Many business owners get stuck on one painful question every year: is my corporation structure quietly draining cash in taxes I do not need to pay? The way federal law treats C corporations and S corporations can turn into a five figure swing once your profit climbs past roughly $80,000. If you do not understand the tradeoffs, you are guessing with your single biggest expense: taxes.

Quick Answer

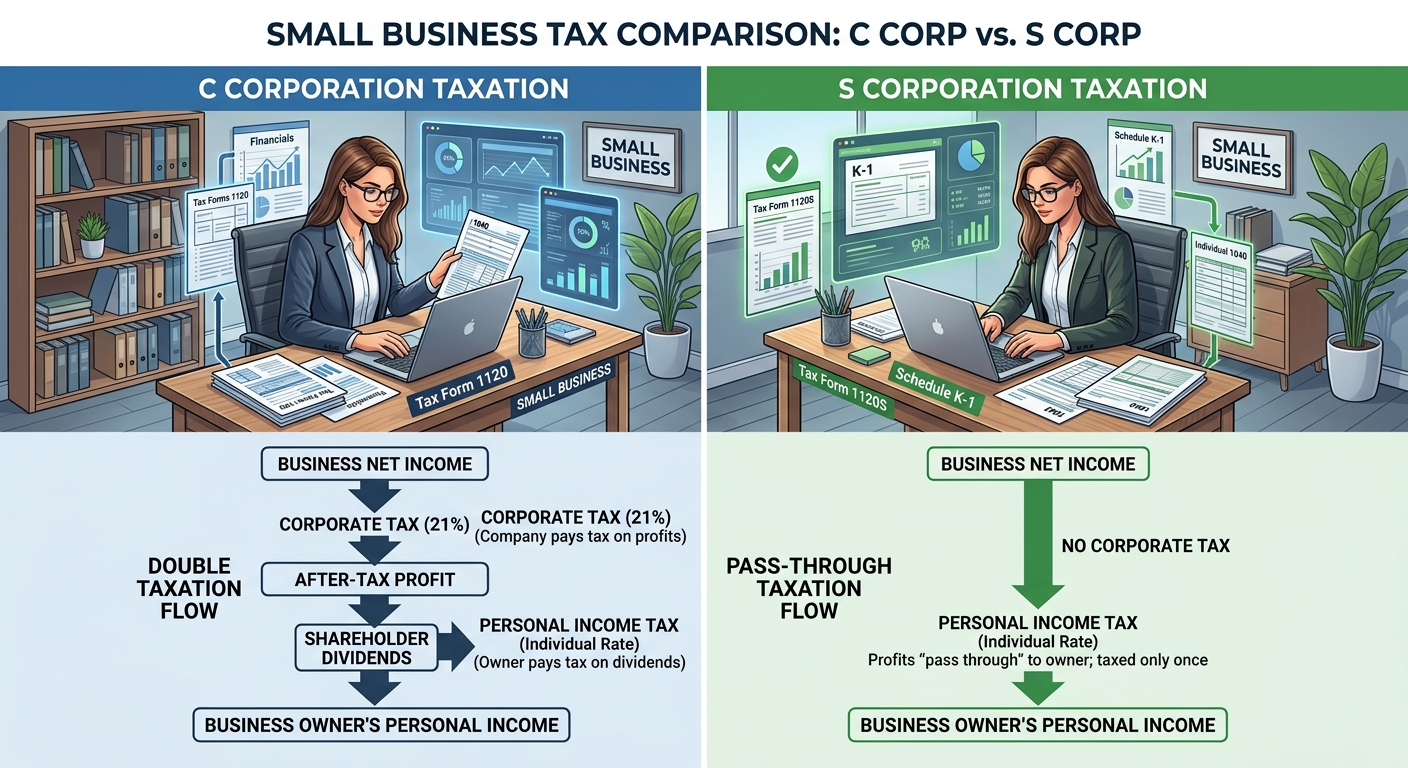

The core difference between taxes c corp vs s corp is how profits are taxed. A C corporation pays a flat federal tax at the entity level, then owners pay tax again on dividends or salary. An S corporation is a pass through: it generally pays no federal income tax itself, and profits flow to shareholders personal returns, often unlocking payroll tax savings and the Section 199A qualified business income deduction. Above certain profit levels, S status often beats C status for closely held businesses, but not always.

How Federal Taxes Treat C Corporations

A C corporation is its own taxpayer. It files Form 1120 and pays federal corporate income tax on its profits. Shareholder owners then pay tax on any wages they receive and on dividends. This is the classic double taxation structure. For 2026, the federal corporate rate is a flat percentage on taxable income. If a C corporation earns $300,000 before owner pay, that full $300,000 shows up on the corporate return after adjustments.

Imagine a marketing agency owned by one person that operates as a C corporation. The company earns $300,000 net before paying the owner. The owner takes a $140,000 W 2 salary and leaves $160,000 inside the corporation. The corporation pays federal tax on the $160,000, then if it distributes that amount as a dividend later, the owner pays individual income tax on the dividend. Your combined effective rate often ends up well over what an S corporation owner would pay on comparable profit.

C corporations can deduct a wide range of business expenses under rules outlined in IRS Publication 535, but they do not qualify for the 20 percent qualified business income deduction that many pass through owners can use on personal returns. That alone can cost a six figure owner tens of thousands per decade.

How S Corporations Change the Tax Equation

An S corporation is a tax status you elect on top of an underlying entity, usually an LLC or corporation. The S corporation files Form 1120 S and issues K 1s to shareholders. The entity itself usually pays no federal income tax. Instead, all remaining profit after salaries and other expenses flows through to the owners personal returns.

Here is the critical twist when you compare taxes c corp vs s corp. In an S corporation, you must pay shareholder employees a reasonable salary subject to payroll taxes. However, profit above that salary generally is not subject to self employment tax or Social Security and Medicare withholding. For an owner netting $200,000, setting a salary at $110,000 and leaving $90,000 as pass through profit can easily save $10,000 to $15,000 each year in payroll taxes alone, depending on your other income and state.

Most active S corporation owners also can claim the Section 199A qualified business income deduction on the pass through portion of their profit, subject to limits and phaseouts. That deduction can be up to 20 percent of qualified business income. For example, $90,000 of K 1 profit might generate an additional $18,000 deduction on your Form 1040, trimming several thousand dollars from your federal bill. Detailed rules live in the Section 199A regulations and related IRS guidance, but the headline is simple: S corporation profit is often more tax efficient for closely held service businesses than C corporation profit.

Comparing Total Taxes C Corp vs S Corp for a Six Figure Owner

Let us put real numbers on taxes c corp vs s corp for an owner operator business. Assume a consulting firm with $260,000 net profit before owner pay, no other employees, and the owner lives in a high tax state. We will compare a C corporation paying the owner only via salary and dividends vs an S corporation paying a mix of salary and pass through profit.

Scenario 1: C corporation. The company pays the owner a $160,000 salary. After payroll taxes and deductions, assume $90,000 remains as taxable corporate income. The C corporation pays federal corporate tax on $90,000. The owner also pays individual tax on the $160,000 salary plus any dividends taken out of remaining after tax corporate cash. By the time that $90,000 has been taxed at the corporate level and again as qualified dividends, the combined hit can easily reach $25,000 or more, depending on brackets.

Scenario 2: S corporation. The same business instead elects S status. The owner takes a $140,000 W 2 salary that meets reasonable compensation standards for their industry and region. After payroll tax, about $100,000 remains as S corporation profit. That $100,000 flows to the owner via Schedule K 1, not subject to Social Security and Medicare. The owner still pays federal and state income taxes on the $100,000, but they avoid roughly 3.8 percent in combined payroll tax on that slice, which is about $3,800 saved. Add a potential $20,000 Section 199A deduction, and federal savings can push $6,000 to $10,000 per year compared to operating as a straight C corporation.

The conclusion for most single owner and small closely held businesses under a certain size is that S corporation status is more efficient at converting profit into spendable after tax cash. Outside investors, stock option plans, and long term growth goals can tilt the equation back toward a C corporation, but you should quantify both tracks before defaulting to one.

KDA Case Study: Consultant Restructures From C Corp to S Corp

A few years ago, KDA worked with a solo marketing consultant based in California who had incorporated as a C corporation on the advice of a previous advisor. She was earning around $280,000 in net profit before owner pay. Her prior CPA had her taking a $150,000 W 2 salary and leaving the rest in the corporation. Each year, the company paid corporate tax on the remaining $100,000 to $120,000 and occasionally issued dividends on top, which were then taxed again on her personal return.

We modeled her situation as an S corporation. Under industry data and reasonable compensation guidelines, we set a $135,000 salary. That left about $120,000 to flow through as K 1 profit. Shifting that $120,000 from fully payroll taxed wages to a mix of wages and pass through profit cut her combined Social Security and Medicare cost by roughly $5,000 in the first year. She also qualified for an additional Section 199A deduction of about $22,000, worth nearly $5,000 in federal tax savings. After accounting for slightly higher payroll compliance costs and our advisory fee, her net first year savings were just over $8,500, and ongoing annual savings are tracking between $7,000 and $9,000 depending on profit.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

When a C Corporation Still Makes Sense

Despite the clear advantages of S corporations for many small owners, there are real situations where C status is the better tool. Venture backed startups that plan to reinvest profits and may never distribute dividends often accept double taxation at exit in exchange for easier stock structures and multiple classes of shares. Businesses pursuing the qualified small business stock exclusion may also favor C status to access potential long term capital gain exclusions on sale under IRC Section 1202.

If your company expects to retain most earnings inside the corporation to fund growth or acquisitions, the flat corporate rate on reinvested profit can look attractive. For example, a manufacturing company that regularly plows $500,000 each year back into equipment may defer a large part of the second layer of tax for many years, only paying when it eventually sells or distributes excess cash. In that context, C status can provide long term planning flexibility.

C corporations also can offer more flexible fringe benefits for certain owner employees, particularly in areas like health plans. However, owners who own more than 2 percent of an S corporation can still access many fringe benefits with special reporting rules. The key is that benefit design alone rarely justifies accepting permanent double taxation on growing profit.

Red Flag Alert: Reasonable Compensation for S Corporation Owners

The IRS focuses heavily on whether S corporation shareholder employees pay themselves a reasonable salary before taking large distributions. If your pay is clearly below market for your role and industry, the Service can reclassify distributions as wages, assess back payroll taxes, and add penalties and interest. For guidance, see the factors outlined in various IRS rulings and practical commentary surrounding audit cases.

As a rule of thumb, if your S corporation nets $250,000 and you are the main driver of revenue, planning to pay yourself only $40,000 in W 2 wages is asking for trouble. A more defensible structure might be wages in the $120,000 to $160,000 range with the rest as K 1 profit. Document your reasoning with comparable salary data, job descriptions, hours worked, and profitability. This helps defend your position in the event of IRS questions.

For many owner operators, it makes sense to engage a specialist in tax planning services to build a reasonable compensation model that balances payroll tax savings with audit safety. The cost of doing this right is usually a fraction of the downside of getting audited for abusive low salaries.

What About LLCs Taxed as C or S Corporations

Many business owners operate as LLCs and assume that means they have no choice in how their income is taxed. In reality, an LLC can check a box to be taxed as a C corporation or elect S corporation status if it meets eligibility rules. The underlying legal entity remains an LLC, but the IRS treats it as a corporation for tax purposes, which opens the same comparison of taxes c corp vs s corp you saw above.

For a single member LLC, the default is to be disregarded for federal tax. That means income shows up directly on Schedule C and is subject to self employment tax. Once profit climbs above roughly $60,000 to $80,000 and is expected to stay there, running the numbers on an S election often reveals meaningful savings. On the flip side, if you are exploring outside investment or planning an eventual stock style exit, electing to be treated as a C corporation early may align better with investor expectations.

This choice can be especially powerful for business owners who started lean and are now crossing six figures in profit. The change in tax treatment does not alter your contracts or operating agreement, but it can reshape where and how much tax you pay. The IRS explains more about entity classification in its check the box regulations and related instructions.

Will Choosing the Wrong Entity Type Trigger an Audit

Choosing C or S status by itself does not trigger an IRS audit. The audit risk comes more from inconsistent positions, missing forms, and abusive patterns once you are in a structure. For example, S corporations that show tiny wages and huge distributions year after year stand out as potential exams. C corporations that report losses for many years but still distribute cash to owners can also attract scrutiny.

From a compliance perspective, you must file the right forms for your structure. C corporations file Form 1120, S corporations file Form 1120 S, and shareholders report K 1 items correctly on Schedule E. Getting the elections right, including Form 2553 for S status, and meeting timing rules is essential. According to IRS Publication 542 on corporations, late or invalid elections can push you into an entity type you did not intend, which may carry higher tax costs until corrected.

Red Flag Alert: Do not switch structures back and forth every year to chase minor rate differences. The IRS can view repeated elections as abusive. Entity choice is a strategic decision you usually hold for several years at a time. Build a three to five year projection before you change, looking at profit trends, hiring plans, and potential exits.

How State Taxes Complicate C vs S Decisions

So far we have focused on federal income taxes c corp vs s corp. State regimes add their own twists. Some states fully respect S corporation pass through treatment, others impose entity level taxes or franchise fees on S corporations, and a few do not recognize S status at all. California, for example, imposes a 1.5 percent tax on S corporation net income plus an $800 minimum franchise tax, while C corporations face an 8.84 percent corporate tax rate in many cases.

This means a California S corporation with $400,000 in net income might pay $6,000 in entity level tax plus the franchise minimum, while a comparable C corporation pays over $35,000 in state income tax before considering shareholder level tax. Those numbers swing your effective combined rate and can widen the federal advantages of S status. When modeling, you must stack federal and state numbers side by side for at least three years of projected profit.

If you own rental property or operate in multiple states, the calculation gets more complex. Some owners may hold operating companies as S corporations and invest via LLCs or partnerships beneath them. Others may use a holding C corporation structure when raising capital and spin out operating LLCs beneath. There is no one size fits all answer, but there are clearly wrong answers once you see the math.

Common Questions on C Corp vs S Corp Taxes

Is there a specific profit level where S status always wins

No single profit threshold guarantees that S corporation status is always better. However, once an owner operator business has consistent net profit above about $80,000 to $100,000 after expenses, the payroll tax savings and 199A deduction often push S status ahead of both a Schedule C sole proprietorship and a C corporation that distributes profit. For capital intensive or high growth companies that retain earnings, C status may still be competitive.

Can I switch from C to S later

Yes, many owners operate as C corporations early and later elect S status as profit patterns change. You generally file Form 2553 to elect S status, and timing rules determine whether the election applies to the current year or the next. Converting can trigger built in gains tax issues if your C corporation holds appreciated assets, so run this with a professional before filing. The IRS details these rules in the instructions to Form 2553 and related guidance.

Do S corporation owners still pay self employment tax

Shareholder employees of an S corporation do not pay self employment tax on their K 1 profit, but their W 2 wages are fully subject to Social Security and Medicare. That is why the reasonable salary decision is central to taxes c corp vs s corp planning. Set salary too high, and you give back much of the S benefit; set it too low, and you invite IRS reclassification and penalties.

Using Calculators to Ballpark Your Savings

Before you pay an advisor, you can ballpark whether a structure change might help by modeling different salary and profit mixes. Start with your current net profit, then test scenarios where 50 percent to 70 percent of that profit shows up as wages and the rest as pass through income. Calculate payroll taxes, federal income tax, and state tax in each scenario. Running these numbers through a dedicated small business tax calculator can highlight just how much entity choice moves your total bill.

These tools do not replace proper planning, but they do make it clear that entity elections are not just paperwork. They are tax strategy decisions with four and five figure consequences. Once you see the gap, it is easier to justify the cost of a tailored engagement.

Bottom Line: Align Your Entity With Your Strategy

Choosing between C and S status is not an abstract legal question; it is a concrete tax cash flow decision. For owner operated service businesses above roughly $100,000 in profit, the S corporation often wins on take home pay because it reduces payroll taxes and can leverage the 199A deduction. Capital hungry companies with multiple investors, complex equity plans, or qualified small business stock goals may still lean toward C corporations even if they temporarily pay more tax on distributed earnings.

This information is current as of 6/28/2026. Tax laws change frequently. Verify updates with the IRS or your state tax authority if you are reading this later. If you are seriously comparing taxes c corp vs s corp for your own business, make sure you are modeling both federal and state impacts, reasonable salary, and your exit plan before you file any elections.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Book Your Tax Strategy Session

If you suspect your current structure is costing you thousands each year, there is no reason to guess. Our team regularly helps owners restructure from C to S or optimize existing S corporations, often uncovering $5,000 to $20,000 in annual tax savings for six figure businesses. Click here to book your consultation now.

Key Takeaway: The IRS is not hiding entity elections; most owners simply have never seen the side by side math. When you run it, the right answer usually becomes obvious.