C Corp vs S Corp vs Partnership in 2026: Why Picking the Wrong Entity Could Cost You $30,000+

Nearly 90% of California business owners and savvy investors are operating in the dark about which business entity—C Corp, S Corp, or Partnership—is actually costing them thousands every single year in 2026. Old-school advice (“Just set up an S Corp if you want to save on taxes!”) doesn’t fit the new IRS scrutiny, rising California payroll taxes, and complex passive income rules facing W-2 earners, 1099 contractors, LLC owners, and real estate investors right now.

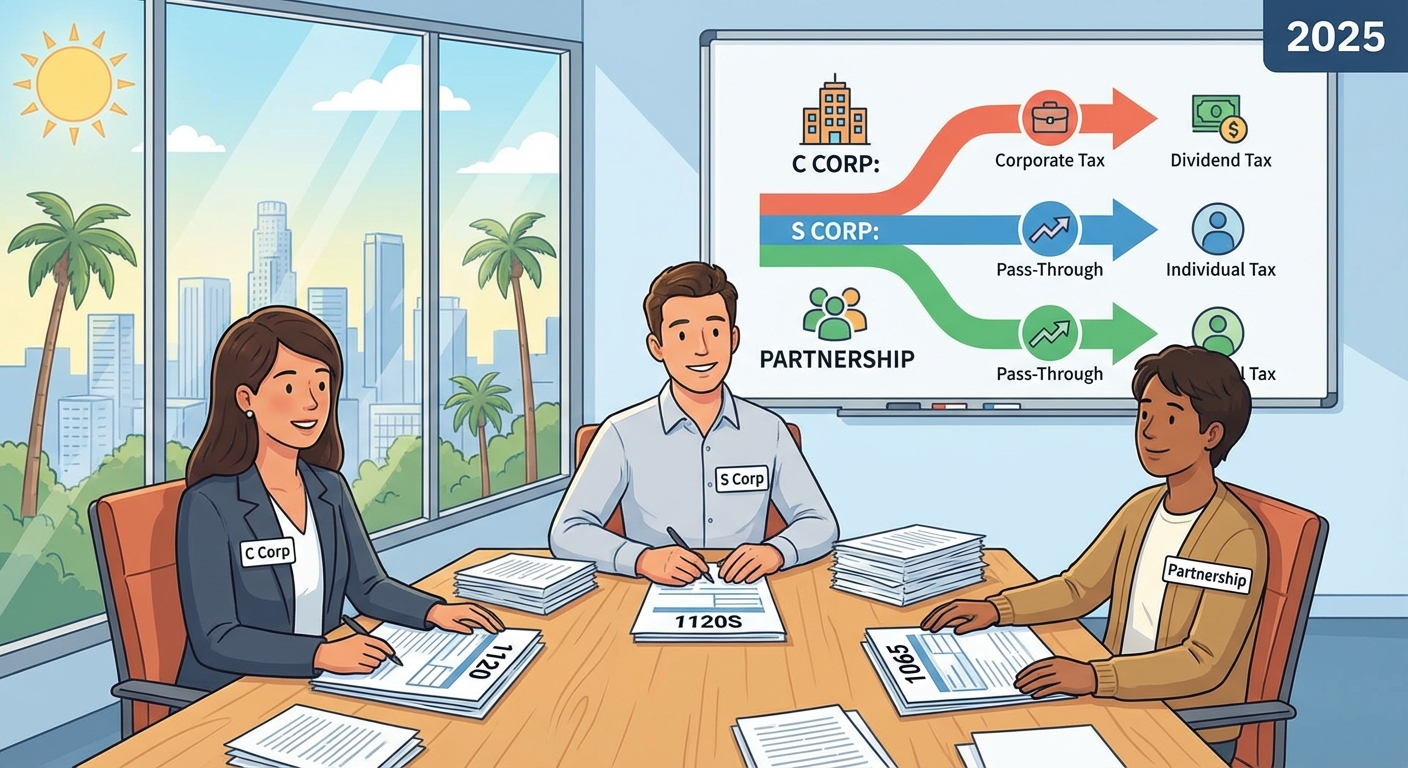

C Corp vs S Corp vs Partnership is not a theoretical debate—these choices are the difference between outsmarting taxes and getting hammered with double-taxation, missed deductions, or even an audit. Knock-on effects range from surprise Medicare taxes for S Corp owners, to missed 20% QBI deductions for partnerships, to C Corp double tax bills that take years to fix. If you’re not running the numbers on entity type every year, you are leaving hard cash (and audit triggers) on the table.

Quick Answer: Which Entity Saves the Most Taxes in 2026?

While there is no single “best” entity, here’s the plain English takeaway for 2026:

- S Corp: Often lowest total tax for owner-operators making $90K–$350K/year in net profit; payroll is required, but distributions can escape self-employment taxes.

- Partnership: Most flexible for investors with passive income or shares in real estate, but often higher self-employment tax exposure for active partners unless structured properly.

- C Corp: Best when long-term reinvestment, funding, or complex ownership is needed (think rapidly growing tech or multi-partner startups). Downside: possible double taxation of profits and dividends.

The difference between entities for a typical $200,000 solo business owner in 2026? Up to $32,400 in tax savings, compliance costs, or lost deductions—every year.

This blog will break down each structure, bust the biggest myths, and give you example scenarios for W-2 employees, 1099 consultants, LLC owners, and real estate investors in California.

Section 1: S Corp (S Corporation)—The ‘Flexible Salary’ Loophole Most Owners Misuse

S Corporations offer a unique advantage for business owners: distributions (profits taken out by the owner) aren’t subject to self-employment tax, only Social Security and Medicare on the salary portion. The IRS requires a “reasonable” salary, but anything above is fair game for FICA savings. For 2026, the Social Security wage base is $168,600, with Medicare at 2.9% plus 0.9% for high-earning owners (see IRS Publication 15).

Example:

• Solo consultant, net income of $200,000.

• As an S Corp, sets salary at $90,000 (passes IRS ‘reasonableness’ test for their field).

• Remaining $110,000 is taken as a distribution, not subject to self-employment tax.

• Estimated savings: $16,830 per year versus sole proprietor or Partnership (calculated at 15.3% SE tax avoided on $110,000).

But here’s the trap: Underpay your salary, and IRS auditors are hunting for you. Overpay, and the benefits are wiped out by wasted payroll taxes and admin costs. Many business owners forget to document the salary justification—which can trigger IRS scrutiny and back-tax penalties.

Our tax planning team routinely sees California LLCs benefit from electing S Corp status starting at just $50,000 in steady profit, especially with QBI deductions still in play through 2026 (IRS QBI rules).

Pro Tip: Revisit your salary/distribution split every January—failing to adjust for profitability changes is the fastest way to lose your S Corp advantage or end up in IRS crosshairs.

KDA Case Study: LLC Owner Restructures, Saves $25,800 in First Year

Mark, an Orange County tech consultant (1099 income, $180,000 net profit) started with a standard LLC. After reviewing his books, he realized nearly $27,500 went to self-employment tax. KDA restructured his business as an S Corp, set up compliant payroll at $85,000 with formal documentation, and moved the remainder to distributions. Not only did Mark save $13,455 in payroll taxes his first year, but KDA also uncovered missed deductions for home office, vehicle expenses, and health insurance—unlocking an additional $12,425 in tax savings. Mark paid $4,000 in tax strategy and payroll setup, netting a 6.4x ROI in year one. With proactive planning and quarterly check-ins, Mark projects $65,000 in cumulative tax savings over five years.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Section 2: Partnership—Flexible, But Can Trigger Sneaky Self-Employment Taxes

Partnerships (including LLCs taxed as partnerships) are the backbone entity for real estate investors, family businesses, and multi-owner companies. They allow full freedom over profit allocation, real property write-offs, and creative structuring through the IRS Form 1065. However, there’s a catch: active partners owe self-employment tax on their guaranteed payments and share of active income—often ignored by DIY tax filers.

Example:

• Husband-wife real estate team in San Diego, Partnership net profit: $240,000.

• Each takes $60,000 as “guaranteed payments” (runs through payroll; subject to SE tax), remaining $120,000 split as partnership income.

• Total SE tax hit: $36,720—about $7,200 more than if their structure allowed for S Corp distributions.

However, for investors not “materially participating,” this structure shines: partnership income allocated to passive partners isn’t subject to self-employment tax, making this entity the winner for complex real estate deals or silent partners.

For a more advanced breakdown of these strategies, review the current California S Corp tax playbook.

Section 3: C Corp—Double Taxation Isn’t Always the Villain (Especially at Scale)

C Corporations (filing on Form 1120) get bashed for “double taxation”—but sophisticated business owners and high-net-worth investors still use them for a reason. Only C Corps can retain profits (paying just the 21% federal flat rate plus California’s 8.84%). Unlike pass-through entities, you only pay personal income tax on what you take as dividends or wages, not on total company profit.

Example:

• Growth-focused wellness startup, $750,000 pre-tax profit (2026).

• Reinvests $450,000, pays owner/founder $180,000 salary. Corporation owes ~$66,300 federal and $39,780 California taxes, but owner only pays individual taxes on salary/dividends.

• This structure allows scaling, shareholder expansion, and even attracts institutional investors.

The downside: If you distribute big profits as dividends, there’s a federal 15–20% tax plus additional California income tax—this is where “double taxation” pinches. Most small businesses don’t need a C Corp, but for venture-backed startups or those seeking IPOs, it’s still the standard structure.

Red Flag Alert: Personal expenses or ‘loans’ running through a C Corp can easily trigger audits, leading to “constructive dividends” and harsh penalties. Keep ironclad records and avoid co-mingling funds.

Section 4: Why Most Owners Choose the Wrong Entity (and How IRS Cracks Down in 2026)

The biggest mistake? Picking an entity based on outdated rules, “set-it-and-forget-it” mindset, or one-size-fits-all internet advice. IRS auditors have new algorithms in 2026 to red-flag mismatches: think S Corps with under-market salaries, Partnerships without material participation logs, or C Corps engaged in owner-employee games.

- If your S Corp has sub-$60,000 salary on $300,000 profit? Expect a letter.

- LLCs with K-1s going to “phantom” partners? Big audit bait.

- C Corp owners living the high life with no dividend reporting? That’s an audit in the making.

This failure to adapt is costing typical KDA business clients $17,000–$38,000 every year in wasted tax, missed deductions, or avoidable penalties.

Want to test which entity actually saves you the most based on your 2026 numbers? Use this small business tax calculator to run your projections for C Corp vs S Corp vs Partnership scenarios.

Section 5: Common Questions About Entity Strategy for W-2, 1099, and Investors

What If My Income Fluctuates Year-to-Year? Can I Switch Entities?

Yes. Many W-2 moonlighters or seasonal 1099 earners can elect S Corp status for some years or revert to a Partnership/LLC as needed. For smooth transitions, document all filings (Form 2553 for S Corp, detailed partnership agreements, and state compliance with the CA Franchise Tax Board).

Which Entity Is Best for Real Estate Investors?

LLCs taxed as Partnerships are often optimal for asset holding and liability—not S Corps. But adding the right structure (such as holding partnerships and management S Corps) can maximize depreciation, passive losses, and protect from IRS anti-abuse rules. Learn more about structures for real estate activity on our real estate investor hub.

Can I Still Deduct Health Insurance and Retirement Plan Contributions?

Generally, yes—all three entities allow for deductions, but the mechanics differ (deduct on the corporate level for C Corps, with AGI adjustments for S Corps and Partnerships). Review IRS Publication 535 for entity-specific deduction rules.

Section 6: The Right Entity—How We Engineer True $20,000+ Tax Savings Each Year

Here’s how KDA approaches bespoke entity structuring for California clients:

- Dive into real, current numbers—no cookie-cutter checklists

- Map out a year-by-year scenario with tax modeling for S Corp vs Partnership vs C Corp

- Consider state compliance (California’s minimum $800 annual fee, CA S Corp tax on net income, FTB filing risks)

- Layer advanced tactics: QBI stacking, home office optimization, Augusta Rule, accountable plans

- Quarterly re-reviews to avoid costly surprises and keep your ROI high

This is why entity formation and tax planning aren’t DIY projects for serious businesses.

This information is current as of 1/21/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Fast Tax Facts by Entity for 2026

- C Corp: Flat 21% federal tax + 8.84% CA; can retain earnings; double taxation on dividends

- S Corp: Pass-through, but California assesses its own S Corp tax; salary/distribution split is vital

- Partnership: Great for multiple owners and real estate; full flexibility on allocations; self-employment tax risk

FAQ: Entity Structures

How hard is it to switch from LLC to S Corp?

Switching is typically a one-time IRS election (Form 2553). The transition is straightforward but must be made within 2.5 months of the tax year you want it to apply. Payroll updates and state paperwork are a must.

Can W-2 employees benefit from an S Corp?

If you only have W-2 income, S Corp status doesn’t help. However, if you earn 1099 or have side-gig income, shifting that income to an S Corp can dramatically reduce taxes, especially above $60,000 net.

What about multi-state businesses?

Each state is different. California is notoriously aggressive about out-of-state income and nexus. Speak with an expert to model cross-state tax impacts and compliance.

Book Your Entity Structure Review and Cut Your 2026 Taxes Now

If your CPA hasn’t run a detailed S Corp vs C Corp vs Partnership scenario for your 2026 situation, you’re almost guaranteed to be leaving tax dollars on the table. Book a custom KDA strategy session today and we’ll review your actual numbers—not just check boxes—so you get the right structure, maximum legal write-offs, and real clarity on where your money goes. Click here to book your consultation now.