Many owners pick a corporation type once, never revisit the decision, and quietly bleed five or six figures of tax over a decade. The wrong structure can lock you into double taxation, higher California fees, and payroll headaches you did not need in the first place. This **c corp vs s corp crash course** is built to stop that.

Quick Answer

If you expect to keep most profits inside the company for years or pursue a future private equity or IPO style exit, a C corporation can make sense. If you are a closely held business where the owners want to pull out profits each year and avoid double taxation, an S corporation or an LLC taxed as an S corporation usually wins. The right answer depends on profit level, how much you take as salary, and your state, especially if you are in California.

How This Crash Course Keeps You Out of Trouble

This article is written for three groups of readers:

- Single owner or family owned businesses currently taxed as an LLC or sole proprietorship wondering whether to elect S status.

- Existing C corporations that suspect they are paying more tax than they should.

- High earning W 2 or 1099 professionals considering their first entity.

We will walk through the real tax math, not theory, using concrete examples with numbers. We will reference official IRS guidance, including IRS Publication 542 on corporations and IRS Publication 535 on business expenses, so you can verify the rules yourself. Then we will give you a simple decision framework so you can see which box you belong in today, not someday.

C Corp vs S Corp Crash Course: Tax Basics In Plain English

Start with structure and how profits are taxed. Ignoring this is why many owners overpay for years.

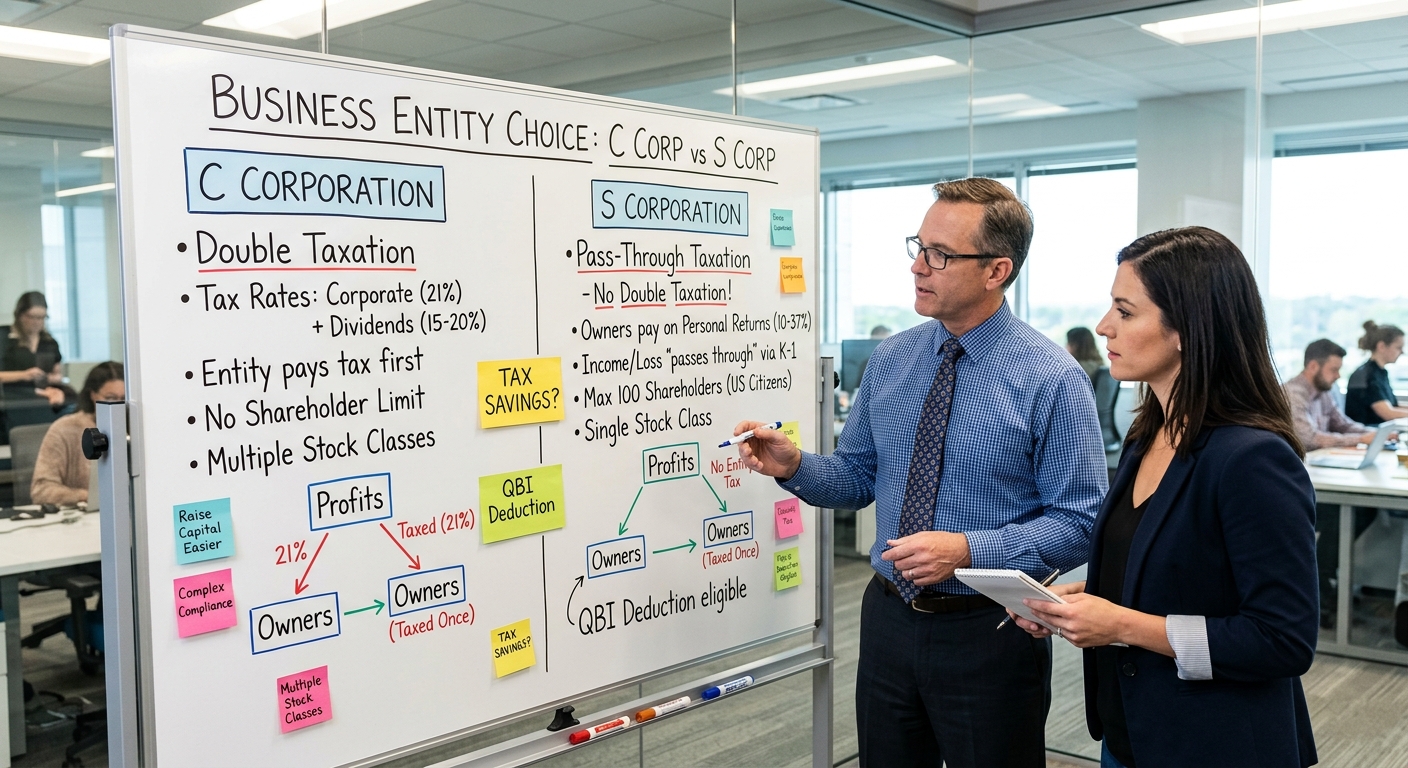

How C Corporations Are Taxed

A C corporation is a separate taxpayer. It files its own return, usually on Form 1120 at the federal level. Net income is taxed at the corporate rate, which under current law is a flat 21 percent for the 2025 tax year. If the corporation distributes after tax profits as dividends, the shareholders pay tax again at their own dividend rate. That is the classic double taxation problem described in Publication 542.

In California, a typical C corporation also files Form 100 and pays an income based tax plus a minimum franchise tax. High growth companies sometimes tolerate this because they plan to reinvest most earnings and later pursue a sale where special rules like the qualified small business stock exclusion under Internal Revenue Code Section 1202 may apply.

How S Corporations Are Taxed

An S corporation is a pass through entity. It generally does not pay federal income tax at the entity level. Instead, income, deductions, and credits flow to the shareholders, who report them on their personal returns using Schedule E. The election to be treated as an S corporation is made on Form 2553.

The big win is that there is usually no federal level double tax on dividends. Instead, owners who work in the business must take a reasonable salary that is subject to payroll taxes, and the rest of the profit can be distributed as shareholder profit that is not subject to self employment tax. The IRS discusses reasonable wages and employment tax obligations in Publication 15.

In California, S corporations pay a 1.5 percent franchise tax on net income with an $800 minimum tax, reported on Form 100S. That 1.5 percent is often a small price for the self employment tax savings that can easily reach five figures for profitable owners.

Side By Side Snapshot

| Feature | C Corporation | S Corporation |

|---|---|---|

| Federal tax at entity level | Yes, 21 percent on profits | Usually no, income passes through |

| Double taxation risk | High, on dividends | Low, profits taxed once to owners |

| Eligibility limits | No shareholder count limit | 100 shareholders max, only allowed types |

| Investor preference | Often preferred by venture capital | Better for closely held operators |

| California franchise tax | Income based plus minimum tax | 1.5 percent of net income, $800 minimum |

Most small and mid sized operating businesses that want to distribute profits regularly do not want double taxation on those distributions. That is why S corporations and LLCs taxed as S corporations dominate the owner operator landscape.

Real Tax Math: How Much You Keep In Each Structure

High level definitions are helpful, but numbers decide whether you move. Here are three practical scenarios that show the C versus S trade off.

Scenario 1: Solo Consultant In California

Maria is a 1099 consultant in Los Angeles. Her LLC shows $240,000 of net profit on Schedule C. As a sole proprietor, she pays income tax and full self employment tax on that amount. Her self employment tax alone is roughly $240,000 times 15.3 percent, or about $36,720, part of which she can deduct as an adjustment to income.

If Maria elects S corporation status and pays herself a reasonable salary of $120,000, the remaining $120,000 can be treated as S corporation profit. Payroll taxes apply only to the salary piece. At 15.3 percent on $120,000, that is about $18,360 of self employment type tax. The other $120,000 is not subject to self employment tax. That single move saves her roughly $18,360 in 2025, even after paying the 1.5 percent California S corporation tax of $1,800.

If you are like many business owners in California, that kind of annual savings is the difference between struggling with cash flow and being able to fund retirement or real estate investments. You can plug your own numbers into KDA’s small business tax calculator to see how the salary versus distribution mix changes your total tax bill.

Scenario 2: Profitable Agency That Reinvests Heavily

Now assume a marketing agency with $1,000,000 of net income and two equal owners. They plan to reinvest 90 percent of profits over the next five years to build a team and technology stack for a potential sale.

As an S corporation, essentially the full million flows to them personally each year. Even if they only distribute a small portion, they pay tax currently on the full income because pass through entities are taxed on allocated income, not cash distributions.

As a C corporation, the company would pay 21 percent corporate tax, or $210,000, and retain $790,000 to reinvest, with no second layer of tax until there is a dividend or sale. If they can qualify for the Section 1202 qualified small business stock exclusion and eventually sell their stock, a large portion of that gain may be federally tax free under the rules summarized in IRS guidance on qualified small business stock.

For owners who genuinely plan to build a scalable company with outside investors and a future exit, this is where C corporations can outperform despite double tax risk.

Scenario 3: Real Estate Focused Owner

Consider David, a high earning W 2 engineer in San Jose who has started a side real estate business that flips two or three properties a year. The profit is lumpy and he wants to channel most of it into long term rental properties.

Running the flip business through an S corporation can reduce self employment tax on business profits, while he holds rentals in separate LLCs taxed as partnerships or disregarded entities. Because S corporations do not work well for holding appreciating real estate, structuring multiple entities becomes important. For more depth on S corporation design for California owners, see KDA’s comprehensive S corp tax strategy guide for California.

In David’s case, S status on the active flip income helps reduce payroll taxes, while separate real estate entities maximize flexibility for depreciation and financing.

KDA Case Study: California Consultant Cuts Tax Bill With S Corp

A San Diego based marketing consultant came to KDA after three years of operating as a sole proprietor. She was a classic high income 1099 taxpayer with very little structure. Her Schedule C for the prior year showed $310,000 of net profit, and she was stunned by a combined federal and California tax bill over $110,000. None of her prior advisors had walked her through the S corporation option.

We started by modeling her income using her existing books and projecting a reasonable salary at $150,000 based on industry data and her role. We then showed her the impact of an S corporation election, including California’s 1.5 percent franchise tax and payroll costs. The math was clean. On the first year alone, shifting from a sole proprietorship to an S corporation was projected to reduce self employment type taxes by just over $24,000, even after paying the California S corporation tax and modest payroll service fees.

KDA handled the entire implementation, including forming a corporation, filing Form 2553, and setting up compliant payroll. We also reworked her bookkeeping and quarterly estimated tax payments so cash flow matched the new structure. Her first year post restructure, her actual tax savings were $23,700 compared to the prior year at similar income. She invested those savings into a down payment on a small rental property, starting the next phase of her wealth plan. Her advisory fee to KDA for the entity work and ongoing strategy was slightly under $6,000, yielding a first year return on investment of nearly 4 times.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Red Flag Alert: Common C Corp and S Corp Mistakes

Once owners understand the mechanics, they often rush into a change without realizing how easy it is to trigger IRS scrutiny or lose benefits.

Ignoring Reasonable Compensation Rules

The most common S corporation mistake is paying the owner an unreasonably low salary to minimize payroll taxes. The IRS has successfully challenged these setups in court when salaries were obviously below market for the work performed. Publication 15 and several revenue rulings give the IRS broad authority to reclassify distributions as wages.

If your S corporation pays you $30,000 in wages and distributes $200,000 in profit while you are doing full time work, you have a target on your back. A better approach is to document a defensible salary based on market data, duties, time spent, and business profitability, then take remaining profit as distributions.

Our entity formation and restructuring services include a compensation analysis so that owners stay in a safe zone for their industry and region, especially under California scrutiny.

Forgetting About State Level Taxes

Another trap is forgetting that states do not all follow federal rules. California imposes that 1.5 percent tax on S corporation net income and the $800 minimum franchise tax on most entities. Other states have their own quirks. When you operate in multiple states, pass through income can be taxed in each state where the business has nexus.

Before you elect S status or convert from C to S, multi state impact must be modeled. Many self employed professionals and online businesses touch more states than they realize through remote employees and contractors.

Missing or Late S Corp Elections

Finally, many taxpayers simply miss the S corporation election deadline. Form 2553 is generally due two months and fifteen days after the start of the tax year you want the election to be effective. The IRS does provide some late election relief in specific circumstances described in the instructions to Form 2553, but you never want your entire strategy hanging on relief the IRS is not required to grant.

Red Flag Alert: If your advisor cannot tell you the exact effective date of your S corporation election and show you a filed Form 2553, assume you are at risk of operating under the wrong tax status.

What The IRS Will Not Spell Out For You

The core rules for corporate taxation live in the Internal Revenue Code and IRS publications, but the IRS will not lay out a clear decision tree for small business owners. They simply explain each regime in isolation. That is why it is easy to miss strategies that appear only when you compare the systems head to head.

There is also no dedicated IRS publication titled C versus S for small business owners. Instead, the burden is on you to synthesize Publication 542, Publication 535, the S corporation sections of the code, payroll rules, and state guidance from agencies such as the California Franchise Tax Board.

This is why a short meeting with a strategist who lives in this material every day can unlock tens of thousands of dollars. You are not paying for forms. You are paying for synthesis and sequencing.

Simple Decision Framework: Should You Be C Or S Right Now

Here is a practical framework KDA uses as a starting point when advising owners. It is not a substitute for personalized advice, but it will tell you quickly where the conversation should go.

Probably S Corp If

- Your business profit before owner wages is at least $80,000 and usually in the $150,000 to $600,000 range.

- You and a small group of individuals own all of the stock, with no foreign shareholders and no plans to add institutional investors soon.

- You want to pull out a significant portion of profit each year for personal use or to invest in other assets.

- You are willing to run payroll and keep clean books.

Probably C Corp If

- You expect to raise money from venture capital, private equity, or institutional investors.

- You plan to reinvest the vast majority of profits for several years to chase scale.

- You may qualify for Section 1202 qualified small business stock and are aiming for a stock sale that could be largely exempt from federal tax.

- You are comfortable managing double taxation on dividends in exchange for investor access and potential exit benefits.

Borderline Cases That Demand Modeling

- High income service businesses where owners split time between W 2 jobs and the company.

- Multi entity real estate and operating business combinations.

- Situations where one owner wants cash flow and the other wants reinvestment.

Bottom Line: Any time your profit, growth plans, or ownership structure changes, your entity choice should be revisited. A structure that was optimal at $120,000 of profit can be suboptimal at $600,000.

Will An S Corp Or C Corp Election Trigger An Audit

Most owners are less afraid of paying some extra tax than they are of inviting an audit. That fear often keeps them in lousy structures.

Electing S status via Form 2553 does not inherently increase audit risk. The IRS processes thousands of these elections as a routine matter. What raises risk is sloppy implementation, such as zero or tiny wages, personal expenses run through the corporate books, or inconsistent reporting between the corporate return and shareholder returns.

On the C corporation side, risk rises when owners attempt to zero out income every year with aggressive deductions that are not well documented, which can draw scrutiny under the rules in Publication 535.

Pro Tip: Clean bookkeeping and a defensible salary are far more important to audit risk than whether you pick C or S. KDA’s bookkeeping and payroll services exist for this exact reason.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About C And S Corporations

What If I Already Have An LLC

If you already operate as an LLC, you do not have to form a brand new corporation to get S corporation style taxation. You can often file Form 2553 and have your LLC taxed as an S corporation while keeping the legal LLC wrapper. This preserves legal flexibility while changing the tax treatment.

Can I Switch From C To S Later

Yes, many companies start as C corporations and later elect S status, or vice versa. However, switching from C to S comes with built in gains tax considerations. Certain appreciated assets may be subject to a corporate level tax if sold within the recognition period. This is complex area and one where advance modeling is essential.

How Does The Qualified Business Income Deduction Fit In

The qualified business income deduction, created by the Tax Cuts and Jobs Act and explained in IRS guidance on the QBI deduction, generally allows eligible owners of pass through businesses, including S corporations, to deduct up to 20 percent of their qualified business income, subject to multiple limits. C corporation income does not qualify, which is one more reason many closely held owners favor S status.

Is This Federal Or California Advice

The core C versus S concepts described here apply at the federal level for the 2025 tax year. State treatment varies. This article focuses on California, where S corporations pay a 1.5 percent tax on net income and most entities pay an $800 minimum tax. If your business operates in other states, additional planning is required.

Key Takeaways You Can Act On This Month

- If your Schedule C or LLC profit before owner wages is over roughly $80,000, you are a strong candidate for an S corporation analysis.

- If you plan to raise institutional capital or chase a stock sale, a C corporation may still be the right foundation despite double tax risk.

- Reasonable compensation, clean books, and timely Form 2553 filings are non negotiable for any S corporation strategy.

- California owners must factor in state franchise taxes alongside federal savings.

This information is current as of 6/6/2026. Tax laws change frequently. Verify updates with the IRS or your state tax agency if you are reading this later.

Book Your Tax Strategy Session

If you are unsure whether your current C or S structure is costing you more than it saves, it is time to get precise. KDA will run the real math on your last year of returns, model C versus S treatment, and give you a clear recommendation backed by IRS rules, not guesswork. Click here to book your consultation now.

You will find this article and other deep dives on strategic tax topics on the KDA blog at kdainc.com, where we publish regularly for serious business owners.