Quick Answer

The C Corp vs S Corp Trump tax law debate changed permanently in 2025 when the One Big Beautiful Bill Act (OBBBA) locked in the 20% QBI deduction for S Corp owners, restored 100% bonus depreciation, raised Section 179 to $2.5 million, and expanded the SALT cap to $40,000. C Corps still pay a flat 21% federal rate plus dividend taxes on distributions. For most California business owners earning $100,000 to $350,000 in profit, the S Corp now delivers $16,600 to $64,700 more per year in tax savings than a C Corp. The gap widened under Trump, not narrowed.

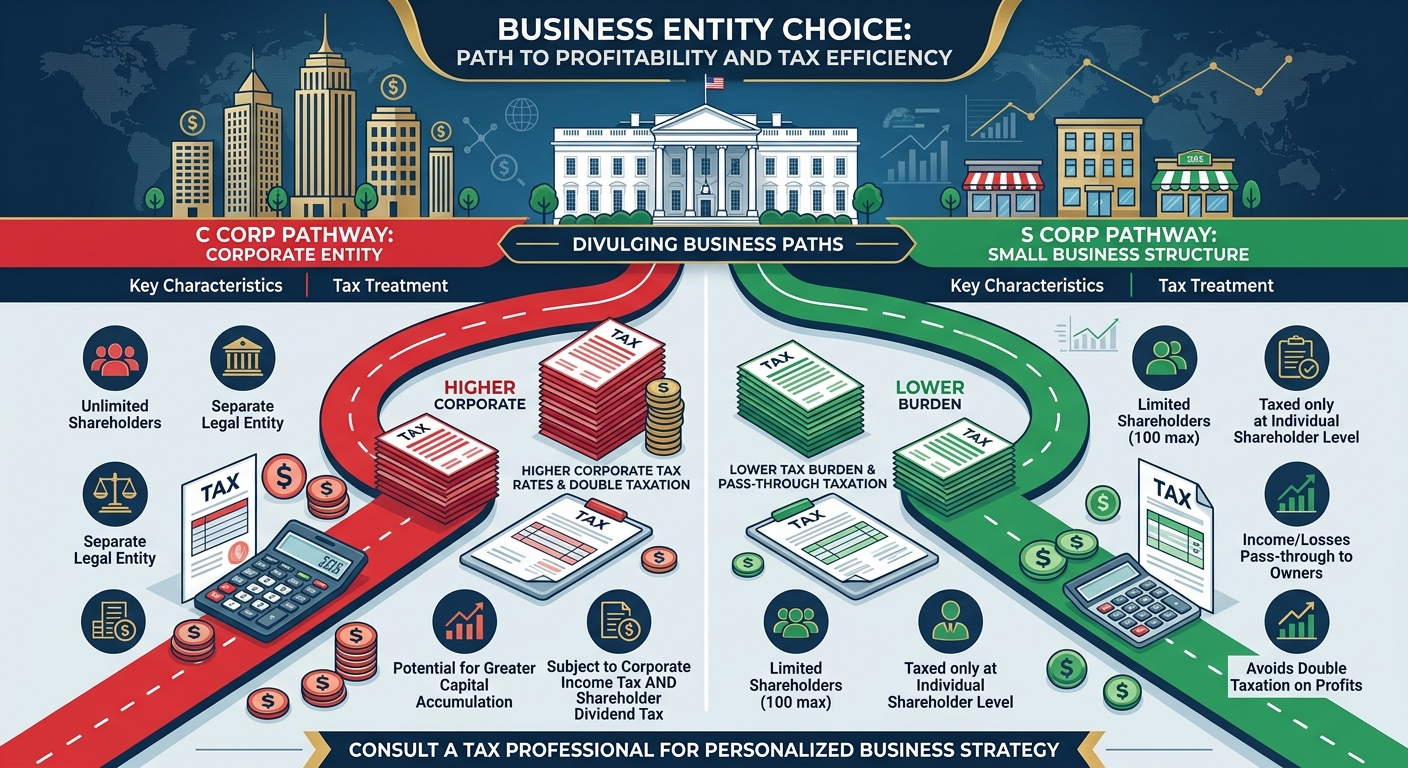

Why the Trump Tax Overhaul Makes the C Corp vs S Corp Decision Even More Expensive to Get Wrong

Most California business owners heard the headline: Trump signed the One Big Beautiful Bill Act, and corporate taxes stayed at 21%. They assumed that meant C Corps won. That assumption is costing them between $16,600 and $64,700 every single year in unnecessary taxes.

The 21% C Corp rate is real. But it is only one layer in a five-layer tax stack that applies when you try to actually use the money your business earns. The moment you take a distribution, dividend taxes kick in at 15% to 23.8%. California adds 8.84% franchise tax on C Corp profits before distributions. And the S Corp advantages that OBBBA made permanent, including the QBI deduction under IRC Section 199A, 100% bonus depreciation, and the expanded SALT cap bypass through AB 150 PTE election, do not apply to C Corporations at all.

The real question behind C Corp vs S Corp Trump era tax planning is not which entity pays a lower headline rate. It is which entity lets you keep more money after every layer of taxation is applied. For California business owners, the answer has never been clearer.

The Five Tax Layers That Separate C Corp From S Corp Under the OBBBA

Understanding the full tax picture requires looking at all five layers that hit C Corp owners but not S Corp owners. Here is the breakdown at $200,000 in business profit for a California owner.

Layer 1: Federal Entity-Level Tax

A C Corporation pays 21% federal corporate tax on all profits. That is $42,000 on $200,000. An S Corporation pays 0% at the entity level because profits pass through to the owner’s personal return. Advantage: S Corp by $42,000 at this layer alone.

Layer 2: California Franchise Tax

California charges C Corps 8.84% franchise tax on net income. On $200,000, that is $17,680. S Corps pay only 1.5% franchise tax, which equals $3,000. Advantage: S Corp by $14,680. This difference alone covers the cost of professional tax planning for most businesses.

Layer 3: Federal Dividend Double Taxation

After paying corporate tax, the C Corp owner receives distributions taxed as qualified dividends at 15% to 23.8% depending on income level. On $200,000 profit after corporate taxes, roughly $140,320 remains. At 18.8% (including the 3.8% Net Investment Income Tax), dividend tax adds another $26,380. S Corp distributions above reasonable salary are not subject to this second layer. Advantage: S Corp by $26,380.

Layer 4: QBI Deduction Exclusivity

The OBBBA permanently extended the Qualified Business Income (QBI) deduction under IRC Section 199A. This allows S Corp owners to deduct up to 20% of their qualified business income from taxable income. On $200,000 in S Corp profit, the QBI deduction could reduce taxable income by $40,000, saving $8,880 in federal taxes at the 22% bracket. C Corps are permanently excluded from claiming QBI. Advantage: S Corp by $8,880.

Layer 5: AB 150 PTE Election

California’s AB 150 allows S Corps (and partnerships) to make a Pass-Through Entity tax election that effectively bypasses the federal SALT cap. Under OBBBA, the SALT cap increased from $10,000 to $40,000, but many California owners still exceed it. The PTE election lets the entity pay state taxes at the entity level, converting them into a federal deduction. C Corps cannot use this election. Advantage: S Corp by variable amount, often $3,000 to $8,000 annually.

When you stack all five layers together, the total S Corp advantage at $200,000 profit ranges from $37,000 to $42,000 per year. If you want to see how your specific numbers shake out, run your business profit through this small business tax calculator to estimate your total tax burden under each entity type.

Side-by-Side Tax Comparison Table

| Tax Layer | C Corp ($200K Profit) | S Corp ($200K Profit) |

|---|---|---|

| Federal Entity Tax | $42,000 (21%) | $0 (0%) |

| CA Franchise Tax | $17,680 (8.84%) | $3,000 (1.5%) |

| Federal Dividend Tax | $26,380 (18.8%) | $0 |

| QBI Deduction Savings | $0 (ineligible) | $8,880 saved |

| AB 150 PTE Benefit | $0 (ineligible) | $3,000 to $8,000 |

| Total Tax Burden | $86,060+ | $43,700 to $48,700 |

That is not a rounding error. That is the difference between building wealth and subsidizing the IRS.

What OBBBA Actually Changed for S Corps and C Corps in 2026

The One Big Beautiful Bill Act, signed in 2025, made several provisions permanent that were set to expire. Many business owners still do not realize the full scope of what happened. Here is what matters most for entity selection.

QBI Deduction Made Permanent

The 20% QBI deduction under IRC Section 199A was originally scheduled to expire after 2025. OBBBA made it permanent. For S Corp owners, this means a guaranteed deduction on qualified business income every year going forward. C Corp owners cannot claim this deduction, period. At $300,000 in S Corp profit, the QBI deduction saves roughly $13,320 annually in federal taxes alone.

100% Bonus Depreciation Restored

Bonus depreciation had been phasing down from 100% to 80%, 60%, and eventually 0%. OBBBA restored it to 100% permanently. Both C Corps and S Corps can use bonus depreciation, but here is the California trap: California does not conform to federal bonus depreciation under Revenue and Taxation Code Sections 17250 and 24356. This means California business owners must maintain dual depreciation schedules regardless of entity type. The advantage for S Corp owners is that they can pair 100% federal bonus depreciation with QBI and PTE election savings, creating a triple-stack that C Corp owners cannot replicate.

Section 179 Increased to $2.5 Million

OBBBA doubled the Section 179 expensing limit from $1.25 million to $2.5 million. This lets businesses deduct the full purchase price of qualifying equipment and property in the year it is placed in service. California caps Section 179 at $25,000, creating another dual-schedule requirement. For S Corp owners, the federal deduction flows through to the personal return and stacks with QBI savings. For C Corp owners, the deduction reduces corporate profit but does not eliminate the double taxation on distributions.

SALT Cap Raised to $40,000

The state and local tax deduction cap increased from $10,000 to $40,000 under OBBBA. For individual filers, this helps. But California owners paying $20,000 or more in state taxes still benefit from the AB 150 PTE election, which converts state taxes into a federal business deduction with no cap. S Corps and partnerships qualify. C Corps do not.

QSBS Section 1202 Expanded

OBBBA expanded Qualified Small Business Stock benefits with new 50% and 75% gain exclusion tiers. This is the one area where C Corps have an advantage, but it only applies when selling company stock after holding it for at least five years. Most California small business owners are not selling shares to outside investors. They are drawing income to pay their mortgage. For those owners, the S Corp wins every time.

For a complete breakdown of how these changes interact with California rules, see our comprehensive S Corp tax strategy guide for California.

The Three Narrow Scenarios Where a C Corp Still Wins Under Trump Tax Rules

Not every business should be an S Corp. There are three specific situations where a C Corporation makes more sense even under the OBBBA framework. But they are narrower than most people think.

Scenario 1: Venture Capital Funding

If you are actively raising institutional venture capital, investors typically require a C Corp structure because they need preferred stock classes, and S Corps are limited to one class of stock under IRC Section 1361(b)(1)(D). Angel investors and VCs want convertible notes, preferred shares, and liquidation preferences that S Corps cannot offer. If you are pitching Sand Hill Road or raising a Series A, a C Corp is likely the right structure for now.

Scenario 2: QSBS Section 1202 Play

If your plan is to build the business and sell the stock in five or more years, the QSBS exclusion under IRC Section 1202 can exclude up to $10 million in capital gains from federal tax. OBBBA added new 50% and 75% tiers with a 28% rate on the included portion. This benefit is only available to C Corp shareholders. But here is the catch: you must hold the stock for at least five years, the corporation must be a C Corp when the stock is issued, and California does not conform to the QSBS exclusion. You will owe California’s 13.3% capital gains rate on the full gain regardless. So the QSBS play works best for non-California exits.

Scenario 3: Full Profit Retention Below $250,000

If you plan to retain 100% of profits inside the corporation and never take distributions, the flat 21% C Corp rate beats the top individual rate of 37%. But the accumulated earnings tax under IRC Section 531 imposes a 20% penalty on profits retained beyond reasonable business needs. The IRS considers retained earnings above $250,000 presumptively unreasonable unless you can document specific capital needs. Most small business owners cannot retain that much without triggering scrutiny.

If none of these three scenarios describe your business, the S Corp is almost certainly the better choice under current tax law.

The Five Costliest Mistakes California Owners Make When Choosing Between C Corp and S Corp After Trump Tax Changes

Mistake 1: Trusting the 21% Headline Rate

The 21% rate looks attractive on paper. But it only applies to profits sitting inside the corporation. The moment you take a distribution, dividend taxes, California franchise tax, and payroll tax obligations push the effective rate to 47% or higher. Comparing 21% corporate tax to a 37% individual rate without accounting for double taxation is the most common error, and it costs California owners an average of $37,000 per year at $200,000 profit.

Mistake 2: Staying in the Default C Corp Structure

When you incorporate in California without filing Form 2553, you default to C Corp status. Many owners do not realize this until their first tax return. Every year you stay as a default C Corp costs you the full five-layer tax disadvantage. Filing Form 2553 with the IRS and Form 3560 with the California Franchise Tax Board is the single most impactful tax election most business owners will ever make.

Mistake 3: Missing the March 15 Form 2553 Deadline

To elect S Corp status for the current tax year, Form 2553 must be filed by March 15. Miss it, and you remain a C Corp for the entire year. Late election relief is available under Revenue Procedure 2013-30, but it requires demonstrating reasonable cause and adds complexity. Many owners discover this deadline after it has passed and lose an entire year of S Corp savings.

Mistake 4: Ignoring California Bonus Depreciation Nonconformity

OBBBA restored 100% federal bonus depreciation permanently. But California does not allow bonus depreciation under R&TC Sections 17250 and 24356. This means every California business must maintain two separate depreciation schedules: one for federal and one for state. Owners who claim bonus depreciation on their federal return and forget to adjust for California end up with FTB notices and recalculated state tax bills. Our tax planning services help California owners navigate these dual requirements and avoid costly correction filings.

Mistake 5: Skipping the AB 150 PTE Election

Even with the SALT cap raised to $40,000, California S Corp owners who skip the AB 150 Pass-Through Entity election leave money on the table. The PTE election converts state income taxes into a federal business deduction with no cap, effectively bypassing the SALT limitation entirely. C Corp owners cannot use this election. S Corp owners who forget to make the election by the deadline lose this benefit for the entire year.

KDA Case Study: Sacramento Tech Founder Saves $41,800 by Converting From C Corp to S Corp Under OBBBA

Marcus, a Sacramento-based software development firm owner, incorporated as a C Corp in 2021 because his attorney told him it was the “standard business structure.” For four years, Marcus paid combined federal and California taxes at an effective rate of 47.1% on $200,000 in annual profit. That meant $94,200 in total taxes each year.

When Marcus came to KDA in early 2026, we ran a five-layer tax analysis comparing his C Corp structure against an S Corp election under the new OBBBA provisions. The results were clear: Marcus was overpaying by $41,800 per year.

Here is what KDA did:

- Filed Form 2553 with the IRS and Form 3560 with the California FTB to elect S Corp status

- Set a reasonable salary of $85,000 and restructured the remaining $115,000 as distributions, eliminating self-employment tax on that portion

- Activated the QBI deduction under IRC Section 199A, saving $8,880 in federal taxes

- Filed the AB 150 PTE election to bypass the $40,000 SALT cap, saving an additional $4,200

- Set up dual depreciation schedules for California nonconformity compliance

- Evaluated and cleared Built-In Gains exposure under IRC Section 1374 with a five-year recognition period analysis

- Implemented a Solo 401(k) contributing $23,500 in employer contributions

Year One Results:

- Total tax savings: $41,800

- KDA fees: $5,800

- Net benefit: $36,000

- ROI: 7.2x first-year return

- Projected five-year savings: $209,000

Marcus went from one of the highest effective tax rates in California to one of the lowest in his income bracket, all through a single entity election and strategic structuring.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

What If You Already Filed as a C Corp for 2025?

If you already filed your 2025 return as a C Corp, you are not stuck forever. Here is the damage-control process to convert for 2026 and beyond.

Step 1: Verify Eligibility

Confirm your business meets all five IRC Section 1361(b) requirements: no more than 100 shareholders, only individuals or qualifying trusts as shareholders, one class of stock, a domestic corporation, and no ineligible corporation types (banks, insurance companies, certain international sales corporations).

Step 2: Evaluate Built-In Gains Exposure

If your C Corp holds appreciated assets, you may owe Built-In Gains (BIG) tax under IRC Section 1374 for a five-year recognition period after conversion. Calculate the net unrealized built-in gain as of the conversion date and plan asset sales accordingly.

Step 3: Calculate and Eliminate AE&P

Accumulated Earnings and Profits from your C Corp years follow you into S Corp status. Under IRC Section 1368(c), distributions exceeding your Accumulated Adjustments Account (AAA) get treated as dividends to the extent of AE&P. Clean this up through strategic distributions or a bypass election under IRC Section 1368(e)(3).

Step 4: File Form 2553 by March 15, 2027

To elect S Corp status for the 2027 tax year, file Form 2553 by March 15, 2027. If you missed the 2026 deadline, you can request late election relief under Revenue Procedure 2013-30 if you can demonstrate reasonable cause.

Step 5: Notify California FTB Separately

California requires a separate notification using FTB Form 3560. This is a step many owners and even some preparers forget, resulting in the FTB continuing to treat the entity as a C Corp and assessing 8.84% franchise tax instead of 1.5%.

Step 6: Set Up Payroll and Reasonable Salary

S Corp owner-employees must pay themselves a reasonable salary through payroll. The IRS uses Watson v. Commissioner standards to evaluate reasonableness. Set your salary based on comparable positions in your industry, not on what minimizes your tax bill.

Step 7: Activate AB 150 PTE Election

File the PTE election by the original return due date. This converts your California state tax into a federal business deduction, bypassing the SALT cap. Do not wait until extension filing to make this election.

Step 8: Establish Dual Depreciation Schedules

Because California does not conform to federal bonus depreciation, you must track two separate depreciation schedules from day one. Failing to do this creates compounding errors that grow more expensive every year.

Will This Trigger an Audit?

Converting from C Corp to S Corp does not, by itself, trigger an IRS audit. However, the IRS Palantir SNAP AI system cross-references entity classification changes with income reporting patterns. Specific audit triggers include:

- Setting an unreasonably low salary (below industry norms for your role)

- Distributing more than your AAA balance without proper AE&P accounting

- Claiming bonus depreciation on your California return (which California does not allow)

- Filing Form 2553 late without proper reasonable cause documentation

- Failing to file Form 7203 (S Corporation Shareholder Stock and Debt Basis Limitations) when required

The conversion itself is a standard IRS election. What triggers audits is sloppy execution, not the election itself.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Did Trump Lower the C Corp Tax Rate?

The Tax Cuts and Jobs Act of 2017 lowered the C Corp rate from 35% to 21%. The OBBBA in 2025 kept it at 21% permanently. But the 21% rate only applies at the corporate level. Once you take distributions, you pay dividend tax of 15% to 23.8%, plus California’s 8.84% franchise tax. The effective combined rate for a C Corp owner who takes distributions often exceeds 47%.

Is the QBI Deduction Permanent Now?

Yes. OBBBA made the 20% QBI deduction under IRC Section 199A permanent for S Corps, partnerships, and sole proprietorships. C Corps remain permanently excluded. This is one of the most significant entity selection factors for California business owners earning $60,000 or more in profit.

Does California Conform to the OBBBA Changes?

Partially. California adopted the increased SALT cap passively through federal conformity on personal returns, but it does not conform to bonus depreciation under R&TC Sections 17250 and 24356, caps Section 179 at $25,000 (versus $2.5 million federal), and does not conform to the QSBS exclusion under Section 1202. California continues to tax all capital gains at up to 13.3% with no preferential rate.

Can I Switch From C Corp to S Corp Mid-Year?

Yes, but only if you file the revocation consent and Form 2553 by March 15 for a January 1 effective date. If you file after March 15, the election is effective for the following tax year. Mid-year conversions with a prospective effective date require split-year filing under IRC Section 1362(e), which adds complexity and cost. January 1 conversions are cleaner and less expensive to execute.

What Happens If I Convert and Then Want to Go Back to C Corp?

Revoking your S election triggers a five-year lockout under IRC Section 1362(g). During that period, you cannot re-elect S Corp status without filing a Private Letter Ruling (PLR) at a cost of approximately $15,300. Think of this as a one-way door for at least five years. Make the decision with full financial projections before filing.

What Is the Best Entity for a California Business Making $150,000?

At $150,000 in profit, an S Corp typically saves $18,000 to $24,000 per year compared to a C Corp when all five tax layers are accounted for. The S Corp advantage at this income level is driven primarily by self-employment tax elimination on distributions, the QBI deduction, and the franchise tax differential. The only exception would be if you are actively raising venture capital or planning a QSBS exit within five years.

This information is current as of April 20, 2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Book Your C Corp vs S Corp Strategy Session

If you are still operating as a C Corp because someone told you the 21% rate was a good deal, you are likely overpaying by $20,000 to $60,000 every year. The OBBBA made S Corp advantages permanent, but only if you actually elect S Corp status and set it up correctly. Let our strategy team run a five-layer tax comparison for your specific situation, show you exactly how much you are losing, and build a conversion plan that captures every available deduction. Click here to book your consultation now.