Why Section 179 and MACRS Vehicles Are Where Business Owners Leave the Most Money on the Table

Most small business owners will spend $60,000 on a heavy SUV, write off a few thousand with regular depreciation, and then complain that their tax bill feels unfair. The problem usually is not the vehicle; it is the wrong mix of Section 179 and MACRS, plus a complete misunderstanding of how the rules treat vehicles over 6,000 pounds versus lighter cars.

For the 2024 tax year, the IRS still lets you front-load a significant portion of your vehicle cost if you structure it correctly. The question is not “Can I deduct my vehicle?” The real question is whether you should use Section 179, bonus depreciation, or regular MACRS – and in what combination – to squeeze the most value out of that purchase without creating audit risk or ugly surprises in future years.

Quick Answer

Section 179 lets you deduct up to the full purchase price of qualifying business vehicles in the year you place them in service, subject to annual limits and business-use percentage. MACRS is the standard depreciation system that spreads the deduction over five years for most passenger vehicles and trucks. For many 2024 buyers of heavy SUVs over 6,000 pounds, a blended approach often wins: use Section 179 to accelerate a chunk of the cost, then use bonus depreciation and MACRS on the rest, with careful attention to future business use so you do not trigger depreciation recapture.

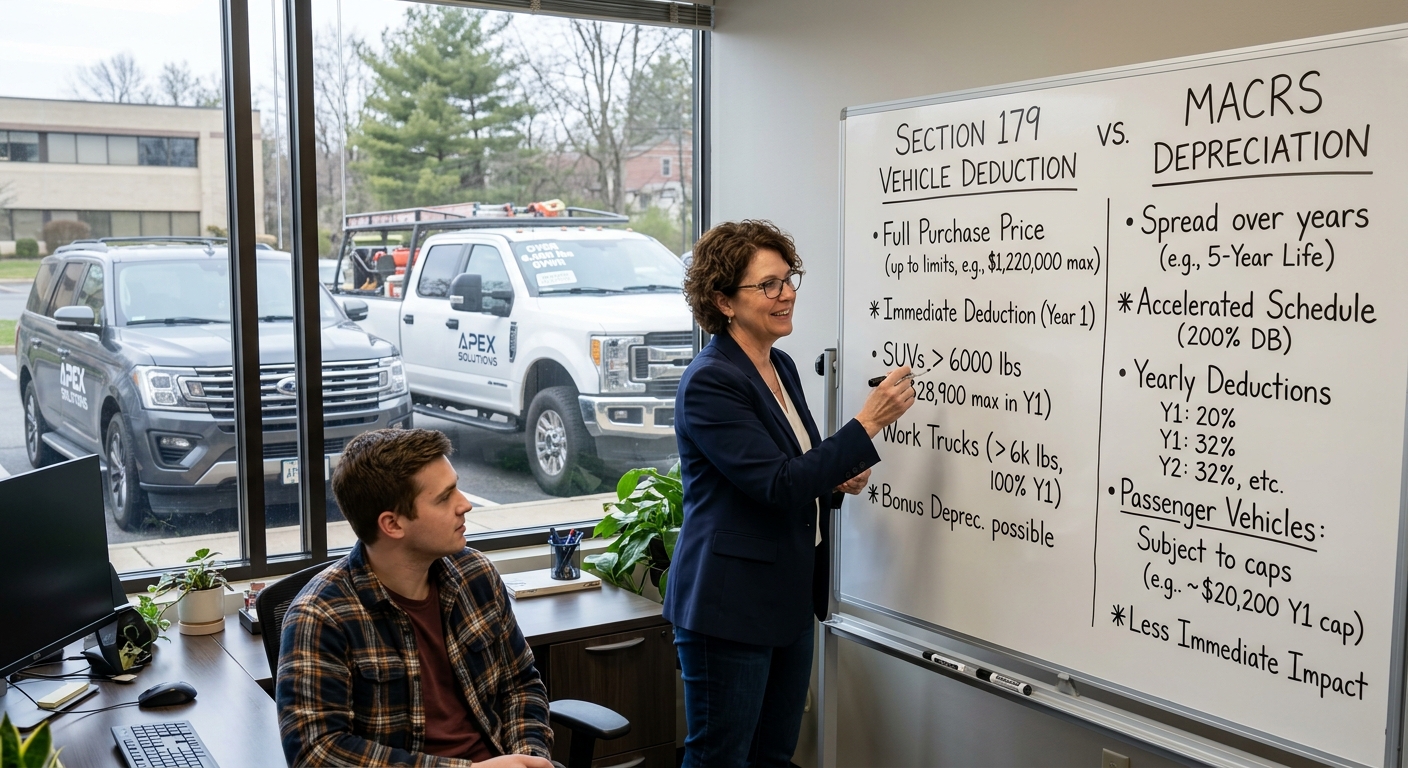

Section 179 Vehicles vs MACRS 2024: The Core Difference

Section 179 vehicles vs MACRS 2024 sounds like a simple either-or choice, but that mindset costs business owners real money. Section 179 is an election to expense qualifying property immediately, while MACRS (Modified Accelerated Cost Recovery System) is the default schedule the IRS gives you to recover the cost over several years. Vehicles are just one category inside these bigger systems.

What Section 179 Does for Your Vehicle

Section 179 allows you to deduct a large portion of the cost of qualifying business equipment, including certain vehicles, in the year you place it in service. For the 2024 tax year, the overall Section 179 limit and phaseout thresholds adjust for inflation, so high-spend businesses can write off millions in equipment if they time purchases correctly. The catch is that passenger vehicles have special caps, while some heavier SUVs and trucks qualify for much more generous treatment. The detailed rules are laid out in IRS Publication 946, which covers how to depreciate property.

Think of Section 179 as an accelerator pedal. If your business has a strong profit year and you want to slash taxable income now, Section 179 can move deductions you would normally take over five years into the current year.

How MACRS Treats Business Vehicles

Under MACRS, most vehicles used for business are five-year property. Instead of one big deduction, you claim a portion of the cost each year based on IRS tables. This can be helpful if your business income is growing steadily and you prefer a predictable deduction instead of a single spike. MACRS becomes especially important if you expect your business to last for many years and want to avoid locking all your tax savings into a single period.

MACRS also interacts with the “luxury auto” limits for lighter vehicles, capping how much depreciation you can claim each year. Heavy vehicles over 6,000 pounds, like many SUVs and work trucks, are treated more favorably, which is why the Section 179 vehicles vs MACRS 2024 discussion focuses so heavily on that weight cutoff.

Red Flag Alert: Business Use Below 50 Percent

If your business use of the vehicle ever drops below 50 percent after you took big Section 179 or bonus depreciation, you may have to recapture (pay back) part of those deductions as income. This is a common trap for real estate agents and consultants who start off driving mostly for business, then gradually shift to more personal use. Proper planning and documentation are nonnegotiable here.

Heavy SUV Over 6,000 Pounds vs Lighter Vehicles

The 6,000-pound gross vehicle weight rating (GVWR) line is where strategy really starts. Many business owners hear about “the 6,000-pound SUV loophole” from friends or social media, but they rarely understand the tradeoffs.

What the 6,000-Pound Threshold Really Means

For 2024, an SUV or truck with a GVWR above 6,000 pounds but below 14,000 pounds may qualify for a large Section 179 deduction that is not subject to the strict “luxury auto” caps that apply to lighter passenger cars. This is why vehicles like certain models of the Chevy Tahoe, Ford Expedition, and many work trucks are so popular with business owners.

Suppose you buy a $75,000 SUV in 2024 used 90 percent for business. Depending on current-year limits, you might be able to expense a large portion of that cost immediately using Section 179, then apply bonus depreciation and MACRS to the remainder. A lighter $45,000 sedan might give you only a fraction of that first-year deduction because it is trapped under luxury auto caps.

When MACRS Alone Makes More Sense

Section 179 is not always the hero. If your business is barely breaking even in 2024 but you expect strong growth in 2025 and 2026, front-loading every deduction into the current year can backfire. In that case, letting MACRS spread the deduction over several years might produce more total tax savings, especially if it keeps you from wasting deductions in a low-tax-rate year.

For some W-2 heavy earners who own side LLCs, it can also help to coordinate vehicle strategy with broader planning like S corporation elections and retirement contributions. Combining Section 179 vehicles vs MACRS 2024 planning with a broader structure review can be worth five figures over a multi-year window.

KDA Case Study: Contractor Uses Vehicle Strategy to Save Five Figures

Consider Diego, a 1099 construction contractor in California with an LLC that cleared $220,000 in profit in 2024. His old pickup was dying, so he bought a new $68,000 heavy-duty truck with a GVWR over 6,000 pounds, used 85 percent for work. Initially, his prior accountant suggested standard MACRS depreciation, which would have produced roughly $13,000 to $14,000 of first-year deductions.

When Diego came to KDA, we reviewed his entire situation. Instead of defaulting to MACRS, we modeled a combination of Section 179 and bonus depreciation tailored to his projected income and California franchise tax exposure. We elected Section 179 on a significant portion of the truck’s cost, then used bonus depreciation for the remainder within safe limits. The result was over $45,000 in first-year deductions tied directly to the truck, cutting his combined federal and state tax bill by approximately $15,000.

Diego paid just under $4,000 for a comprehensive planning engagement and implementation support, yielding a nearly 4x first-year return before even counting ongoing savings from better recordkeeping and mileage tracking going forward.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How to Choose Between Section 179 and MACRS for 2024 Purchases

The right answer rarely comes from a single rule. It comes from comparing scenarios over several tax years and, ideally, over the life of the vehicle. Here is a practical way to think about this choice.

Step 1: Map Your Profits for the Next Three Years

If 2024 will be a banner year, there is a strong case for front-loading deductions with Section 179 and bonus depreciation. If 2024 is soft but 2025 and 2026 will be your big years, MACRS may be more valuable. Remember, a deduction is worth more when you are in a higher tax bracket.

Step 2: Confirm Business Use Above 50 Percent

To qualify for Section 179 on a vehicle, you generally must use it more than 50 percent for business. This is not a guess; the IRS expects you to track mileage carefully and be able to prove your numbers. Using an app that logs trips and lets you categorize them business vs personal is usually the simplest solution. If you are close to the 50 percent line, it is often safer to lean toward MACRS with minimal or no Section 179 to avoid recapture headaches later.

Step 3: Decide How Aggressive You Want to Be

For many California business owners, the conservative strategy combines modest Section 179 with standard MACRS to keep a healthy deduction in future years. More aggressive planners may use Section 179 heavily on a heavy SUV and pair it with other strategies like an S corporation election or advanced retirement planning. For help with entity and compensation planning around your vehicle deductions, some business owners work with specialists who understand how all the pieces fit together.

What the IRS Really Cares About With Vehicle Deductions

The IRS is less concerned with whether you chose Section 179 or MACRS and more focused on three things: business use percentage, documentation, and consistency. If those are strong, you have room to be strategic inside the rules.

Business Use Percentage and Substantiation

According to IRS Publication 463, which covers travel, gift, and car expenses, you must be able to substantiate your mileage and business purpose. That means dates, destinations, and the business reason for the trip, not just a rough estimate at year-end. A 1099 consultant driving 20,000 miles in a year with 14,000 documented as business has a much stronger position than someone who calls it “about 70 percent” with no backup.

Consistency Across Years

Once you place a vehicle in service and start depreciating it, the IRS expects your method to continue unless you have a legitimate reason to change. Abrupt shifts in business-use percentage or method without explanation invite questions. Planning your Section 179 vehicles vs MACRS 2024 strategy up front avoids ugly corrections later.

Red Flag Alert: Mixing Personal and Business Without Care

Commuting from home to a regular office is not business mileage, even if you are answering calls on the way. Confusing commuting with business use is one of the fastest ways to get mileage disallowed in an audit. The same is true for claiming that a family SUV is “100 percent business” with no personal weekend or evening use. The numbers need to pass a common-sense test.

Section 179 vs MACRS for Different Taxpayer Personas

The best strategy changes dramatically depending on whether you are a W-2 employee with a side gig, a full-time 1099 contractor, or a multi-entity real estate investor. Here is how the decision typically looks for each group.

W-2 Employee With Side Business

For W-2 employees, unreimbursed employee vehicle expenses are no longer deductible at the federal level under current rules. The vehicle deduction must run through your side business, such as a Schedule C sole proprietorship or single-member LLC. If that business only nets $10,000 to $15,000 a year, dropping a $60,000 Section 179 deduction onto it is usually a waste; you cannot use what you do not have income to offset.

In this case, taking MACRS depreciation and possibly standard mileage (if more advantageous) may be better. Coordinating this with your overall federal tax picture is crucial. To get deeper help integrating vehicle strategies with other planning, our tax planning services can model different paths before you commit.

Full-Time 1099 Contractor or Consultant

Full-time self-employed professionals with high net income are usually prime candidates for heavy use of Section 179, especially when buying a qualifying SUV or truck over 6,000 pounds. If you are clearing $180,000 or more and facing a combined marginal rate north of 35 percent, a $40,000 immediate deduction can easily translate to $14,000 or more in tax savings for 2024 alone.

Here, the main decisions are timing (Q4 vs early next year), what mix of Section 179 and MACRS to use, and whether you are comfortable with the recordkeeping burden to defend those deductions if the IRS ever asks you to prove them.

Real Estate Investor With Multiple Properties

Real estate investors often overlook vehicle strategy because their focus is on depreciation schedules for buildings, not cars and trucks. Yet a dedicated SUV used for property management, renovations, and site visits can generate meaningful deductions, especially when combined with other real estate tactics. For some investors, it makes sense to coordinate the timing of property improvements, Section 179 vehicles vs MACRS 2024 decisions, and potential cost segregation studies into a single multi-year plan. Many will benefit from tools like a small business tax calculator to preview the combined impact.

Will Section 179 or MACRS Trigger an Audit?

Neither Section 179 nor MACRS automatically triggers an audit. What raises flags is when your deductions are unusually large compared to your income or peers, or when the details do not match what you report elsewhere on your return.

Common Triggers to Avoid

- Claiming 100 percent business use on a luxury SUV with no personal use documented

- Taking the maximum Section 179 deduction in a year where your profit is low or negative

- Switching erratically between actual expenses and standard mileage without clear basis

- Failing to report vehicle-related reimbursements correctly

According to publicly available IRS data, small business and self-employed returns are more likely to be examined when deductions appear disproportionate to income. That does not mean you avoid deductions; it means you take the ones you can support, in the right way, at the right time.

Fast Tax Fact: Section 179 vs MACRS Is Not a One-Time Decision

Many owners treat vehicle expensing as a one-time choice made when they sign the purchase paperwork. In reality, you are choosing a strategy that affects every return filed while you own the vehicle or until it is fully depreciated. The best approach to Section 179 vehicles vs MACRS 2024 weighs:

- Your expected profit over several years

- Your appetite for audit risk

- Your willingness to track mileage in detail

- How vehicles fit into your broader entity and compensation structure

This information is current as of 7/18/2026. Tax laws change frequently. Verify updates with the IRS if you are reading this in a later year.

Will I Still Get Deductions If I Finance the Vehicle?

Yes. Section 179 and MACRS are based on the cost of the vehicle and when you place it in service, not whether you paid in cash. If you finance a $70,000 truck in late 2024 with $5,000 down, you may still be able to deduct a large portion of that $70,000 cost in the first year under Section 179 and bonus depreciation. Your loan payments themselves are not deductible; instead, you deduct depreciation (and interest, if the loan is a qualified business loan).

Can I Change My Mind After Electing Section 179?

Once you make a Section 179 election on a return and it becomes final, changing course is not trivial. You may be able to amend in limited circumstances, but the cleaner approach is to run scenarios before you file so you do not need to unwind anything. That is why smart business owners treat Section 179 vehicles vs MACRS 2024 as part of a larger planning conversation instead of a box to check at tax time.

Bottom Line: Get a Vehicle Plan, Not Just a Purchase

A vehicle can be an outstanding tax tool if you buy the right type of vehicle, document business use carefully, and coordinate Section 179 and MACRS with the rest of your tax strategy. Getting it wrong can produce years of weak deductions and real risk if the IRS ever looks closely at your return.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Book Your Tax Strategy Session

If you are a business owner, contractor, or real estate investor wondering whether your current vehicle setup is costing you thousands of dollars every year, it is time to get answers. Book a personalized consultation with our strategy team and we will review your entity structure, vehicle usage, and deduction options so your Section 179 and MACRS choices support your long-term goals. Click here to book your consultation now.