Many business owners walk into a dealership believing they can write off a six figure SUV in the year they buy it, only to have their tax software or preparer tell them they are capped or disallowed. The good news is that the rules do not always kill the deduction. Used correctly, the section 179 vehicles carryover 2024 rules can keep a big piece of that write off alive for future years instead of losing it forever.

Quick Answer

Section 179 lets you expense qualifying business vehicles in the year you place them in service, subject to income limits, SUV caps, and business use requirements. If Part of your vehicle write off is disallowed in 2024 because of those limits, you usually do not lose it. Instead, the unused portion becomes a Section 179 carryover that you can deduct in later years when you have enough taxable business income, as long as you keep using the vehicle more than 50 percent for business.

How Section 179 Works For Heavy Vehicles In 2024

Before you can use any Section 179 vehicles carryover 2024 strategy, you need to understand the basic mechanics of the rule. Section 179 is the part of the Internal Revenue Code that lets you expense, rather than slowly depreciate, qualifying business equipment. Vehicles used in your trade or business qualify, but the IRS puts extra restrictions on anything you can drive home.

For 2024, the overall Section 179 limit is over seven figures for most small businesses, and it starts phasing out once you place a few million dollars of assets in service. The exact numbers change every year for inflation, which is why the IRS publishes them in IRS Publication 946 and explains how to report them on Form 4562.

Vehicles are a special animal. Heavy SUVs, pickups, and vans with a gross vehicle weight rating above 6,000 pounds but below 14,000 pounds can qualify for an expensing amount that is much higher than the regular luxury auto limits, but still not unlimited. The IRS caps the Section 179 deduction for these vehicles at a specific dollar amount that typically lands in the high 20,000 to low 30,000 range each year. The exact figure for your filing year is in Publication 946 and Publication 463 for vehicle expenses.

If you are an LLC or S corporation owner, this is often where things get confusing, because your business level deduction is limited by your taxable income from the business. Many business owners see a six figure purchase price and assume they get the same size deduction. In reality, Section 179 for vehicles is a mix of purchase price, special SUV caps, business use percentage, and an income limit. Any part that gets blocked by those tests is where the carryover can come into play.

Where Section 179 Vehicle Carryover Comes From

The code is clear that Section 179 is limited by your taxable business income. In plain English, you cannot use Section 179 to create or deepen a net loss from your active trades or businesses. If your vehicle purchase pushes the deduction above your income, the excess portion is a disallowed Section 179 amount for that year. Publication 946 describes this as a “carryover of disallowed deduction.”

Here is how the math might look. Suppose your single member LLC generates $80,000 of net profit before any vehicle write off. You purchase a qualifying SUV for $90,000 that you use 90 percent for business. The Section 179 SUV limit for the year lets you claim, for example, $30,000 multiplied by your 90 percent business use, so $27,000 is potentially expensable instead of regular depreciation.

However, Section 179 also says your total 179 deduction across all assets cannot exceed your $80,000 of taxable business income. If you have already used $70,000 of 179 expensing on equipment, you only have $10,000 of income capacity left. The remaining $17,000 of potential vehicle expensing becomes part of your Section 179 vehicles carryover 2024 calculation. It does not vanish. It sits in a carryover bucket you can use against future business income.

This carryover is tracked on Form 4562 and in your depreciation schedules. In later years, when your taxable business income increases, you apply the carryover amount before you calculate any new Section 179 deduction. The IRS explains the ordering rules and examples in Publication 946, which is essential reading if you are self preparing.

KDA Case Study: Contractor Rescues A Blocked SUV Deduction

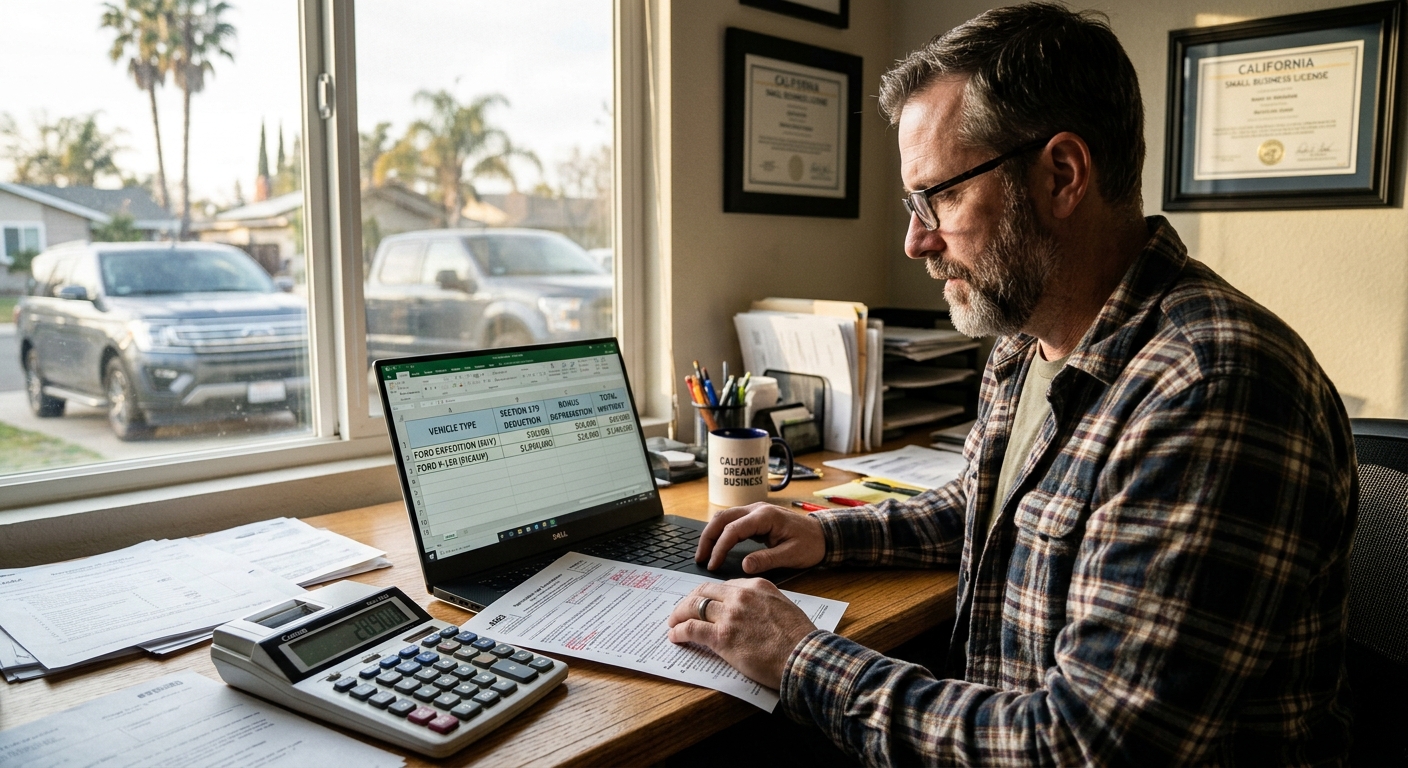

Consider a real world style case we see often. Carlos runs a California construction LLC taxed as an S corporation. In late 2024 he buys a $95,000 heavy pickup with a gross vehicle weight rating over 6,000 pounds so he can haul tools and crews to job sites. His business use is 85 percent based on mileage logs. His S corporation shows $120,000 of ordinary income before vehicle write offs.

Carlos originally tried to expense the truck entirely using a mix of Section 179 and bonus depreciation and expected to show almost no income. His prior preparer treated the truck as fully deductible, creating a large pass through loss on his K 1. The problem: the 179 SUV cap and the taxable income limit were ignored, and the bonus depreciation calculation did not account for basis already used by the attempted 179 deduction.

When Carlos came to KDA, we rebuilt the fixed asset schedule correctly. We applied the SUV specific Section 179 limit for 2024 times his 85 percent business use. That gave him a first year 179 deduction of roughly $25,000. Because of other 179 assets, only $15,000 of that fit under the income cap. The $10,000 excess went into a Section 179 vehicles carryover 2024 bucket to use against 2025 income.

Next we layered in bonus depreciation on the remaining vehicle basis and regular MACRS depreciation on any leftover amount. After running the numbers, Carlos still reduced his 2024 S corporation income from $120,000 to around $40,000, saving roughly $24,000 in combined federal and California tax. In 2025, when the business had another strong year, we applied the $10,000 carryover plus the second year depreciation, trimming another $6,000 in tax. Over two years, the total tax savings exceeded $30,000 on a $3,500 tax planning fee for this and other issues, an almost 9 times return.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How To Calculate Your Section 179 Vehicle Carryover Step By Step

You do not need to guess at your carryover. You can walk through it methodically, using Form 4562 and a simple worksheet. Here is a practical sequence for a business owner with one or two vehicles and some equipment purchases.

Step 1: Confirm The Vehicle Qualifies

Check the manufacturer sticker for gross vehicle weight rating. If it is above 6,000 pounds and below 14,000 pounds, used more than 50 percent for business, and not a vehicle designed primarily for personal use like many typical SUVs, it likely qualifies for the higher Section 179 cap rather than the standard luxury auto limits. Publication 463 gives examples of qualifying and non qualifying vehicles.

Step 2: Determine Business Use Percentage

Track total miles and business miles. Divide business miles by total miles to get your business use percentage. If you come in at 70 percent business and 30 percent personal, only 70 percent of the Section 179 cap and the vehicle cost is relevant. Drop below 50 percent business use and your vehicle is not eligible for Section 179 at all, which can also trigger recapture of prior deductions.

Step 3: Apply The SUV Section 179 Limit

Look up the specific SUV limit for your tax year in Publication 946. Multiply that cap by your business use percentage. That gives you the maximum Section 179 you can claim on that vehicle in 2024, before factoring in income limits. If your vehicle cost times business use is below that figure, you are capped instead by actual cost.

Step 4: Apply The Taxable Income Limit

Next, calculate your tentative taxable income from all active trades or businesses before Section 179. This includes S corporation wages from your own company, Schedule C income, and certain rental activities if they rise to the level of a trade or business. Compare your total Section 179 across all assets to that income number. Any excess is disallowed this year and becomes part of your Section 179 vehicles carryover 2024 and other 179 carryovers.

Step 5: Track And Use The Carryover In Later Years

Disallowed amounts do not just float in space. Track them on the carryover line of Form 4562 and in your depreciation schedules. In 2025 and later years, you start with your prior year carryover and apply it against current year taxable income before you claim any new Section 179 deductions. A good bookkeeping and tax system, or working with professionals through our tax planning services, can keep this straight.

If you want to sanity check how much tax impact that carryover might have as your business profit changes, plug your expected income into this small business tax calculator to see how much additional deduction could save you next year.

Red Flag Alert: Mistakes That Kill Your Vehicle Deduction

Heavy vehicles draw attention when the numbers do not line up. The IRS has seen every variation of the “I bought a G Wagon so I get a $100,000 write off” story. Several common mistakes either destroy the Section 179 deduction completely or turn your potential Section 179 vehicles carryover 2024 into a recapture nightmare.

Claiming 100 Percent Business Use Without Support

Claiming you never once use an SUV or pickup for personal errands is a hard sell. If you want to be aggressive, you must have bulletproof mileage logs and a business structure that makes personal use truly rare. For most owners, a realistic 70 to 90 percent business use backed by logs is safer and still powerful.

Dropping Below 50 Percent Business Use Later

Section 179 requires more than 50 percent business use not just in the first year, but for as long as you are benefiting from the deduction. If your business shrinks or your driving pattern changes and you start using the vehicle mainly for personal reasons, the IRS can require you to recapture part of the prior 179 deduction as ordinary income. That includes amounts that came from your Section 179 vehicles carryover 2024 bucket.

Ignoring The Ordering Rules With Bonus Depreciation

In recent years, generous bonus depreciation has overlapped with Section 179. Many owners layered them in the wrong order. Section 179 is applied first, limited by income and SUV caps. Bonus depreciation then applies to the remaining basis. Getting this wrong can distort both current deductions and future carryover. According to IRS guidance, you also need to apply any carryover before claiming new Section 179, then compute bonus depreciation on whatever basis remains.

These mistakes are exactly why high income owners with complex vehicle and equipment purchases tend to benefit from proactive planning. Our team frequently pairs Section 179 and bonus depreciation analysis with broader S corporation salary and distribution planning. If you are restructuring your entity or officer compensation, it is worth reviewing our complete S corp tax strategy guide for California owners and then coordinating how your vehicle strategy fits into that bigger picture.

Will Section 179 Vehicle Carryovers Help You If You Are An S Corp Owner

Many California entrepreneurs operate through S corporations, which changes how Section 179 vehicles carryover 2024 amounts behave. The corporation itself makes the Section 179 election and reports allowed and disallowed amounts on Form 4562. The allowed portion then flows through to your personal return on the Schedule K 1, where it can further interact with basis and at risk limitations.

Here is the nuance. The corporate level income limit applies first. If your S corporation has only $60,000 of taxable income and tries to claim $100,000 of Section 179 across vehicles and equipment, only $60,000 is allowed. The extra $40,000 is a carryover at the corporate level. It does not appear on your personal return yet. In later years when corporate income increases, the carryover can finally be used and passed through.

At the shareholder level, you then need enough stock and loan basis to absorb the pass through deduction, and your personal return needs enough aggregate business income so that passive loss rules or at risk rules do not block it. This is where a vehicle strategy must be synced with your overall S corporation planning, including reasonable salary, shareholder loans, and distributions. Coordinating those moving parts is exactly the kind of work we do for growth minded owners looking to keep more of their profit instead of sending it to Sacramento and Washington.

What If You Sell Or Trade The Vehicle Before Using The Carryover

A natural question once you understand Section 179 vehicles carryover 2024 rules is what happens if you dispose of the vehicle before the carryover is fully used. The short answer is that you do not get to keep the unused Section 179 bucket. When you sell, trade, or otherwise dispose of the vehicle, you calculate gain or loss based on your adjusted basis. The carryover that was never used simply reduces that basis.

In practice, this often means more of your sale price is treated as taxable gain, especially if you sell the vehicle while it still has high market value. If you hold the vehicle long enough that its value falls below your adjusted basis, you may instead recognize a deductible loss. Either way, the tax outcome can be very different from what you expected when you first claimed or planned the deduction.

This is another area where timing matters. Sometimes waiting an extra year to trade in a truck lets you use up a remaining Section 179 vehicles carryover 2024 amount against strong business income, then dispose of the vehicle when its value has declined, hitting two different tax years in a favorable way. Other times, selling sooner and triggering gain while you are in a temporarily low tax bracket is better. There is no one size fits all answer, which is why modeling the scenarios with a strategist can be so valuable.

Will This Strategy Trigger An Audit

Any time you are taking large deductions on movable assets with personal use potential, you should think like an auditor. The IRS is not allergic to Section 179 vehicles carryover 2024 claims, but it does look closely at patterns that suggest abuse, such as multiple high end SUVs expensed in quick succession with claimed 100 percent business use.

To stay on solid ground, focus on documentation and reasonableness. Maintain contemporaneous mileage logs, keep purchase and financing documents, and document the business purpose for the vehicle, especially if it is not obviously a work truck. Make sure your personal vehicle situation supports the story. If your only car is a 7,000 pound luxury SUV and you claim it is purely a business asset, that will raise more questions than if you also own a modest personal car for non business driving.

Remember that the IRS publishes detailed rules for vehicle deductions in Publication 463, including examples of what it views as acceptable recordkeeping. Aligning your habits with those expectations goes a long way toward keeping your Section 179 deduction and any related carryover intact.

Key Takeaways For 2024 Vehicle Buyers

If you are considering a heavy SUV, pickup, or van for your business, do not wait until tax time to think about the write off. The best Section 179 vehicles carryover 2024 outcomes happen when you plan the purchase amount, timing, and financing alongside your expected profit for the next few years.

- Section 179 can offset a large portion of a qualifying vehicle cost in the first year, but SUV caps and income limits may push part of it into a carryover bucket instead of wiping out your tax bill immediately.

- Carryover amounts are not lost. They can reduce future year tax as long as you keep business use above 50 percent and track them correctly on Form 4562.

- S corporation owners need to think at both the corporate and shareholder level, coordinating vehicle deductions with basis, salary, and distribution planning.

- Poor documentation, unrealistic business use claims, and ignoring ordering rules with bonus depreciation are what actually put you on the IRS radar, not the mere fact that you used Section 179.

Pro Tip: The smartest vehicle deductions usually come out of a broader tax plan that also addresses your entity structure, how you pay yourself, and how you handle other big purchases. Treat the vehicle as one piece of a multi year strategy instead of a one time trick.

The IRS is not hiding these write offs. They are in plain view in IRS Publication 946 and Publication 463. You just were not taught how to line them up with your actual business income and cash flow.

This Information Has A Shelf Life

This information is current as of 7/1/2026. Tax laws change frequently. Verify updates with the IRS or the California Franchise Tax Board if you are reading this in a later year, especially the precise SUV dollar caps, bonus depreciation percentages, and Section 179 income limits for your filing year.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Book Your Vehicle Tax Strategy Session

If you are not sure whether your current or planned vehicle purchases are optimized under the Section 179 vehicles carryover 2024 rules, do not guess. A wrong move can cost you five figures in tax or trigger avoidable recapture later. A right move can turn the same truck or SUV into a powerful multi year tax tool.

If you want help matching your vehicle strategy to your S corporation or LLC structure, projected income, and California specific rules, our team is ready to dig in. Book a personalized consultation with our strategy team and leave with a clear, written plan for how to handle your next vehicle purchase and existing carryovers. Click here to book your consultation now.