Many business owners assume they can tuck an S corporation under a larger C corporation and still keep all the pass through tax benefits. That misunderstanding is expensive. Setting up ownership the wrong way can blow up your S election overnight and turn a supposedly tax efficient structure into a double taxed C corporation without you realizing it until the IRS notice arrives.

Here is the bottom line that trips people up. Under federal law, **a s corp can be own by a c corporations** is flat out wrong. An S corporation cannot have a C corporation as a shareholder under Internal Revenue Code Section 1361. The IRS is very strict about who can and cannot own S corporation stock, and California follows those federal rules for state purposes. If you ignore that, you risk retroactive S status termination, extra corporate tax, and messy amended returns going back years.

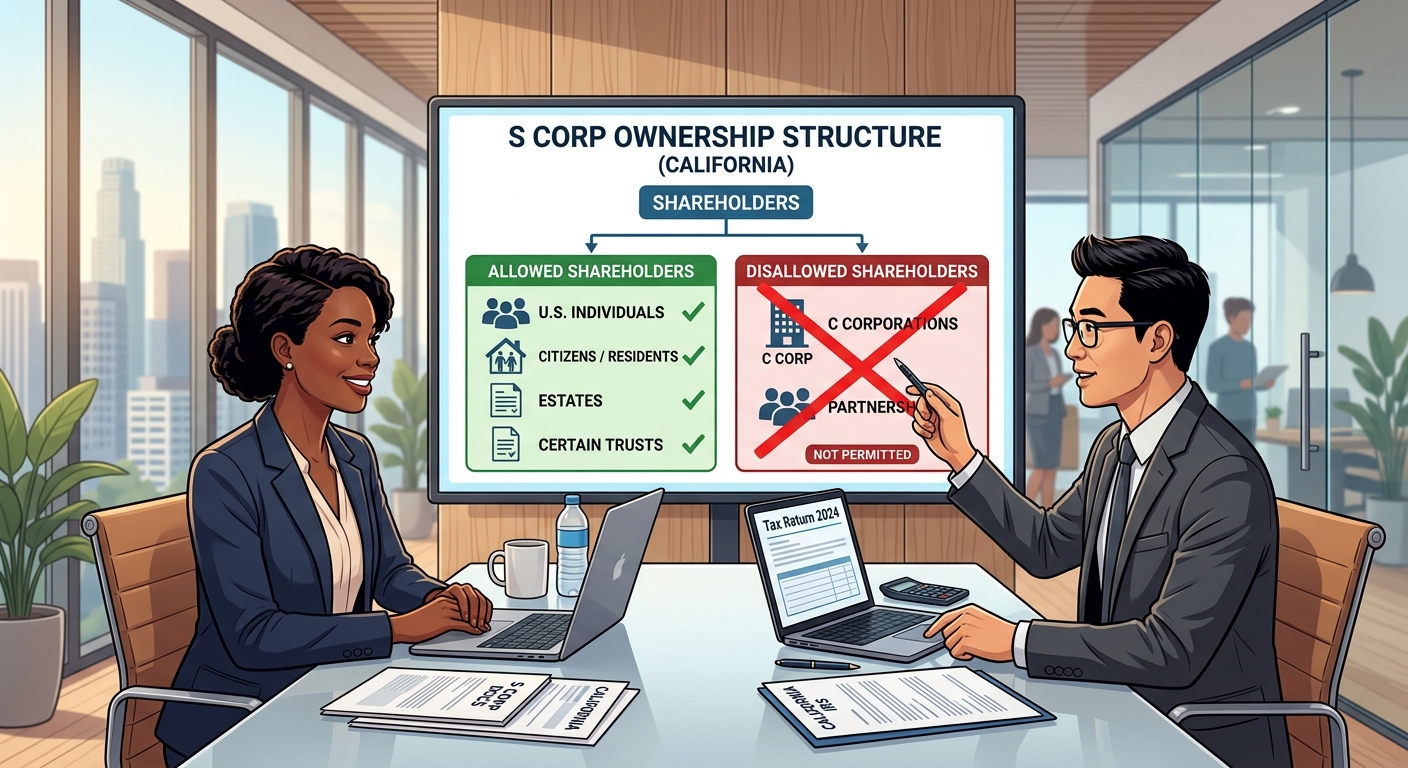

Quick Answer: Who Can Own an S Corporation (and Who Cannot)

At a high level, an S corporation is a regular corporation that has elected to be taxed under Subchapter S of the Internal Revenue Code. That election turns the entity into a pass through for federal income tax so the company itself generally does not pay federal income tax. Instead, profits and losses flow through to the shareholders.

To keep that privilege, the IRS limits who is allowed to be a shareholder. According to IRS guidance for Form 2553 and Internal Revenue Code Section 1361:

- Shareholders must generally be U.S. individuals, certain estates, and specific types of trusts.

- Some tax exempt organizations can qualify in narrow circumstances.

- There can be no more than 100 shareholders.

- There can only be one class of stock (differences in voting rights are allowed, but not differences in economic rights).

- Critically, C corporations, partnerships, and foreign individuals are not permitted shareholders.

Once you accept that “a C corporation cannot be an S corporation shareholder,” ownership planning gets much cleaner. If you violate the rule, the S election terminates, usually effective back to the date of the disallowed shareholder’s entry. At that point the entity becomes a C corporation and gets hit with corporate level tax under the rules described in IRS Publication 542.

Why Business Owners Get Confused About C Corporations Owning S Corporations

On paper, the restriction seems simple. In practice, real life entity structures are messy. Here are some common reasons the myth that a C corporation can own an S corporation persists.

Layered Holding Company Structures

Larger groups often set up a parent corporation with multiple subsidiaries. If that parent is a C corporation, owners sometimes assume they can drop an S corporation under it as a subsidiary the same way they would a regular corporation or LLC. Federal tax law does not allow that. A C corporation can own another C corporation or an LLC taxed as a corporation, but it cannot own an S corporation.

What is allowed is the reverse. An S corporation can own a C corporation subsidiary, often used for specific activities that benefit from C corporation treatment. That structure is explained in more depth in KDA’s comprehensive S corporation tax strategy guide for California owners, which walks through how parent S entities and C subsidiaries interact.

LLCs Electing S Status

Another trap comes from LLCs that elect to be taxed as S corporations using Form 2553. Owners then think any entity that owns an LLC member interest can be treated as an S corporation shareholder. That is wrong. For S status, the IRS ignores the LLC shell and looks through to who owns the membership interests. If a C corporation owns those interests, the S election is invalid.

State Law vs Federal Tax Law

California allows corporations and LLCs to organize pretty freely under state law. Just because the Secretary of State accepts your filing does not mean the IRS accepts your tax classification. State level corporate ownership charts do not override federal S corporation eligibility rules. The Franchise Tax Board generally respects federal S status only when the federal rules are followed.

How This Impacts Different Taxpayer Types

Whether you are a W 2 employee with a side business, a 1099 consultant, a real estate investor, or running a growing operating company, misunderstanding S corporation ownership rules can quietly cost you five figures or more in unnecessary tax.

W 2 Employee with Side Consulting Income

Assume Sara earns $220,000 in W 2 wages as a software engineer and another $80,000 on the side doing consulting. Her advisor suggests setting up an S corporation to reduce self employment tax. That can be a smart move once net profit gets into the $60,000 to $80,000 range for many professionals.

If Sara’s employer is a large C corporation and offers to “sponsor” her business by taking a small ownership stake in her S corporation, that would destroy S eligibility. The smarter move is to keep the S corporation owned directly by Sara or through a permitted trust while using a clean independent contractor or referral agreement with the employer. For tech professionals in this situation, getting both compensation and equity strategy right usually calls for coordinated planning like we provide on our engineer focused tax advisory page.

1099 Contractor Operating Through Multiple Entities

Now consider Michael, a 1099 construction project manager who already owns a C corporation from a previous business. He hears that an S corporation could save him $10,000 or more in self employment tax on $150,000 of net income, so he forms a new corporation, elects S status, and has his C corporation hold the shares.

On paper, the structure looks tidy. In reality, it is a time bomb. The moment the C corporation became shareholder, the S election failed. If the IRS catches this three years later, they can reclassify the S corporation as a C corporation for the entire period. That means corporate level tax on roughly $450,000 of net income over three years plus potential late payment penalties and interest.

This is the type of situation where it pays to have both bookkeeping and entity maintenance handled professionally. Our bookkeeping and payroll services keep the day to day clean so ownership and tax elections do not accidentally drift into noncompliance.

Real Estate Investors Using Multiple LLCs

Real estate investors often use several LLCs for liability protection. Some consider electing S status for the entity that collects active management fees. The same shareholder rules apply. If a C corporation owns that management company, S status is not available. On the other hand, if the investors are individuals and the LLC meets the eligibility tests, electing S status can be part of a broader California real estate tax plan that coordinates with tools such as depreciation and, when appropriate, capital gains tax projections when properties are sold.

KDA Case Study: Business Owner Fixes Invalid S Election Before the IRS Does

A manufacturing client came to KDA after their prior accountant retired. The owner, a California resident, had formed a corporation years earlier and elected S status. Two years before calling us, he reorganized his structure so that a C corporation holding company owned 100 percent of the S corporation’s stock. His attorney drafted the state corporate documents, but nobody revisited the tax implications.

At the time he reached out, the operating S corporation had averaged $600,000 in annual net income for the last two years. The C corporation parent was essentially a shell. If the IRS discovered that a C corporation shareholder had owned the S corp during that period, the S election could be treated as terminated retroactively. As a result, the operating company would owe corporate income tax on roughly $1.2 million of cumulative profit plus interest and potential penalties. In California, that extra layer of tax could have approached $250,000 for those two years.

We rebuilt the ownership structure so the individuals owned the S corporation directly again, documented a reasonable cause argument for preserving S status, and corrected related state filings. We then walked the owner through cleaning up intercompany transactions and prepared detailed workpapers showing that no abusive income shifting had occurred. The IRS accepted the reasonable cause relief request, and the S election was preserved. The client invested the six figure tax savings into new equipment instead of sending it to the Treasury.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Building a Compliant Ownership Structure When a C Corporation Is in the Mix

The fact that a C corporation cannot own S corporation shares does not mean you cannot combine the two in a broader structure. It just means you have to be careful about what owns what.

Option 1: Individuals Own S Corporation, S Corporation Owns C Corporation

A common structure is to have the individual owners hold the S corporation stock directly, then have the S corporation own one or more C corporation subsidiaries. For example:

- Three individuals own 100 percent of ABC, Inc., an S corporation.

- ABC, Inc. owns 100 percent of XYZ, Inc., a C corporation that conducts a specific line of business or holds risky assets.

In this design, S corporation shareholder rules are satisfied because only individuals own ABC, Inc. The C subsidiary is just another asset of the S corporation. Profits at the C level are taxed under C corporation rules, while the S corporation passes through its own income and any dividends it receives from the subsidiary according to standard S corporation rules. When properly planned, this lets you combine S level pass through treatment for core operations with C level treatment where that is advantageous.

Option 2: Parallel Ownership with Coordinated Tax Planning

Another approach is parallel entities. The individuals own an S corporation that handles active service income and a C corporation that holds intellectual property, branded content, or a narrow line of products. Money flows between them through properly priced intercompany agreements rather than ownership.

This method keeps S corporation eligibility clean while still using the flat corporate rate for certain income streams. The exact split has to be supported by transfer pricing principles and documented carefully to avoid IRS scrutiny. For high income professionals and operating companies, this kind of structure is best built as part of a broader entity planning engagement like what we describe on our tax planning services page.

Option 3: S Corporation with Qualified Subchapter S Subsidiary (QSub)

An S corporation can own 100 percent of another corporation and elect to treat it as a Qualified Subchapter S Subsidiary (QSub) by filing Form 8869. For tax purposes, the QSub is disregarded and treated as part of the parent S corporation. This structure can be helpful when you need separate legal entities for liability or licensing reasons but want a single S corporation tax return.

Again, the key is that the S corporation’s owners are eligible shareholders. No C corporation sits above them. The QSub itself cannot have any other shareholders, and if that changes, the QSub election terminates, which can have tax consequences described in the official IRS instructions for Form 8869.

Red Flag Alert: Hidden C Corporations That Quietly Break S Status

When the IRS reviews an S corporation return, they are allowed to look past the entity names on the shareholder schedule and examine who actually holds the economic interest. Hidden C corporations often show up in these situations.

Employee Stock Plans and Holding Entities

Sometimes companies create a corporation to hold shares for employees or to centralize ownership. If that corporation is taxed as a C corporation and it is listed as an S corporation shareholder, S eligibility is lost. Even if employees “beneficially” own the shares, the legal shareholder matters for S status.

Any structure that uses a corporation or partnership as the named owner of S corporation stock should be reviewed immediately. Cleaning this up proactively is far less painful than explaining it during an audit.

Foreign Ownership and Residency Changes

S corporation shareholders must be U.S. persons. If an individual shareholder moves abroad and becomes a nonresident alien or transfers shares into a foreign corporation for planning reasons, S status terminates just as surely as if a domestic C corporation bought those shares. Global mobility is common for high earning professionals and investors, so S corporation ownership needs to be revisited before any major residency changes.

Trusts and Estates Holding S Stock

Certain trusts can hold S corporation shares, but the rules are detailed. Electing Small Business Trusts (ESBTs) and Qualified Subchapter S Trusts (QSSTs) can qualify when elections are filed correctly. If a trust does not meet those standards or misses the required elections, it may be treated similarly to a disqualified shareholder. The relevant requirements are described in IRS Publication 559 and in the instructions to Form 2553.

Will Fixing Ownership After the Fact Save Your S Election

Many owners only learn that a C corporation cannot hold S corporation shares after they have already implemented the structure. Whether the S election can be saved depends on timing, facts, and how quickly you act.

Late Relief for Invalid Elections

The IRS has procedures that sometimes allow an S corporation to retain its status even when there has been an “inadvertent termination.” In broad strokes, you must show that:

- The termination was not motivated by tax avoidance.

- Reasonable steps were taken to correct the problem once discovered.

- All affected parties agree to any adjustments the IRS requires.

In practice, that means documenting when the C corporation became a shareholder, what advice you received at the time, how you discovered the issue, and what you did to unwind it. The IRS has discretion here, and sloppy planning combined with aggressive tax positions makes relief less likely.

California Franchise Tax Board Considerations

In California, the Franchise Tax Board generally conforms to federal S corporation rules. If the federal S election is treated as terminated, the state will follow. That can cascade into additional California corporate tax, late payment penalties, and higher minimum franchise taxes for each affected year.

Because California’s top personal income tax rate is significantly higher than the federal rate for many high earners, the stakes are even higher when an S election is lost. A structure that accidentally converts to a C corporation can quietly add $20,000 to $50,000 or more in combined federal and state tax over a few years for a profitable closely held company.

How to Audit Your Current Structure for S Corporation Compliance

Whether you are a W 2 high earner with a side business, a 1099 consultant, or running a seven figure operating company, you should not assume your current structure is compliant just because no one has raised a red flag. A targeted ownership audit can surface issues long before the IRS or FTB does.

Step 1: List Every Direct and Indirect Shareholder

Start by gathering your corporate records, stock ledgers, and any buy sell agreements. Identify who is listed as shareholder on paper and who actually has a right to profits or liquidation proceeds. Do not stop at the first layer. If a corporation or trust is listed, look through to its owners and beneficiaries.

Step 2: Match Each Owner Against S Corporation Eligibility Rules

For each owner, ask two questions: Is this owner an eligible shareholder under Section 1361? And if not, is there a way to restructure ownership so that an eligible person or trust holds the shares instead.

Individuals who are U.S. citizens or residents usually qualify. Domestic estates can qualify. Certain trusts qualify when elections are made. C corporations, partnerships, LLCs taxed as partnerships, and foreign owners do not.

Step 3: Review Formation Documents and Tax Elections

Next, confirm that all necessary elections were filed and accepted. That includes:

- Form 2553 (Election by a Small Business Corporation) with proof of IRS acceptance.

- Any ESBT or QSST elections for trusts that hold shares.

- Form 8869 elections for QSubs if you have subsidiary corporations.

Gaps here may not only affect whether an S election is valid but also how income is reported among related entities and owners.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About S Corporation Ownership and C Corporations

Can I Have My C Corporation Buy Into My S Corporation for Liability Protection

No. If your C corporation becomes a shareholder in your S corporation, you no longer have a valid S election. You might gain some superficial liability separation, but the tax cost is steep. If you want entity layering for risk management, a better design is usually an S corporation at the top with one or more C corporation or LLC subsidiaries beneath it.

What If I Accidentally Listed a C Corporation as Shareholder for a Short Period

The shorter the period and the smaller the impact, the easier it may be to obtain relief as an inadvertent termination. That said, there is no automatic forgiveness. You will need to correct the ownership, file appropriate requests with the IRS, and likely work with a tax professional to present the facts clearly.

Can a C Corporation Be a Shareholder in an S Corporation for State Law but Not for Tax Purposes

State corporate law sometimes allows arrangements that federal tax law does not. For S corporation status, the IRS cares about who owns the stock under state law. Trying to bifurcate “legal” and “tax” ownership with a C corporation involved is risky and typically not respected. If a C corporation is on the stock ledger, you have a problem.

Is an LLC Taxed as a C Corporation Allowed to Own S Corporation Stock

No. The rule disqualifies corporations that are not themselves S corporations. An LLC taxed as a C corporation is treated as a C corporation for this purpose and so cannot be an S corporation shareholder.

Bottom Line and Next Steps

The simple statement that a C corporation cannot own S corporation stock hides a lot of nuance, and misunderstanding it can undo years of tax planning. If you have layered entities, foreign owners, trusts, or prior restructurings, do not assume your S election is safe just because you have been filing Form 1120 S without pushback. The IRS has more data matching tools than ever before and California is aggressive about following up when structures look off.

This information is current as of 5/21/2026. Tax laws change frequently. Verify updates with the IRS or FTB if you are reading this at a later date or your situation involves multiple states or complex ownership.

Book Your Tax Strategy Session

If your corporate chart involves both S and C corporations, or you are not sure whether your S election is even valid, it is time to get ahead of the IRS. A focused entity review typically uncovers at least one structural improvement or risk that can be fixed before it turns into a costly notice. Book a personalized consultation with the KDA strategy team and get a clear, written plan for how your entities should be structured for both tax efficiency and compliance. Click here to book your consultation now.

Key Takeaway: the IRS is not hiding the S corporation ownership rules. Most owners simply were never taught how they work. Fixing your structure today is almost always cheaper than explaining it during an audit.