California LLCs and Quarterly Tax Payments: The $15K Mistake Owners Keep Making in 2026

This year, the IRS and the California Franchise Tax Board will rack up record late-payment penalties from LLCs—most of it from missed or miscalculated quarterly estimated taxes. If you run a California LLC, ignoring these due dates can quietly cost $8,000–$30,000 a year, whether you’re netting $60,000 or $1.5M. Yet most owners and even experienced freelancers begin the year without knowing if or when they actually need to make these payments or how much the penalty is for getting it wrong.

Quick Answer: California LLCs are required to make quarterly estimated tax payments if their business (pass-through entity or single-member) expects to owe $500 or more to the IRS—or $800 or more to the state. If you’re projecting any profit, you’re almost certainly required to pay quarterly. Missing just one quarter brings a cascade of late fees, interest, and compounding penalties. This affects every LLC, from real estate investors to consultants to Main Street retail—regardless of whether you’re a new LLC, a seasoned operator, or just flipping a few properties on the side.

Who Must Make Quarterly Payments—and Who Gets a Pass?

Here’s the hard truth: do LLCs need to make quarterly payments in California? Nearly every LLC with a positive bottom line owes at least the $800 annual Franchise Tax Board (FTB) minimum. But for anyone who expects more than $500 in annual profit, you’re also on the IRS radar for federal estimated taxes. Even if you’re a single-member LLC (SMLLC) treated as a sole proprietorship, you, not the LLC, are responsible for IRS quarterly estimates—but the obligation never goes away.

- LLCs classified as partnerships, multi-member, or SMLLCs—filed as pass-through entities—are subject to California’s $800 minimum tax, due in quarterly installments, plus possibly entity income tax at the state level (1.5% for most, 0% for disregarded SMLLCs, but watch state apportionment rules).

- Newly formed LLCs in California enjoy a one-year FTB minimum tax holiday (for the first taxable year only)—but become subject to quarterly payment rules for the next tax year beginning January 1.

- LLCs classified as S Corps: Also owe quarterly, but rules differ—see our business owners entity structure page.

Myth: If your LLC didn’t make a profit last year or you’re holding losses forward, you can ignore quarterly payments.

Fact: Both the IRS and FTB require estimates if you expect profit this year. Losses from prior periods don’t automatically exempt you (unless you 100% offset expected gains) and penalties are automatic if you miss the safe harbor calculation per IRS Form 1040-ES guidance.

Strategically, even brand-new LLCs who aren’t “required” to pay quarterly should consider conservative estimates, because first-year profits (not subject to the $800 minimum, but are subject to federal taxes if over $1,000 due) can surprise.

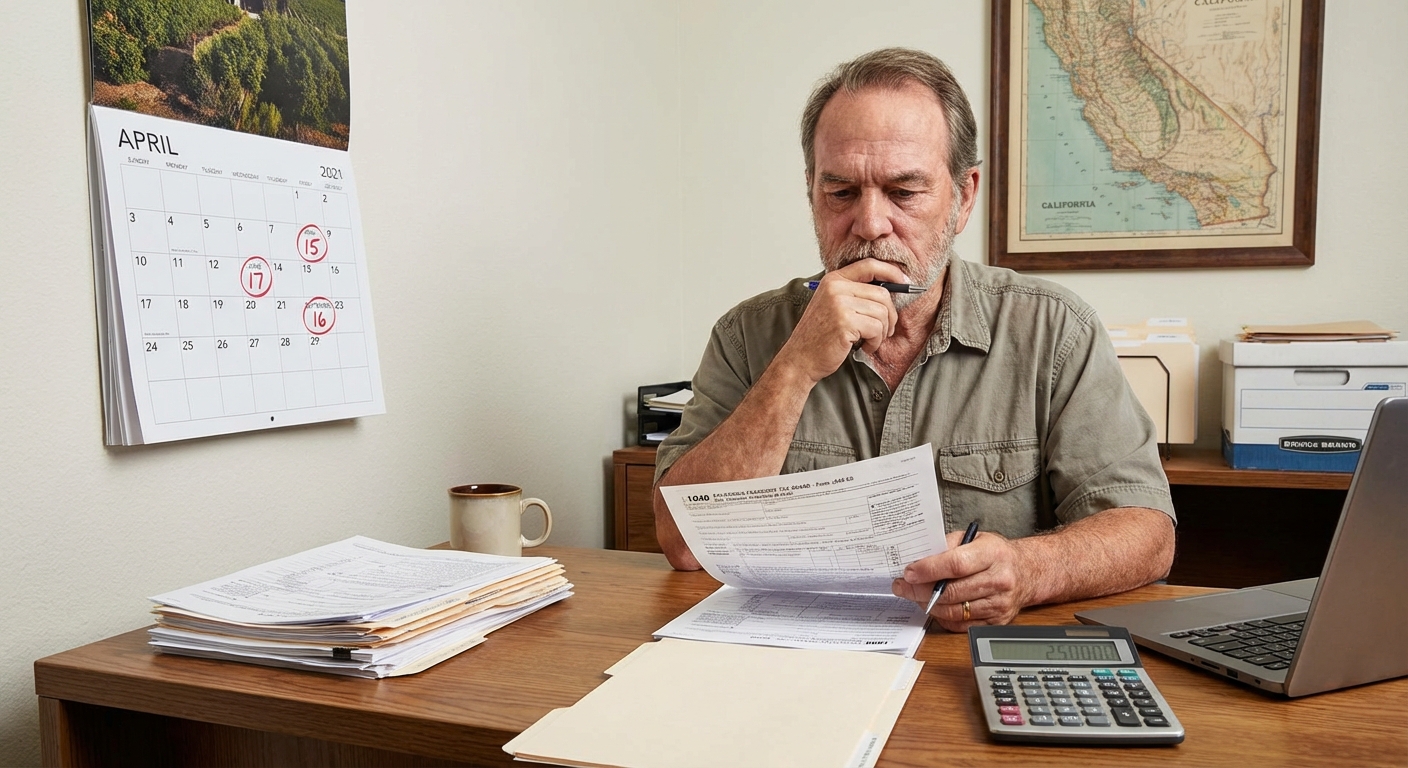

2026 Quarterly Estimated Payment Deadlines—What Actually Happens If You Miss?

Let’s walk through the real tax calendar for a California LLC in 2026. At the federal level, your estimated payments (Personal 1040-ES if SMLLC or Partnership; 1120-W if taxed as a corporation) are due four times a year:

- April 15: 1st Quarter (Jan 1–Mar 31)

- June 15: 2nd Quarter (Apr 1–May 31)

- September 15: 3rd Quarter (Jun 1–Aug 31)

- January 15 (next year): 4th Quarter (Sep 1–Dec 31)

California’s FTB expects either quarterly or annual payments for the $800 minimum (Form 3522), plus a form of entity-level “estimated fee” if your gross receipts top $250,000 (Form 3536, due by the 15th day of the 6th month of your tax year).

What’s the Penalty? Failure to pay the IRS on time is an automatic late filing and underpayment penalty, typically at 0.5% a month (plus interest), and the FTB tacks on another 5–25%. Example: On just $10,000 of missed payments, the FTB can rack up $1,200 in a year of missed estimates, and the IRS another $421. These stack up until the return and payment are filed.

For a tax calendar reference, check our detailed compliance calendar on the tax preparation and filing services page.

KDA Case Study: LLC Consultant Who Dodged $9,000+ in Penalties

Meet Jamie, a Los Angeles-based marketing consultant who launched an LLC in January 2024. After grossing just under $225,000 in her first year, she focused entirely on client work—skipping all quarterly estimated payments, having spent her cash on tools and hiring. Come April 2025, her CPA broke the news: her profit pushed her into $37,000 in IRS taxes—$14,700 owed to California—plus $8,875 in penalties and interest (IRS and FTB combined) for underestimating and missing every quarterly deadline.

She called KDA in panic. Here’s what we did:

- Created a six-quarter lookback, applying prior period loss carryforwards against profit, “catching up” her estimates in Q2, and working with the IRS to abate much of the federal late penalty using the first-time abatement program (FTB denied abatement).

- Set her up on automated quarterly payments for 2026—adjusted to fluctuate based on seasonality, not just last year’s taxes.

- Jamie’s net penalty outlay: $859 (down from $8,875 total), and a savings plan to ensure no more missed quarters. KDA fee: $2,400; ROI: 3.5x first-year recovery, plus future peace of mind.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How to Calculate & Pay Your Quarterly Estimated Taxes the KDA Way

Worried about “getting dinged” for making payments too high or too low? There’s an IRS safe harbor, and we use it for every LLC: If you pay at least 90% of what you owe this year or 100% of last year’s total tax (110% if AGI above $150,000), you avoid penalties, even if you underpay by a small amount. For most LLC owners, this boils down to running a quarterly profit-and-loss, then breaking out business income, allowable deductions, and deductible self-employment tax.

Here’s a simplified KDA-estimate workflow:

- Step 1: Add up all expected revenue from Jan–Mar, minus expenses. That’s your Q1 net profit.

- Step 2: Calculate self-employment tax (15.3%).

- Step 3: Federal income tax—use your bracket, subtract business deductions. California tax: start with $800, then run the FTB 568 calculation if your gross receipts are over $250,000.

- Step 4: Pay each quarterly amount using EFTPS online (for IRS) or WebPay (for FTB). Never mail a paper check unless you like payment delays and lost mail drama.

Want to see if you’re in penalty territory—or whether it’s better to overpay and refund later? Estimate your numbers in this small business tax calculator

If you need help with entity formation, see our entity formation services page for step-by-step guidance.

Pro Tip: If your LLC is having a seasonal slump (a slow summer or down Q4), you can adjust future quarters lower to avoid overpaying, as long as you meet the safe harbor by year-end. Don’t blindly pay “last year divided by four.”

Why Most LLC Owners Miss This Deduction

The classic trip-up? Mixing business and personal bank accounts, or failing to track irregular income spikes. Many LLC owners get an unexpected windfall (a big client payment, property sale, or one-off contract) mid-year. They don’t adjust their next quarterly estimate and get nailed for underpayment at year’s end.

Another trap: using your LLC as a “pass-through” and thinking you can push off taxes until the year is over. The IRS and FTB both look at current-year profit, not just prior-period net. Quarterly payments need to reflect this year’s real results. If you sell property or make a sudden profit, update your estimate—don’t wait until next January.

Red Flag Alert: The FTB sometimes sends delayed notices when you’re underpaid. So if you don’t catch a missed payment early (especially in Q2 or Q3), you can rack up two years of noncompliance before the audit letter lands. The fix? Use accounting software like QuickBooks or Xero, reconcile income monthly, and run a quarterly tax checkup—not just in April.

FAQ: Quarterly Payments for California LLCs—Your Next Questions Answered

What if my LLC made zero profit?

If you expect to make $0 taxable income for the year, you’re exempt from federal quarterly payments but still owe the California $800 minimum (unless it’s your first taxable year with the one-year holiday). If you later end up with more than $500 in profit, you’re retroactively required to pay, so quarterly is safer than skipping and hoping for the best.

Can I pay extra to cover a surprise windfall?

Yes. You can make additional “catch-up” estimated payments anytime, and the IRS will apply them to the current quarter. The FTB recognizes late but voluntary payments, but interest may still accrue until the balance is paid in full.

Will I get audited for missing a quarterly payment?

Missing a payment is not an audit trigger by itself, but the cumulative noncompliance is a red flag that increases your risk, especially if underpayments recur and your return is high-stakes (>$250,000 gross receipts for California, or big spikes in reported income versus payments made).

How do I know the right projected amount if my income fluctuates?

Do a rolling estimate each quarter, update your profit-and-loss projections. Put aside 25–32% of net profits each month into a tax account and adjust upward if you have a windfall quarter. When in doubt, work with a specialist—KDA builds custom payment calculators for LLC clients facing exactly this issue.

For a wider look at LLC tax strategy, dive into our ultimate LLC tax blueprint.

Book a Consultation with KDA to Avoid LLC Penalties

If you’re a California LLC owner unsure about your quarterly payment schedule—or worried you might already owe late payment penalties—don’t gamble with your profits or your peace of mind. Book a 30-minute strategy session with our LLC tax team and walk away knowing exactly what, when, and how much to pay, with a custom quarterly plan built for your real income swings. Click here to book your consultation now.