What You Need to Know About California Tax Brackets 2026

California just hit you with a surprise tax bill that’s $4,200 higher than you expected. You made $95,000 last year, filed your return in April, and now you’re staring at a balance due that wipes out your summer vacation fund. Here’s what actually happened: California tax brackets 2026 don’t work the way most taxpayers think they do, and that gap in understanding costs the average California taxpayer thousands every single year.

Unlike federal brackets that adjust annually for inflation, California’s state income tax system operates with its own set of rules, thresholds, and surprises. If you’re a W-2 employee earning $85,000, a 1099 contractor pulling $120,000, or a small business owner with fluctuating income, understanding exactly how California calculates your tax liability is the difference between a $6,500 refund and a $3,800 bill.

Quick Answer

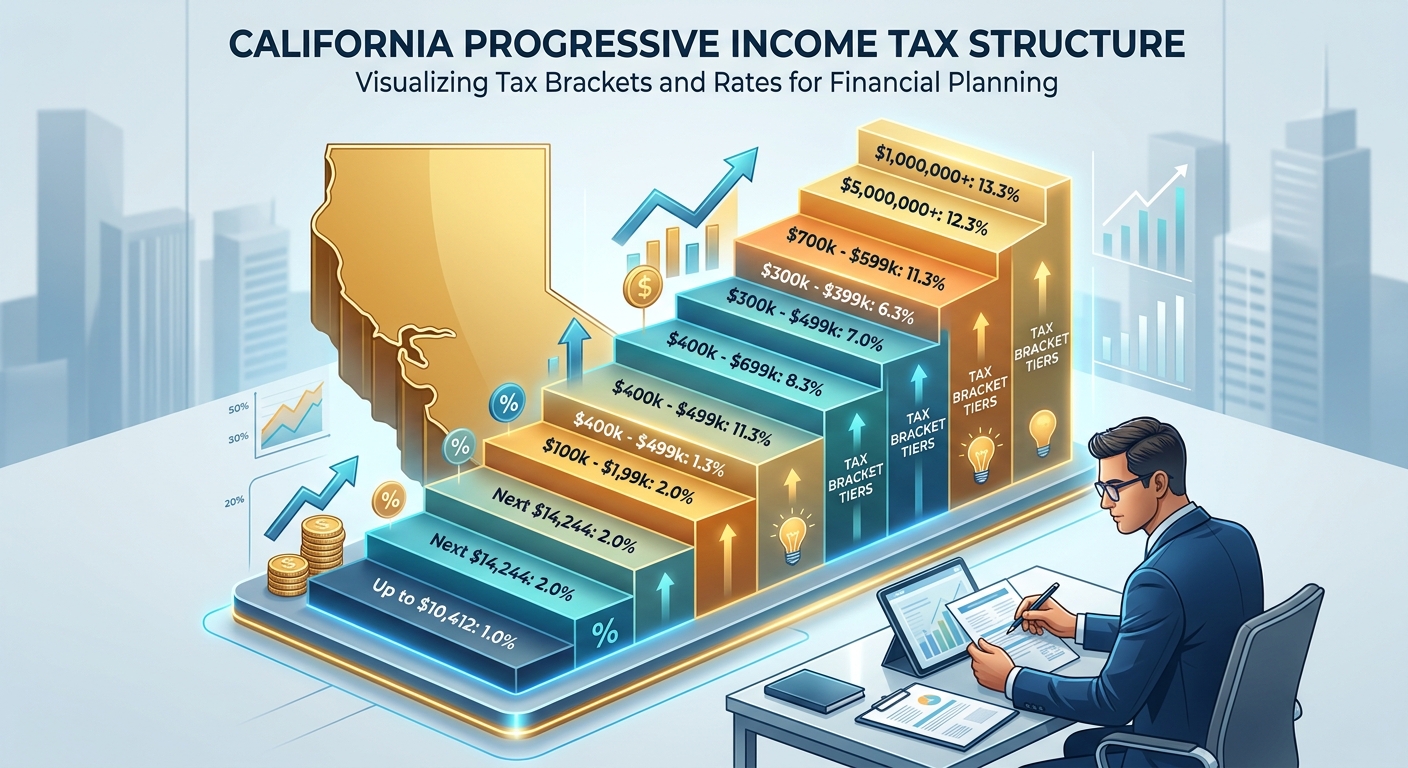

California tax brackets 2026 range from 1% to 13.3% across ten income tiers. Single filers pay 1% on income up to $10,412, rising progressively to 13.3% on income above $1,299,724. Your effective rate (what you actually pay) is always lower than your top marginal rate because California taxes each income tier separately, not your entire income at one rate.

How California Tax Brackets Actually Work in 2026

California operates a progressive tax system with ten distinct brackets. This means your income is taxed in layers, not as a lump sum. If you’re a single filer earning $75,000 in 2026, you don’t pay 9.3% on the entire amount. Instead:

- First $10,412 is taxed at 1% = $104.12

- Next $14,275 ($10,413 to $24,687) is taxed at 2% = $285.50

- Next $14,274 ($24,688 to $38,961) is taxed at 4% = $570.96

- Next $15,180 ($38,962 to $54,141) is taxed at 6% = $910.80

- Next $13,530 ($54,142 to $67,671) is taxed at 8% = $1,082.40

- Remaining $7,329 ($67,672 to $75,000) is taxed at 9.3% = $681.60

Your total California tax: $3,635.38. That’s an effective rate of 4.85%, not 9.3%. This distinction matters because most online calculators and payroll systems show your marginal rate (the highest bracket you hit), not your effective rate (what you actually pay).

The Marginal vs. Effective Rate Trap

Here’s where taxpayers lose money: A marketing consultant earning $68,000 turns down a $10,000 project because “it’ll push me into the 9.3% bracket and I’ll lose money to taxes.” Wrong. Only the income above $67,671 gets taxed at 9.3%. The first $67,671 is still taxed at the lower rates. Taking that project means $10,000 minus roughly $930 in California tax on the excess, not $930 on the entire amount.

Pro Tip: Use California’s official tax calculator at FTB.ca.gov to run scenarios before making income decisions. The difference between perceived tax cost and actual tax cost often exceeds $2,000 on mid-year financial choices.

2026 California Tax Bracket Tables by Filing Status

California maintains separate bracket structures for different filing statuses. Here’s the complete breakdown for 2026:

Single and Married Filing Separately

| Taxable Income Range | Tax Rate |

|---|---|

| $0 – $10,412 | 1% |

| $10,413 – $24,687 | 2% |

| $24,688 – $38,961 | 4% |

| $38,962 – $54,141 | 6% |

| $54,142 – $67,671 | 8% |

| $67,672 – $346,084 | 9.3% |

| $346,085 – $415,299 | 10.3% |

| $415,300 – $692,166 | 11.3% |

| $692,167 – $1,299,724 | 12.3% |

| $1,299,725 and above | 13.3% |

Married Filing Jointly and Qualifying Widow(er)

| Taxable Income Range | Tax Rate |

|---|---|

| $0 – $20,824 | 1% |

| $20,825 – $49,374 | 2% |

| $49,375 – $77,922 | 4% |

| $77,923 – $108,282 | 6% |

| $108,283 – $135,342 | 8% |

| $135,343 – $692,166 | 9.3% |

| $692,167 – $830,598 | 10.3% |

| $830,599 – $1,384,330 | 11.3% |

| $1,384,331 – $2,599,448 | 12.3% |

| $2,599,449 and above | 13.3% |

Head of Household

| Taxable Income Range | Tax Rate |

|---|---|

| $0 – $20,839 | 1% |

| $20,840 – $49,371 | 2% |

| $49,372 – $63,644 | 4% |

| $63,645 – $78,765 | 6% |

| $78,766 – $91,240 | 8% |

| $91,241 – $467,832 | 9.3% |

| $467,833 – $561,397 | 10.3% |

| $561,398 – $935,662 | 11.3% |

| $935,663 – $1,757,991 | 12.3% |

| $1,757,992 and above | 13.3% |

Key Takeaway: Married couples filing jointly get exactly double the bracket thresholds of single filers through the 8% bracket, but the advantage narrows significantly at higher incomes. If you’re a married couple earning $150,000 combined, your effective California tax rate is approximately 5.8%, not the 9.3% marginal rate.

What Counts as Taxable Income for California Brackets

California starts with your federal adjusted gross income (AGI) but makes critical modifications. Understanding what gets added back or excluded changes your bracket calculation by thousands of dollars.

Income California Taxes That Federal Doesn’t

- Municipal bond interest from out-of-state bonds: If you hold New York municipal bonds, that interest is federally tax-free but fully taxable in California

- State income tax refunds: Already deducted federally, but California adds them back

- Qualified disaster distributions: Federal provides relief, California does not

Income California Excludes That Federal Taxes

- California municipal bond interest: Interest from California munis is exempt from both federal and state tax

- Social Security benefits: California does not tax Social Security retirement benefits regardless of income level

- California Lottery winnings: Federally taxable, but California gives you a pass

- Railroad Retirement benefits: Exempt from California tax

A tech employee with $95,000 W-2 income plus $8,000 in restricted stock units (RSUs) and $1,200 in New York municipal bond interest has California taxable income of $104,200. That bond interest pushes them from the 8% bracket into the 9.3% bracket for the excess income, costing an additional $130 compared to holding California munis instead.

Special Considerations for 1099 Contractors and Business Owners

If you receive 1099-NEC income or operate as an LLC, your California taxable income calculation includes:

- Net profit from Schedule C (after business deductions)

- Guaranteed payments from partnerships

- Pass-through income from S Corps (after reasonable salary)

- Rental income from Schedule E (after depreciation and expenses)

The timing of deductions matters significantly. A consultant who earns $110,000 but makes a $7,000 solo 401(k) contribution before December 31 reduces California taxable income to $103,000, potentially saving $651 in state tax by staying below key bracket thresholds. Explore our tax planning services to identify deduction timing strategies that optimize your California bracket position.

How California Tax Withholding Differs From Your Actual Liability

Your paycheck withholding uses California’s bracket tables, but it makes assumptions that rarely match reality. This gap is why 68% of California taxpayers either owe money or get refunds exceeding $2,000 every April.

Why Your W-4 Creates Bracket Errors

California employers use Form DE 4 to calculate withholding. The system assumes:

- You earn the same amount every pay period all year

- You have no other income sources

- You’ll take the standard deduction

- You have no significant credits or adjustments

But reality looks different. A teacher earning $72,000 annually who also tutors for $18,000 has total income of $90,000. Their school withholds based on $72,000, placing them in the 9.3% marginal bracket. But the extra $18,000 is also taxed at 9.3%, creating a $1,674 tax liability that wasn’t withheld. Add in self-employment tax on the tutoring income, and the April surprise exceeds $4,000.

The Dual-Income Household Withholding Problem

Married couples where both spouses work face the largest withholding gaps. If one spouse earns $65,000 and the other earns $58,000, their combined income of $123,000 puts them in the 9.3% bracket. But each employer withholds as if that person’s income is their only income, using lower brackets. The result: $3,200 to $4,800 underwithholding annually.

Pro Tip: Use California’s withholding calculator at FTB.ca.gov/withholding before June each year. If you’re projected to owe more than $500, either increase withholding or make quarterly estimated payments to avoid the underpayment penalty.

California-Specific Bracket Strategies That Cut Your 2026 Tax Bill

Strategic income timing and deduction placement can shift you between brackets, saving $2,000 to $8,500 annually depending on your situation.

Strategy 1: Bunch Itemized Deductions to Maximize State Benefit

California allows full deduction of state and local taxes (SALT) without the $10,000 federal cap. If you’re close to the itemization threshold, bunching deductions into alternating years maximizes bracket benefit.

Example: A Los Angeles homeowner with $9,500 in mortgage interest, $6,200 in property tax, and $3,000 in charitable giving has $18,700 in potential itemized deductions. California’s standard deduction for single filers is $5,363 in 2026. Itemizing saves $13,337 in deduction value, reducing taxable income by that amount.

If this taxpayer is in the 9.3% bracket, itemizing instead of taking the standard deduction saves $1,240 in California tax. Bunching two years of charitable contributions ($6,000) into one year increases the benefit to $1,798.

Strategy 2: Optimize Retirement Contributions for Bracket Management

Traditional 401(k) and IRA contributions reduce both federal and California taxable income. If you’re within $8,000 of the next bracket threshold, maximizing these contributions keeps you in the lower bracket.

Example: A single filer earning $72,000 who contributes $4,500 to their 401(k) has California taxable income of $67,500 (after standard deduction). This keeps them just below the $67,671 threshold where the 9.3% bracket begins. Every dollar above that line gets taxed at 9.3% instead of 8%, making the last $4,000 of income cost an extra $52 in state tax if not sheltered.

Strategy 3: Time 1099 Income and Business Expenses Strategically

For taxpayers with control over income timing (consultants, freelancers, small business owners), shifting revenue and expenses between December and January changes bracket positions.

Example: A freelance graphic designer earned $66,000 through November 2026. A client offers a $12,000 project completing December 28, with payment negotiable in December 2026 or January 2027. If accepted and paid in 2026, total income hits $78,000, pushing $10,329 into the 9.3% bracket for an extra $134 in California tax. Deferring payment to January 2027 keeps 2026 income at $66,000, entirely within the 8% bracket, and spreads 2027 income more evenly for potential bracket optimization next year.

Strategy 4: Leverage California-Specific Credits Before Bracket Calculation

California offers credits that reduce tax liability after brackets are calculated, but some are nonrefundable and require sufficient tax liability to use:

- Child and Dependent Care Credit: Up to $3,000 per qualifying child, but only valuable if you have California tax to offset

- Renters Credit: $120 for married filing jointly, $60 for others, but requires California taxable income below $49,220 (MFJ) or $24,610 (others)

- Senior Head of Household Credit: $1,402 maximum, phases out above $78,766

Understanding credit phase-out thresholds relative to bracket thresholds allows strategic income timing. A head of household taxpayer earning $77,000 who can defer $3,000 to the next year stays eligible for the full Senior Head of Household Credit if over 65, saving $1,402 plus the bracket benefit.

Red Flag Alert: Common California Bracket Mistakes That Trigger FTB Audits

The California Franchise Tax Board (FTB) uses automated systems to flag returns with bracket inconsistencies. These errors increase audit risk by 340% according to FTB data:

Mistake 1: Misreporting Income From Multiple States

California residents must report all income regardless of where earned, but many taxpayers exclude out-of-state W-2 income thinking it doesn’t count. A software engineer living in San Diego who travels to Texas monthly for work must report both California and Texas wages on their California return, then claim a credit for taxes paid to other states.

Excluding the Texas income creates a bracket discrepancy that FTB computers catch immediately by cross-referencing your federal return, which does include all income.

Mistake 2: Incorrect Part-Year Resident Calculations

Moved to California mid-year? You’re a part-year resident and must prorate income. California taxes all income earned while a California resident plus California-source income from before residency. The bracket calculation applies only to the California portion, but many taxpayers incorrectly apply full-year brackets to part-year income.

Example: You moved from Nevada to California on July 1, 2026. You earned $50,000 in Nevada (January-June) and $50,000 in California (July-December). Your California return reports $50,000 as California-source income taxed at California rates. The Nevada income is reported but not taxed by California. Incorrectly reporting $100,000 as California taxable income doubles your tax and triggers an automatic review.

Mistake 3: Overstating Business Losses to Manipulate Brackets

Schedule C losses reduce taxable income and can drop you into lower brackets, but FTB scrutinizes losses exceeding $25,000 or losses claimed for more than three consecutive years. Claiming $35,000 in “consulting expenses” against $40,000 in 1099 income creates a $5,000 net, but without receipts, this becomes audit bait.

California’s audit rate for Schedule C filers with losses is 4.7%, compared to 0.8% for W-2 only filers. Make sure every deduction has documentation including receipts, mileage logs, and business purpose notes.

KDA Case Study: Real Estate Investor Saves $7,200 Using Bracket Optimization

Marcus, a Los Angeles-based real estate investor, came to KDA in February 2026 with a tax problem. He owned three rental properties generating $48,000 in net rental income, plus he earned $89,000 from his W-2 job as an operations manager. His total income of $137,000 put him firmly in the 9.3% California bracket, and his 2025 tax bill was $8,950 in state tax alone.

We identified three immediate opportunities:

- Cost segregation study: Accelerated depreciation on one property created an additional $22,000 paper loss, reducing taxable income to $115,000

- Retirement contribution timing: Marcus increased his 401(k) contribution from $8,000 to $15,000, further reducing taxable income to $108,000

- Property tax prepayment: Paying 2027 property taxes in December 2026 added $4,800 in itemized deductions, dropping taxable income to $103,200

Final result: California taxable income dropped from $137,000 to $103,200. State tax liability decreased from $8,950 to $6,315, a savings of $2,635. Combined with federal tax savings of $4,565, Marcus saved $7,200 in total tax for a strategy implementation cost of $2,400, delivering a 3.0x first-year return.

The depreciation strategy continues providing benefits for five additional years, with projected cumulative savings exceeding $28,000. Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How 2026 California Brackets Compare to Previous Years

California adjusts tax brackets annually for inflation using the California Consumer Price Index. For 2026, brackets increased by approximately 3.2% compared to 2025, meaning threshold amounts rose but rates remained unchanged.

What Changed From 2025 to 2026

| Filing Status | 2025 Bracket Threshold (9.3%) | 2026 Bracket Threshold (9.3%) | Increase |

|---|---|---|---|

| Single | $65,581 | $67,671 | $2,090 |

| Married Filing Jointly | $131,160 | $135,342 | $4,182 |

| Head of Household | $88,443 | $91,240 | $2,797 |

If your income stayed flat from 2025 to 2026, you received a minor tax cut due to bracket expansion. A single filer earning exactly $67,000 both years saved approximately $27 in California tax because more of their income stayed in the 8% bracket instead of jumping to 9.3%.

Looking Ahead to 2027 Projections

Early estimates suggest 2027 California brackets will increase by another 2.8% to 3.4% based on projected inflation. This means the 9.3% bracket for single filers could start around $69,600 in 2027. For tax planning purposes, assume modest bracket expansion but no rate changes unless California legislation changes significantly.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions: California Tax Brackets 2026

Do California Tax Brackets Apply to All Income Types?

Yes, California taxes most income types using the same bracket structure: wages, self-employment income, rental income, capital gains, and interest. However, capital gains receive no preferential rate in California unlike federal tax. A $40,000 long-term capital gain is taxed at your ordinary income bracket rates (potentially 9.3% or higher), whereas federally it would be taxed at 15% for most taxpayers. This makes California particularly expensive for investors realizing large gains.

What Happens If I’m Right on the Edge of a Bracket?

Only the dollars exceeding the bracket threshold get taxed at the higher rate. If you’re a single filer earning $67,700 in 2026, you’re $29 into the 9.3% bracket. That means $67,671 gets taxed using the lower brackets (1%, 2%, 4%, 6%, 8%), and only $29 gets taxed at 9.3%. The additional tax cost is $2.70, not thousands. Never turn down income because you’re “close to the next bracket.”

How Do Bonuses and RSUs Affect My California Tax Bracket?

Bonuses and restricted stock units (RSUs) are taxed as ordinary income in the year received. California doesn’t offer special rates for these types of compensation. If your base salary is $95,000 and you receive a $25,000 bonus in December, your total California taxable income becomes $120,000, pushing you deeper into the 9.3% bracket. Employers often withhold at a flat supplemental rate (10.23% for California), but your actual liability depends on total annual income and bracket position. For detailed bonus tax calculations, check out this bonus tax calculator to estimate your actual take-home.

Can I Use Federal Tax Credits to Reduce My California Bracket?

No, federal credits don’t transfer to California returns. California has its own credit system including the Earned Income Tax Credit (CalEITC), Child and Dependent Care Credit, and Renter’s Credit. These credits reduce your final tax liability but don’t change which bracket your income falls into. Credits apply after bracket calculations are complete. For example, the CalEITC can reduce your tax bill by up to $3,417 if you qualify, but it doesn’t lower the rate at which your income is taxed.

Are There California Tax Brackets for Businesses?

California businesses pay different tax structures depending on entity type. C Corporations pay a flat 8.84% corporate tax rate on net income, not progressive brackets. S Corporations, LLCs, and partnerships are pass-through entities, meaning business income flows to owners’ personal returns and gets taxed using individual bracket rates shown in this article. LLCs also pay an annual LLC fee ranging from $800 to $11,790 based on gross receipts, separate from income tax. Understanding which structure minimizes your combined tax burden requires professional analysis of your specific situation.

Does Working Remotely for an Out-of-State Company Change My California Brackets?

No, if you’re a California resident working remotely for an out-of-state employer, all income is California-source income and taxed using California brackets. The location of your employer doesn’t matter; your residency determines tax obligation. You’ll pay California tax on 100% of your wages and may need to file a nonresident return in your employer’s state to claim a refund if they withheld taxes there. California offers a credit for taxes paid to other states, but you still calculate your California tax using the full bracket tables on all income.

How Does Moving to or From California During the Year Affect Brackets?

Part-year residents use a special calculation. You’ll file Form 540NR and report all income, but only pay California tax on California-source income plus income earned while a resident. For example, if you lived in California January through June earning $60,000, then moved to Texas and earned $60,000 there July through December, only the first $60,000 is subject to California brackets. The Texas income is reported but not taxed by California. Bracket calculations apply only to the taxable portion. Many taxpayers make errors here, so consider professional help if you moved mid-year.

Special Situations: High-Income Earners and the 13.3% Bracket

California’s 13.3% top bracket is the highest state income tax rate in the nation. It affects single filers with taxable income above $1,299,724 and married couples above $2,599,448. This rate applies to all income types including capital gains, making California particularly challenging for high-net-worth individuals and entrepreneurs realizing business sale proceeds.

The Mental Health Services Tax Addition

Income exceeding $1 million triggers an additional 1% Mental Health Services Tax, bringing the effective top rate to 13.3% total. This applies to taxable income, not gross income, so deductions matter significantly. A business owner with $1.5 million in gross revenue but $600,000 in legitimate business expenses has $900,000 in taxable income, staying below the $1 million threshold and avoiding the additional tax.

Strategies for High-Income Taxpayers

When income regularly exceeds $1 million, bracket strategies shift from timing deductions to structural planning:

- Charitable Remainder Trusts (CRTs): Defer capital gains recognition while receiving income stream, potentially spreading gain across multiple years and lower brackets

- Opportunity Zone investments: Defer and potentially exclude capital gains by investing in qualified Opportunity Funds

- Installment sales: Spread business sale proceeds across multiple years instead of recognizing all gain in one year

- Residency planning: Establishing residency in a no-income-tax state before a liquidity event can save 13.3% on the entire amount, but requires careful documentation and genuine residency change

For those considering estate planning strategies in conjunction with tax bracket management, our California business owner tax strategy hub provides comprehensive guidance on coordinating multiple planning elements.

Book Your California Tax Strategy Session

You just learned that California tax brackets work differently than you thought. You discovered that your withholding probably isn’t covering your actual liability. And you saw exactly how strategic planning saves thousands in state taxes every single year. But reading about strategies and implementing them correctly are two completely different things.

If you earned over $75,000 in 2026, have multiple income sources, own rental property, or received a windfall like RSUs or a bonus, you’re likely overpaying California taxes by $2,500 to $8,500 annually. The difference between figuring it out yourself and working with a California tax strategist is the difference between reading a medical textbook and seeing an actual doctor when you’re sick.

KDA specializes in California tax optimization for W-2 employees, 1099 contractors, business owners, and real estate investors. We don’t just file your return. We analyze your complete financial picture, identify bracket opportunities you’re missing, and build a multi-year tax plan that compounds savings. Most clients save 3x to 7x our fee in the first year alone.

Stop guessing whether you’re in the right bracket. Stop hoping your withholding is correct. Stop leaving thousands on the table because California’s tax code is deliberately confusing. Book your personalized California tax strategy session now and find out exactly what you’re missing.

This information is current as of 5/1/2026. Tax laws change frequently. Verify updates with the California Franchise Tax Board or IRS if reading this later.