The Federal Write-Off Your California Return Quietly Rejects

A business owner in Fresno buys $180,000 worth of equipment in 2025, files a federal return claiming 100% bonus depreciation, and celebrates a $180,000 deduction that wipes out most of her taxable income. Then she opens her California return and discovers that Sacramento allows exactly zero dollars of that same deduction. The gap between her federal refund and her California tax bill is $16,740. She is not alone. Thousands of California bonus depreciation vs bonus depreciation 2024 California comparisons are flooding search engines right now because business owners are realizing the rules changed dramatically and the state never followed along.

This is not a small technical footnote. It is a five-figure tax trap that hits every California business owner who buys qualifying property and assumes the federal deduction carries over to Sacramento. It does not. And the gap just got wider.

Quick Answer

Federal bonus depreciation is back to 100% for assets placed in service after January 19, 2025 under the One Big Beautiful Bill Act. California still rejects bonus depreciation entirely under Revenue and Taxation Code Section 17250 and Section 24356. That means California business owners must maintain two separate depreciation schedules, one federal and one state, and the difference can cost $10,000 to $30,000 or more in unexpected state taxes every single year.

What Changed at the Federal Level and Why California Ignored It

The Tax Cuts and Jobs Act of 2017 introduced 100% bonus depreciation for qualifying assets placed in service between September 27, 2017 and December 31, 2022. Starting in 2023, that percentage began stepping down: 80% in 2023, 60% in 2024, 40% in 2025. That phase-down created the original “bonus depreciation 2024” landscape where business owners were losing ground every year.

Then the One Big Beautiful Bill Act, signed into law on July 4, 2025, restored 100% bonus depreciation retroactively for property placed in service after January 19, 2025. The OBBBA also raised the Section 179 expensing limit to $2.5 million with a phase-out beginning at $4 million in qualifying purchases.

California did not adopt any of it. Not the 100% bonus depreciation. Not the expanded Section 179 limits. Not the retroactive application. The Franchise Tax Board still follows its own depreciation rules under the California Revenue and Taxation Code, which means your federal return and your California return live in two different universes when it comes to asset write-offs.

The 2024 vs 2025 Federal Shift

Here is the timeline that matters for anyone comparing bonus depreciation vs bonus depreciation 2024 California rules:

- 2024 Federal: 60% bonus depreciation on qualifying property. Section 179 limit of $1,220,000.

- 2025 Federal (post-OBBBA): 100% bonus depreciation on qualifying property placed in service after January 19, 2025. Section 179 limit increased to $2,500,000.

- 2024 California: 0% bonus depreciation. Section 179 capped at $25,000 (the pre-TCJA limit California froze at).

- 2025 California: Still 0% bonus depreciation. Section 179 still capped at $25,000.

The federal government expanded the deduction. California kept the door locked. That is the core problem, and it is not going away anytime soon. For a deeper dive into California-specific business tax strategies, see our complete California business owner tax strategy hub.

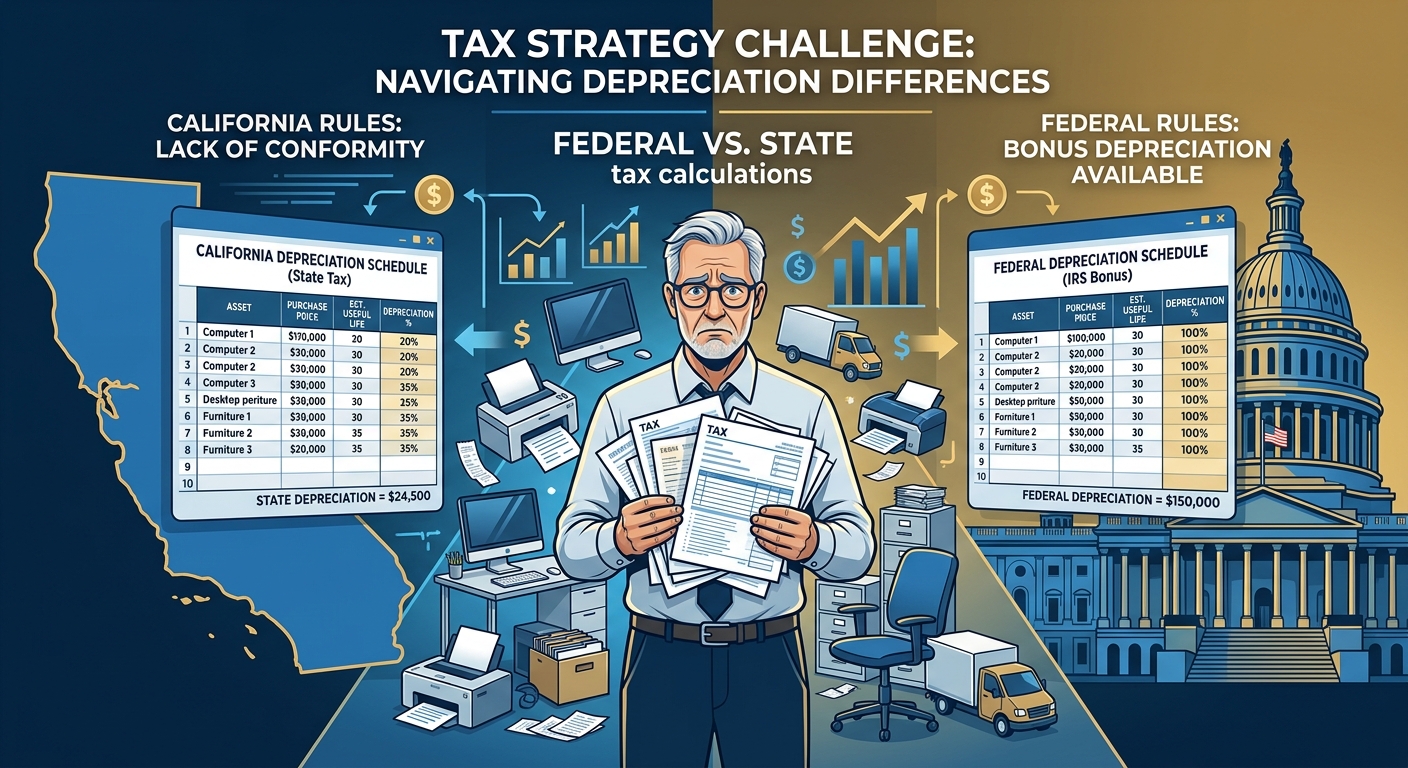

How the Dual Depreciation Schedule Actually Works

Every California business owner who claims federal bonus depreciation must maintain two separate depreciation schedules. Your accountant should be tracking this, but many do not, and the resulting errors trigger FTB adjustments and surprise tax bills.

Federal Schedule: Full Immediate Write-Off

Under the federal rules restored by OBBBA, when you purchase a $120,000 piece of equipment in 2025 and place it in service by December 31, you deduct the full $120,000 on your federal return in year one. That is 100% bonus depreciation under IRC Section 168(k). Your federal taxable income drops by $120,000 immediately.

California Schedule: Slow Depreciation Over 5 to 7 Years

On your California return, that same $120,000 asset gets depreciated using the Modified Accelerated Cost Recovery System without bonus depreciation. For 5-year property, that means roughly $24,000 in year one using the 200% declining balance method. For 7-year property, even less in year one. California also caps Section 179 at $25,000, so you cannot use that as a workaround for larger purchases.

The Math That Hurts

On a $120,000 equipment purchase for a business owner in the 9.3% California bracket:

- Federal year-one deduction: $120,000

- California year-one deduction: approximately $24,000 (5-year MACRS) or $25,000 (Section 179 cap)

- Gap: $95,000 to $96,000 in income recognized by California but not by the IRS

- Additional California tax in year one: approximately $8,835 to $8,928

That is real money. And it repeats every year you buy qualifying assets. Many business owners discover this only after filing and receiving a notice from the FTB.

Five Strategies to Close the Federal-California Depreciation Gap

You cannot eliminate the gap entirely, but you can minimize it with the right approach. Our tax planning services focus specifically on these multi-layer strategies for California business owners.

Strategy 1: Stack Section 179 With California MACRS

California allows up to $25,000 in Section 179 expensing. That is not much, but it is better than straight-line depreciation. Stack the $25,000 Section 179 with whatever first-year MACRS depreciation California allows. On a $100,000 asset classified as 5-year property, your California year-one deduction could reach approximately $40,000 instead of $20,000. That cuts the gap from $80,000 to $60,000.

Strategy 2: Time Purchases for Maximum First-Year Recovery

Under MACRS rules, the half-year convention applies to most property placed in service during the year. If you place an asset in service in January rather than December, you do not gain extra depreciation under the half-year convention, but you do gain 12 months of operational use and can start planning next year’s purchases earlier. For mid-quarter convention property, timing matters more.

Strategy 3: Use the AB 150 Pass-Through Entity Elective Tax

California’s AB 150 allows qualifying pass-through entities (S Corps, LLCs, partnerships) to pay an elective tax at the entity level. This generates a dollar-for-dollar federal tax credit on the owner’s personal return and effectively works around the $40,000 SALT cap under OBBBA. While this does not directly change your depreciation calculation, it reduces the overall state tax burden, which partially offsets the depreciation gap.

For an S Corp earning $300,000, the AB 150 election can save $3,000 to $12,000 in federal taxes, which helps absorb the higher California income caused by the depreciation difference.

Strategy 4: Elect Out of Federal Bonus Depreciation Under Section 168(k)(7)

This sounds counterintuitive, but sometimes it makes sense. If your federal taxable income is already low (or you have net operating losses), claiming 100% bonus depreciation wastes the deduction. Electing out under Section 168(k)(7) aligns your federal and California depreciation schedules, simplifies bookkeeping, and preserves the deduction for future years when you might be in a higher bracket.

Want to see how different income levels change your total tax picture? Run your numbers through this small business tax calculator to estimate the impact before making the election.

Strategy 5: Maximize Retirement Contributions to Offset the Gap

If the depreciation gap pushes your California taxable income higher than expected, offset it with retirement contributions that California does recognize. A Solo 401(k) allows up to $69,000 in total contributions for 2025 ($76,500 if you are 50 or older). California conforms to these limits, so every dollar you contribute reduces both your federal and state taxable income equally.

The Five Costliest Mistakes Business Owners Make With California Bonus Depreciation

Mistake 1: Assuming California Follows Federal Depreciation Rules

This is the most common and most expensive error. Business owners see the 100% write-off on their federal return and assume the same number flows to California. It does not. Every asset must be separately tracked for state purposes. If your CPA uses a single depreciation schedule for both returns, you have a compliance problem.

Mistake 2: Ignoring the Section 179 California Cap

The federal Section 179 limit is $2,500,000 under OBBBA. California’s limit is $25,000. That is a 100x difference. Business owners who rely on Section 179 for large purchases get a massive federal deduction and almost nothing on the California side. Plan accordingly.

Mistake 3: Not Running Dual Projections Before Buying

Before purchasing any asset over $25,000, run two projections: one for your federal return and one for your California return. Without both numbers, you cannot accurately predict your total tax liability. Many owners buy equipment in December thinking they will save a fortune, then discover the California tax hit in April.

Mistake 4: Missing the Depreciation Adjustment on Schedule CA

California Form 540, Schedule CA (California Adjustments) requires you to add back the difference between federal and California depreciation. If you skip this line or calculate it incorrectly, the FTB will catch it, usually 12 to 18 months later, with penalties and interest attached.

Mistake 5: Letting the Gap Grow Without a Multi-Year Plan

The depreciation gap is a timing difference, not a permanent one. Over the life of the asset, you will eventually deduct the same total amount on both returns. But “eventually” can mean 5 to 7 years, and the cash flow impact in year one is real. Without a multi-year tax plan, you are flying blind.

KDA Case Study: Riverside Contractor Saves $27,400 by Closing the Depreciation Gap

Marcus runs a general contracting business in Riverside with $340,000 in net profit. In 2025, he purchased $195,000 in heavy equipment, including a $68,000 excavator and $127,000 in specialized tools and machinery.

His previous accountant filed both returns using the same depreciation schedule, claiming 100% bonus depreciation on both the federal and California returns. The FTB flagged the California return, and Marcus received a notice for $14,200 in additional tax plus $1,800 in penalties and interest.

KDA stepped in and rebuilt both depreciation schedules from scratch. On the federal side, we confirmed the $195,000 in 100% bonus depreciation under OBBBA was correctly applied. On the California side, we calculated the proper MACRS depreciation plus the $25,000 Section 179 cap, then filed a corrected Schedule CA.

But we did not stop at compliance. We restructured Marcus’s tax plan using four layered strategies:

- AB 150 PTE elective tax election on his S Corp, generating $8,400 in federal savings

- Solo 401(k) contribution of $46,000, reducing both federal and California income equally

- Strategic timing of his 2026 equipment purchases to maximize California first-year recovery

- Section 168(k)(7) election analysis for low-income years to preserve future deductions

Total first-year savings: $27,400. KDA’s engagement fee: $4,800. That is a 5.7x return on investment in year one alone.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Bonus Depreciation vs Section 179: Which One Actually Helps in California?

Since California rejects bonus depreciation entirely, the real question for California business owners is not “bonus depreciation vs Section 179” at the federal level. It is “which tool gives me any California deduction at all?”

Section 179 in California: Limited but Real

California’s $25,000 Section 179 cap is your only shot at an accelerated write-off on the state return. Use it every year you have qualifying purchases. Eligible property includes machinery, equipment, off-the-shelf software, and certain improvements to nonresidential real property.

Bonus Depreciation in California: Zero

No amount of planning changes this. California Revenue and Taxation Code Section 17250 (for individuals) and Section 24356 (for corporations) explicitly decouple from federal bonus depreciation. This has been the case since 2002, and there is no pending legislation to change it.

The Combined Federal-State Playbook

Smart California business owners use bonus depreciation federally and Section 179 on the state return, then bridge the remaining gap with the strategies outlined above. Here is a side-by-side comparison for a $200,000 equipment purchase:

| Deduction Method | Federal Year-One Deduction | California Year-One Deduction |

|---|---|---|

| 100% Bonus Depreciation | $200,000 | $0 |

| Section 179 | $200,000 (within $2.5M limit) | $25,000 (hard cap) |

| MACRS Only (5-year property) | $40,000 | $40,000 |

| Section 179 + MACRS (CA strategy) | N/A (use bonus instead) | Approximately $60,000 |

The gap between $200,000 federal and $60,000 California is $140,000 in additional state-taxable income. At a 9.3% rate, that is $13,020 in extra California tax. You cannot avoid it entirely, but you can plan for it and offset it with other deductions.

What About the OBBBA Changes You Keep Hearing About?

The One Big Beautiful Bill Act, signed July 4, 2025, made several changes that affect the bonus depreciation vs bonus depreciation 2024 California comparison directly:

- 100% bonus depreciation restored permanently for property placed in service after January 19, 2025. This replaces the phase-down schedule that would have dropped to 40% in 2025 and 20% in 2026.

- Section 179 raised to $2.5 million with a $4 million phase-out threshold. This is a permanent increase.

- Section 163(j) interest limitation loosened: Depreciation, amortization, and depletion can now be added back to adjusted taxable income, allowing larger interest deductions for businesses with significant debt.

- SALT cap raised to $40,000 for 2025, up from $10,000. This helps but does not eliminate the depreciation gap issue.

- Revenue Procedure 2026-17: The IRS issued guidance allowing businesses to withdraw previous Section 163(j)(7) elections and make late Section 168(k)(7) elections to take advantage of the new rules.

California has not adopted any of these provisions. The FTB continues to apply pre-TCJA depreciation limits, which means the federal-state gap is now wider than it has been since 2017.

Will This Trigger an Audit?

The depreciation gap itself does not trigger an audit, but errors in reporting it do. Here are the red flags the FTB watches for:

- Missing Schedule CA adjustments: If your California return shows the same depreciation as your federal return, the FTB’s matching system will flag it automatically.

- Inconsistent asset listings: If your federal Form 4562 lists $200,000 in bonus depreciation but your California return shows no corresponding adjustment, expect a letter.

- Large Section 179 claims: If you claim more than $25,000 in Section 179 on your California return, the FTB will disallow the excess and assess tax plus penalties.

- S Corp depreciation pass-through errors: If your S Corp’s federal K-1 shows different depreciation than the California K-1, and the shareholder does not adjust on Schedule CA, the FTB will catch it.

The fix is simple: maintain accurate dual schedules, report the adjustment correctly on Schedule CA, and keep documentation for every asset. If you are already behind, file amended returns before the FTB contacts you.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Does California Allow Any Bonus Depreciation at All?

No. California has never conformed to federal bonus depreciation. The state follows its own version of MACRS without the Section 168(k) bonus. This has been consistent since 2002 and there is no legislation pending to change it.

Can I Use Section 179 to Make Up the Difference?

Partially. California allows up to $25,000 in Section 179 expensing. For assets under $25,000, this effectively replaces bonus depreciation on the state return. For larger purchases, the gap remains significant and must be planned around.

What Happens to the Depreciation I Cannot Claim in Year One on My California Return?

It is not lost. California allows the full MACRS depreciation over the asset’s recovery period (5 years, 7 years, etc.). The difference is timing: you deduct it all at once federally but spread it over multiple years in California. Over the asset’s life, total deductions are equal. The cash flow impact in year one is the problem.

Should I Elect Out of Federal Bonus Depreciation to Simplify My Returns?

Only if you have a specific strategic reason. Electing out under Section 168(k)(7) aligns your schedules but sacrifices the immediate federal tax savings. This makes sense only when your federal taxable income is already low, you have NOLs to use, or the bookkeeping cost of dual schedules exceeds the tax benefit.

How Do I File Correctly if My CPA Only Prepared One Depreciation Schedule?

File an amended California return (Form 540X) with the correct depreciation calculations. Prepare a separate California depreciation schedule for every asset that received federal bonus depreciation. Attach it to your amended return and include the proper adjustments on Schedule CA. Do this before the FTB contacts you to avoid penalties.

Your Year-End Depreciation Checklist for California

Use this checklist before December 31 of every year:

- Confirm all assets placed in service during the year are logged with purchase date, cost, and recovery period

- Run federal depreciation schedule using 100% bonus depreciation under Section 168(k)

- Run separate California depreciation schedule using MACRS without bonus depreciation

- Apply the $25,000 California Section 179 cap to the highest-value qualifying asset

- Calculate the depreciation gap and estimate the additional California tax owed

- Evaluate whether AB 150 PTE election, retirement contributions, or other offsets can reduce the gap

- Run dual projections for any planned equipment purchases in the next 90 days

- Review Schedule CA for accurate add-back of federal-state depreciation differences

- Confirm your bookkeeping system tracks both schedules separately

This information is current as of 3/30/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

The IRS is not hiding these deductions and California is not trying to punish you. The two systems just operate on different timelines with different rules. The business owners who win are the ones who plan for both.

Book Your Depreciation Strategy Session

If the gap between your federal and California depreciation is costing you $10,000 or more every year, stop guessing and start planning. Book a personalized consultation with our strategy team to build a dual-schedule depreciation plan, maximize your California Section 179, and layer in every legal offset available to you. Click here to book your consultation now.