C Corp vs S Corp in Massachusetts: The Unspoken 2026 Tax Math That Changes Everything

Most business owners in Massachusetts are flying blind when it comes to entity selection—especially with sweeping 2026 tax law shifts looming. This isn’t just about avoiding double taxation or sidestepping paperwork. With state-level decoupling, new R&D pass-through credits, and shifting federal conformity, the stakes for both comparing c corp to s corp in ma have never been higher. Choosing wrong could quietly bleed your profits by $15,000–$50,000+ next year—yet nearly every generic article skips the real-world dollar math and misses the new red flags. Here, you get the truth.

When comparing c corp to s corp in ma, the IRS math—not labels—decides the winner. A C Corp pays a flat 21% federal tax under IRC §11, plus Massachusetts’ 8% corporate excise, before a single dollar reaches the owner. An S Corp bypasses entity-level federal tax entirely, but shifts the battle to payroll compliance, reasonable compensation, and state-specific excise rules. The wrong structure doesn’t just cost you taxes—it locks you into the wrong cash flow model for years.

Quick Bottom Line: When a C Corp or S Corp Wins in MA

For the 2026 tax year, Massachusetts C Corps face double taxation: a state and federal corporate rate on net profits, and a second layer of tax when dividends are distributed to shareholders. S Corps avoid this “tax-on-tax” by passing income directly to owners’ personal returns, but must follow stricter ownership and compensation rules. Recent state law changes mean that R&D and other key credits may apply to pass-through S Corps in 2026, reducing historic C Corp advantages. The real savings come down to your profit levels, projected distributions, and whether you qualify for those new pass-through breaks.

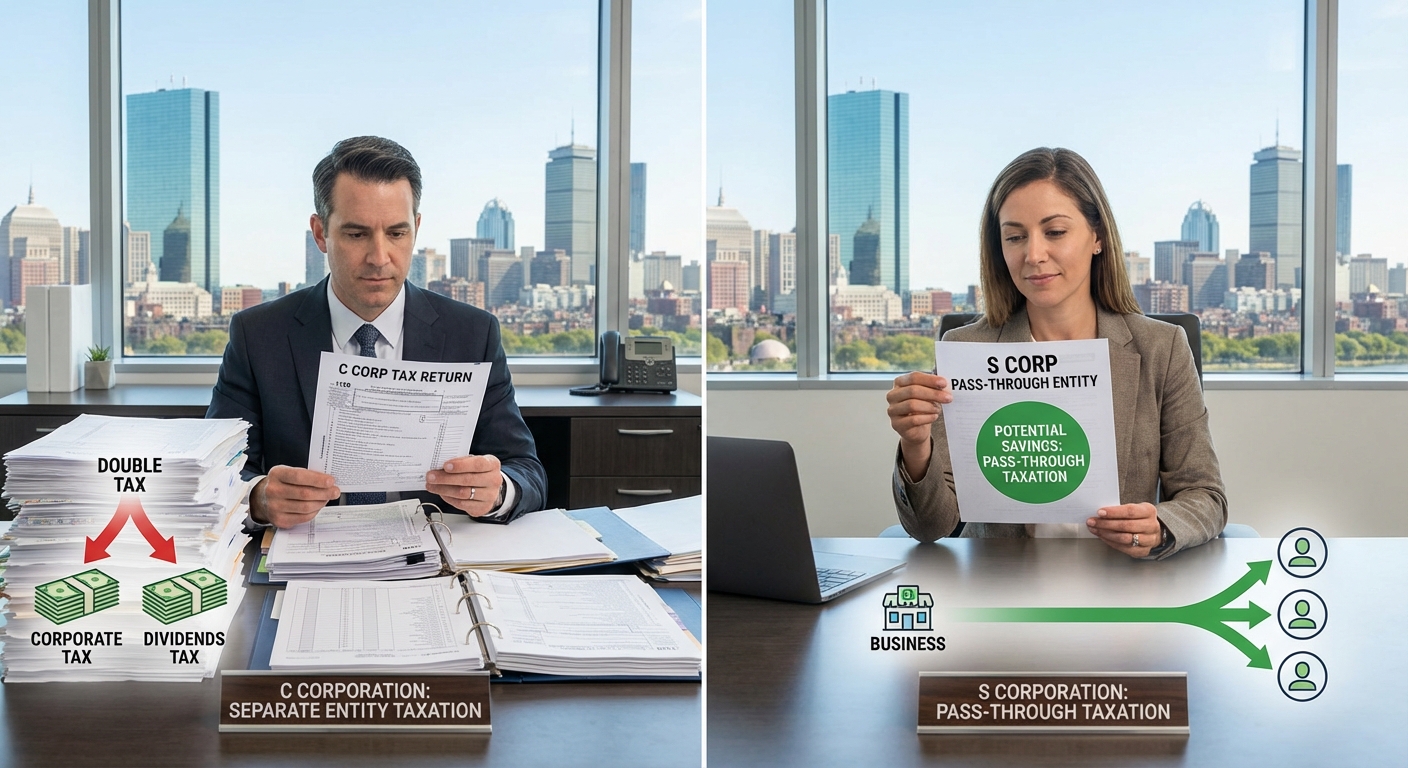

Understanding the Core C Corp vs S Corp Difference

The defining split between a Massachusetts C Corp and S Corp is taxation. A C Corporation (“regular” corporation) pays both federal and state income taxes on profits, then shareholders pay again on any distributed dividends. This is classic “double taxation.” In contrast, an S Corporation is a pass-through entity: profits (and most losses) show up on the owners’ personal returns—there’s no federal entity-level tax—so you only pay tax once at the personal level. As of 2026, Massachusetts recognizes S Corp status for state returns but applies a special S Corp rate, which can be higher than other pass-throughs. For high-profit businesses looking for R&D credits or corporate benefits, the scales are shifting.

If you’re a Massachusetts business owner or thinking of switching entity types, it’s essential to understand how these rules intersect with your industry. Many business owners face a surprise tax bite after missing one detail—like not running “reasonable salary” payrolls in S Corps or overlooking state filing requirements.

KDA Case Study: S Corp Restructure Saves a Boston LLC Owner $41,200

Consider Jordyn, a 1099 consultant in Boston grossing $250,000—previously operating as a single-member LLC. She’d heard S Corps were for “bigger companies,” but her CPA missed the latest pass-through benefit expansion. After switching to S Corp (with KDA’s guidance), Jordyn paid herself a $90,000 salary—incurring payroll tax—but distributed $100,000 as dividends, now shielded from an additional 15.3% self-employment tax. In 2026, she was also able to claim Massachusetts’s new pass-through R&D credit through her S Corp. Total first-year savings: $41,200 after fees, compared to just $27,600 as a standard LLC. She paid $4,500 for the setup and S Corp compliance, a 9x ROI in year one.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Why Most Massachusetts Owners Miss the Real Savings

Here’s the trap: Advisors focus on federal tax, but at the state level, Massachusetts modifies S Corps with a “built-in gains” tax and imposes a higher minimum excise tax than on basic LLCs or partnerships. In 2026, pass-throughs can also now claim certain credits previously reserved for C Corps—so the old penalty for going S Corp is lower than ever. Yet, if you don’t meet all “reasonable compensation” and ongoing compliance steps, savings can vanish in an audit. Simple math: If your business profit is under $50,000, the complexity of an S Corp usually isn’t worth it. But above $75,000—especially with R&D credits or advisor compensation—a proper S Corp setup typically saves $8,000–$18,000 in combined federal and MA taxes annually.

How Payroll, Owner Compensation, and Draws Work in 2026

The IRS requires S Corps to pay “reasonable” salaries to shareholder-employees—subject to payroll tax—before profits can be distributed as dividends. Fail this rule and you face audit risk and retroactive payroll taxes. In Massachusetts, S Corps must also pay a minimum excise ($456 in 2026) and file state S Corp returns. C Corps, conversely, can retain profits in the business, but distributions to owners will be taxed again as dividends (2026 Massachusetts rate: 5%, federal top capital gains: 20%). With C Corps, Massachusetts allows for “Section 1202” small business stock exclusions but only for qualified startups and growth businesses.

Strategic planning—especially payroll setup—is where the elite deductions are found. Get tax help tailored for bookkeeping and payroll to avoid costly errors.

What the IRS Won’t Tell You About 2026 Entity Choice

Myth: “C Corps are best for reinvestment; S Corps are best for distributions.” This was true pre-2026, but with expanded Massachusetts pass-through credits, the line is blurring. The IRS (see S Corporation guidance) now focuses more on compliance and reporting accuracy than entity type. If your business works with non-U.S. shareholders, has multiple classes of stock, or plans an IPO, C Corp remains the only viable option. For classic Main Street businesses, wealth transfer plans, or tightly held companies, S Corp is still king—especially at profits between $60,000–$500,000.

Red Flag Alert:

Failing to run proper S Corp payroll is the #1 cause of IRS and Massachusetts audits for pass-throughs. Always check your salary, withholdings, and documentation.

Pro Tip: Visualizing the True S Corp vs C Corp Math

| Scenario (2026) | S Corp | C Corp |

|---|---|---|

| Net Profit (pre-owner comp) | $200,000 | $200,000 |

| Owner Salary (reasonable comp) | -$90,000 (payroll taxed) | varies (can be $0-200K) |

| Corporate Tax (Fed+MA) | 0% entity-level | 21% federal + 8% MA = $58,000 |

| Owner Dividend | $78,000 (one layer tax) | $142,000 (post-corp-tax) |

| Dividend Tax (Fed+MA) | Personal rate (~24%) | Up to 23.8% fed + 5% MA |

| Effective Net to Owner | $127,680 | $114,344 |

Key Takeaway: For most profitable Massachusetts businesses, a correctly run S Corp setups puts $13,000+ more in your pocket annually at $200K profit, if coupled with payroll and state incentive compliance.

FAQ: Comparing S Corp and C Corp in MA

What if my business has out-of-state owners?

C Corps are better for complex ownership; S Corps limit you to 100 U.S. shareholders, one class of stock.

Can S Corps deduct health insurance?

Yes, owners owning 2% or more of the S Corp can deduct their health insurance (with documentation; see IRS Publication 535).

Do both C Corps and S Corps qualify for new R&D credits in MA?

In 2026, yes—state rules have expanded to allow some credits for S Corps that were previously C Corp-only. Confirm details with your tax strategist each year.

What about Massachusetts minimum tax?

Both entity types face $456 minimum excise for 2026, but S Corps must still run payroll and file pass-through returns to qualify.

How do capital gains work on sale of the business?

C Corps may face double tax on asset sale gains, while S Corps’ owners are taxed only once at the personal level, often with federal rates lower than C Corp distributions.

What If My Profits Aren’t High Enough for S Corp Benefits?

If your profit is under $55,000, the compliance cost of an S Corp may outweigh the tax benefit—especially if you’re not taking full advantage of new state credits. Use this small business tax calculator to see the true after-tax impact by plugging in your specific numbers for 2026 in Massachusetts.

How to Switch Entity Types (or Fix Past Mistakes) in MA for 2026

- Run the numbers first. Do a 3-year projection. If S Corp savings (even after setup cost) exceed C Corp by $7,000+ annually, move before March 15, 2026.

- File Form 2553. This is your IRS S Corp election (find it here), due no later than 2.5 months after start of your tax year, with a Massachusetts S Corp election aligned.

- Set up compliant payroll. Ensure “reasonable compensation,” especially for owner-operators. This avoids red flags at both IRS and state.

- Document R&D and other credits eligibility. S Corp owners, check new Massachusetts credit applications in 2026—you may need to pre-certify or meet thresholds.

- Review annually. Election and compliance rules can shift every year. Massachusetts updates rates and credit eligibility often, especially in post-federal change years.

Bottom Line: The Right Call for 2026

If you are actively comparing c corp to s corp in ma for 2026, don’t let generic guidance or last year’s advice tie your hands. Run scenario-based projections, weigh all credits (federal and MA), and prioritize long-term owner strategy—not just the current year’s tax bill. If you’re shifting profits, planning for sale, or adding owners, the right structure can easily generate six-figure savings (or costs) over five years. Review guidance annually and act well ahead of tax-filing deadlines.

For a deeper dive on entity strategy and to see advanced scenarios, visit our comprehensive S Corp tax guide.

This information is current as of 2/4/2026. Tax laws change frequently. Verify updates with the IRS or MA DOR if reading this later.

Book Your Massachusetts Entity Review Strategy Session

Still unsure which path will keep more profit in your business? Book a personalized Massachusetts tax and entity review with our strategy team and walk away with answers tailored to your numbers—no fluff, just the real savings moves. Click here to book your consultation now.