (SSTB)?

SSTBs — which include law, accounting, consulting, financial services, health, and similar fields — face phase-out restrictions on the QBI deduction at higher income levels. If your taxable income exceeds $197,300 (single) or $394,600 (married filing jointly) in 2025, the QBI deduction begins to phase out for SSTBs. An S Corp election doesn’t eliminate this limitation, but proper income management — through retirement contributions, health insurance deductions, and other above-the-line adjustments — can keep income below the phase-out threshold.

California-Specific Rules That Change the Math

California does not conform to many federal tax benefits, and the LLC-vs-S Corp decision carries state-level nuances that every California owner needs to understand before filing.

California Franchise Tax: LLCs vs. S Corps

Both LLCs and S Corps in California pay a minimum annual franchise tax of $800. But the rates diverge from there:

- Default LLC: Pays a gross receipts fee (Schedule D on Form 568) that kicks in when annual income exceeds $250,000. A $500,000-revenue LLC owes an additional $900 gross receipts fee on top of the $800 minimum.

- S Corp: Pays 1.5% of net income as the California franchise tax, with an $800 minimum. On $150,000 net income, that’s $2,250.

In most cases, the 1.5% S Corp franchise tax is lower than the combined franchise tax and gross receipts fee for a comparable LLC at moderate revenue levels. But the calculus shifts at very high revenue with low margins. Always model both scenarios before electing.

California Does Not Recognize the Federal QBI Deduction

The 20% QBI deduction is a federal benefit only. California FTB does not allow it on your California return. This means the QBI benefit is a pure federal win — valuable, but your California taxable income will be higher than your federal taxable income when you’re running an S Corp.

AB 150 Pass-Through Entity Elective Tax

California’s AB 150 Pass-Through Entity (PTE) tax election allows S Corp shareholders and partners to pay California income tax at the entity level, generating a full federal deduction for the state tax paid. The federal SALT deduction cap ($40,000 under OBBBA for 2025) is a household-level limitation — it does not apply to deductions made at the entity level under AB 150. This election is available to California S Corps and can save qualified shareholders between $3,000 and $15,000 or more in additional federal tax. To take advantage, the entity must make the annual election before June 15 of the tax year. Our entity formation services include AB 150 PTE compliance to ensure you never miss this deadline.

KDA Case Study: San Diego Marketing Consultant Saves $17,400 in Year One

A San Diego marketing consultant came to KDA operating as a single-member LLC with $155,000 in annual net profit. She had been filing Schedule C for three years and paying self-employment tax on her full income. Her prior CPA had mentioned an S Corp election “someday” but never acted on it.

KDA ran a full entity optimization analysis. The recommendation: elect S Corp status retroactively to January 1 of the current tax year (using the late election relief provisions under IRS Rev. Proc. 2013-30), set a reasonable salary of $68,000 based on comparable marketing director compensation data, and enroll in AB 150 PTE for California.

Results in year one:

- SE tax eliminated on $87,000 in distributions: $13,311 saved

- QBI deduction on $87,000: $17,400 deduction, worth $3,828 in federal savings at 22%

- AB 150 PTE election: $4,100 additional federal tax benefit

- Less S Corp compliance costs (payroll, 1120-S filing): -$3,800

Net year-one savings: $17,439. KDA’s fee: $3,800. First-year ROI: 4.6x.

She used the savings to fund a SEP-IRA, which further reduced her taxable income by $20,000 and added another $4,400 in federal tax savings in year two.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

The S Corp Election Deadline: What You Need to Know

Filing IRS Form 2553 is the mechanism for electing S Corp status. The timing rules matter and are frequently misunderstood.

Standard Deadline

To elect S Corp status effective for the current tax year, you must file Form 2553 by the 15th day of the 3rd month of the tax year — March 15 for calendar-year entities. If you miss that deadline, the election generally takes effect on January 1 of the following year.

Late Election Relief

The IRS offers late election relief under Revenue Procedure 2013-30. If you can show “reasonable cause” for the late filing (which is broadly interpreted — most administrative oversights qualify), you can make a retroactive S Corp election. KDA has successfully filed hundreds of late elections for California business owners, often recovering multiple years of excess SE tax exposure through amended returns.

California Form 3560

In California, the S Corp election also requires filing FTB Form 3560 with the Franchise Tax Board. Missing this filing while operating as a federal S Corp is a common mistake that creates California tax exposure. Both federal and state elections must be active for the full tax benefit to apply.

LLC vs. S Corp: A Side-by-Side Comparison

| Factor | Default LLC | LLC Taxed as S Corp |

|---|---|---|

| Self-Employment Tax | 15.3% on all net profit | Only on salary portion |

| QBI Deduction (Federal) | Available on all net income | Available on distributions only |

| California Franchise Tax | $800 min + gross receipts fee | 1.5% of net income ($800 min) |

| AB 150 PTE Election | Not available | Available to shareholders |

| Annual Compliance Cost | Low (Schedule C) | Moderate (payroll + 1120-S) |

| Best For | Under $60K net profit | $60K+ net profit |

When You Should NOT Elect S Corp Status

The S Corp election is not the right move for every LLC. Here’s when to hold off:

- Net profit under $40,000: The administrative overhead (payroll processing, Form 1120-S, bookkeeping) typically costs $2,500 to $4,000 annually. The SE tax savings below this profit level rarely justify that expense.

- You have active net losses: If your business is in a loss year, there’s no SE tax to eliminate. Wait until you’re consistently profitable before electing.

- You plan to raise outside equity: S Corps can have no more than 100 shareholders, and shareholders must be U.S. citizens or permanent residents. If you’re building a venture-backed company or plan to bring in non-resident investors, an S Corp election restricts your equity flexibility.

- Your income is highly variable: If profit swings dramatically year to year, the fixed payroll compliance costs can become burdensome in low-revenue years. Model at least two years of projected income before committing.

Common Mistakes That Wipe Out Your S Corp Tax Savings

Setting Your Salary Too Low

The IRS defines “unreasonably low” compensation as compensation inconsistent with what a third party would pay for the same services. Paying yourself $20,000 when your business generates $180,000 in profit — and you’re the only service provider — is a red flag that triggers IRS scrutiny under Rev. Rul. 74-44. The fix: document your salary decision with Bureau of Labor Statistics data, industry salary surveys, or comparable offers from job boards. Keep that documentation on file.

Not Running Payroll Properly

Salary paid to S Corp shareholders must be processed through a formal payroll system. That means W-2 withholding, quarterly 941 deposits, and year-end W-2 issuance. Paying yourself via owner draws and calling it a salary on your return is not compliant. The IRS has authority to recharacterize distributions as wages and assess back payroll taxes plus penalties.

Forgetting the California AB 150 Election Window

The AB 150 PTE election must be made by June 15 of the tax year — and a prepayment of at least $1,000 must be submitted with the election. Missing this window means waiting an entire year. Given that the federal tax benefit of the AB 150 election typically runs $3,000 to $12,000 for mid-income shareholders, a missed deadline is a costly oversight.

Failing to Track Shareholder Basis

S Corp shareholders must maintain a cumulative basis schedule — a running tally of contributions, income allocations, distributions, and losses. This matters when you take distributions in excess of basis, which the IRS treats as capital gain rather than a tax-free return of investment. Failing to track basis is one of the most common S Corp bookkeeping errors, and it surfaces at the worst time: during an audit or when the business is sold.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Can I convert my existing LLC to an S Corp mid-year?

Yes, but the election must be filed by March 15 for the election to be effective January 1 of the same year. If you miss March 15, the IRS allows a late election with reasonable cause documentation, which can make the election retroactive to the beginning of the year. Do not wait until Q4 — early-year elections preserve the most SE tax savings.

Does an S Corp protect me from California FTB audits?

No entity structure eliminates audit risk. But a properly structured S Corp with documented salary reasoning, clean payroll records, and consistent bookkeeping dramatically reduces the likelihood of an adverse FTB outcome. The FTB specifically targets S Corps with zero salary on shareholder-service income — which is why documentation matters as much as the election itself.

What is the minimum salary for an S Corp shareholder in California?

There is no legal minimum, but there is a practical floor: the IRS requires “reasonable compensation” based on the services performed. For most active owner-operators, a salary below $40,000 on net profit above $100,000 is almost impossible to defend without exceptional documentation. For California specifically, EDD may also audit S Corps with suspiciously low wages — the state employment department applies its own reasonable compensation standard independently of the IRS.

Do I still need to pay the $800 California minimum franchise tax as an S Corp?

Yes. Both LLCs and S Corps in California owe a minimum $800 annual franchise tax to the FTB, payable by the 15th day of the 3rd month after the close of the tax year (March 15 for calendar-year S Corps). First-year entities received a temporary exemption under AB 85, but that applied only to entities formed in 2021. As of 2026, the $800 minimum applies from the first year of existence.

This information is current as of March 22, 2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Book Your Entity Optimization Consultation

If your LLC is generating $60,000 or more in annual profit and you haven’t run an S Corp analysis, you’re almost certainly overpaying the IRS. The math is that straightforward. Book a personalized strategy session with our team and we’ll model your exact scenario — salary structure, AB 150 eligibility, QBI deduction impact, and net savings — before you commit to anything. Click here to book your consultation now.