Most small business owners pick a corporation type based on something they heard in a Facebook group, then discover later that choice is quietly draining five figures in taxes every year.

If you own an LLC, already incorporated, or are planning to launch a business in 2025 or 2026, you cannot afford to guess on structure. You need to understand **whats a c corp and s corp** in plain English, what each one really does to your tax bill, and when the fancy-sounding option is actually the wrong move.

Quick Answer

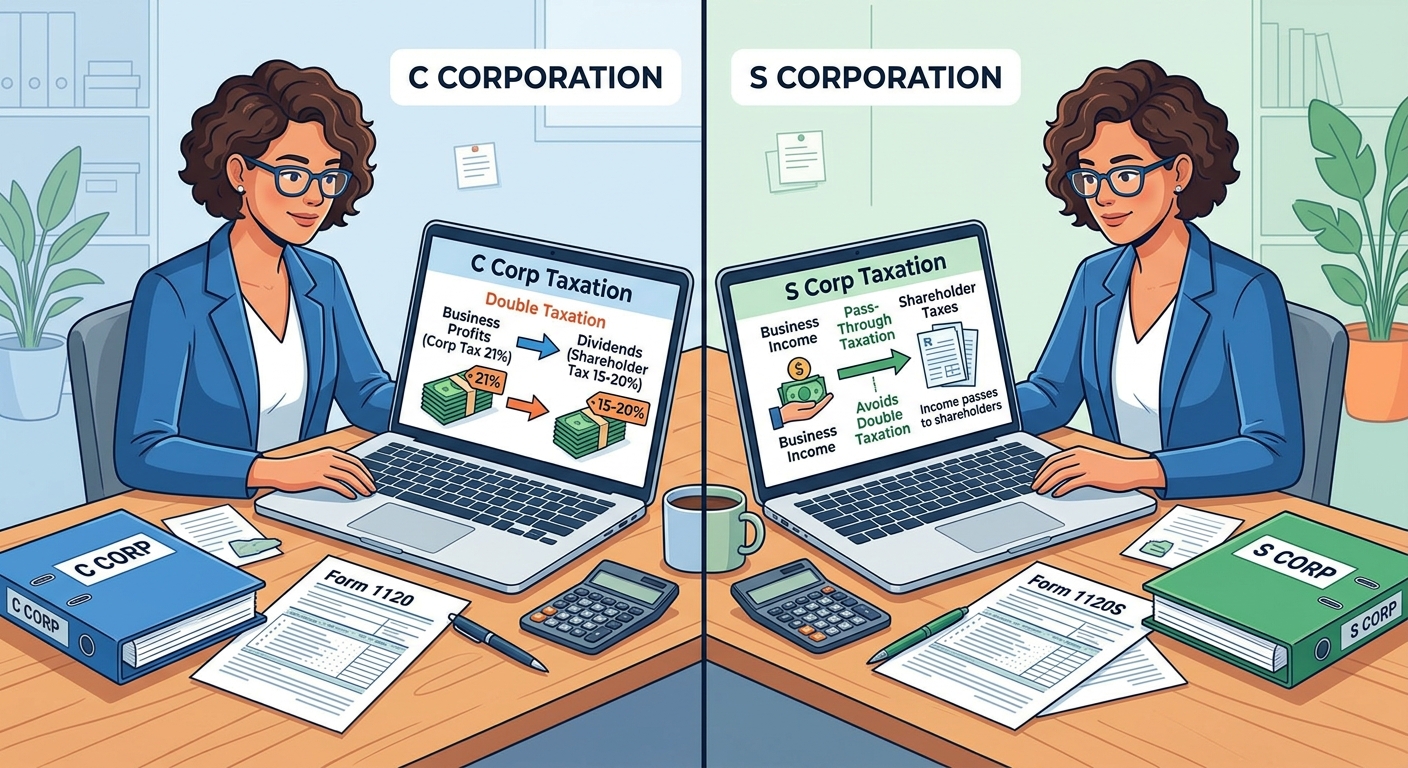

A C corporation is a separate taxpayer that files its own return and pays a flat federal tax (currently 21 percent) on profits using Form 1120. When owners take money out as dividends, they pay personal tax again. That is classic double taxation. An S corporation is a pass through entity that files Form 1120S; profits generally skip corporate tax and flow to the owners personal returns once, but owners working in the business must take a reasonable W 2 salary before pulling out extra profit as distributions.

This information is current as of 6/28/2026. Tax laws change regularly, so confirm details with the IRS or a professional if you are reading it later.

What We Cover

- Clear definitions of C corporations and S corporations

- How each structure really gets taxed, with numbers

- Who should lean C corp and who should lean S corp

- Common mistakes that trigger IRS problems

- A case study showing how the right call creates real savings

- How to decide your next step without overcomplicating it

Understanding Whats a C Corp and S Corp Without Legal Jargon

Start with the basics. Both C corporations and S corporations sit on top of some underlying legal entity, usually a corporation or an LLC organized at the state level. The C or S label is about how the IRS treats that entity for federal income tax, not what your Secretary of State records say.

What a C Corporation Really Is

A C corporation is the default tax treatment for a standard corporation. It is its own taxpayer. It earns income, claims deductions, and pays corporate income tax on its net profit. The flat federal rate has been 21 percent in recent years, with state corporate tax added on top in places like California.

Example: A tech startup in California has $500,000 of revenue and $350,000 in deductible expenses, leaving $150,000 of profit inside the C corporation.

- Federal corporate tax at 21 percent: $31,500

- Assume roughly 8 percent state corporate tax: about $12,000

- Combined corporate level income tax: around $43,500

If the corporation then pays a $50,000 dividend to its owner, that $50,000 shows up on the owner’s personal return and gets taxed again at dividend rates. That is the second layer of tax.

What an S Corporation Really Is

An S corporation is not a separate type of legal entity. It is a tax election that turns a qualifying corporation or LLC into a pass through for federal income tax. The S corporation usually pays no federal income tax itself. Instead it files an informational return on Form 1120S, issues each owner a Schedule K 1, and owners report their share of profit on their personal returns.

The crucial twist: Any owner who actually works in the business must be treated as an employee receiving a reasonable salary reported on Form W 2. That salary is subject to payroll taxes. Remaining profit can usually be distributed free of self employment tax, which is where much of the savings comes from for profitable service businesses.

How C Corp And S Corp Taxation Differs In Real Dollars

To see the real stakes you need to move beyond definitions and look at after tax cash in your pocket. Below is a simple side by side scenario for a single owner consulting business that could be taxed either way.

Scenario Setup

Assume the business earns $250,000 in net profit before any owner salary. The owner lives in a high tax state and is already in the 24 percent federal bracket on other income.

C Corporation Outcome

- Business reports $250,000 profit on Form 1120.

- Federal corporate tax at 21 percent: $52,500.

- Assume state corporate tax of 8 percent: $20,000.

- After tax profit left in the corporation: $177,500.

- Corporation pays out $150,000 as a dividend.

- Owner pays, say, 15 percent qualified dividend tax federal plus state tax; assume total 25 percent on that dividend: $37,500.

- Owner keeps about $112,500 after the second layer of tax.

Combined, the IRS and state took roughly $72,500 on that $150,000 distribution plus $23,000 left in the company for future use. There can be reasons to accept this, but you need to know what you are paying for.

S Corporation Outcome

- Owner sets a reasonable salary of $120,000 based on market rates.

- Payroll taxes (employer plus employee side) on $120,000 are roughly 15.3 percent up to the Social Security wage base plus Medicare above that. Ballpark: $18,000 combined.

- Remaining business profit after salary and payroll tax is around $112,000.

- That $112,000 passes through to the owner’s personal return on Schedule K 1, subject to income tax but generally not self employment tax.

- Owner may also qualify for a Qualified Business Income deduction on part of that profit under IRS Publication 535, depending on income level and type of business.

Compared to running the same business as a C corporation, an S corporation can easily trim $10,000 to $25,000 per year in combined payroll and income taxes for a profitable solo or small team service business, as long as salary is chosen correctly and the entity stays compliant.

Why Most Business Owners Misunderstand C Corp Versus S Corp

The internet is full of half right advice about C corporations and S corporations, especially for LLC owners and online entrepreneurs. Three dangerous myths show up over and over.

Myth 1: C Corporations Are Always Bad Because of Double Taxation

Double taxation is real, but it does not automatically make C corporations the loser. C corporations can reinvest profits without paying dividends, can sometimes access more flexible employee benefit plans, and can be attractive for startups expecting outside investors or eventual sale of stock. They also open the door to the Qualified Small Business Stock rules for some companies, which can wipe out federal tax on a big chunk of stock sale gain if conditions are met.

Myth 2: S Corporations Are Magic Tax Shelters

S corporations are powerful, but the IRS has decades of audit experience tearing apart setups with artificially low or zero owner salaries. If your S corporation pays you $30,000 in wages while you pull out $200,000 in distributions, expect questions. The reasonable compensation standard is enforced using market data and facts about your role.

Myth 3: You Can Decide Later And It Will Be Fine

Waiting often costs money. S corporation elections generally must be filed timely, and late elections can create messy cleanup scenarios. C corporation status can lead to trapped earnings or built in gains tax if you try to unwind at the wrong time. Structure is not a line you casually move back and forth over every year.

KDA Case Study: California Consultant Choosing Between C Corp And S Corp

Consider a real client pattern we see often. Maria is a self employed marketing consultant in California. She started as a Schedule C sole proprietor, then formed an LLC when she crossed $150,000 in annual profit. Her friend told her that investors prefer C corporations, so her attorney converted the LLC to a California corporation taxed as a C corp “just in case.” No one ran the numbers.

By the time Maria reached KDA, her corporation was clearing about $220,000 per year after expenses. Her CPA had her leave most profit inside the corporation and pay herself irregular bonuses. Between corporate income tax and personal tax on bonuses and small dividends, the effective tax bite on those profits was roughly 38 percent.

We reviewed Maria’s growth plans and confirmed she had no realistic near term venture capital or IPO path. Her work was expertise based, tied to her personally. We recommended electing S corporation status effective at the start of the next tax year, setting a $110,000 salary backed by industry compensation data, and distributing remaining profit quarterly.

In the first full year as an S corporation, Maria’s effective tax rate on business profit dropped by about 7 percentage points. On $220,000 of profit, that translated to roughly $15,000 in annual savings after factoring in payroll taxes and California’s 1.5 percent S corporation tax. Our planning fee for the restructure and ongoing support was just under $5,000, so she saw a three to one first year return with ongoing annual savings.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

When A C Corporation Actually Makes Sense

Despite the buzz around S corporations for small businesses, there are situations where a C corporation is the right call.

High Growth Startups Aiming For Equity Investors

If you plan to raise money from venture capital funds or institutional investors, they will almost always require a C corporation, often a Delaware corporation, due to securities law, investor preference, and stock option structures. Here, the corporate form is about deal reality more than tax efficiency in the early years.

Businesses Reinvesting Most Of Their Profits

If your company keeps most after tax profit inside the entity for expansion instead of distributing it, the second layer of dividend tax is less of a problem. A flat 21 percent federal rate plus state corporate tax can be competitive against top individual rates for high income owners, particularly where Qualified Business Income deductions are limited by income or specified service business rules.

Complex Employee Benefit Plans

C corporations can sometimes offer richer fringe benefits, such as certain health reimbursement arrangements, that are not taxed to high income owner employees in the same way as in pass through entities. The details are highly technical and depend on ownership percentages, so this is an area where a specialist needs to run the numbers.

When An S Corporation Tends To Win

For many profitable service businesses with a small number of actively involved owners, an S corporation often produces better after tax results than a C corporation or a straight LLC taxed as a sole proprietorship or partnership.

Active Owners With Consistent Profits Above $80,000

If your net profit before owner salary is reliably above about $80,000, it is often possible to set a defensible salary level and still have meaningful excess profit to distribute free of self employment tax. For example, a design studio with $180,000 profit might support a $90,000 salary and $70,000 to $80,000 in distributions, saving perhaps $10,000 to $12,000 per year compared to pure Schedule C treatment.

Many growing business owners underestimate how much structure and payroll planning affect these savings. Getting the books and payroll calibrated correctly is where strategy turns into real cash results.

Professional Services And Online Businesses

Consultants, agencies, medical and legal practices, engineering firms, and many online education or coaching businesses often fit well into the S corporation framework once profits justify the additional compliance overhead. In these cases, the owner is the primary driver of revenue and can be paid a market rate salary, with remaining profit flowing through more tax efficiently.

Strategic year round monitoring of profit, salary, and distributions is where experienced tax planning services earn their keep. Adjusting salary mid year when profits spike can keep you in the IRS’s comfort zone while still protecting the tax advantage on the rest of your earnings.

Red Flag Alert: Common Mistakes That Trigger IRS Scrutiny

The IRS has a well documented focus on S corporation reasonable compensation and shareholder basis issues. It also scrutinizes C corporations that appear to be retaining earnings primarily to avoid shareholder level tax.

Underpaying Salary In An S Corporation

The most frequent problem we see is an S corporation owner taking very low salary and large distributions to dodge payroll taxes. IRS guidance and court cases show that “reasonable” means what you would pay someone else to do your job. Factors include training, experience, duties, time spent, and what similar businesses pay for comparable roles.

According to discussions in IRS ruling archives and enforcement campaigns, auditors routinely reclassify distributions as wages when salaries are unrealistic, then assess back payroll tax, penalties, and interest. A pattern like $30,000 salary and $170,000 distributions for a hands on owner is an invitation for that treatment.

Paying No Dividends In A Profitable C Corporation

C corporations that accumulate large amounts of cash without credible business reasons can run into accumulated earnings tax concerns. While this specialized surtax is not common for small businesses, the IRS can and does ask why money is being parked inside the entity instead of being returned to shareholders.

Mixing Personal And Corporate Expenses

Both C and S corporations get into trouble when owners treat the business bank account like a personal wallet. Unreimbursed personal expenses, undocumented loans to shareholders, and casual transfers create messy records. They also give auditors ammunition to argue that deductions should be disallowed or that cash transfers were disguised dividends or wages.

Will Choosing The Wrong Corp Type Trigger An Audit?

Choosing C vs S status by itself does not raise a red flag. The IRS is more interested in how you use the structure you chose.

- For S corporations, the hot buttons are low salary, large distributions, and basis errors that lead to losses being claimed without enough investment or earnings to support them.

- For C corporations, patterns of large related party payments, excessive owner perks, and consistently high accumulated earnings with minimal shareholder payouts attract more questions.

If you are uneasy about how your current setup looks on paper, that is a sign to get a second opinion before an IRS letter forces the issue.

How To Decide Between C Corp And S Corp For Your Situation

You do not start with the tax code. You start with your actual business model and goals, then fit the tax rules around that reality.

Step 1: Clarify Your Realistic Growth Path

Are you building a lean, profitable firm that will spin off cash to you for years, or a high growth startup seeking outside equity? Few businesses are truly both at the same time. Your honest answer pushes you toward S corporation for the former or C corporation for the latter.

Step 2: Measure Sustainable Profit

Look at the last two to three years of results and strip out flukes. What is a normal year of profit before paying yourself? Sustainable six figure profit with you personally doing most of the work is prime S corporation territory. Highly volatile or low profit may mean sticking with an LLC taxed as a sole proprietorship or partnership until things stabilize.

Step 3: Run Side By Side Projections

Have a professional model your next three to five years both ways, including entity level taxes, payroll taxes, likely dividend or distribution patterns, and exit possibilities. Projections should reflect your state’s tax environment, not just federal rules. In California for example, S corporations pay a 1.5 percent entity tax while C corporations pay the standard corporate rate, which materially changes the math.

Step 4: Think About Exit And Succession

Will you sell stock in a C corporation, sell assets out of an S corporation, or simply wind down and collect remaining cash? Built in gains rules, depreciation recapture, and potential use of small business stock provisions all change the net result at exit time. A choice that looks slightly more expensive on annual taxes can win by a wide margin at sale.

What If You Already Chose And Regret It?

Many owners come to us midstream. They formed an LLC, elected S corp status on bad advice, or defaulted into C corp status when incorporating and now feel locked in. In reality, the IRS does allow changes, but the timing and tax consequences vary.

Switching From C Corporation To S Corporation

You can generally elect S status for a C corporation by filing Form 2553, but built in gains tax rules can apply if the corporation holds appreciated assets. That means some asset appreciation that occurred while you were a C corp can still be taxed at the corporate level if recognized within a specified window after converting to S status.

Revoking S Corporation Status

An S corporation can revoke its election and become a C corporation again, but you usually cannot bounce back and forth freely. There are waiting periods and anti abuse rules to prevent whipsawing the tax system. That is why we treat entity changes as strategic, one time moves, not annual toggles.

Fixing Botched S Corporation Elections

Late or defective S corp elections can sometimes be salvaged using relief provisions, but the process is technical and requires careful documentation. The IRS provides guidance in various revenue procedures, and you need an advisor willing to do the paperwork grind correctly.

Using Tools And Professional Help To Get This Right

If you are self employed or own an LLC and trying to understand your own self employment and income tax exposure, it helps to run actual numbers before filing any elections. A focused calculator, like a small business comparison tool or a small business tax calculator, can give you a first pass on how entity choice shifts your estimated federal liability.

Once you move from back of the napkin math to real planning, combining that with specialist support around bookkeeping, payroll, and entity elections matters. Poor implementation erases the advantage of an otherwise smart structure.

Bottom Line

Choosing between C corporation and S corporation status is not about picking the trendy option or copying what a friend did. It is about aligning your tax treatment with how your business actually earns, keeps, and eventually hands off money. The wrong choice can quietly bleed $10,000 or more per year in extra tax; the right one, implemented cleanly, can fund your retirement accounts, new hires, or an extra property.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Book Your Tax Strategy Session

If you are unsure whether your current entity status is costing you money or putting you on the wrong side of IRS scrutiny, this is the moment to fix it. Book a focused strategy session with our team and get a clear, written game plan for your next one to three years of structure, salary, and distributions, tailored to your state and industry. Click here to book your consultation now.

The IRS is not hiding these options; most owners simply were never shown how to use them.

For a broader look at S corporation tactics across California, review our complete guide to S corporation strategy here: California S corporation tax strategy guide.