Most owners are more afraid of choosing the wrong entity than they are of getting an IRS letter years later. If you are staring at your tax return or talking to your bookkeeper and thinking, am i s corp or c corp, you already know this choice can add or erase tens of thousands of dollars over your career.

The problem is that most explanations sound like law school lectures. You do not need theory. You need a clear path that says, based on your profit, goals, and where you live, which side of the line you should be on today and what it would take to change it.

Quick Answer

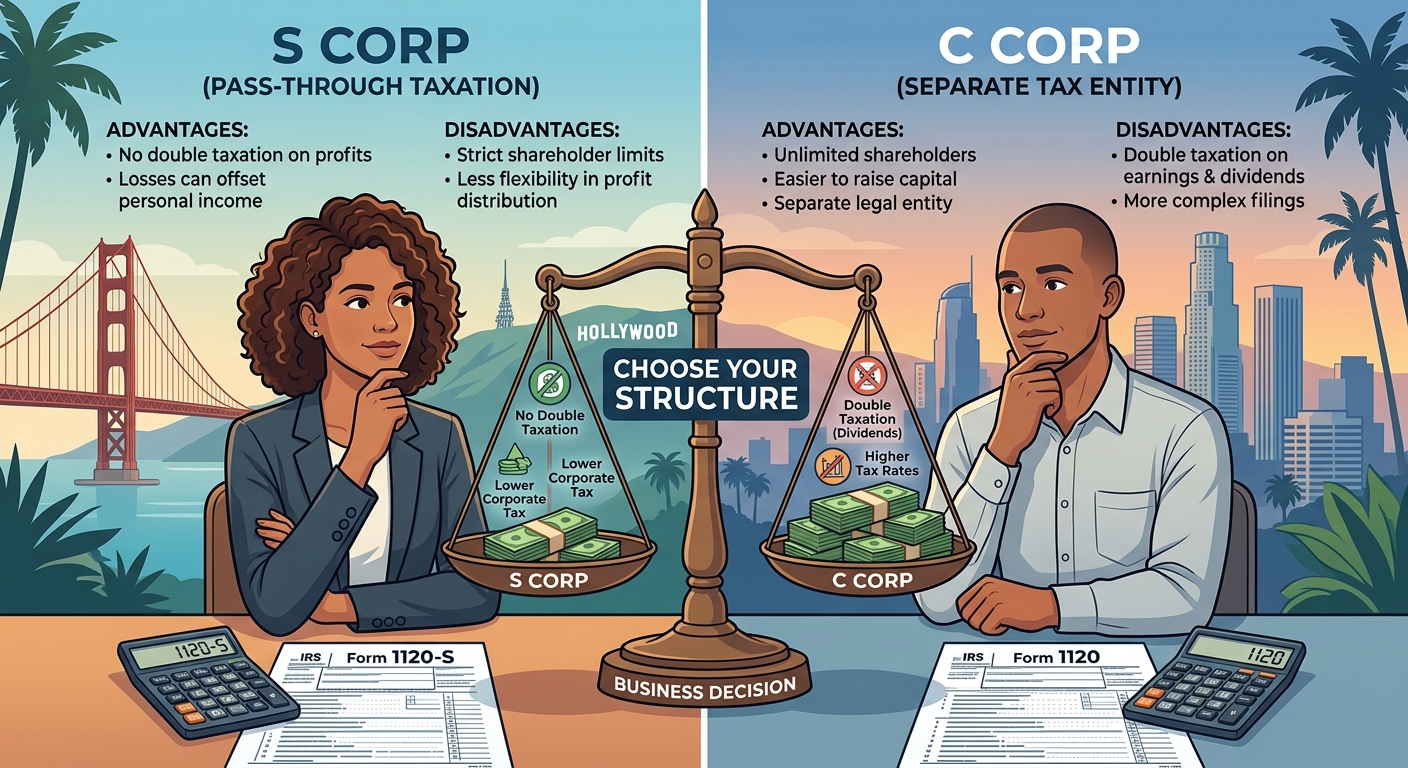

If your business is closely held, profitable, and you intend to pull most of the money out for yourself, an S corporation is usually more tax efficient than a C corporation because only your salary is hit with payroll tax and remaining profit passes through once. A C corporation can make sense when you plan to reinvest profits, bring in investors, or eventually sell the company and take advantage of long term capital gain treatment on stock, but you must be comfortable with corporate level tax plus potential dividend tax. In California, both S and C corporations still pay the Franchise Tax Board, so you are comparing federal savings, long term plans, and compliance complexity, not looking for a magic state tax loophole.

How To Think Through “Am I S Corp or C Corp”

Start with how your money actually moves. Forget labels for a moment and answer three questions.

- How much profit does the business produce in a typical year after expenses but before your own pay

- How much of that profit do you want to pull out personally in the next one to three years

- Do you expect to bring in outside investors or sell stock, or is this primarily an income machine for you

Owners with stable profit above roughly 60,000 dollars and no immediate need for outside investors are usually better off with an S corporation structure because it allows part of that profit to avoid self employment tax. According to the IRS S corporation overview, an S corporation is a regular corporation that has elected to pass income, losses, deductions, and credits through to shareholders for federal tax. The entity itself usually does not pay federal income tax.

A C corporation, by contrast, is the default corporation under federal law. It pays its own tax on profits and then shareholders pay tax again on dividends. The basic rules are laid out in IRS Publication 542. This double layer is not always bad. If your plan is to leave much of the profit in the company to expand, or you are building a startup that needs venture capital, corporate level tax can be acceptable in exchange for flexibility raising money and issuing different share classes.

If you are a service based owner in California, such as a consultant, agency head, or professional practice, and you expect to live on most of your profit, an S corporation usually puts more money in your pocket. Many business owners find that this one decision changes their effective tax rate more than any other move they make.

Tax Differences That Actually Hit Your Wallet

Let us run numbers for a single owner business with 200,000 dollars of net profit before the owner pays themself.

Scenario 1: Operating As A C Corporation

The corporation pays federal corporate income tax on its profit. At a 21 percent federal rate, that is about 42,000 dollars. If the owner then distributes 100,000 dollars of the remaining profit as dividends, the owner may pay, for example, 15 percent qualified dividend tax plus the 3.8 percent net investment income tax, roughly another 18,800 dollars. Ignoring state tax for the moment, the combined hit is around 60,800 dollars.

In California there is also an 8.84 percent corporate tax for C corporations, so another roughly 17,680 dollars on the same 200,000 dollars of profit. The combined federal and state drag can easily cross 78,000 dollars each year for this level of income.

Scenario 2: Electing S Corporation Status

Now assume the same business is an S corporation. The owner pays themself a reasonable salary of 110,000 dollars and takes the remaining 90,000 dollars as an S corporation distribution. Salary is subject to payroll tax. The distribution is not.

Roughly 110,000 dollars is hit with Social Security and Medicare. Using 15.3 percent on most of that wage, payroll tax is around 16,830 dollars, split between employee and employer side. The 90,000 dollar distribution is only subject to income tax. There is no federal corporate level tax on the S corporation profit itself. In California, the S corporation pays a 1.5 percent tax on net income, about 3,000 dollars in this example, far lower than the 8.84 percent C corporation rate.

The difference between nearly 80,000 dollars in combined tax for the C corporation scenario and closer to 40,000 to 50,000 dollars total burden for the S corporation scenario is why the question am i s corp or c corp matters so much above certain profit levels.

If you want to see roughly how different profit levels affect your own bill, plug your numbers into this small business tax calculator and compare C corporation tax versus pass through assumptions.

Payroll, Dividends, And Reasonable Salary Rules

The biggest operational difference between the two structures is how you pay yourself.

Paying Yourself From A C Corporation

As a C corporation shareholder employee, you typically take a salary. The corporation deducts that salary as a business expense and pays payroll taxes. You can also receive dividends, which are not deductible to the corporation and are taxed to you at dividend tax rates. If you underpay salary and overpay dividends to dodge payroll tax, the IRS can reclassify those dividends as wages and assess back payroll taxes and penalties.

Paying Yourself From An S Corporation

As an S corporation owner, the rule is that you must take a reasonable salary for the work you perform, then you can take additional profit as distributions. The IRS has been clear, through court cases and guidance, that zero salary for an active owner is not acceptable. The definition of reasonable comes from facts and circumstances, industry norms, and what you would pay someone else to do your job. The IRS discusses this in several places, including its S corporation reasonable compensation guidance.

Get the salary number wrong and your S corporation advantage erodes quickly. Set it thoughtfully and document how you arrived at it and you can often carve 20,000 dollars or more each year out of the self employment tax base for an established six figure business.

Owners who want help designing that salary split and making sure it ties back to their bookkeeping often lean on professional entity formation services so that payroll, minutes, and elections line up correctly with the tax story they are telling the IRS.

California Franchise Tax And State Level Issues

In California, the S versus C conversation comes with its own twist. Both entities pay the Franchise Tax Board, but the rates differ.

- C corporations generally pay 8.84 percent of net income to California, even if the federal corporate rate is 21 percent

- S corporations pay 1.5 percent of net income, with a current minimum of 800 dollars

- LLCs taxed as partnerships or disregarded entities pay an 800 dollar minimum tax plus a fee on gross receipts at certain levels

So in California, the C corporation often carries the heaviest combined federal and state load, while the S corporation usually offers a better balance, especially for professional services, consultants, and other high margin businesses.

If you want a deeper, California specific breakdown of S corporation planning, including how to structure payroll and distributions, the article at this link is worth a full read: complete guide to S corporation tax strategy in California.

This is also why the answer to am i s corp or c corp is rarely the same for a Silicon Valley startup seeking venture capital and for a solo consultant in San Diego earning 250,000 dollars with no investors on the horizon.

KDA Case Study: Agency Owner Chooses The Right Election

Consider Maria, who runs a marketing agency in Los Angeles. She operates through an LLC that is currently taxed as a disregarded entity, reporting all profit on Schedule C. In 2024 her business generated 230,000 dollars of net income. She paid self employment tax on the entire amount and her total tax bill for federal and California income and self employment taxes was just over 80,000 dollars.

Heading into 2025 she asked the same question, am i s corp or c corp, after a friend suggested she elect S status. During her strategy session, we walked through her goals. She planned to stay owner operated for the next five years, had no interest in raising outside capital, and expected profit to grow to 260,000 dollars. Based on her role and comparable salaries for creative directors in her market, we agreed that a 130,000 dollar salary was defensible, with the remaining 130,000 dollars taken as S corporation distributions.

We helped her file Form 2553 to elect S corporation status and set up payroll. In the first full year under the new structure, Maria still paid income tax on the full 260,000 dollars, but only 130,000 dollars was hit with Social Security and Medicare. Her self employment and payroll tax burden fell by about 17,000 dollars, while California corporate tax at 1.5 percent added roughly 3,900 dollars. Net first year savings were just over 13,000 dollars. Her fee for comprehensive setup and ongoing advisory ran about 4,500 dollars, so she achieved nearly a 3 to 1 first year return and expects even higher savings as profit grows.

Maria did not need a C corporation because she did not plan to issue preferred stock or bring in investors. For her, the S corporation was the answer to the am i s corp or c corp question and it shaved five figures off her annual tax bill in a way that will compound over the next decade.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Red Flag Alert: Mistakes That Trigger IRS Scrutiny

Choosing between S and C is only half the battle. The other half is operating in a way that matches the rules you signed up for. Here are mistakes that regularly get owners into trouble.

Zero Or Tiny Salary In An S Corporation

The IRS pays special attention to S corporations where owners take large distributions and little or no salary. If your business shows 200,000 dollars of profit and you pay yourself 20,000 dollars of W 2 wages, that is a problem waiting to be reclassified. Expect back payroll taxes, penalties, and interest if the IRS audits and concludes your pay is not reasonable for your role.

Personal Expenses Through A C Corporation

Some C corporation owners treat the company like a personal checking account, running family travel, groceries, and personal vehicle costs through the books. The IRS can disallow these deductions, reclassify them as wages or dividends, and assess additional tax. Publication 535 and related guidance are clear that only ordinary and necessary business expenses are deductible, see IRS Publication 535.

Late Or Botched Elections

Another issue we see is owners deciding to be an S corporation but never properly filing Form 2553, or filing it late without using the relief procedures. They operate as if they were an S corporation, then find out years later that the IRS still views them as a C corporation or as an LLC taxed as a sole proprietorship. Cleaning this up usually requires amended returns and sometimes a private letter ruling request, which is not cheap.

The fix is simple. Make the election on time, document it, and keep confirmation letters with your permanent records. If you are not sure which box you checked years ago, that is a good reason to pull your prior returns and get clarity before the next filing season.

Will This Choice Lock Me In Forever

Many owners freeze because they believe picking S or C is irreversible. That is not true, but there are timing rules and side effects.

You can elect S status for an existing C corporation as long as you meet the eligibility rules, such as having no more than 100 shareholders and only one class of stock. Once you terminate an S election, you generally must wait five years before electing again, with some exceptions. Converting from S back to C can create built in gains tax exposure if the company holds appreciated assets.

If you are operating as an LLC, you can often elect to be treated as an S corporation without changing your state law entity. For many service businesses this is the cleanest path because it keeps legal structure simple while optimizing taxes. The question am i s corp or c corp then becomes, do you want the LLC to be taxed as an S corporation or as a C corporation, and on what timeline.

What If I Plan To Sell Or Raise Investors

If you are building a startup that expects outside funding, the conversation shifts. Venture capital funds generally insist on C corporations because they need preferred stock and flexible equity structures. In that world, double taxation is part of the model and your main tax lever often becomes long term capital gain treatment when you sell your shares.

For a more traditional small business, such as a medical practice, engineering firm, or construction company, the exit is often a sale of assets, not stock. In those cases S corporations often provide a cleaner flow through of gain to individual tax returns, and buyers may be willing to pay a bit more for an asset deal. Each scenario is different, which is why high income professionals often layer in ongoing advisory, not just year end tax prep. If you are in one of these groups, it can be worth reviewing the service options on KDA’s premium advisory page to see how multi year planning can be structured.

Fast Tax Fact: Deadlines And Documentation

To elect S corporation status for a calendar year entity, you generally file Form 2553 no later than two months and 15 days after the beginning of that tax year. For a new corporation formed on January first, that means March 15. The IRS has late election relief in many cases, but you should not rely on it unless you have to. Details are in the instructions to Form 2553 on IRS.gov.

Regardless of entity type, keep copies of filed elections, stock ledgers, meeting minutes, and payroll reports. If the IRS questions whether your S election was valid, or whether your salary level is defensible, well organized records are often the difference between a short correspondence exam and a painful multi year lookback.

This information is current as of 6/29/2026. Tax laws change frequently. Verify major decisions against current IRS guidance and California Franchise Tax Board rules if you are reading this at a later date.

How To Decide In Under An Hour

If you want a practical framework rather than a tax treatise, use this simple sequence.

- Estimate next year’s net profit before your own pay

- Decide how much you need to take home as personal income

- Ask whether outside investors or complex equity are likely in the next three years

- Roughly price the tax difference between remaining as you are and becoming an S or C corporation, using your tax pro or a planning tool

- Factor in California franchise tax and compliance costs, including payroll and bookkeeping support

If profit is high, your plans are simple, and you do not need preferred stock, S corporation status usually wins. If you are seeking funding or building an exit through stock sale, C corporation status may be the right bet despite double taxation. The key is to decide deliberately, not by accident.

For many owners, a one time deep dive followed by annual check ins is enough to stay on the right side of the am i s corp or c corp question as profit, headcount, and goals evolve.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Can I switch from C corporation to S corporation later

Yes, many businesses start as C corporations and later elect S status, especially when they move from heavy reinvestment to a more mature, cash generating phase. You must meet the eligibility rules and file Form 2553 on time. If the company has appreciated assets when you switch, there may be built in gains tax exposure if those assets are sold within a recognition period, so the timing deserves careful modeling.

Is an LLC taxed the same as an S corporation

No. By default a single member LLC is disregarded for federal tax and a multi member LLC is taxed as a partnership. Both can elect S corporation status so that income passes through on a Schedule K 1 but is treated under S corporation rules, including the reasonable salary requirement. The legal wrapper and the tax classification are related but separate decisions.

Does an S corporation always save money over an LLC taxed as a sole proprietorship

Not always. At low profit levels, the cost of payroll, bookkeeping, and tax prep can eat up the savings. There is also extra complexity around shareholder basis, distributions, and fringe benefit rules. That is why we rarely suggest S corporation elections for owners with less than roughly 60,000 to 80,000 dollars of consistent annual profit.

Will choosing the wrong entity trigger an audit

Simply being a C or S corporation does not by itself trigger an audit. What draws attention is mismatched behavior, such as very low officer wages in a profitable S corporation or large personal expenses booked as deductions. Staying inside the lines and documenting your decisions does far more to reduce audit risk than chasing perfect entity status.

Top 3 Takeaways For Busy Owners

- S corporations usually favor owners who pull most profit out as pay and distributions, while C corporations can work when profit is reinvested or institutional investors are involved.

- In California, the 1.5 percent S corporation tax is often kinder than the 8.84 percent C corporation tax, especially for six figure service businesses.

- The real savings come from matching entity choice with reasonable salary, clean books, and timely elections, not from hoping the label alone will fix your tax bill.

The IRS is not hiding better entity choices; it simply lets owners donate extra tax when they drift into a structure that does not match their goals.

Book Your Tax Strategy Session

If you are still debating am i s corp or c corp and you want a clear, number driven answer for your specific situation, it is time to sit down with a strategist. We will model your next three to five years, quantify the tax impact of each option, and give you a concrete implementation plan so you are not guessing. Click here to book your consultation now.