Most owners think converting a profitable C corporation to an S corporation is a magic switch that stops double tax instantly. Then they sell an asset, get hit with a built in gains tax at the corporate level, and realize too late that the old C corp history followed them into their new S election.

This post walks through how the c corp to s corp conversion built in gains rules really work, why the three year recognition period is not a free pass, and how California business owners can plan ahead so they do not hand the IRS and FTB a surprise check for six figures.

Quick Answer

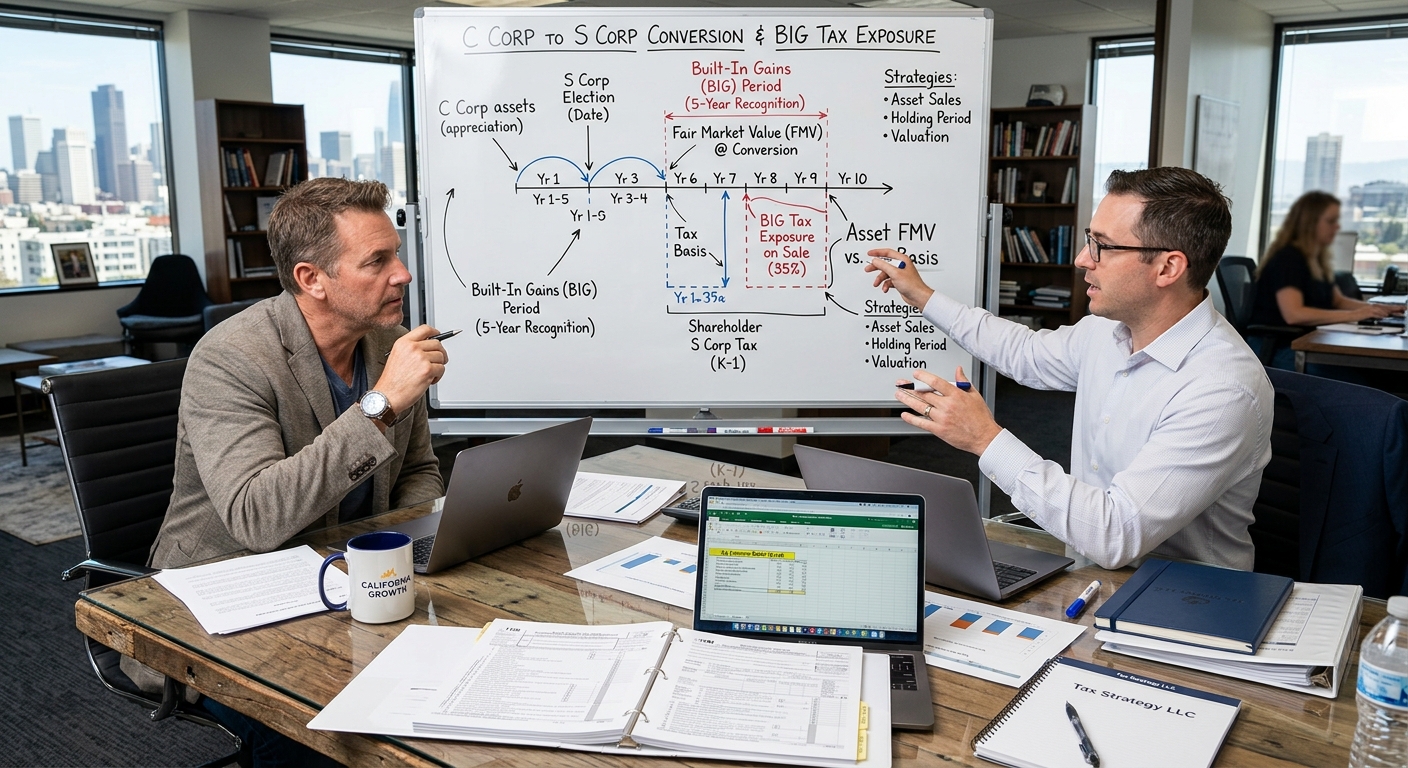

When a C corporation elects S corporation status, any built in gain that existed on its assets as of the conversion date is potentially subject to a corporate level tax if those assets are sold during a limited “recognition period.” Under current federal rules in Internal Revenue Code Section 1374, that period is generally five years, though recent legislation has at times shortened it to as little as three years. If you sell or dispose of appreciated assets during that window, the S corporation itself pays tax on the built in gain as if it were still a C corporation, and the shareholders can also be taxed on the same income at the individual level.

In plain English: the IRS lets you become an S corporation, but for a few years it reserves the right to collect C corporation tax on old appreciation that built up before the election.

How Built In Gains Work When You Convert a C Corp to an S Corp

To understand the c corp to s corp conversion built in gains problem, you need to define three things: what counts as a built in gain, which assets are subject to it, and how long the risk lasts.

What Is a Built In Gain?

A built in gain is the unrealized profit embedded in an asset on the day your C corporation becomes an S corporation. If your balance sheet shows a building with a tax basis of $500,000 and a fair market value of $1,200,000 on the effective date of your S election, there is a $700,000 built in gain sitting there waiting to be recognized.

The same concept applies to:

- Equipment that has been depreciated below its real value

- Customer lists, goodwill, and other intangibles created inside the C corporation

- Investments, marketable securities, or partnership interests held by the corporation

- Inventory whose fair market value exceeds its tax basis

Section 1374 of the Internal Revenue Code says that if the S corporation disposes of these assets during the recognition period, the corporation owes a special built in gains tax at the highest corporate rate on the gain that was “built in” at conversion.

What Is the Recognition Period Today?

Congress has tinkered with the recognition period repeatedly. It was originally ten years, was temporarily shortened during and after the financial crisis, and recent legislation has often settled on a five year window for most years. The reason you see references to a three year period is that temporary laws shortened it even further for certain tax years, but you cannot assume three years for planning without checking the specific tax year rules.

Practically, that means if your C corporation becomes an S corporation effective January 1, 2026, you should expect at least a five year window where selling appreciated assets can trigger the built in gains tax, unless Congress again enacts a shorter period and you clearly qualify. You can review the technical details in the IRS instructions for Form 1120 S and recent IRS guidance on Section 1374.

Why This Matters to Real Business Owners

Consider a California manufacturing company that has operated as a C corporation for 15 years. The company owns a facility with a $600,000 tax basis and a current value of $1,500,000. The owners convert to an S corporation on January 1, 2026, planning to sell the business in 2028.

If they sell the facility in 2028 for $1,600,000, there is a $1,000,000 gain. Up to $900,000 of that gain may be subject to the built in gains tax at the corporate level because it was built in on the conversion date. At a 21 percent federal corporate rate, that is $189,000 of tax inside the S corporation, plus individual level tax on the same income when it flows through. Add California’s 1.5 percent S corporation tax and the individual California tax, and you can easily cross $250,000 in combined tax on that one piece of the deal.

That is why c corp to s corp conversion built in gains planning is not optional for anyone with appreciated hard assets or goodwill on the books.

Strategic Planning Before You Elect S Status

If you are still a C corporation today, your cheapest strategy is often to plan before you file Form 2553 to elect S status. The goal is to reduce or manage built in gains exposure so you are not locked into a five year tax trap.

Step 1: Map Your Built In Gains Exposure

Start by building a detailed schedule of every asset with potential built in gain:

- Original cost and accumulated depreciation

- Current tax basis

- Estimated fair market value, backed by appraisals where appropriate

- How critical the asset is to operations

- Whether you realistically expect to sell or dispose of it in the next five to seven years

For real estate and major equipment, spend the money on professional valuations. If the IRS ever reviews your built in gains tax, contemporaneous appraisals carry weight.

Step 2: Decide Which Assets Should Be “Rung Out” in the C Corp

In some cases, it is cheaper to sell or dispose of assets while you are still a C corporation so the gain is taxed once at the corporate level and can then be distributed in a planned way. For example:

- Sell underused equipment and lease instead

- Dispose of obsolete inventory

- Sell a secondary property that is not core to operations

Yes, you pay C corporation tax on those gains, but you avoid compounding that with built in gains tax plus shareholder level tax later. The math matters. A $300,000 gain taxed once at 21 percent is $63,000. The same gain under Section 1374 plus individual-level capital gains can easily approach $100,000 in combined tax, especially when you add California.

Step 3: Consider Dropping Assets into Separate Entities

Another advanced tactic is dropping certain assets into separate entities before the S election. For example, you may move real estate into a separate LLC taxed as a partnership, with the C corporation as a tenant instead of an owner. Done properly and early enough, this can strip large built in gains assets out of the corporation’s balance sheet so they are not subject to Section 1374.

This is highly technical work that must be coordinated with entity formation and state law. Many business owners pair this with a broader restructuring to clean up ownership, debt, and compensation before they flip the S corp switch.

Step 4: Align the Conversion Date with Your Exit Timeline

Section 1374 does not care that you plan to sell “someday.” It cares whether you sell during the recognition period. If you expect a sale in the next two years, it might be smarter to wait on the S election instead of creating a built in gains problem that did not exist.

On the other hand, if your exit window is seven to ten years out, the recognition period will likely be over before any sale, and the S election can deliver years of pass through taxation at the shareholder level.

Step 5: Layer in Broader Tax Planning

Entity choice is only one piece. You should be reviewing officer compensation, retirement contributions, fringe benefits, and family employment at the same time you consider an S election. Strategic year end moves can save thousands. Our tax planning services integrate entity structure with those day to day deductions so your C to S decision is part of a complete plan, not a one off election.

KDA Case Study: California C Corp Owner Avoids a Six Figure Built In Gains Hit

A husband and wife owned a California distribution company operating as a C corporation for nearly 20 years. The company owned a warehouse purchased for $900,000 with a current market value of about $2,200,000. It also held fully depreciated equipment worth roughly $300,000 and strong customer relationships that gave it significant goodwill.

The couple, both in their mid fifties, wanted to elect S corporation status in 2026 and sell the business around 2029. On their own, they assumed the S election would eliminate double tax and let them take sale proceeds once at favorable capital gains rates.

When they came to KDA, we walked them through the c corp to s corp conversion built in gains rules. The built in gain on the warehouse alone was about $1,300,000. Add $300,000 on equipment and another $500,000 of goodwill, and they were looking at potentially $2,100,000 of built in gain exposure if they sold within the recognition period.

At a 21 percent federal corporate rate, that meant roughly $441,000 of corporate level tax under Section 1374, plus shareholder level tax, plus California. Their “tax efficient” S corporation sale would have produced an effective tax rate north of 40 percent on a large part of the deal.

We restructured the plan. Before any S election, we facilitated an appraisal, moved the real estate into a separate LLC, and had the C corporation sign a market rent lease. We also sold outdated equipment and tightened inventory. By the time the S election took effect, built in gain exposure was down to about $600,000.

When they ultimately sold, the built in gains tax bill under Section 1374 was under $130,000, and their combined tax savings compared to the original path was just over $300,000 in the first year alone. Their advisory fee to KDA was about $25,000, delivering more than a 12x first year return on investment.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

What Happens If You Sell During the Recognition Period?

Once your S election is in place, the number one question is what happens if you sell an appreciated asset before the recognition period ends.

Step by Step Tax Result on a Built In Gain Sale

Assume your S corporation sells an asset with a $500,000 built in gain during the recognition period. Here is what happens in simplified terms:

- The S corporation reports the sale on its Form 1120 S, including the total gain realized.

- It then calculates the portion of that gain that was “built in” on the conversion date, subject to Section 1374.

- The S corporation computes a built in gains tax at the highest corporate tax rate on the smaller of built in gain or taxable income, after certain adjustments.

- The built in gains tax is paid by the S corporation itself and reported on its return, reducing the income that flows through to shareholders.

- The remaining gain, after the built in gains tax, passes through to shareholders and is taxed again at their individual rates.

This double layer is exactly what most owners tried to avoid by becoming an S corporation. The IRS’s logic is that it only applies to the appreciation that accrued while you enjoyed C corporation status.

Can You Offset Built In Gains with Losses?

Section 1374 does allow certain offsets. If your S corporation has net operating losses or other deductions, they can reduce the taxable income subject to the built in gains tax. That is where careful timing comes in:

- Plan major deductible expenses in the same year as a built in gain sale

- Use cost segregation studies to accelerate depreciation on new assets

- Consider bonus depreciation where available

- Make retirement plan contributions that reduce S corporation income

You can review how corporate level tax and pass through income interact in IRS Publication 542 and IRS Publication 535. These rules are complex enough that a modeling exercise is mandatory before any sale.

Will This Trigger an Audit?

The built in gains tax itself does not automatically trigger an audit, but large asset sales often do. Red flag situations include:

- Big gains with no supporting appraisals at the conversion date

- Inconsistent reporting between the C corporation’s final 1120 and the S corporation’s early 1120 S returns

- Unusually low officer compensation and high distributions after the S election

These are all fixable with planning. Document valuations, keep clean workpapers showing how built in gains were calculated, and put reasonable salary and distribution policies in writing.

California Specific Angles You Cannot Ignore

California does not follow every federal pass through rule perfectly, and S corporations pay a 1.5 percent tax on net income at the entity level, regardless of federal built in gains status. That means your modeling for a c corp to s corp conversion built in gains scenario must include both federal corporate tax under Section 1374 and the California S corporation tax, plus personal California tax on shareholders.

Franchise Tax and Minimum Fees

Even if your S corporation has losses or low income in a given year, the California Franchise Tax Board still expects the annual minimum franchise tax and any applicable fees. These do not disappear because you elected S status.

When we design multi entity structures involving separate real estate LLCs and an operating S corporation, we factor in these California costs. In many cases, the tax savings from avoiding built in gains tax dwarf the extra $800 per entity, but the full picture matters.

Coordination with Personal Tax Brackets

The built in gains tax calculation interacts with your individual tax bracket. A thoughtful plan will:

- Spread large gains over multiple years where possible

- Use installment sale structures to avoid bunching income in one year

- Coordinate S corporation distributions with your other W 2, 1099, and investment income

If you are self employed or have a mix of business and W 2 income, try running your numbers through a tax bracket calculator to see how different sale scenarios change your marginal rate.

Common Mistakes That Trigger Unnecessary Built In Gains Tax

Most built in gains disasters come from basic planning mistakes, not obscure legal traps. Here are the major ones.

Rushing the S Election Without a Balance Sheet Review

Many owners elect S status the same year they hear about it for the first time. Their accountant files Form 2553, but nobody maps the built in gain on assets or reviews their exit horizon.

Red Flag Alert: If you cannot produce a schedule of every major asset with basis and fair market value on the conversion date, you are flying blind. The IRS is happy to accept your election and collect built in gains tax later.

Ignoring Intangibles and Goodwill

Goodwill is often the largest built in gain, especially for professional practices and brand driven businesses. If your C corporation has built a strong brand, a loyal customer base, and recurring revenue, there is economic goodwill on the books whether you have formally recorded it or not.

Failing to consider these intangibles means you undervalue your built in gains risk and underplan for it. The IRS, however, will not forget goodwill if it reviews your sale.

Assuming the Recognition Period Will Be Shortened Again

Owners read articles about a three year recognition period and build plans around that assumption. That is dangerous. Congress changes these rules, and your specific fact pattern may or may not qualify for a shorter period even when the law changes.

Build your plan around a conservative assumption, typically a five year window. If the law later shortens the period and you qualify, that is a bonus, not the foundation of your plan.

How to Decide if an S Election Still Makes Sense

Given the c corp to s corp conversion built in gains exposure, when is an S election still the right move?

When Your Future Profits Outweigh the Built In Gains Risk

If your C corporation is generating $500,000 of annual profit and you expect that to continue for ten years, avoiding double tax on that profit usually outweighs a one time built in gains hit, especially if you can plan asset sales carefully.

In this scenario, a detailed projection will compare:

- Ten years of C corporation tax plus shareholder dividends

- Ten years of S corporation pass through taxation plus any likely built in gains tax

Running those numbers correctly is not a back of the envelope exercise. Complex cases often end up in our premium advisory services program so we can model multiple scenarios and entity combinations.

When You Have Minimal Built In Gains

Some corporations, especially newer ones or those that lease most assets, have minimal built in gains exposure. If your balance sheet is light and you do not own appreciated real estate or equipment, the built in gains tax risk may be minor. In those cases, an S election can be a relatively clean way to improve after tax cash flow to shareholders.

When You Can Wait Out the Recognition Period

If you are early in your business journey and do not plan a sale for a decade, electing S status now lets you enjoy pass through taxation while the recognition period quietly expires. You still need to document built in gains at conversion, but you can avoid triggering them with any major sales until the window closes.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Does the Built In Gains Tax Apply to New Assets Purchased After the S Election?

No. The built in gains regime only applies to assets that had built in gain on the conversion date. Assets purchased later or appreciation that accrues after the S election generally are not subject to Section 1374, although they can still generate regular S corporation income taxed to shareholders.

What If My C Corporation Has Net Operating Losses?

Net operating losses from C corporation years do not automatically carry over to offset S corporation built in gains. The interaction of NOLs and Section 1374 is technical and depends on timing and how the losses were generated. This is a situation where you should review IRS Publication 536 and run scenarios with a professional.

Can I Undo an S Election If I Realize the Built In Gains Exposure Is Too High?

Revoking an S election is possible, but it usually creates its own set of problems and timing rules. In many cases, it is more effective to manage around built in gains through asset planning and sale timing than to bounce back and forth between C and S status.

Bottom Line

The c corp to s corp conversion built in gains rules are the IRS’s way of preventing taxpayers from dodging corporate level tax on old appreciation. For California owners with valuable real estate, equipment, or goodwill, this is not a technical footnote; it is a six figure swing in your exit number.

This information is current as of 5/28/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Book Your Tax Strategy Session

If you are considering an S election or planning a business sale and you are not sure how built in gains could affect your net proceeds, do not guess. Our team builds detailed, California focused models that show you exactly how much tax is at stake and how to legally reduce it. Click here to book your consultation now.

The IRS is not hiding these rules; most advisors simply are not modeling them. That is the difference between a routine return and a real tax strategy.