Most business owners only think about switching from a C corporation to an S corporation after they get a painful tax bill. By the time the return is in front of them, it is usually too late to fix the timing problem that caused the damage in the first place. The tax code gives you powerful tools, but it also punishes bad timing.

In this article, we are going to unpack the timing rules around converting a c corp to a s corp timing so you understand not just whether you should elect S status, but exactly when that election has to happen for it to deliver real savings instead of surprise taxes.

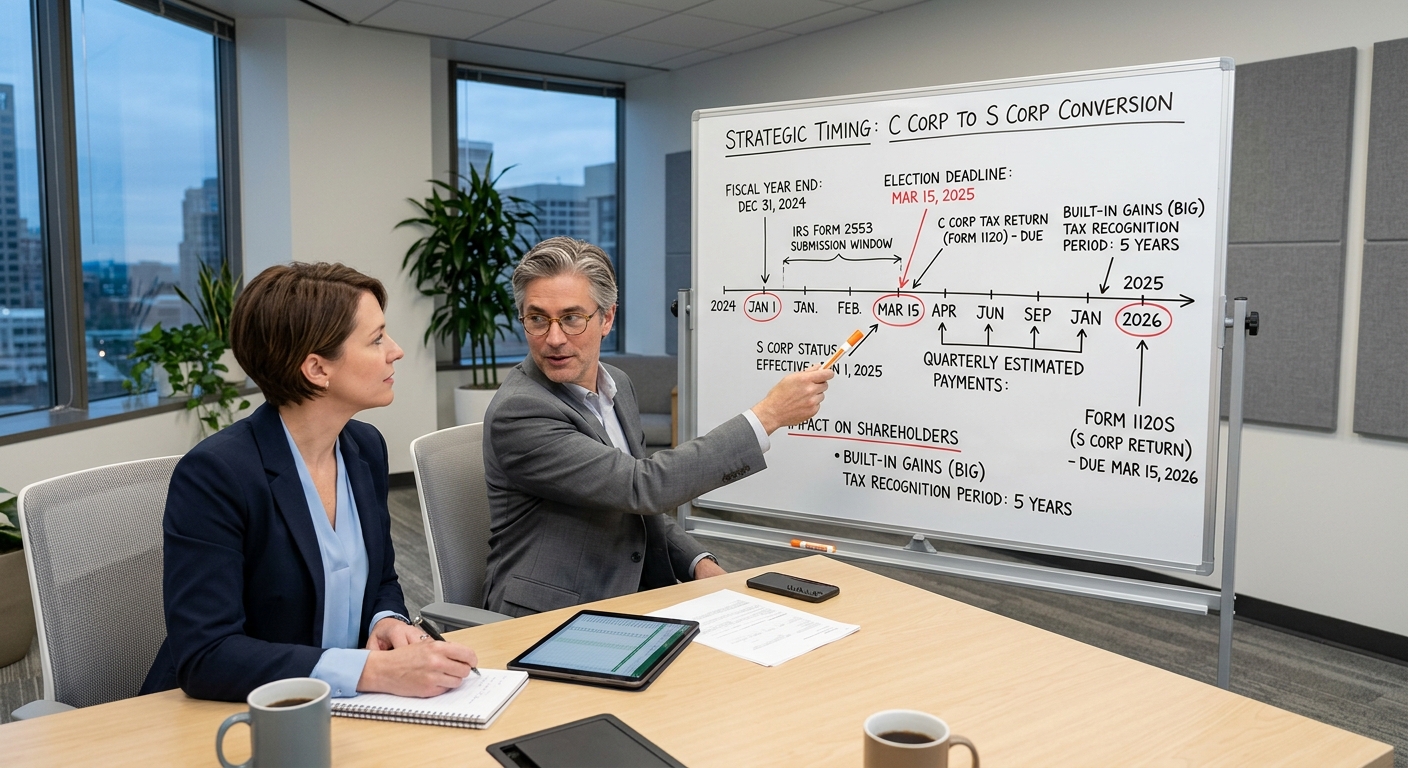

Quick Answer: When a C Corp S Election Really Takes Effect

For most calendar year corporations, an S election takes effect for the current year if you file Form 2553 by March 15. If you miss that date, the default is that your S election will not kick in until January 1 of the next year. There is late election relief available under IRS Revenue Procedure 2013-30, but you have to meet specific conditions and document reasonable cause.

The other critical timing issue is the built in gains tax window. After converting a C corporation to an S corporation, you carry a five year period where the IRS can hit you with a corporate level tax on appreciated assets that were built up during C status if you sell them. That five year clock starts on the first day your S election is effective.

Why Timing the Switch from C Corp to S Corp Matters So Much

Most C corporations pay tax at 21 percent at the federal level on their profits. When those profits are distributed as dividends, owners pay tax again at their personal rate. That double taxation can easily push your combined rate north of 30 percent, sometimes closer to 40 percent once state tax and Net Investment Income Tax are layered in.

An S corporation is a pass through entity. The business itself does not pay federal income tax in most cases. Profits flow through to the shareholders and are taxed once on their individual returns. If structured intelligently, that can shave tens of thousands of dollars off your long term tax bill.

Here is why timing matters so much. Imagine a C corporation with $400,000 of annual profit owned by a single shareholder. At a 21 percent federal rate, the corporation owes $84,000 of federal tax. If the owner then takes out $300,000 in dividends, and those dividends are taxed at 15 percent, that is another $45,000. Federal total is roughly $129,000, before state taxes.

If that same business had been an S corporation for the year, there would typically be no 21 percent corporate tax. The $400,000 would pass through. The shareholder might pay around 24 percent on the flow through and maybe some Net Investment Income Tax, but the net federal liability might come in closer to $90,000. That is a $39,000 gap in a single year.

Missing the election deadline by a week can literally lock you into the higher C corporation regime for an entire year. That is why serious tax planning services focus so heavily on the calendar when they talk about entity changes, not just on rate comparisons.

Key Deadlines for C to S Elections and How They Really Work

The mechanics seem simple, but the details are where owners get tripped up. For a corporation that runs on a calendar year, the standard rule is that you must file Form 2553, Election by a Small Business Corporation, no later than two months and fifteen days after the beginning of the taxable year you want the election to be effective. That is why March 15 is the magic date for a year that starts January 1.

Calendar Year vs Fiscal Year Corporations

If your C corporation uses a non calendar fiscal year, the same two months and fifteen days rule applies, you just count from the first day of that fiscal year. A corporation with a July 1 to June 30 year has until mid September to get Form 2553 into the IRS if it wants S status starting July 1.

Many business owners with fiscal years forget that entity elections follow the year they actually use to file, not the calendar. That disconnect shows up later when they sell assets or try to take distributions assuming they have a full year of S status and instead get C corporation treatment for part of the year.

Late Election Relief Under Rev. Proc. 2013 30

The IRS recognizes that owners and their advisors sometimes miss the 2553 deadline. Revenue Procedure 2013 30 provides a framework for late S elections if the corporation meets certain requirements. In plain English, you need to show that:

- The corporation always intended to be an S corporation as of a certain date.

- It actually met all S qualifications from that date forward.

- All shareholders reported their income in line with S treatment.

- The election is filed within the time window the procedure allows.

You generally have up to three years and 75 days from the effective date you wanted to use, but the specifics can be technical. Relief is not automatic. If your facts do not fit the procedure, you may need a private letter ruling, which costs time and legal fees.

Understanding Built In Gains Tax and the Five Year Clock

One of the least understood pieces of converting from C corporation to S corporation is the built in gains tax under Internal Revenue Code Section 1374. When you switch, the IRS draws a line between asset appreciation that happened while you were a C corporation and appreciation that occurs after the S election is effective.

For five tax years after the conversion, if the S corporation sells an asset that had built in gain from C years, the corporation can owe a corporate level tax on that gain similar to the old C rules. That can catch people off guard when they finally sell a building or a business line and discover they are paying tax at the corporate level and again at the shareholder level.

The timing takeaway is simple. The earlier you make the S election before a planned sale, the more of your future appreciation escapes the built in gains net. If you convert and then immediately sell highly appreciated assets, you have not bought yourself much.

Example: Real Estate Inside a C Corporation

Assume a C corporation owns a warehouse it bought for $500,000 that is now worth $1,500,000. There is $1,000,000 of built in gain sitting inside the corporation. The owners are planning to sell the business in about five years.

If they stay a C corporation and sell the stock, they have a completely different tax profile than if they sell assets. If they convert to an S corporation now, start the five year built in gains clock, and then sell assets after that window closes, a large portion of that $1,000,000 gain can avoid the corporate level tax. Again, the decision might be the same in both scenarios, but the outcome depends heavily on when you file and when you sell.

KDA Case Study: C Corporation Owner Restructures in Time

A California based professional services firm operated for years as a C corporation out of habit. The sole shareholder, a high income consultant with roughly $600,000 of annual profit in the corporation, assumed that the 21 percent corporate rate after the Tax Cuts and Jobs Act meant the C structure was permanently efficient.

When he came to KDA, we tested the numbers side by side. With the corporation paying 21 percent on $600,000, federal corporate tax was $126,000. After another $300,000 of dividends taxed at 15 percent, he was effectively giving up more than $171,000 to federal tax alone, before California’s corporate and personal layers.

We evaluated whether an S election made sense, including reasonable compensation, California’s 1.5 percent S corporation tax, and the shareholder’s bracket. The math showed that a timely S election for the following year would likely cut his combined federal and California hit by roughly $45,000 per year, even after payroll tax on his salary.

The critical move was timing. It was already October, so we could not salvage the current year. We filed Form 2553 before March 15 of the next year, structured a $220,000 salary, and let the remaining profit pass through as S income. In the first S year, his total combined tax dropped enough that he effectively recovered KDA’s advisory fee several times over.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Red Flag Alert: Partial Year Conversions and Short Years

Another common trap in converting a C corporation to an S corporation is misunderstanding short year returns. When the S election takes effect mid year because you changed your year end or incorporated mid year, you can end up filing two corporate returns for the same calendar year one as a C corporation for the pre election short year and one as an S corporation for the post election short year.

This is not always bad, but it changes the way you allocate income and deductions. If most of your profit landed in the C short year because you accelerated billing or closed large deals early, you could accidentally stack income into the less favorable regime.

From a planning standpoint, this is why you cannot just say we will file 2553 when we get around to it. If you are going to have a split year, you want to intentionally manage when big contracts close, when bonuses are paid, and when major purchases are made so that you are not stuffing taxable income into the wrong side of the line.

Will Converting C to S Trigger an IRS Audit?

Corporations worry that big structural changes draw attention. An S election by itself is not an automatic audit trigger. The IRS processes thousands of 2553 forms every year. What does raise risk is sloppy implementation around the election.

If you claim S status but keep filing C corporation returns, or if your shareholder compensation looks unreasonable given your profit level, you are inviting questions. IRS guidance in Publication 15 A makes it very clear that the service expects owner employees of S corporations to receive reasonable wages subject to payroll taxes before taking large distributions.

In other words, the audit risk is less about the act of changing from C to S and more about whether your behavior after the change matches what the S rules require.

How to Decide When to Pull the Trigger on S Status

The right timing for an S election depends on a mix of your current profits, expected growth, future exit plans, and state tax environment. There is no single answer that fits every C corporation, but there are clear patterns.

If You Are Early Stage with Losses

A startup C corporation burning cash might want to stay C for a while, especially if it expects outside investment or wants to preserve certain loss utilization strategies. Converting to S status when you have large net operating losses can cause you to lose the ability to use some of those losses at the corporate level.

On the other hand, if the founders are bootstrapping and will not be raising institutional capital, making an S election before the business swings into steady profit can be smart. The early losses may pass through and offset salary or other income instead of being trapped.

If You Are Profitable and Closely Held

Once a C corporation is generating predictable profits and is owned by a small group of eligible shareholders, an S election often starts to make sense. The decision then becomes when in the life cycle of the business you want to start your built in gains clock and when you expect to sell or recapitalize.

This is where digging into a detailed model with advisors who understand both federal and California rules pays off. A firm like KDA is not just looking at one year’s savings. We are checking how the change affects your qualified business income deduction, payroll tax exposure, California franchise tax, and even the way you use retirement plans.

What About California Treatment When You Switch?

For California corporations, converting from C to S has a few extra wrinkles. California recognizes federal S status, but S corporations still pay a 1.5 percent tax on net income, and there is a minimum franchise tax. Former C corporations also need to watch how pre election earnings and profits are handled when making distributions after the S election.

Distributions from an S corporation that has C corporation earnings and profits can sometimes be treated as taxable dividends instead of tax free return of basis if you do not follow the ordering rules in the Internal Revenue Code and California law. Those rules are complicated enough that most owners are better off having their returns handled by a team that works with corporate taxes every day instead of once a year in March.

Pro Tip: Use a Tax Calculator Before You Change

Before you file Form 2553, you should run a side by side projection of what your next few years look like under C rules versus S rules. That means modeling owner salary, distributions, corporate tax, personal tax and potential built in gains exposure.

To get a rough sense of your overall federal liability as an owner before you even talk to an advisor, it helps to estimate your total tax under both structures using a tool like a small business tax calculator. That will not replace strategy work, but it will force you to think in numbers instead of just labels.

Common Mistakes That Cost Owners Money When Converting

There are patterns in the problems we see when a new client shows up after a poorly timed switch from C status to S status. Avoiding these mistakes is usually worth more than any clever tactic.

Missing the Form 2553 Deadline and Hoping for the Best

Waiting until tax season to realize you wanted S status last year is a recurring theme. While late election relief exists, it is not guaranteed and can be painful to navigate. You are far better off putting a hard internal deadline on the calendar to revisit your entity structure each December so you have time to file before the window closes.

Ignoring Shareholder Eligibility Rules

An S corporation cannot have partnerships, corporations, or non resident aliens as shareholders. If you add an ineligible shareholder even briefly, you can accidentally terminate your S status. That can drop you back into C corporation treatment mid year with messy consequences.

When mapping out ownership succession or bringing in a new investor, you need to think about S eligibility months before the deal closes. That is a structural timeline issue, not just a legal paperwork checklist.

Forgetting About Built In Gains When Planning a Sale

Owners routinely assume that once they flip the S switch, they are free of the old corporate tax regime. The built in gains rules say otherwise for five years. If you are within that window and planning to sell a major asset, you need to have a clear model of how much of the gain is exposed to corporate tax and how much comes through as pass through income.

Fast Tax Fact: When to Talk to a Strategist

If your C corporation is clearing more than $150,000 in pre tax profit and has a manageable shareholder base, you are at the point where the timing of a potential S election can move real money. Waiting until profit is double that usually just means you paid a six figure tuition to the IRS to learn a lesson you could have learned earlier.

This information is current as of 6/2/2026. Tax laws change frequently. Verify updates with the IRS or California Franchise Tax Board if you are reading this in a later year. For deeper reading on S corporation strategy choices and how they play out in California, see our comprehensive S corporation tax guide.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Book Your Timing Strategy Session

Choosing S status is not hard. Choosing when to switch from C to S without tripping built in gains tax, losing valuable C corporation loss carryforwards, or triggering avoidable California issues is where the real work lives. If your corporation is already profitable or you are planning a sale or recapitalization in the next five to seven years, you should not be making this decision on a gut feeling.

If you want a clear, numbers first view of how the timing of an S election will affect your tax bill over the next decade, our advisory team can map it out in plain English and real dollar terms. Click here to book your consultation now.