What Is the CA State Tax Percent in 2026?

California operates a progressive income tax system with ca state tax percent rates ranging from 1% to 13.3% depending on your income level. Unlike flat-rate states, California taxes higher earners at significantly higher percentages, which means your effective tax burden depends entirely on where you land in the state’s nine income tax brackets. For small business owners and W-2 employees, understanding these percentages is the difference between paying what you owe and overpaying thousands of dollars every year.

California’s 2026 tax brackets apply to both wage earners and business owners, but the way you structure your income, your entity type, and your deduction strategy can drastically change your effective tax rate. The top marginal rate of 13.3% kicks in at $1 million for married filers and $677,276 for single filers, making California the highest income-tax state in the nation. But here’s what most taxpayers miss: you don’t pay 13.3% on all your income. You pay it only on the portion that exceeds the top threshold.

How California’s Progressive Tax Brackets Actually Work

California uses a marginal tax rate system. This means each dollar you earn is taxed at the rate of the bracket it falls into. If you’re a single filer earning $80,000 in 2026, you don’t pay 9.3% on the entire amount. Instead, the first $10,412 is taxed at 1%, the next chunk at 2%, and so on up the ladder until your last dollars are taxed at 9.3%.

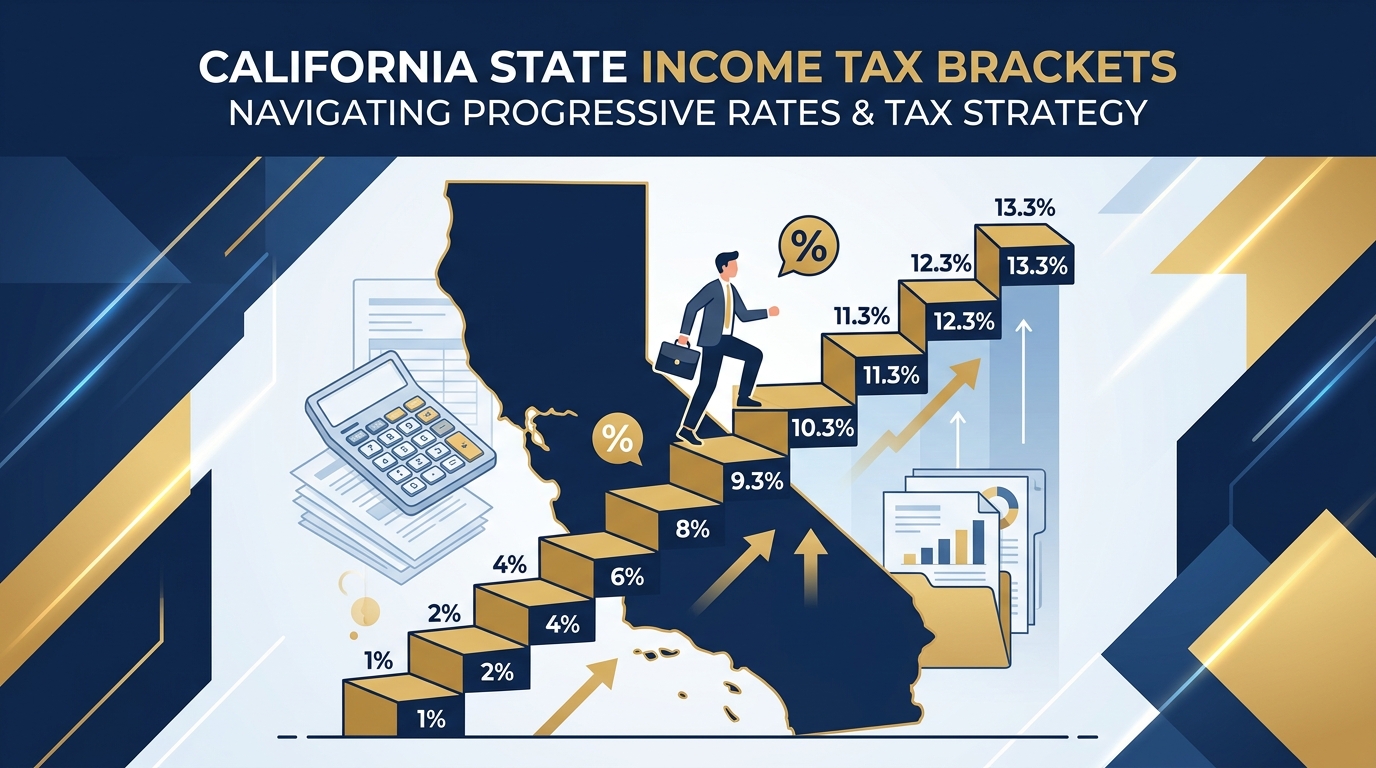

Here’s the 2026 California income tax bracket breakdown for single filers:

- 1% on income up to $10,412

- 2% on income from $10,413 to $24,684

- 4% on income from $24,685 to $38,959

- 6% on income from $38,960 to $54,081

- 8% on income from $54,082 to $68,350

- 9.3% on income from $68,351 to $349,137

- 10.3% on income from $349,138 to $418,961

- 11.3% on income from $418,962 to $677,275

- 12.3% on income from $677,276 to $1,000,000

- 13.3% on income over $1,000,000

For married filing jointly, the thresholds roughly double. The 9.3% bracket starts at $136,700, and the top 13.3% rate applies to income over $1,000,000.

This structure rewards strategic income planning. If you can keep your taxable income below certain thresholds by maximizing deductions, deferring income, or restructuring how you pay yourself, you avoid the higher marginal rates entirely.

Real-World Example: W-2 Employee

Sarah, a software engineer in San Francisco, earns $120,000 as a W-2 employee. Her employer withholds California state taxes throughout the year, but Sarah doesn’t realize she’s paying an effective rate of around 6.8% on her entire income, not the 9.3% marginal rate her last dollars fall into. By maximizing her 401(k) contributions ($23,000 in 2026) and claiming the standard deduction, she reduces her California taxable income to $97,000, saving approximately $2,140 in state taxes alone.

How Business Owners Can Reduce Their CA State Tax Percent

If you own an LLC, S Corp, or sole proprietorship in California, your business income flows through to your personal return and gets taxed at these same progressive rates. But business owners have far more control over their taxable income than W-2 employees. The key strategies include choosing the right entity structure, timing income and expenses, and leveraging California-specific deductions.

One of the most powerful moves for California business owners is electing S Corp status. Instead of paying self-employment tax plus California income tax on all your business profit, S Corp owners pay themselves a reasonable salary (subject to payroll taxes) and take the rest as distributions, which avoid the 15.3% self-employment tax. While distributions are still subject to California income tax, the overall tax savings can exceed $8,000 annually for businesses earning over $80,000 in profit.

S Corp Strategy Breakdown

Let’s say you run a consulting business as a single-member LLC and net $150,000 in profit. Under default LLC taxation, you pay approximately $21,186 in federal self-employment tax plus California income tax on the full $150,000. Your California state tax liability is roughly $10,200 (effective rate of 6.8%).

If you elect S Corp status and pay yourself a $70,000 salary with $80,000 in distributions, you eliminate self-employment tax on the $80,000 distribution, saving around $11,304 in federal SE tax. Your California income tax stays roughly the same because California doesn’t distinguish between salary and distributions for state income tax purposes, but the federal savings alone justify the election.

California also taxes S Corps with a 1.5% franchise tax on net income over $250,000, and all entities pay an $800 annual minimum franchise tax. Factor these costs into your planning before making the switch. For more details on entity structuring, explore our entity formation services.

California-Specific Deductions That Lower Your Tax Percent

California offers several state-specific deductions and credits that don’t exist at the federal level. These can significantly reduce your taxable income and drop you into a lower marginal bracket.

Renters’ Credit

If you rent your primary residence in California and meet income thresholds, you qualify for a renters’ credit of up to $120 for married filers and $60 for single filers. It’s a small benefit, but it’s often overlooked by renters who assume tax breaks only apply to homeowners.

Child and Dependent Care Credit

California offers a state-level child and dependent care credit that can be worth significantly more than the federal version, especially for lower-income families. The credit phases out at higher income levels, but middle-income families earning under $100,000 can claim hundreds of dollars.

College Access Tax Credit

If you contribute to certain California college access programs, you may qualify for a dollar-for-dollar tax credit. This isn’t widely advertised, but it’s one of the few true 1:1 credits available at the state level.

California Earned Income Tax Credit (CalEITC)

Low-to-moderate-income workers can claim the CalEITC, which provides a refundable credit of up to $3,417 for families with qualifying children. The income thresholds are strict (under $30,950 for families with three or more children in 2026), but for those who qualify, this credit can completely offset state tax liability and provide a refund.

Red Flag Alert: Common CA Tax Mistakes That Increase Your Percent

California’s Franchise Tax Board (FTB) is one of the most aggressive state tax agencies in the country. They audit more returns than most states, and they’re particularly focused on high earners, business owners, and anyone claiming residency outside California while maintaining ties to the state.

Mistake 1: Misclassifying Residency

If you moved out of California but still have property, business interests, or family in the state, the FTB may argue you’re still a California resident subject to tax on all your worldwide income. California uses a “domicile” test that looks at where your true home is, not just where you physically spend time. If you leave California, document the move with lease agreements, voter registration changes, and driver’s license updates.

Mistake 2: Ignoring the $800 Minimum Franchise Tax

Every LLC and corporation registered in California owes an $800 annual minimum franchise tax, even if the business made zero revenue. First-year LLCs get a waiver, but after that, the $800 is due every year by the 15th day of the 4th month after the start of your tax year. Missing this payment triggers penalties and interest that can exceed $1,000 within a year.

Mistake 3: Failing to Estimate Quarterly Payments

California requires estimated tax payments if you expect to owe more than $500 in state tax for the year. Business owners and 1099 contractors frequently underpay their estimates, which results in underpayment penalties. The penalty rate fluctuates but typically runs around 5-8% annually. Use FTB Form 540-ES to calculate and pay estimates on time.

KDA Case Study: Small Business Owner

Jason runs a digital marketing agency structured as a single-member LLC. He earned $210,000 in net profit in 2025 and paid roughly $16,800 in California state income tax (effective rate of 8%). Jason also paid over $29,000 in federal self-employment tax, bringing his total tax burden to nearly $70,000 after federal income tax.

KDA worked with Jason to elect S Corp status for 2026, set a reasonable salary of $95,000, and take the remaining $115,000 as distributions. We also identified $12,000 in overlooked business deductions, including home office expenses, software subscriptions, and professional development costs. The result: Jason saved $8,200 in self-employment tax and reduced his California taxable income enough to drop into a lower effective bracket, saving an additional $1,400 in state taxes.

Total first-year savings: $9,600. KDA’s advisory fee: $3,500. Jason’s first-year ROI: 2.7x, with ongoing annual savings every year forward.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

What Happens If You Underpay California State Tax?

The FTB doesn’t mess around. If you underpay your California state tax, you’ll face interest charges and potential penalties. The underpayment penalty applies if you didn’t pay at least 90% of your current year tax liability or 100% of your prior year liability through withholding and estimated payments.

Interest accrues daily on any unpaid balance, and the rate adjusts quarterly. As of early 2026, the FTB interest rate is approximately 5% annually. That may not sound steep, but combined with penalties, a $5,000 underpayment can cost you an extra $500 or more within a year.

If you can’t pay your full tax bill by the April deadline, file your return on time anyway and request a payment plan. The FTB offers installment agreements for balances under $25,000 with relatively simple approval processes. Filing late triggers a failure-to-file penalty of 5% per month (up to 25% of the unpaid tax), which stacks on top of interest.

Pro Tip: Safe Harbor Estimated Payments

To avoid underpayment penalties entirely, use the “safe harbor” rule. Pay at least 100% of your prior year California tax liability through withholding and estimates (110% if your prior year income exceeded $150,000). Even if your income spikes in the current year, you’re protected from penalties as long as you hit the safe harbor threshold.

How the 2026 Billionaire Tax Act Could Impact CA Tax Policy

California voters will decide this November on the Billionaire Tax Act, a one-time 5% wealth tax on residents with net worth exceeding $1 billion. If it passes, it would be the first billionaire-specific wealth tax in the world and could generate nearly $100 billion in revenue over five years. The tax would apply to billionaires who were California residents as of January 1, 2026, meaning those who left the state after late 2025 are still on the hook.

For the average small business owner or W-2 employee, this measure has no direct impact. Your income tax rates won’t change. But the passage of a wealth tax signals California’s willingness to push aggressive tax policies, which could lead to future proposals targeting high-income earners below the billionaire threshold. Some tax policy experts warn that once a wealth tax framework is established, it becomes easier to lower the threshold in future years.

The counterargument is that California needs the revenue to offset federal funding cuts and address budget shortfalls. The state’s progressive tax system already relies heavily on high earners: the top 1% of taxpayers pay nearly 50% of all California income tax revenue. A wealth tax would diversify that base slightly, but it also increases the risk of capital flight if ultra-wealthy residents relocate to zero-income-tax states like Nevada or Texas.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About California State Tax Percent

Do I Pay CA State Tax on Out-of-State Income?

Yes, if you’re a California resident. California taxes all your worldwide income, regardless of where you earned it. If you work remotely for an out-of-state employer while living in California, you pay California income tax on those wages. Non-residents only pay California tax on income sourced from California (like rental property income or wages earned while physically working in the state).

Is Social Security Income Taxed in California?

No. California is one of the few states that does not tax Social Security benefits. If your only income is Social Security, you’ll owe zero California state income tax. This makes California relatively retiree-friendly for those living on fixed Social Security income, despite the high tax rates on other income types.

How Does California Tax Remote Workers?

If you’re a California resident working remotely for an out-of-state company, California taxes your wages. If you’re a non-resident working remotely for a California company while living in another state, California generally does not tax those wages (but there are exceptions for certain executive-level employees). The key factor is your residency status, not your employer’s location.

Can I Deduct State Taxes on My Federal Return?

Yes, but the SALT (state and local tax) deduction is capped at $10,000 per year under current federal law. This means if you paid $15,000 in California income tax, you can only deduct $10,000 on your federal return. High earners in California are hit hardest by this cap, which is why strategic tax planning at the state level becomes even more important.

What Is California’s Franchise Tax?

The franchise tax is a separate tax California imposes on corporations and LLCs for the privilege of doing business in the state. All entities pay an $800 minimum annually, even with zero income. S Corps and C Corps with net income over $250,000 also pay an additional 1.5% franchise tax on California-sourced income. This is separate from personal income tax and applies regardless of your individual tax situation.

Action Steps to Lower Your California Tax Percent in 2026

Your California state tax percent isn’t set in stone. With the right strategies, you can legally reduce your effective rate and keep thousands of dollars in your pocket every year. Here’s your checklist:

- Maximize retirement contributions: Every dollar you put into a traditional 401(k) or IRA reduces your California taxable income. For 2026, you can contribute up to $23,000 to a 401(k) ($30,500 if over 50) and up to $7,000 to an IRA ($8,000 if over 50).

- Consider S Corp election: If your business nets over $60,000 annually, S Corp status can save you thousands in self-employment tax without increasing your California income tax burden.

- Document all business expenses: Home office deductions, vehicle mileage, software subscriptions, and professional development costs all reduce your taxable income. Keep receipts and use accounting software to track everything.

- Claim California-specific credits: Don’t leave money on the table. Renters’ credits, dependent care credits, and education credits can add up to hundreds or thousands in savings.

- Pay estimated taxes on time: Avoid underpayment penalties by making quarterly payments or hitting the safe harbor threshold based on your prior year liability.

- Review your residency status: If you split time between California and another state, make sure your residency determination is accurate to avoid double taxation or FTB audits.

This information is current as of 5/30/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Book Your Tax Strategy Session

If you’re tired of overpaying California state taxes because you’re not sure which deductions you qualify for or how to structure your business income, let’s fix that. Our team specializes in California tax strategy for business owners, 1099 contractors, and high-income W-2 employees. We’ll review your situation, identify opportunities you’re missing, and build a plan that saves you real money. Click here to book your consultation now.