Difference Between LLC and S Corp and C Corp: The Entity Selection Stakes Most California Owners Never Calculate

Thousands of business owners, freelancers, and real estate investors lose out on five-figure tax savings every year because they don’t understand the difference between LLC and S Corp and C Corp—and the IRS is just fine with this confusion. Entity selection is more than a paperwork choice: it determines exactly how much tax you pay, where audit red flags get raised, and how easy it is to move money or sell your business later. This is a live-issue for the 2025 tax year, especially as California ramps up enforcement and audit scrutiny.

This information is current as of 1/27/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Quick Answer: Which Entity Saves You the Most on Taxes?

Business owners, freelancers, and investors must match their entity structure to real-world income and exit plans. LLCs are flexible, C Corps carry double-tax but protect for IPO, S Corps are tax-saving machines for profits over $60,000/year, and the wrong move can cost $25,000 or more annually. IRS rules (see IRS entity structures) show each has unique pitfalls, paperwork, and savings potential.

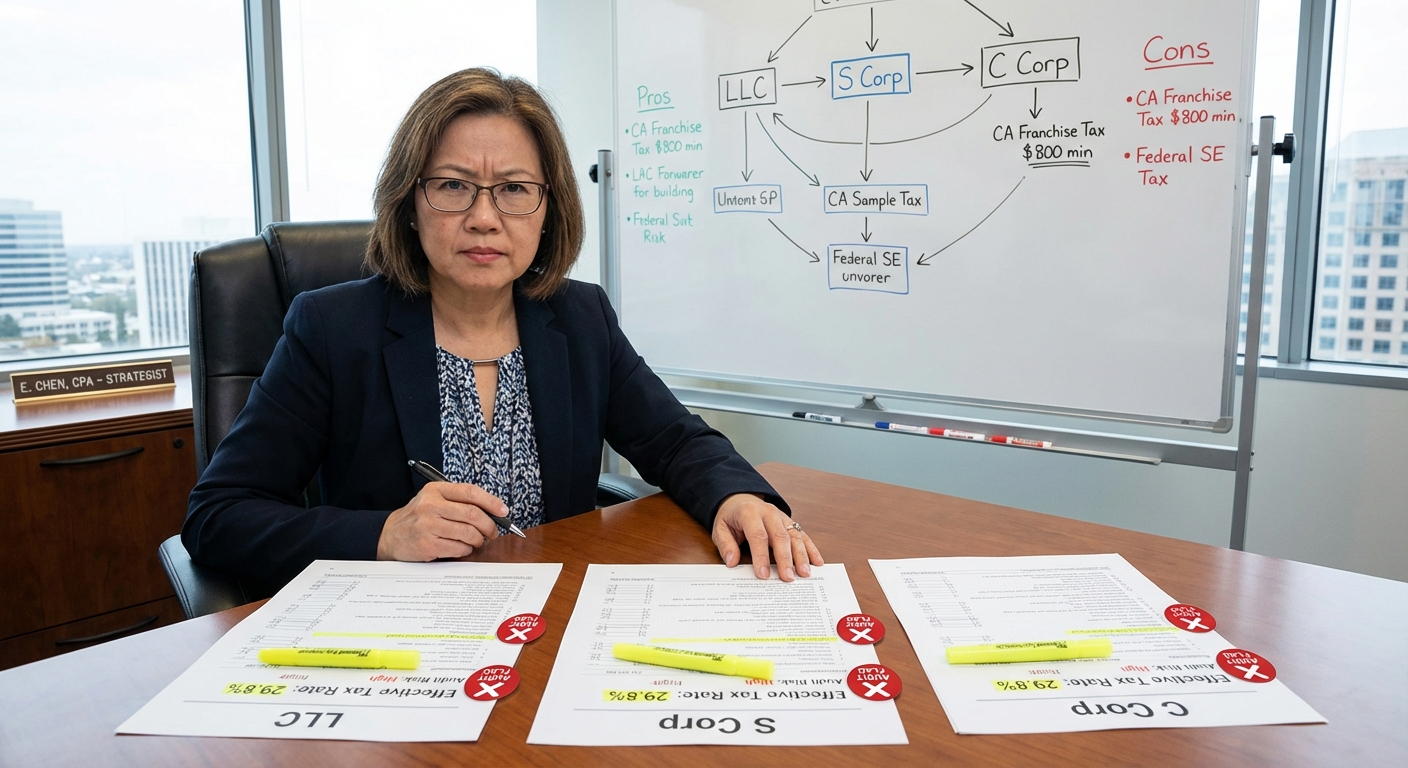

LLC vs. S Corp vs. C Corp: The Taxation and Compliance Breakdown

The biggest mistake is thinking LLC, S Corp, and C Corp are interchangeable or just “ways to register.” In reality, they set distinct tax rules for your income, distributions, and risk, especially in California:

- LLC: Default pass-through. Profits taxed once on your federal return, additional $800+ annual California franchise fee, plus Gross Receipts Fee on large LLCs (>$250K revenue).

- C Corp: Separate taxpaying entity. Corporation pays 21% federal, 8.84% California tax (see FTB Form 100), then shareholders pay tax AGAIN on dividends. Beware double-tax trap.

- S Corp: IRS pass-through that avoids most payroll/self-employment tax. Pays 1.5% California franchise tax (min $800). Requires owners take “reasonable salary,” the rest is profit not hit with Social Security/Medicare tax.

For a side-by-side deep dive, see our complete S Corp tax guide.

If you’re a business owner weighing these options, check out tailored advice for business owners—choosing wrong can set you up for high taxes or audit risk.

Pro Tip: The IRS will never proactively recommend the optimal entity for your situation. They only enforce what you file, unless you trigger an audit.

Cost to Set Up, Maintain, and Transition Entities

An overlooked factor in evaluating the difference between LLC and S Corp and C Corp is the cost–both upfront and ongoing. Let’s show how this stacks up:

- LLC: $70–$150 state filing + $800/year minimum tax in California. Additional Gross Receipts Fee applies for revenues over $250,000.

- C Corp: $100+ state filing, $800/year minimum tax, and extra cost for corporate compliance (minutes, bylaws, board meetings).

- S Corp: Must first be LLC or C Corp, then file Form 2553. $800/year minimum tax, plus payroll setup costs ($500–$2,500/year typical for owner-operator running payroll). California S Corps also pay 1.5% tax on net income.

Transitioning entities (e.g., LLC to S Corp, or S to C Corp) triggers strict IRS events, recapture taxes, and—most dangerously—can create “built-in gains” traps for appreciated assets. See IRS S Corp instructions for details. Our entity formation services can help you avoid these costly mistakes (they’re rarely well explained by online LLC mill sites).

KDA Case Study: Physician Turns $116,900 Tax Trap Into $58,400 in Net Savings

Dr. Patel, a high-earning California medical professional, initially ran his practice as a sole LLC. With $420,000 net income, he paid nearly $61,300 in self-employment tax and faced $11,000 in California taxes and minimum fees. After review, KDA restructured him into an S Corp. Through S Corp payroll ($170,000/year salary), the rest of the profit ($250,000+) passed through as distributions not subject to payroll tax. His new bottom line: $32,900/year payroll tax savings, $6,400 lower California tax, and streamlined shareholder compensation–with audit-proof documentation. KDA’s fee: $9,500. Net gain in year one: $26,100. Five-year projection: $116,900 in savings.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Which Structure Works Best for Each Persona?

Every taxpayer persona faces distinct pros and cons in the LLC, S Corp, and C Corp decision—and the optimal choice can change as your earnings rise or your business evolves.

- W-2 Employees with a Side Hustle: Start with an LLC for liability, but consider S Corp when net profit exceeds $65,000, to save on self-employment tax. Example: Alex, UX Designer with $18,000 freelance income, stays LLC. When he jumps to $89,000, S Corp saves $8,900 payroll tax per year.

- Full-Time 1099 Professionals: S Corp often wins once past $60,000 profit. Example: Lisa, a consultant, pays herself a $70,000 salary, takes $65,000 as distribution—not hit with 15.3% payroll tax on that amount.

- Real Estate Investors: Never use S Corp for rental property—creates tax traps and makes 1031 exchanges almost impossible. Partnership LLC is optimal for passive rental. Fix-and-flip investors (high volume) may consider C Corp, but must monitor double-tax impact.

- High Net Worth Owners and Tech Startups: Choose C Corp if you’re pursuing VC funding or IPO, but beware of trapped profits and exit tax. Plan ahead if converting to S Corp down the line—IRS rules impose a 5-year lockout on S to C conversions.

If your business runs payroll or you want to optimize your entity structure, bookkeeping and payroll services are critical to ensure compliance and catch savings opportunities.

Why Most Business Owners Miss This Deduction

The single most common error: owners assume that forming an LLC, C Corp, or S Corp guarantees tax benefits, but failing to file annual forms and maintain compliance blows up the plan. California is notoriously aggressive on late filings: $2,000–$10,000 in penalties for failing to file Form 568 for LLCs or 100 for C Corps. The IRS, meanwhile, triggers late-S Corp election penalties (but allows late relief for good cause).

Red Flag Alert: Don’t assume you can “fix it later.” Once an entity misses key filing or payroll deadlines, many benefits are lost for the year. Always check compliance with specialized tax preparation and filing services—not just generic CPAs.

How Do I Know If I Should Switch Entities?

Great question. Entity strategy is not “set and forget.” Triggers for a change include:

- Profit climbs past $60,000–$80,000 net (consider S Corp)

- Additional business owners or outside investors (consider C Corp or partnership)

- New plans for rapid growth, sale, or going public (C Corp may be necessary)

- Buying/renting commercial property (real estate LLC or partnership for rental, C Corp only for flips or operating business owning property)

Your decision should align with exit plans, state-specific fees, and timing. For a deeper dive, review our S Corp guide.

Pro Tip: If you want to see tax impact for each structure at your profit level, use this small business tax calculator to compare scenarios before you file anything.

What the IRS Won’t Tell You About Entity Selection

The IRS never calls to recommend a smarter structure. But they’ll penalize you for mismatches: LLCs choosing S Corp status must file payroll, or they trigger high audit risk; C Corps that “leak” dividends get double-taxed; S Corps can get shut down for improper owner distributions. You must act well before December 31 each year—most elections can’t be made retroactively after the deadline.

According to IRS S Corp guidance, reasonable salary is the #1 S Corp audit flag. Don’t underpay yourself as an owner-employee, or you’ll face back taxes and penalties.

FAQ: Real-World Entity Selection Scenarios

Can an LLC Be Taxed as an S Corp or C Corp?

Yes. An LLC can elect S Corp or C Corp taxation by filing the right IRS form (2553 or 8832, respectively). This changes tax treatment but not state legal protections. Watch out: late or improper filing means you stay as a default LLC for that year.

Is There Ever a Reason to Keep a C Corp?

Yes, for businesses wanting to attract venture capital, go public, or retain profits for big reinvestment. C Corps suit larger companies but are almost never optimal for small service-based businesses due to double taxation.

Can I Convert from C Corp to S Corp (or S Corp to LLC)?

Yes, but conversion triggers can create phantom income, extra taxes, or “built-in gains.” Get expert help before making the switch—never attempt solo. See our entity and tax planning services for a safe pathway.

What’s the Simplest Entity for a Solo Freelancer?

Start as an LLC for legal protection. S Corp election is warranted once profits are reliably above $60,000–$75,000, or if audit risk and compliance can be managed.

Get Strategic, Not Generic: Your Next Step

Don’t let the IRS or California FTB profit from indecision. Every owner, consultant, and investor faces unique stakes with entity choices—these initial setup and compliance moves create lifelong tax consequences. For federal rules, see IRS business structures. For a live, California-specific assessment, it’s best to get a true strategist on your side.

Book a Custom Entity Strategy Session

If you’re unsure whether your LLC, S Corp, or C Corp setup is saving you money or setting you up for five-figure surprises, don’t guess. Book a consultation with our entity and tax specialists—you’ll leave with a clear, dollar-based map for your next step. Click here to get started and safeguard your after-tax profit.