Most business owners have been told that electing S Corp status is always the smart move. Skip the C Corp, avoid double taxation, take the pass-through savings, and never look back. That advice is repeated so often it has become gospel. The problem is that it is wrong for a growing number of profitable, ambitious business owners in 2026. Understanding the real advantages of c corp vs s corp can be the difference between overpaying tens of thousands in taxes and building a genuinely tax-efficient company.

This is not a case of one entity being universally better. It is a case of matching your entity to your actual plans, your profit level, your reinvestment strategy, and your long-term exit goals. Below, we break down exactly when a C Corp beats an S Corp, when the reverse is true, and how to decide with confidence.

Quick Answer: C Corp vs S Corp in One Paragraph

The core advantages of c corp vs s corp come down to how profits are taxed and what you plan to do with them. A C Corp is a separate taxpaying entity that pays a flat 21% federal corporate tax and can retain earnings, offer richer fringe benefits, and attract outside investors. An S Corp is a pass-through entity where profits flow to your personal return, avoiding a corporate-level tax but limiting who can own it and how it raises capital. If you reinvest heavily, want venture funding, or plan to hold profits inside the company, the C Corp often wins. If you distribute most profit to yourself and want to minimize self-employment tax on a mid-range income, the S Corp usually wins.

Key Takeaway: The right choice depends on your profit level, reinvestment plans, and exit strategy, not on a one-size-fits-all rule.

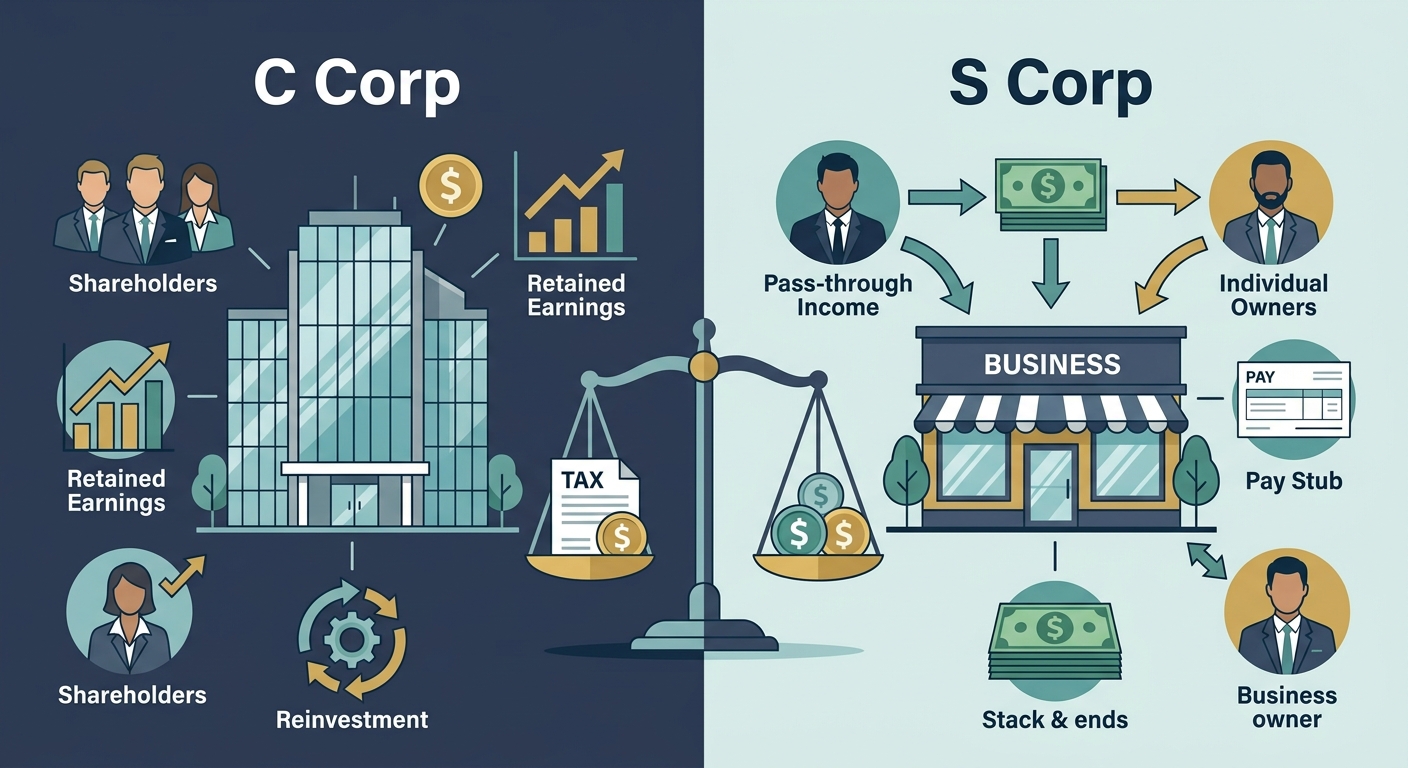

What Is a C Corp and What Is an S Corp?

Before comparing them, let’s define both in plain English so the rest of this guide makes sense.

C Corporation Defined

A C Corporation (C Corp) is a legal business structure taxed as its own entity under Subchapter C of the Internal Revenue Code. It files its own return using Form 1120 and pays a flat 21% federal corporate income tax on profits. When those profits are distributed to owners as dividends, the owners pay tax again on their personal returns. This is the famous “double taxation” you have heard about. The tradeoff is that a C Corp can have unlimited shareholders, multiple stock classes, and foreign or institutional owners.

S Corporation Defined

An S Corporation (S Corp) is not a different kind of company. It is a tax election that an LLC or corporation makes by filing Form 2553. An S Corp passes its income directly through to the owners’ personal returns, reported on Schedule K-1, so there is no separate corporate income tax. The catch: it is limited to 100 shareholders, all must be U.S. individuals (with narrow exceptions), and only one class of stock is allowed. For a deeper walkthrough of how this plays out for California owners, our complete guide to S Corp tax strategy lays out the mechanics step by step.

S Corp vs C Corp: Key Differences at a Glance

| Factor | C Corp | S Corp |

|---|---|---|

| Federal tax on profits | Flat 21% at entity level | Passed through to owner |

| Double taxation | Yes, on dividends | No |

| Ownership limits | Unlimited, any type | 100 U.S. individuals max |

| Stock classes | Multiple allowed | One class only |

| Retaining earnings | Easy and tax-efficient | Taxed to owner even if retained |

| Outside investors | Attractive to VCs | Difficult to fund |

The Real Advantages of C Corp vs S Corp for Growing Businesses

Here is where the conventional wisdom breaks down. For certain business owners, the advantages of c corp vs s corp are substantial and often overlooked by advisors who default to the S Corp election. Let’s walk through the five strongest C Corp advantages with real numbers.

1. Retaining Earnings at a Lower Tax Rate

An S Corp owner is taxed on all profit, whether or not the money leaves the company. If your business earns $300,000 and you leave $150,000 inside to fund growth, you still pay personal tax on the full $300,000, potentially at a 32% or 35% marginal rate. A C Corp pays just 21% on retained profit. On that $150,000 held inside the company, a C Corp owner keeps roughly $19,500 more than an S Corp owner who reinvests the same amount. For a company scaling hard, that reinvestment gap compounds fast.

2. Richer, Fully Deductible Fringe Benefits

C Corps can deduct a wider range of owner benefits that S Corps cannot fully deduct for shareholders owning more than 2%. This includes health insurance structured through the company, certain group-term life insurance, and more generous medical reimbursement plans. A C Corp owner paying $18,000 a year in family health premiums gets a clean corporate deduction, while a 2%-plus S Corp shareholder must run those premiums through wages first, creating extra payroll complexity.

3. Qualified Small Business Stock (QSBS) Exclusion

This is the advantage almost no one talks about. Under Section 1202 of the tax code, shareholders of a qualifying C Corp can potentially exclude up to 100% of capital gains on the sale of their stock, subject to limits. This benefit is only available to C Corp stock. An S Corp owner selling a company simply does not qualify. For a founder who builds and eventually sells, this can mean excluding millions in gain from tax, a benefit an S Corp structure forecloses entirely.

Pro Tip: If there is any chance you will sell your company down the road, model the QSBS exclusion before defaulting to an S Corp. It is one of the most powerful exit-planning tools in the code.

4. Attracting Investors and Issuing Multiple Stock Classes

Venture capital funds, private equity firms, and many institutional investors cannot or will not invest in S Corps because of the single-class-of-stock and shareholder restrictions. If you plan to raise outside money, a C Corp is effectively mandatory. The ability to issue preferred stock, common stock, and options gives you the flexibility investors expect.

5. Predictable, Flat Corporate Rate

The 21% flat federal rate is simple and predictable. High-income S Corp owners can face marginal rates well above that on pass-through income. For a profitable business owner whose personal bracket sits at 35% or 37%, keeping profit inside a C Corp at 21% is a meaningful planning lever, especially when paired with a smart distribution strategy. If you want to run your own numbers, a small business tax calculator can help you sketch out the difference before you commit.

KDA Case Study: The Reinvesting Business Owner

Marcus, a 41-year-old founder, runs a software services firm structured as an S Corp. His company netted $420,000 in profit, and he was reinvesting roughly $200,000 of it into new hires and product development. Because his S Corp passed all $420,000 through to his personal return, he was paying tax at a 35% marginal rate on money he never took home. His effective tax on the reinvested portion alone was costing him around $70,000 a year.

When Marcus came to KDA, we modeled a conversion to C Corp status paired with a reasonable salary and a disciplined retained-earnings plan. By holding the $200,000 of reinvested profit inside a C Corp at 21% instead of exposing it to his 35% personal rate, we projected a first-year federal tax reduction of roughly $28,000. We also positioned his stock to potentially qualify for the Section 1202 QSBS exclusion for a future sale.

Marcus paid $6,500 for the entity analysis, restructuring, and first-year implementation. Against $28,000 in first-year savings, that is a 4.3x first-year return, before counting the long-term QSBS upside. The lesson: the advantages of c corp vs s corp are not theoretical for a reinvesting owner. They are real dollars.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

When the S Corp Still Wins

To be fair and accurate, the S Corp remains the better choice for a large share of business owners. Ignoring that would be malpractice. Here is where the S Corp advantages hold up.

Self-Employment Tax Savings on Mid-Range Profit

The classic S Corp benefit is splitting income between a reasonable salary and distributions. Only the salary portion is subject to the 15.3% self-employment and payroll tax. Consider an owner netting $120,000. As a sole proprietor or standard LLC, nearly all of that is exposed to self-employment tax. As an S Corp paying a reasonable $70,000 salary and taking $50,000 in distributions, the $50,000 avoids the 15.3% tax, saving roughly $7,650 a year. This is where our tax planning services often deliver immediate wins for owners in the $80,000 to $250,000 profit range.

No Double Taxation on Distributions

Because S Corp profits are not taxed at the entity level, distributing money to yourself does not trigger a second layer of tax the way C Corp dividends do. For an owner who wants to pull most profit out each year rather than reinvest, the S Corp is simpler and cheaper.

Decision Framework: Which Entity Fits You?

Lean toward a C Corp if:

- You reinvest most of your profit back into growth

- You plan to raise venture or institutional capital

- You may sell the company and want QSBS treatment

- You want the richest possible fringe benefit deductions

Lean toward an S Corp if:

- Your profit is roughly $80,000 to $300,000 and mostly distributed

- You want to minimize self-employment tax now

- You have a small number of U.S. individual owners

- Simplicity and a single layer of tax matter most

Red Flags and Common Mistakes When Choosing an Entity

The wrong entity election can quietly drain profit for years. These are the mistakes we see most often.

Red Flag Alert: Electing S Corp Purely to Follow the Crowd

Many owners elect S Corp status because a peer or generic online article told them to, without modeling their reinvestment plans. If you are plowing profit back into the business, the S Corp can actually increase your tax bill compared to a C Corp because you are taxed on money you never received. Always model both before electing.

Red Flag Alert: Unreasonably Low S Corp Salary

The IRS scrutinizes S Corp owners who pay themselves a tiny salary to dodge payroll tax. Paying yourself $20,000 while taking $180,000 in distributions is an audit magnet. The salary must be reasonable for your role and industry, as the IRS explains in its guidance on S corporation compensation.

What Happens If You Choose Wrong?

If you elect S Corp status and later realize a C Corp fits better, revoking the election has consequences, including a potential five-year wait before you can re-elect S status. Converting a C Corp with appreciated assets to an S Corp can trigger built-in gains tax. These are not casual switches, which is exactly why the initial analysis matters so much.

California-Specific Considerations

California adds a layer most national articles ignore. California imposes a 1.5% franchise tax on S Corp net income (with an $800 minimum), and C Corps face an 8.84% state corporate tax. That means the federal-only math never tells the whole story for California owners. A profitable California C Corp must weigh the combined federal 21% plus state 8.84% against the S Corp’s pass-through treatment and 1.5% franchise tax. This is where local expertise changes the answer, and where a national rule of thumb can cost you real money.

This information is current as of 7/18/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Can I switch from an S Corp to a C Corp?

Yes. You can revoke your S Corp election and become a C Corp, but timing and consequences matter. The revocation generally takes effect at the start of a tax year if filed by the deadline, and once revoked, you typically must wait five years before re-electing S status without IRS consent. Model the full impact before acting.

Does a C Corp always mean double taxation?

No. Double taxation only occurs on profits distributed as dividends. If you retain earnings inside the company for growth or pay yourself a reasonable salary, you can significantly reduce or defer the second layer of tax. Strategic distribution planning is what makes the C Corp work.

Which entity is better for a business making $500,000 in profit?

It depends on what you do with the profit. If you distribute most of it to yourself, an S Corp usually wins by avoiding entity-level tax. If you reinvest heavily or plan a future sale, the C Corp advantages, including the flat 21% rate and potential QSBS exclusion, often make it the smarter structure. Only a side-by-side model gives a reliable answer.

The Bottom Line on C Corp vs S Corp

The advantages of c corp vs s corp are not about which entity is “best.” They are about which entity fits your profit level, your reinvestment strategy, and your exit plan. Reinvesting founders and future sellers frequently leave serious money on the table by defaulting to an S Corp, while owners who distribute most of their profit often benefit most from S Corp treatment. The only wrong move is choosing without running the numbers.

Mic drop: The most expensive tax mistake is not the deduction you missed. It is the entity you never questioned.

Book Your Entity Strategy Session

If you are reinvesting profit, planning a raise, or eyeing an eventual sale, your entity choice could be quietly costing you thousands every year. Let’s put real numbers on the table and pick the structure that keeps the most money in your business. Book a personalized consultation with our strategy team and get a clear, compliant, custom entity plan. Click here to book your consultation now.