Meta description: Confused about the difference between a C and S corp? This guide breaks down tax, salary, and exit implications in plain English so you can pick the right structure and stop overpaying the IRS.

Why Your Entity Choice Is Quietly Controlling Your Tax Bill

Many profitable owners obsess over revenue and ignore the one decision that quietly controls how much of that revenue they actually keep: whether they are taxed as a C corporation or an S corporation.

Pick wrong, and a business with $400,000 of profit can easily leak $20,000 to $60,000 a year in avoidable federal and state tax. Pick right, and that same profit can fund retirement, buy you audit protection, and make a future sale far cleaner.

Quick Answer: The Real Difference Between a C and S Corp

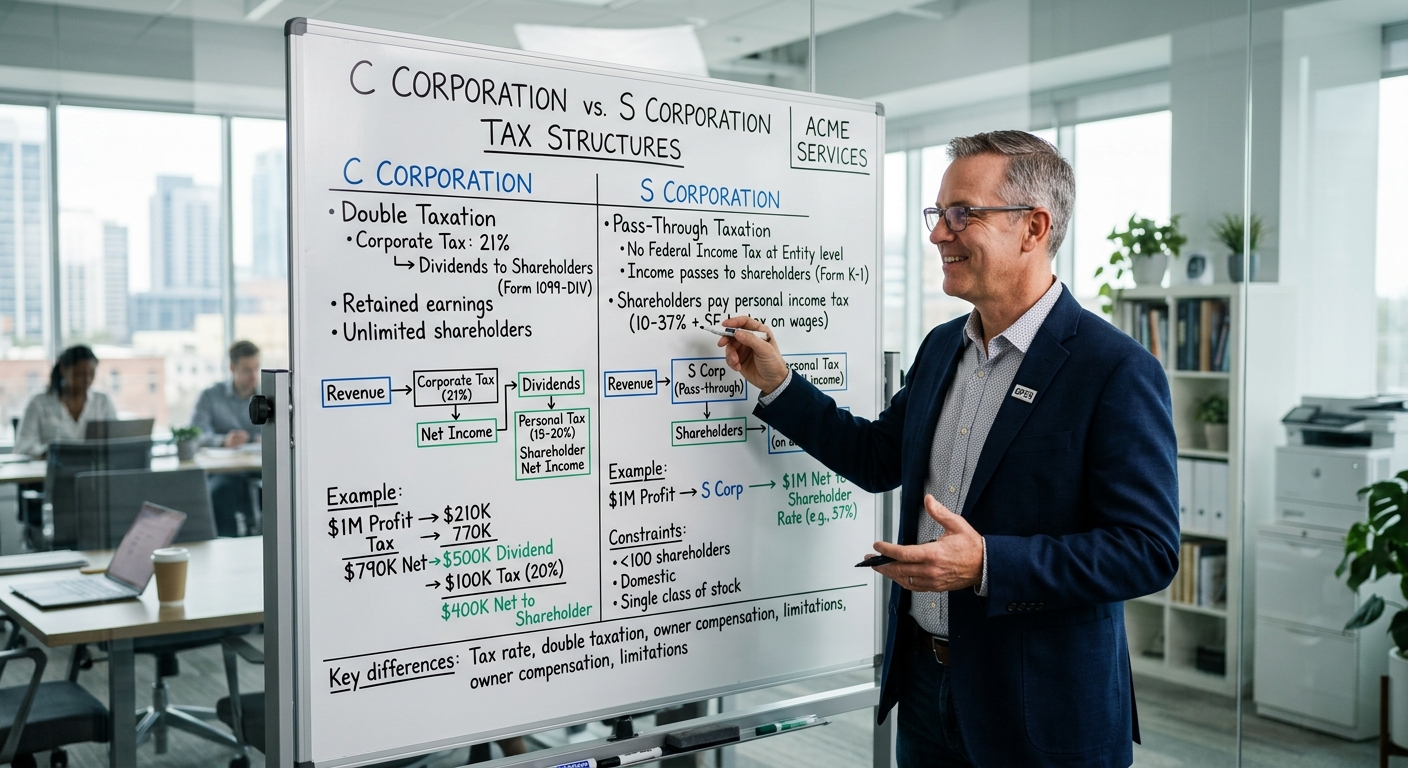

The core difference between a C and S corp is how profits get taxed.

- C corporation: The company pays its own tax on profit, then you pay tax again on any dividends or certain redemptions. This is the classic “double tax” structure.

- S corporation: The company generally does not pay federal income tax. Profit flows through to the shareholders’ personal returns, and only your W-2 salary is hit with payroll taxes.

That sounds simple, but for real owners with real money on the line, the decision is not just about “double tax vs pass through.” It is about reasonable salary, self employment tax, California minimum taxes, and the story you want to tell when you eventually exit.

How C Corp Taxation Actually Works in Practice

At the federal level, a C corporation pays a flat 21 percent corporate income tax on its taxable income. If your company earns $500,000 in taxable profit, the federal bill is about $105,000 before state tax. States then layer their own corporate rates on top.

When you distribute that after tax cash as dividends, you pay tax again at your personal level, usually somewhere between 15 percent and 23.8 percent on qualified dividends, plus any state tax. That is where the phrase “double taxation” comes from.

Example: High Profit, No Planning

Imagine a marketing agency generating $600,000 of pre tax profit as a C corporation in California.

- Federal corporate tax at 21 percent: about $126,000

- California corporate tax (8.84 percent): about $53,040

- Combined entity level tax: roughly $179,040

- After tax profit left in the company: about $420,960

If the owner wants to pull out $300,000 of that as dividends to spend, there is another personal level tax hit. At a 20 percent dividend rate plus 3.8 percent net investment income tax, that is roughly $71,400 in additional federal tax, plus state tax.

The effective total tax on that $300,000 can easily push past 40 percent once you stack both levels and California on top. That is the math most owners are trying to escape from when they ask if they should elect S corp status instead.

How S Corp Taxation Changes the Picture

An S corporation is a pass through entity. It files its own return (Form 1120 S), but generally does not pay federal income tax. Instead, it issues a Schedule K 1 to each shareholder, and the profit is reported directly on their personal Form 1040.

This is where the “reasonable salary” concept matters. The IRS expects owner employees of S corporations to pay themselves a fair W-2 wage for the work they do. That wage is subject to Social Security and Medicare taxes just like any other paycheck. Profit beyond that salary, though, typically is not subject to self employment tax.

Example: Same Business, S Corp Election

Take the same California agency now structured as an S corporation. It produces $600,000 of net profit before paying the owner.

- The owner sets a W-2 salary of $180,000 based on market comps.

- After wages, there is $420,000 of S corp profit.

- The W-2 salary is hit with full payroll taxes, but the $420,000 pass through profit is not subject to self employment tax.

Compared to being a sole proprietor, that shift alone can reduce Social Security and Medicare taxes by tens of thousands per year. For detailed California focused math on this, see KDA’s comprehensive S corp tax guide.

At the same time, because the S corp is a pass through, that $420,000 of profit lands on the owner’s personal return where it may qualify for the qualified business income (QBI) deduction, subject to the usual limitations in IRS Publication 535.

Comparing Tax Outcomes: C Corp vs S Corp on the Same Profit

To see the difference clearly, it helps to put the numbers side by side. Assume the following for a single owner business in 2026:

- Business profit before owner compensation: $400,000

- Owner could reasonably be paid $150,000 in W-2 wages

- Owner lives in California

Scenario 1: C Corporation

- Company pays corporate tax on $400,000 at 21 percent federal: $84,000

- California corporate tax (8.84 percent): about $35,360

- After tax corporate profit: about $280,640

- If the owner pulls out $200,000 as dividends, assume 23.8 percent federal plus 9.3 percent California: about $66,200 in tax

Total taxes related to that year’s profit quickly climb above $185,000 when you stack corporate and personal layers together.

Scenario 2: S Corporation

- Owner takes $150,000 W-2 salary, taxed for income and payroll taxes

- Remaining S corp profit: $250,000

- No corporate income tax at the federal level; profit passes through to owner

- Payroll tax on $150,000 runs roughly $22,950 for employer and employee Social Security and Medicare combined (before wage base caps and planning)

The $250,000 of S corp profit is not hit with self employment tax the way sole proprietor income would be. For a high earner, that can easily represent $10,000 to $20,000 of savings just on the payroll tax side compared to other structures, before layering in QBI, retirement contributions, and California nuances.

If you want to see how these scenarios hit your own bracket, run your estimated income through KDA’s online tax bracket calculator and then model the impact of shifting some profit out of wages and into S corp distributions.

Where C Corps Still Win

With all of that said, a C corporation is not “wrong” by default. There are situations where C status creates advantages that S status simply cannot replicate.

Retained Earnings and Reinvestment

If your business tends to keep profits inside the company to reinvest in equipment, R&D, or hiring, the flat 21 percent rate can be attractive, especially if your personal marginal rate is much higher. A $1,000,000 profit taxed at 21 percent leaves $790,000 to plow back into the company without ever hitting your personal return that year.

For some founders chasing institutional investment or planning an eventual stock sale, that simplicity and separation is worth the double tax risk on dividends that may never be paid.

Stock Based Compensation and VC Expectations

Technology startups and venture backed companies are usually C corporations because investors expect a share based cap table and the ability to issue stock options in a way that lines up with securities law and common exit structures.

If you are running a high growth startup aiming for a large exit, the S corp vs C corp conversation is less about current year tax and more about what type of entity professional investors are willing to fund.

How Your Work Style Changes the Calculation

The right choice between C and S status is not just about today’s tax rate. It is about how you actually work in the business.

Owner Operator With Hands On Role

If you are in the business every day, generating revenue, managing clients, and making key decisions, an S corporation often lines up well because it lets you split your income between reasonable salary and pass through profit.

That is the pattern that pairs most naturally with the “profit heavy, lean team” model we explore in KDA’s AI focused articles. When software and small teams drive large profit, the S corp structure gives you tools to manage payroll taxes, retirement contributions, and distributions in a coordinated way.

Passive or Semi Passive Owner

If you are more of a capital provider and less of a day to day operator, the mechanics change. In some cases, you may not be allowed to use S corp status at all if your entity mix or shareholder base does not qualify. Even when you do qualify, you have to think carefully about how “reasonable compensation” applies when you are not the one doing most of the work.

Common Mistakes When Choosing Between C and S Corp

Most of the expensive errors we see around entity choice fall into just a few buckets.

Red Flag Alert: Deciding Based on One Year of Profit

Owners often choose a structure based on last year’s income without considering where profit is actually headed. That is especially dangerous for businesses leaning into AI and automation, where margins can expand quickly as headcount stays flat.

If your profit can realistically double over the next two years because software is replacing payroll, an S corp might save far more in self employment tax than it appears to at today’s numbers. This is exactly the pivot we modeled in our earlier article on AI driven payroll reduction, where the shift from five full time employees to a lean, AI supported team changed everything about the owner’s ideal salary and distribution mix.

Ignoring California’s Entity Level Costs

California layers on its own annual minimum taxes and franchise fees. An S corporation in California pays a 1.5 percent tax on net income with an $800 minimum, while LLCs pay a flat fee based on gross receipts.

For California owners, a decision between C and S status is rarely pure theory. It needs to be grounded in the real FTB rules that show up in your mailbox every year. If your operation is California based or has significant California sales, this is not something to guess at.

How the C vs S Decision Fits Into the Bigger Picture

Entity choice is not a stand alone question. It sits inside a bigger story about how you build profit, how you pay yourself, and how you eventually exit.

For example, if you are building a lean, AI supported service firm and your profit margin is climbing, the S corporation becomes a powerful tool to control self employment tax while still letting you show strong, clean earnings on your personal return. That is the same profit dynamic we unpack in KDA’s article on the rise of profit heavy businesses in an AI world, where fewer employees and more software create a very different tax profile than the traditional “big team, low margin” agency.

On the other hand, if you are pursuing outside investment or planning a stock based exit, a C corporation can position you for that future, even if it means living with some double tax exposure along the way. In that case, the tax planning conversation shifts toward salary, bonuses, and timing of dividends rather than entity election alone.

What If You Picked Wrong?

Owners often discover years later that their entity choice no longer fits how the business actually operates. The good news is that in many cases you can change trajectory, but it needs to be done deliberately.

Electing S Status After Operating as a C Corp

You can usually elect S corp status for an existing C corporation by filing Form 2553 and meeting the eligibility requirements. However, there may be built in gains tax and other transition issues if the company holds appreciated assets.

This is where a forward looking analysis matters. We want to understand not only today’s tax hit, but the next five years of expected profit, salary, and distributions before making the switch.

Moving From LLC to S Corp Taxation

An LLC can often elect to be taxed as an S corporation without changing its legal shell at the state level. That can be a powerful move for 1099 consultants, small agencies, and real estate heavy operators who are starting to see consistent profit above the $80,000 to $100,000 range.

For self employed professionals, our self employed client work often starts with this exact question: at what point does S status make more sense than staying a default sole proprietor or partnership for tax purposes.

Step by Step: How to Evaluate C vs S for Your Business

If you want a disciplined way to approach this instead of guessing, use this framework.

Step 1: Map Your Real Profit Trajectory

Look at profit, not just revenue. If you expect a jump over the next two years because you are adopting AI tools or trimming payroll, build that into the model. A business at $200,000 profit today and $400,000 profit in two years needs a different structure than one that will stay flat.

Step 2: Define a Reasonable Salary Range

Work with compensation surveys, recruiter data, and your own role description to establish what the market would pay someone to do your job. That range becomes the anchor for S corp salary planning and for any future IRS conversation about “reasonable comp.”

Step 3: Run Side by Side Projections

Build at least three scenarios: current structure, S corp, and C corp. For each, calculate:

- Owner level income tax

- Payroll or self employment taxes

- Entity level taxes (federal and state)

- Cash actually available to you after all taxes

This is where a firm like KDA uses real world examples and tools to model year by year outcomes, not just a single snapshot. Owners often discover that the best choice over a five year window is not the one that looks best on this year’s return alone.

Step 4: Align With Your Exit Story

If you plan to sell the business, bring that into the decision now. Some buyers prefer stock deals, others prefer asset deals, and the entity you choose will shape what is possible and how much tax you pay when that day comes.

Getting these projections wrong can easily cost a profitable owner six figures over a relatively short window. That is why we treat entity selection as part of a broader advisory engagement, not a one off form filing.

KDA Case Study: Switching an LLC to S Status for a Lean, AI Supported Agency

A recent KDA client ran a boutique marketing agency in California. The company had started as a simple single member LLC, taxed as a sole proprietorship, with the owner reporting everything on Schedule C.

By 2025, the business was generating about $480,000 in net profit before the owner paid themself. The owner had embraced AI tools and a small contractor bench instead of a large payroll, so margins were significantly higher than in the early years.

- Under the default Schedule C setup, the entire $480,000 was exposed to self employment tax.

- Total annual self employment tax alone was running near $54,000, on top of income tax and California’s burden.

We restructured the tax treatment by electing S corp status for the LLC. Based on the owner’s role and industry data, we set a W-2 salary at $190,000, with the remaining $290,000 flowing through as S corp profit.

- Payroll taxes applied to the $190,000 salary, but the $290,000 pass through profit was not subject to self employment tax.

- First year payroll tax savings compared to staying a Schedule C filer were just over $18,000.

- We also layered in a Solo 401(k) strategy that allowed the owner to defer $69,000 between employee and employer contributions, reducing current year income tax by another ~$18,000 at their combined federal and state marginal rate.

All in, the restructure produced around $36,000 of annual tax benefit in year one, with even larger savings projected as AI driven profit growth continued. Our advisory fee for the modeling, election, and implementation was under $8,000, so the client saw a clear first year ROI of more than 4 to 1.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Where Professional Guidance Makes the Biggest Difference

Deciding between C and S status is not a quick quiz you take online. It is a modeling exercise that touches your salary, your retirement plan design, your state exposure, and your exit path.

For hands on business owners, especially those in California, our work with business owners and our dedicated tax planning services are built around this kind of decision. We look at your real numbers, your actual team, and your realistic growth plans instead of forcing you into a template.

This information is current as of 6/4/2026. Tax laws change frequently. Verify updates with the IRS or FTB if you are reading this later.

Bottom Line

The label on your entity is less important than how that structure interacts with your profit, your role, your state, and your exit goals. For many owner operators in the $150,000 to $750,000 profit range, S corp status paired with a disciplined reasonable salary plan produces a cleaner, lower tax outcome than staying a default LLC or becoming a C corporation, especially as AI tools push margins higher.

If your business is moving into that profit band, the cost of guessing is simply too high. A few hours of serious modeling can reveal five figures of annual savings and save you from a painful surprise when you eventually sell.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Book Your Tax Strategy Session

If you are unsure whether your current structure should stay a C corporation, convert to S status, or move an LLC into an S framework, this is exactly the kind of decision we help owners make with confidence. Book a personalized consultation with our strategy team and get a clear, numbers driven comparison tailored to your situation. Click here to book your consultation now.