Many owners hit a growth point and realize their napkin-level entity choice could be quietly costing them five figures in tax every year. They google structures, see “Ltd” and “LLC” thrown around, and quickly drown in half-correct advice from forums and friends. If you are planning to operate in the US or the UK, getting this decision wrong creates expensive friction with both tax agencies and future investors.

Here is the bottom line in plain English. A **ltd vs llc** decision is really a decision about how flexible you want your tax treatment to be, how much admin you are willing to tolerate, and what future exit you are building toward. In the US, an LLC starts out tax-transparent by default but can elect to be taxed like a corporation. In the UK, a Ltd is a corporation from day one and stays that way. That one design choice changes how profits reach your pocket and how hard HMRC or the IRS can hit you if you are sloppy.

Quick answer for busy founders

If you are a US based solo or small partnership selling services or digital products and expect under 500,000 dollars in profit in the near term, a US LLC with the option to elect S corporation status later usually gives you more tax flexibility than organizing as a UK style Ltd equivalent. If you are building a UK headquartered business with investors, a private limited company is almost always the required structure. The trap is mixing the two worlds without planning, for example running a US LLC as a UK resident and triggering complex cross border rules.

What ltd and llc really mean in practice

On paper, both structures promise limited liability. That means your personal house and savings are generally protected if the business is sued, as long as you keep business and personal finances separate and follow formalities. The big divergence shows up in how each structure is treated for tax.

How a US LLC is taxed by default

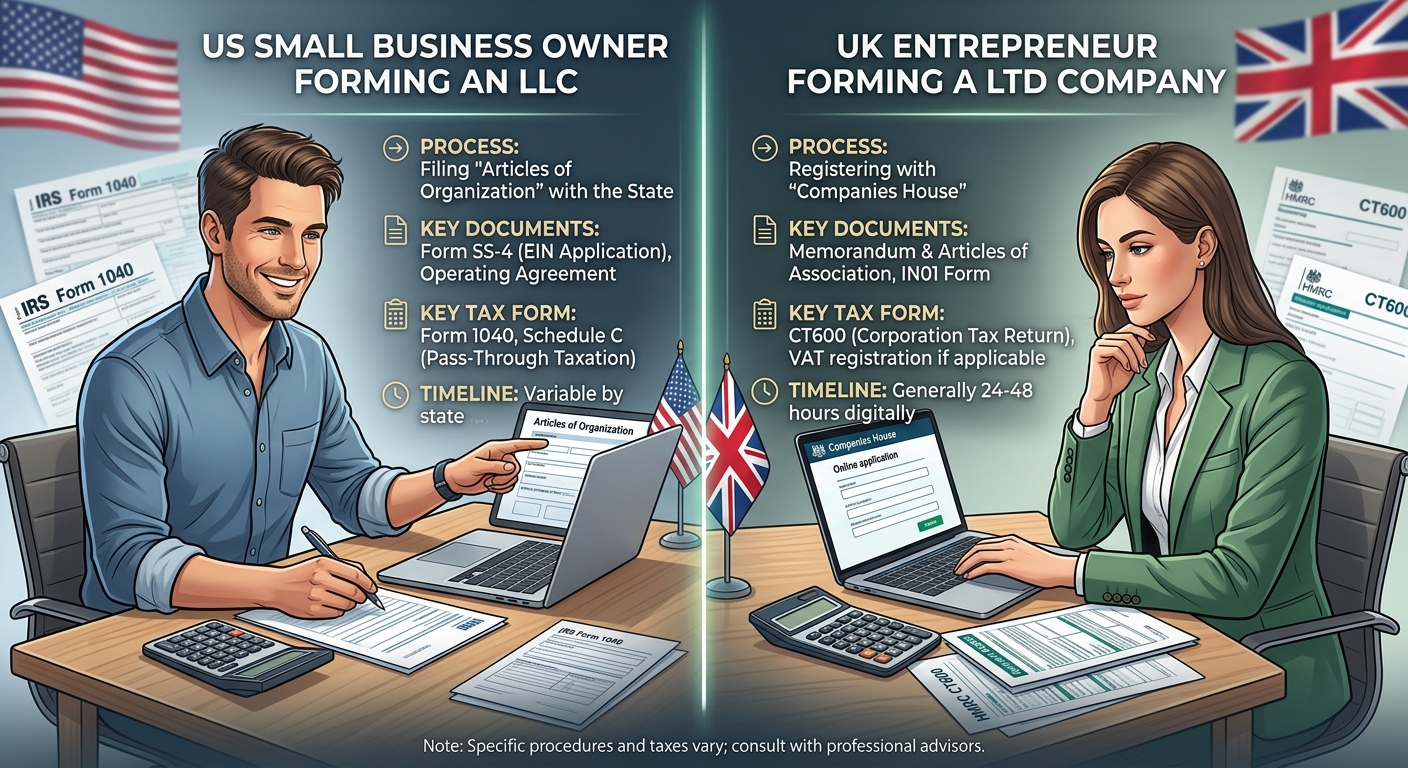

In the United States, the Internal Revenue Service treats a single member LLC as a “disregarded entity” by default. For tax purposes it does not exist separately from you. Your business income and expenses flow straight onto your personal return, usually Schedule C of Form 1040, and you pay income tax and self employment tax on the net profit. A multi member LLC is treated as a partnership, filing Form 1065 and issuing K 1s to owners. IRS Publication 3402 describes this flexible treatment in more detail and is worth skimming before you sign any operating agreement.

Crucially, an LLC can elect to be taxed as a corporation by filing Form 8832, and a qualifying LLC can go further and elect S corporation status using Form 2553. That election can drastically cut self employment taxes for the right owner, which is why tax pros often recommend an LLC as the most adaptable starting point for US based business owners.

How a UK Ltd is taxed

A UK private limited company is always a separate legal and tax entity. It pays corporation tax on its profits at the prevailing rate, then you personally pay income tax and potentially National Insurance on money you extract as salary or dividends. There is no option to “disregard” the company for UK tax, so you do not get the transparent pass through default that a US LLC offers.

For a UK resident founder taking, for example, 60,000 pounds in salary and 40,000 pounds in dividends from a profitable Ltd, you must juggle PAYE withholding, employer National Insurance, and dividend tax rules each year. That can be powerful for planning, but it is never as simple as one form on your personal return.

Tax savings potential when comparing ltd vs llc

To see how much is at stake, take a US based consultant netting 180,000 dollars from clients. If they run the work directly as a sole proprietor, all 180,000 dollars is hit with both income tax and self employment tax of 15.3 percent up to the Social Security cap plus 2.9 percent for Medicare, with an extra 0.9 percent Medicare surtax if high enough. If instead they operate through an LLC that elects S corporation status, they might pay themselves a 90,000 dollar salary and take the remaining 90,000 as distributions not subject to self employment tax. That simple shift can reduce payroll style taxes by roughly 12,000 dollars or more in year one.

This flexibility to toggle tax treatment is unique to US LLCs and S corporations. A UK Ltd can dial salary and dividends, but it cannot opt out of being a separate taxpayer. For cross border founders working with both systems, it often makes sense to get specialized tax planning services so the structures cooperate rather than collide.

When the LLC advantage disappears

The LLC is not always the clear winner. Once your retained profits grow large or you plan to bring in institutional investors, corporate style stock structure and governance can matter more than tax rate differences. Many venture funds will only invest through C corporations or UK Ltd companies, not member managed LLCs. In those cases you may accept slightly higher tax friction in exchange for access to capital and a clean exit path.

KDA Case Study: US LLC owner avoids double taxation mistake

Consider Maria, a software developer in California earning 210,000 dollars as a 1099 contractor. She initially set up a single member LLC but treated it as a C corporation after a friend suggested it “looks more professional” for enterprise clients. No one adjusted her bookkeeping. The LLC paid corporate income tax on its 160,000 dollar profit, but Maria also pulled most of that profit out as informal “draws,” which her preparer originally treated as dividends. That stacked corporate tax and personal tax on the same dollars. Her combined bill approached 55,000 dollars for the year, and she still had IRS notices asking for estimated tax penalties.

When she engaged KDA, we reworked her structure so her California LLC elected S corporation status going forward. We set a 110,000 dollar reasonable salary documented with market data, enrolled her on compliant payroll, and classified the remaining profit as S corporation distributions. For the next year, her combined federal and California self employment style taxes dropped by about 13,500 dollars compared to staying in C corporation mode, even after factoring in payroll costs and advisory fees of roughly 3,000 dollars. Just as important, she now had clean records that align with IRS expectations under guidance like Publication 535 on business expenses and payroll rules in Publication 15.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Legal and compliance differences that matter

Even if you only care about taxes today, the law and paperwork around these entities can hurt you later if you ignore them. A US LLC formed in one state but operating in another often has to register as a foreign LLC and may owe separate state level franchise or gross receipts taxes. California, for example, hits most LLCs with at least an 800 dollar annual franchise tax plus a tiered fee based on total revenue, not just profit. By contrast, UK Ltd companies deal with Companies House filings, confirmation statements, and strict rules on director duties that can create personal exposure if ignored.

For US readers juggling multiple states or considering a move into real estate, it often makes sense to coordinate entity selection with bookkeeping and payroll support. That is where a combined bookkeeping and payroll service can keep your legal structure and tax treatment aligned across state lines.

What LTD and LLC owners must track

Regardless of jurisdiction, you need clean documentation to defend your structure in an audit. For an LLC that elected S corporation status, that means minutes documenting salary decisions, timesheets for working owners, and payroll tax filings that align with what hits your Form W 2. For a UK Ltd, that means board minutes approving dividends, accurate statutory accounts, and timely filing of corporation tax returns and PAYE remittances.

If the IRS or HMRC sees personal expenses flowing through the business without clear separation, they can pierce the corporate veil and reach your personal assets. They can also reclassify distributions as wages and assess back payroll taxes plus penalties. According to IRS enforcement data, employment tax misclassification remains a high priority area, so the more your structure relies on splitting salary and dividends, the tighter your records must be.

Red flag alert: common ltd vs llc mistakes

The most expensive errors we see do not involve exotic international tax rules. They revolve around basic misunderstandings of what each entity does and does not do.

Treating a UK style Ltd like a pass through

Some UK based contractors assume they can simply sweep whatever cash sits in the company bank account at year end and treat it as “owner’s pay” without regard to salary versus dividends. That is risky. HMRC expects formal payroll runs if you pay yourself a salary and may challenge excessive dividends if the company balance sheet does not support them. Unlike a US single member LLC, you cannot ignore the company for tax purposes just because you are the only shareholder.

Ignoring elections for a US LLC

On the US side, we regularly meet owners who formed an LLC years ago and never realized it can change its tax classification. They operate with rising profits on Schedule C and pay full self employment tax on every dollar while complaining about IRS bills. For many service businesses once profits cross roughly 80,000 to 100,000 dollars, an S corporation election can often save several thousand a year, subject to reasonable salary rules. Waiting too long to elect or filing incorrectly can cost a year or more of potential savings.

How to decide: ltd vs llc decision framework

Rather than chasing the “best” structure in the abstract, match the entity to your actual plans.

Questions for US based owners

- Where are you resident and where will most of your clients be located

- Are you primarily earning active service income or building an asset heavy business like real estate

- Do you expect to bring in outside investors who might insist on a corporate form

- Is your near term goal to minimize current taxes or to position for a high value exit

If you are a US resident consultant or online business owner expecting 150,000 dollars of profit with no immediate investor plans, a US LLC taxed as an S corporation is usually more efficient than trying to hold the operation through a UK Ltd. You avoid cross border tax filings and can target self employment tax savings early.

Questions for UK based owners

- Are you UK resident for tax and planning to stay that way

- Will your customers mostly be in the UK or global

- Do you need a vehicle that investors already understand and accept

- How comfortable are you running payroll and meeting Companies House deadlines

If you are a UK resident freelancer billing 90,000 pounds a year to UK companies, a simple Ltd with modest salary and dividends often works well. Trying to own work through a US LLC as a UK resident can drag you into US filing obligations without delivering clear tax savings once double tax relief is applied.

Will this trigger an audit

Choosing one structure over another does not, by itself, trigger an audit. What attracts IRS or HMRC attention is inconsistent reporting. For example, an LLC that files as an S corporation but shows no officer compensation on its corporate return, or a Ltd that pays no salary to an obviously active director while reporting large dividends every year. Those patterns conflict with published expectations and can lead to questions.

IRS publications, including Publication 535 on business expenses and Publication 3402 on LLC taxation, outline what the agency considers reasonable in common cases. Staying within those guardrails, documenting your decisions, and filing on time with accurate forms is far more important than whether you picked an LLC or a Ltd nameplate.

Fast tax fact: ltd vs llc across borders

For globally active owners, the decision is not either or. You might run a US LLC for US operations and a UK Ltd for UK operations, coordinating them with tax treaties and transfer pricing rules. That setup is only worth the complexity once revenue justifies paying for coordinated advisory on both sides of the Atlantic. For many six figure entrepreneurs, simplifying to one primary jurisdiction first and layering others later reduces both stress and audit risk.

Key takeaways before you file anything

- An LLC in the US offers flexible tax treatment and can mimic either a pass through or a corporation, but that flexibility only pays off if you actually file the right elections.

- A UK Ltd is always a corporation for tax purposes, so you must manage salary, dividends, and corporation tax filings from day one.

- Self employment tax savings from an S corporation election can be substantial for profitable US service businesses, but the IRS expects a well documented reasonable salary.

- International setups amplify the stakes. Mixing residence, incorporation, and customer locations across countries without planning usually invites double taxation or painful clean up work.

This information is current as of 6/21/2026. Tax laws change frequently. Verify updates with the IRS or HMRC if you are reading this at a later date, and always confirm details specific to your situation with a qualified advisor.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Book your entity strategy session

If you are staring at forms wondering whether to set up an LLC, a corporation, or a cross border structure, do not guess your way into five figure mistakes. Book a focused consultation with our team, walk through your income, goals, and risk tolerance, and leave with a concrete plan rather than a stack of contradictory blog posts. Click here to book your consultation now.

The IRS is not hiding better structures from you. You just have to pick the one that fits the business you are actually building, not the one your friend chose on a different continent.