What Is the AMT Tax Rate for 2024?

The AMT tax rate 2024 is a parallel tax system that hits high earners who claim too many deductions or credits. If your adjusted gross income exceeds $609,350 (married filing jointly) or $406,900 (single), you could face AMT exposure. The tax has two rates: 26% on the first $220,700 of AMT income, and 28% on anything above that. The AMT exemption for 2024 is $133,300 for married couples filing jointly and $85,700 for single filers, but these exemptions phase out as your income climbs.

Here is the reality: The AMT was designed in 1969 to stop 155 ultra-wealthy households from paying zero federal income tax. Fast-forward to 2024, and it now affects engineers with stock compensation, business owners deducting state taxes, and real estate investors accelerating depreciation. If you live in California where the top state tax rate is 13.3%, your federal SALT deduction is capped at $10,000. That cap alone can trigger AMT, forcing you to recalculate your entire tax bill under a system that disallows many common deductions.

Who Gets Hit by AMT in 2024?

AMT exposure is not random. It targets specific taxpayer profiles and income situations. Understanding whether you fall into a high-risk category can save you from a five-figure surprise tax bill in April.

High-Income W-2 Employees with Stock Compensation

If you exercise incentive stock options (ISOs), the spread between your exercise price and fair market value becomes an AMT preference item. You pay no regular income tax on ISO exercises, but the AMT system treats that spread as taxable income. A software engineer in San Francisco exercising $200,000 worth of ISOs could face a $56,000 AMT bill even though they received no cash from the transaction.

Business Owners in High-Tax States

California, New York, New Jersey, and other high-tax states create AMT risk for business owners who pay significant state income taxes. The $10,000 SALT cap enacted in 2017 means if you paid $50,000 in California state taxes, you can only deduct $10,000 on your federal return under the regular tax system. The AMT system disallows the entire SALT deduction, treating that $10,000 as an AMT adjustment. For a married couple earning $500,000 in California, this one adjustment can trigger $8,000 to $12,000 in additional AMT liability.

Real Estate Investors Accelerating Depreciation

Real estate professionals using cost segregation or bonus depreciation to write off $100,000+ in a single year need to watch AMT closely. Accelerated depreciation creates a timing difference between regular tax and AMT calculations. If you deduct $150,000 in bonus depreciation on commercial property, the AMT system recalculates your depreciation using slower methods, adding back $80,000 to $100,000 as an AMT adjustment. That adjustment can push you into AMT territory even if your cash flow is negative.

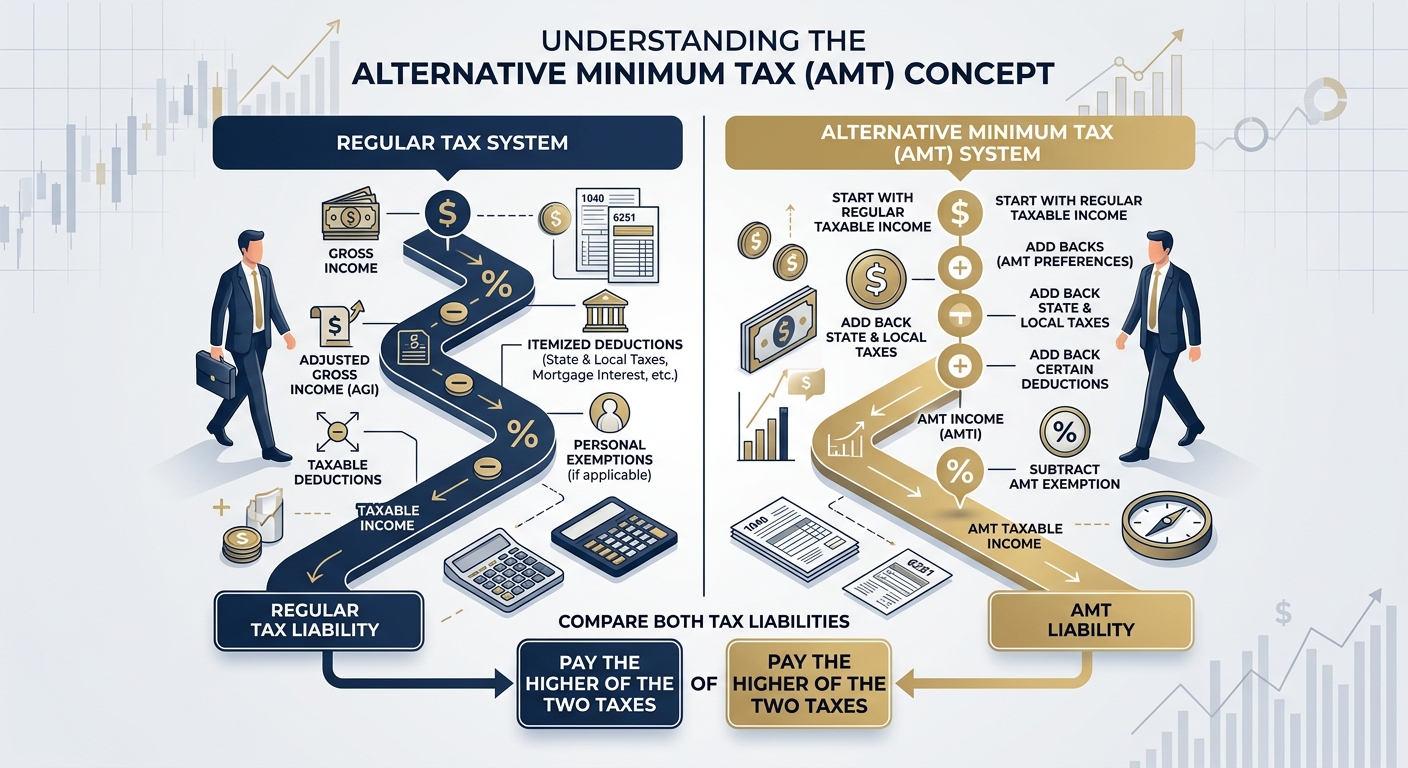

How AMT Actually Works: The Two-System Tax Trap

Most taxpayers assume they calculate one tax bill and pay it. AMT forces you to run two parallel calculations, then pay whichever amount is higher. Here is the step-by-step breakdown of how the IRS makes you calculate AMT.

Step 1: Calculate Your Regular Taxable Income

Start with your adjusted gross income (AGI). Subtract your standard deduction or itemized deductions, including mortgage interest, charitable contributions, and state and local taxes up to $10,000. Apply the regular federal tax brackets ranging from 10% to 37%. This gives you your regular federal income tax liability.

Step 2: Add Back AMT Adjustments and Preferences

Now the AMT system makes you add back certain deductions you just claimed. Common AMT adjustments include the entire state and local tax deduction beyond the first dollar, personal exemptions if you claimed them, miscellaneous itemized deductions, ISO exercise spreads, accelerated depreciation on real estate, and certain tax-exempt interest from private activity bonds. These add-backs can increase your AMT income by $50,000 to $200,000 depending on your situation.

Step 3: Subtract the AMT Exemption

For 2024, the AMT exemption is $133,300 for married couples filing jointly and $85,700 for single filers. However, this exemption phases out at a rate of 25 cents per dollar once your AMT income exceeds $1,218,700 for joint filers or $609,350 for single filers. If your AMT income is $1,750,000, your exemption phases out completely, meaning you get zero exemption amount.

Step 4: Apply AMT Tax Rates

The AMT system uses only two tax rates: 26% on the first $220,700 of AMT income above your exemption, and 28% on everything above that threshold. If your AMT income after exemption is $400,000, you pay 26% on the first $220,700 ($57,382) plus 28% on the remaining $179,300 ($50,204), for a total AMT of $107,586.

Step 5: Compare and Pay the Higher Amount

Calculate the difference between your AMT liability and your regular tax liability. If your AMT is higher, you pay the difference as additional tax on top of your regular tax bill. If your regular tax is higher, you pay that amount and AMT does not apply. There is no middle ground, you always pay the higher of the two calculations.

Real-World AMT Scenarios: What It Actually Costs

Understanding AMT in theory is one thing. Seeing the actual dollar impact on taxpayers like you makes the risk concrete. These scenarios use real numbers based on 2024 tax rates and common taxpayer situations.

Tech Employee Exercising ISOs

David is a software engineer in San Jose earning a $180,000 salary. In March 2024, he exercised 5,000 ISOs with an exercise price of $10 per share when the fair market value was $50 per share. His ISO spread is $200,000 ($40 per share × 5,000 shares). Under regular tax rules, he pays zero tax on the ISO exercise. Under AMT rules, that $200,000 spread is added to his AMT income. After his AMT exemption of $85,700 as a single filer, he has $294,300 of AMT income ($180,000 salary + $200,000 ISO spread – $85,700 exemption). His AMT calculation is $76,418 (26% on $220,700) plus $20,608 (28% on the remaining $73,600), totaling $97,026 in AMT. His regular tax on $180,000 is approximately $38,000. He owes an extra $59,026 in AMT even though he received no cash from exercising his options.

California Business Owner with High State Taxes

Maria runs an LLC taxed as an S Corp in Los Angeles. Her business generated $450,000 in profit in 2024. She is married filing jointly and paid $48,000 in California state income taxes. Under regular tax rules, she can deduct only $10,000 of state taxes due to the SALT cap. Her taxable income is $440,000 after the standard deduction of $29,200, resulting in a regular federal tax bill of approximately $96,000. Under AMT rules, the entire $10,000 SALT deduction is disallowed as an AMT adjustment. Her AMT income becomes $450,000. After subtracting the $133,300 joint filer exemption, she has $316,700 in AMT income. Her AMT is $82,222 (26% on $220,700) plus $26,880 (28% on $96,000), totaling $109,102. She owes an additional $13,102 beyond her regular tax because California’s high state taxes triggered AMT.

Real Estate Investor Using Cost Segregation

Robert purchased a $2 million commercial building in 2024 and hired a cost segregation firm to reclassify $800,000 of the building into 5-year and 15-year property. Using bonus depreciation, he deducted $480,000 in the first year. His rental income from all properties was $220,000, so the depreciation created a $260,000 tax loss that offset his W-2 income of $260,000 from his day job as a physician. Under regular tax rules, his taxable income is near zero. Under AMT rules, the IRS requires straight-line depreciation over 40 years for the reclassified assets, limiting his AMT depreciation to $120,000 instead of $480,000. The $360,000 difference is added back as an AMT adjustment. His AMT income becomes $360,000 ($260,000 W-2 income + $220,000 rental income – $120,000 AMT depreciation). After the $133,300 exemption, his AMT income is $226,700. His AMT is $58,942 (26% on $220,700) plus $1,680 (28% on $6,000), totaling $60,622 in AMT despite showing a tax loss under regular tax rules.

Special Situations and Edge Cases

AMT does not affect all taxpayers equally. Certain scenarios create disproportionate AMT exposure that most tax software does not flag until you file. Knowing these edge cases in advance lets you plan around them.

Multi-State Income Earners

If you earned income in California and moved to Texas mid-year, the SALT cap applies to the combined state taxes you paid in both states. Your California taxes for the first six months could be $25,000, but you can still only deduct $10,000 federally. The AMT system disallows that $10,000 entirely, creating a $25,000 AMT adjustment even though you are now a Texas resident with no state income tax.

Married Filing Separately Taxpayers

Married filing separately (MFS) taxpayers get only half the AMT exemption of joint filers: $66,650 instead of $133,300 for 2024. If you file MFS to preserve student loan income-driven repayment benefits or because of a separation, you face AMT exposure at much lower income levels. A single earner with $150,000 in income filing MFS could trigger AMT with just $15,000 in state tax payments and a modest ISO exercise.

AMT Credit Carryforward from Prior Years

If you paid AMT in previous years due to timing differences like ISO exercises or accelerated depreciation, you may have an AMT credit that reduces your regular tax in future years. The credit is nonrefundable, meaning it can reduce your regular tax to zero but does not generate a refund. If you have a $30,000 AMT credit from 2022 ISO exercises and you sell those ISO shares in 2024, you can apply the credit against your 2024 regular tax bill. However, the credit cannot be used if you owe AMT again in 2024, creating a catch-22 situation where the credit sits unused for years.

What Happens If You Miss This?

Failing to calculate AMT when you owe it creates immediate financial and compliance consequences. The IRS does not treat AMT underpayment as an optional calculation error. Here is what goes wrong when you ignore AMT exposure.

If you file your return without calculating AMT and the IRS later determines you owed it, you receive a CP2000 notice showing the additional tax, plus penalties and interest. The failure-to-pay penalty is 0.5% per month on the unpaid AMT amount, capped at 25%. If you owe $15,000 in AMT and do not pay it for 12 months, you owe an additional $900 in penalties plus 7% annual interest compounded daily, adding roughly $1,050 in interest. Your total bill becomes $16,950 instead of $15,000 if you had calculated it correctly upfront.

Underpayment penalties apply if you did not pay enough estimated tax throughout the year. AMT increases your total tax liability, which means your estimated tax payments may fall short. If you owed $40,000 in regular tax plus $12,000 in AMT ($52,000 total) but only paid $36,000 in estimated taxes (90% of your prior year tax), you face underpayment penalties on the $16,000 shortfall. The penalty rate is the federal short-term rate plus 3 percentage points, currently around 8% annually. On a $16,000 underpayment for six months, you owe approximately $640 in additional penalties.

The IRS has three years from your filing date to audit and assess additional AMT. If you filed in April 2024 without calculating AMT, the IRS can send you a notice as late as April 2027 demanding payment. By that time, penalties and interest can add 30% to 40% to your original AMT liability, turning a $10,000 AMT obligation into a $13,500 to $14,000 bill.

KDA Case Study: High-Net-Worth Individual

Jennifer is a venture capital partner in Palo Alto earning $850,000 annually with significant ISO holdings from portfolio companies. In 2023, she exercised $400,000 worth of ISOs without calculating AMT exposure. She paid $72,000 in California state income taxes that year and claimed a $10,000 SALT deduction. When she filed her return using basic tax software, she did not realize she triggered $94,000 in AMT liability on top of her $210,000 regular tax bill. The software never flagged the ISO exercise as an AMT preference item because she did not link her brokerage statements to the tax program.

KDA performed a comprehensive AMT analysis in early 2024 before she exercised additional ISOs. We identified that her 2023 return had underpaid AMT by $94,000 and helped her file an amended return before the IRS caught it, avoiding penalties. For 2024, we restructured her ISO exercise strategy by splitting exercises across two tax years, keeping her AMT income below the exemption phase-out threshold. We also helped her make estimated tax payments covering both regular tax and AMT, eliminating underpayment penalties. Jennifer paid $8,500 for our AMT planning and amended return work. The strategy saved her $94,000 in potential penalties and interest, plus another $31,000 in 2024 AMT through smarter ISO timing. Her first-year ROI was 14.7x, and she now exercises ISOs strategically every year with zero AMT surprises.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How to Calculate Your AMT Exposure Before Filing

You can estimate your AMT risk before filing your return by tracking the key inputs that trigger the parallel tax system. This five-step process takes 20 minutes and prevents expensive surprises in April.

Gather Your AMT Adjustment Data

Pull together documentation showing your total state and local taxes paid (check your W-2 box 17 and estimated tax payment records), ISO exercise information from your brokerage including spread amounts, accelerated depreciation schedules from cost segregation studies or bonus depreciation elections, private activity bond interest from municipal bonds (check your 1099-INT), and miscellaneous itemized deductions like unreimbursed employee expenses if you qualify. Each of these creates an AMT add-back that increases your AMT income above your regular taxable income.

Calculate Your AMT Income

Start with your adjusted gross income from line 11 of your Form 1040. Add back your state and local tax deduction amount from Schedule A line 5e, your ISO exercise spread from Form 3921, your excess depreciation (regular depreciation minus AMT straight-line depreciation), and any private activity bond interest. This gives you your alternative minimum taxable income (AMTI) before exemptions.

Apply the AMT Exemption and Phase-Out

Subtract the 2024 AMT exemption: $133,300 if married filing jointly or $85,700 if single. If your AMTI exceeds the phase-out threshold ($1,218,700 for joint filers or $609,350 for single filers), reduce your exemption by 25 cents for every dollar above the threshold. For example, if your AMTI is $1,500,000 as a joint filer, you exceed the threshold by $281,300. Your exemption is reduced by $70,325 (25% of $281,300), leaving you with a $62,975 exemption instead of the full $133,300.

Compute Your Tentative Minimum Tax

Apply the AMT tax rates to your AMTI after exemption. Use 26% on the first $220,700 and 28% on any amount above that. If your AMTI after exemption is $350,000, your tentative minimum tax is $57,382 (26% of $220,700) plus $36,204 (28% of $129,300), totaling $93,586.

Compare to Your Regular Tax

Calculate your regular federal income tax using the standard or itemized deductions and regular tax brackets. Subtract any nonrefundable credits like the child tax credit or foreign tax credit. If your tentative minimum tax ($93,586) exceeds your regular tax after credits ($78,000), you owe AMT of $15,586. If your regular tax is higher, you owe zero AMT.

If you prefer a calculator to run these numbers quickly, use this federal tax calculator to estimate your total federal tax bill including potential AMT exposure.

Strategies to Reduce or Avoid AMT

AMT is not inevitable. Strategic planning throughout the year can reduce or eliminate your exposure entirely. These approaches work for W-2 employees, business owners, and investors facing AMT risk.

Time ISO Exercises Across Multiple Tax Years

Instead of exercising $500,000 worth of ISOs in one year, split the exercises into $125,000 per year over four years. This keeps your AMT income below the exemption phase-out threshold and prevents the 28% AMT rate from applying. If you exercise $125,000 of ISOs in 2024 as a single filer with $180,000 in salary, your AMTI is $305,000 ($180,000 + $125,000). After the $85,700 exemption, your AMT income is $219,300, keeping you entirely in the 26% bracket. Your AMT is $57,018. If you exercised all $500,000 in one year, your AMTI would be $680,000, triggating the 28% rate and exemption phase-outs, resulting in $158,000+ in AMT.

Maximize Deductions That AMT Allows

Focus on deductions that work under both tax systems. Charitable contributions, mortgage interest on acquisition debt (up to $750,000 of principal), and business expenses under Schedule C are allowed under both regular tax and AMT. If you are charitably inclined and facing AMT, donate appreciated stock instead of cash. You deduct the fair market value under both systems and avoid capital gains tax on the appreciation. A $50,000 donation of stock with a $10,000 cost basis saves you $13,000 to $14,000 in AMT (26% to 28% rate) and eliminates $8,000 to $9,400 in capital gains tax (20% federal rate plus 3.8% net investment income tax).

Defer State Tax Payments to Future Years

If you pay estimated state taxes in January instead of December, you shift that deduction to the next tax year. For California taxpayers who paid $40,000 in estimated state taxes, deferring the January 2025 payment from December 2024 moves $10,000 of SALT deduction from 2024 to 2025. If you are in AMT in 2024 but expect to be out of AMT in 2025, deferring the payment lets you claim the $10,000 SALT deduction when it actually reduces your tax bill instead of wasting it in an AMT year where it provides zero benefit.

Use Cost Segregation Strategically

Real estate investors can avoid AMT depreciation adjustments by electing out of bonus depreciation under IRC Section 168(k)(7). If you purchase a $3 million commercial building and perform cost segregation, you can take regular MACRS depreciation over 5, 15, and 39 years without triggering AMT add-backs. You lose the first-year bonus depreciation benefit, but you avoid the $100,000+ AMT adjustments that come with it. For investors in AMT already, this trade-off makes sense because the bonus depreciation provides zero incremental tax benefit if you are paying AMT anyway.

Accelerate Income Into AMT Years

If you know you will pay AMT in 2024 regardless of planning, accelerate additional income into that year. Sell appreciated stock, convert traditional IRA funds to Roth IRAs, or take larger retirement account distributions. Once you are in AMT, additional income is taxed at 26% to 28% instead of the regular 32% to 37% rates. If you are a business owner planning to sell your company in the next two years and you are already in AMT due to ISO exercises, sell in the AMT year to pay 28% AMT plus 20% capital gains (48% combined) instead of 37% regular rate plus 20% capital gains (57% combined) in a non-AMT year.

California-Specific Considerations

California taxpayers face unique AMT challenges due to the state’s 13.3% top income tax rate. The SALT cap and California tax system interact to create AMT exposure that residents of zero-income-tax states never experience.

A married California couple earning $450,000 pays approximately $38,000 in state income taxes. Under federal tax rules, they can deduct only $10,000 of those taxes. The remaining $28,000 is disallowed and triggers an AMT adjustment. For these taxpayers, the AMT adds $7,280 to $7,840 to their federal tax bill (26% to 28% of the $28,000 adjustment) solely because they live in California instead of Nevada or Texas.

California does not conform to many federal AMT rules. The state has its own AMT system with different exemption amounts and phase-out thresholds. For 2024, California’s AMT exemption is $120,484 for joint filers, lower than the federal exemption. California taxpayers can pay federal AMT, California AMT, both, or neither depending on their specific adjustments. You must run four separate tax calculations (federal regular, federal AMT, California regular, California AMT) to determine your total tax liability.

If you work in California but live in Oregon or Nevada, you still pay California income tax on your California-source income. Those taxes are fully deductible on your Oregon or Nevada return but subject to the $10,000 SALT cap on your federal return, creating federal AMT exposure even though you are not a California resident. Employees working remotely from zero-income-tax states for California employers face this issue frequently.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Can I avoid AMT by taking the standard deduction instead of itemizing?

No. AMT adjustments apply regardless of whether you itemize or take the standard deduction. The most common AMT triggers like ISO exercises, accelerated depreciation, and private activity bond interest have nothing to do with itemized deductions. Even taxpayers who take the standard deduction can owe AMT if they have these preference items.

Does AMT apply to capital gains and qualified dividends?

Capital gains and qualified dividends are taxed at the same preferential rates under both regular tax and AMT systems (0%, 15%, or 20% depending on income). However, large capital gains can push your overall income high enough to trigger AMT on your other income. If you realize a $500,000 capital gain, that income can cause your AMT exemption to phase out entirely, forcing you to pay AMT on your ordinary income even though the gain itself is taxed at 20% under both systems.

How long does the AMT credit last?

The AMT credit has no expiration date. It carries forward indefinitely until you use it to offset regular tax in a year when you do not owe AMT. If you paid $50,000 in AMT in 2024 due to ISO exercises and you sell those shares in 2029, you can claim the $50,000 credit in 2029 to reduce your regular tax bill. The Tax Cuts and Jobs Act of 2017 made all remaining pre-2018 AMT credits refundable, but credits generated in 2018 and later remain nonrefundable and carryforward only.

Book Your Tax Strategy Session

If you exercised ISOs this year, paid over $20,000 in state taxes, or used cost segregation on investment property, you could owe tens of thousands in AMT without realizing it. Most tax software does not flag AMT exposure until you file, leaving you scrambling in April to pay a bill you did not budget for. KDA specializes in proactive AMT planning for high earners, business owners, and real estate investors. We calculate your AMT risk before year-end and implement strategies to reduce or eliminate the liability entirely. Book your consultation now and stop paying the IRS more than you legally owe.

This information is current as of 3/29/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.