Most business owners hear they should avoid C corporations at all costs because of double taxation, then a different advisor insists every growing business needs a C corp. Caught in the middle, they end up freezing entity choices that can cost tens of thousands of dollars over a few years.

This article breaks down the real, practical difference between and s corp and a c corp for federal and California taxpayers so you can choose the structure that actually fits your situation instead of following hand-me-down rules from someone else’s industry.

Fast Tax Fact

If you run an active business generating $150,000 to $500,000 of annual profit, the entity choice question is not academic. The wrong answer can easily mean paying $10,000 to $40,000 more in combined income and payroll taxes every single year.

Quick Answer: How S Corps and C Corps Really Differ

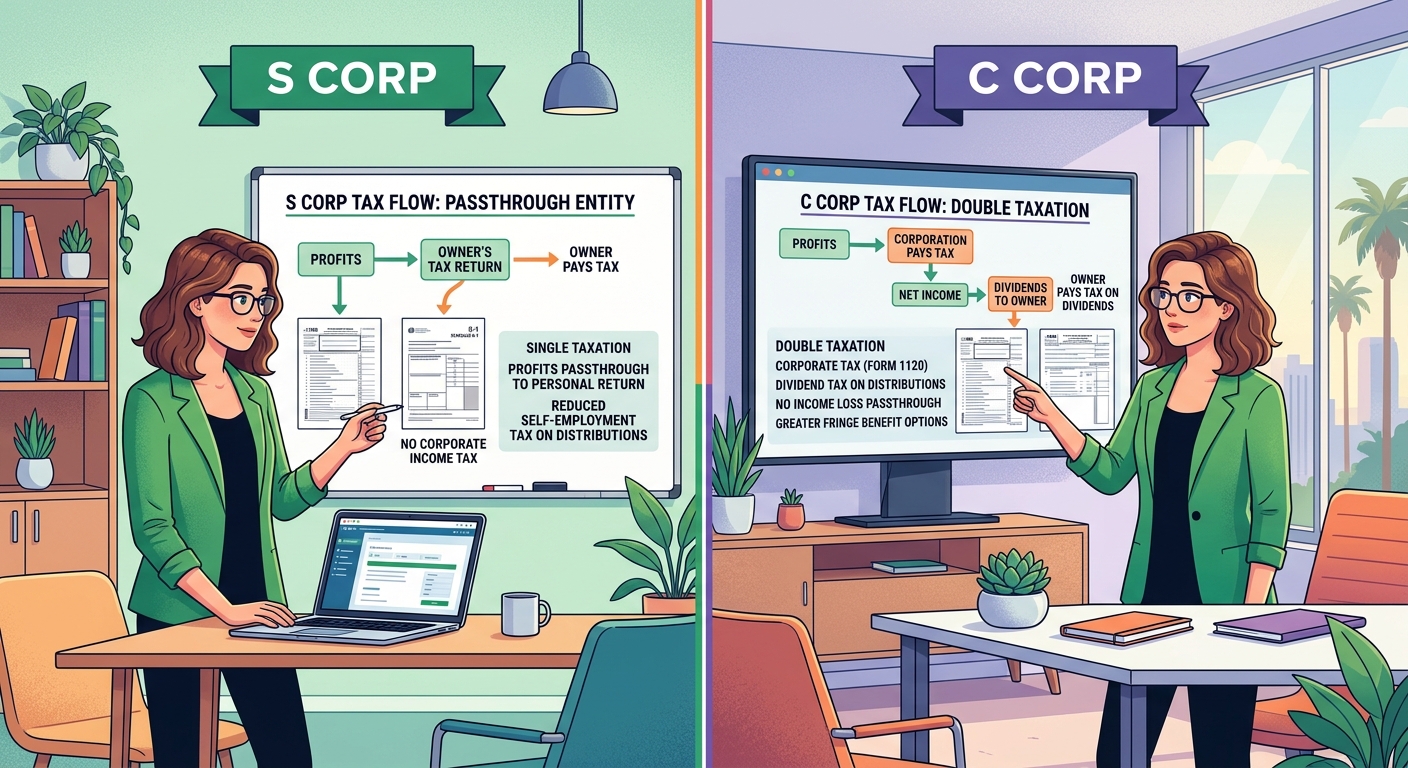

In plain English, the core difference between and s corp and a c corp is how profits are taxed and how money gets from the company to you personally.

- An S corporation is a pass-through entity. The company itself generally does not pay federal income tax. Instead, profits pass through to the shareholders’ personal returns, reported on Schedule K-1. You avoid corporate-level tax, but you must pay yourself a reasonable salary subject to payroll tax.

- A C corporation is a separate taxpayer. The company pays corporate income tax on profits. Then, when it distributes after-tax profits to you as dividends, you pay a second layer of tax personally. That is the classic “double taxation” problem.

For a California business owner, the S corporation usually wins for active operating businesses once profits climb above roughly $80,000 to $100,000, but there are clear exceptions for high-growth, investor-backed, or retained-earnings-heavy companies.

Understanding Ownership and Qualification Rules

Before diving into tax savings, you need to know who can actually use each structure. This is often the first hidden difference between and s corp and a c corp that trips people up.

S Corporation Eligibility

The IRS limits who can be an S corporation shareholder and how the stock is structured. Under IRS instructions for Form 1120-S, an S corporation must:

- Have no more than 100 shareholders

- Issue only one class of stock (no preferred shares with different rights)

- Have eligible shareholders (individuals who are U.S. citizens or residents, certain trusts, and certain estates)

- Not be an ineligible type of corporation such as certain financial institutions or insurance companies

This means if you plan to raise money from venture capital funds, foreign investors, or issue multiple classes of preferred stock, an S corporation is usually off the table.

C Corporation Flexibility

A C corporation has very few of these shareholder restrictions. It can have:

- Unlimited shareholders

- Multiple classes of stock with different economic rights

- Domestic and foreign individual or institutional investors

This flexibility is one reason most venture-backed technology companies and startups are C corporations by design.

Where This Hits Real Business Owners

Take a California marketing agency earning $300,000 in profit with two U.S. citizen owners. They are perfect S corporation candidates. By contrast, a biotech startup that expects to raise $5 million from a fund and a European investor will almost always organize as a C corporation because S status is not practical for their cap table.

How Profits Are Taxed: Pass-Through vs Double Taxation

When you compare the difference between and s corp and a c corp, taxation of profits is where most of the dollars move. Here is how money flows in each structure for an active California business.

Federal and California Taxation of S Corporations

An S corporation files an informational return on Form 1120-S, but federal income tax on its net profit is generally paid at the shareholder level. Key points:

- The company pays you a W-2 salary that is subject to Social Security and Medicare taxes.

- Remaining profit after salary flows through as S corporation income, usually not subject to self-employment tax.

- You may qualify for the qualified business income deduction (QBI) under IRS Publication 535, effectively giving you up to a 20 percent deduction on qualified pass-through income, subject to limits.

- In California, S corporations pay a 1.5 percent entity-level tax on net income, and shareholders pay state tax again on their share of income.

Example: An S corporation generates $250,000 in profit before owner compensation in 2025. The sole owner takes an IRS defensible salary of $110,000 and leaves $140,000 as pass-through profit.

- $110,000 is taxed as W-2 wages with full payroll taxes.

- $140,000 flows through as S corporation income not subject to self-employment tax.

- The owner may also get a QBI deduction up to $28,000 if income and business type meet the rules.

Federal and California Taxation of C Corporations

A C corporation files Form 1120 and is taxed directly on its profits at the corporate level. Current federal corporate tax is a flat 21 percent. California imposes an 8.84 percent corporate tax on most C corporations.

Using the same $250,000 of pre-compensation profit example:

- The corporation pays the owner a reasonable salary, say $110,000, taxed as wages with payroll tax, just like an S corporation.

- The remaining $140,000 is corporate profit. The C corporation pays 21 percent federal ($29,400) plus 8.84 percent California ($12,376), leaving about $98,224 inside the corporation after tax.

- If the corporation then distributes $80,000 of that profit as a dividend, the owner pays federal and state income tax on the dividend, often creating an effective total tax rate of 35 to 45 percent on that slice of income.

That second layer of tax is the essence of double taxation and one of the biggest practical difference between and s corp and a c corp for closely held businesses.

KDA Case Study: California Consultant Chooses S Corp Over C Corp

Consider Maria, a 1099 technology consultant in Los Angeles netting $220,000 on her Schedule C. She was getting hammered by self-employment tax and wondered whether she should form a C corporation to “look more official.”

After a detailed review, KDA structured her as a California S corporation. We set a salary of $120,000 based on market data for senior consultants and allowed the remaining $100,000 to flow as S corporation profit. That move alone reduced her exposure to Social Security and Medicare taxes on that $100,000 portion. Between payroll tax savings and a partial QBI deduction, Maria’s total annual tax bill dropped by roughly $14,000 in the first year.

Our fee to handle the entity setup, reasonable salary study, and ongoing S corporation tax planning was roughly $4,500, giving her more than a three-to-one first-year return on investment, not counting the additional planning we layered in around retirement contributions and accountable plan reimbursements.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Owner Compensation and Payroll Taxes

Owner pay is a critical part of the difference between and s corp and a c corp, especially when the goal is reducing payroll tax exposure without triggering IRS problems.

S Corporation Reasonable Salary Rules

The IRS expects S corporation shareholder-employees who provide substantial services to receive a reasonable salary before taking distributions. There is no precise formula, but IRS Topic No. 761 and several court cases emphasize factors like:

- Duties and responsibilities

- Training and experience

- What similar businesses pay for similar services

- Time and effort devoted to the business

In practice, a California S corporation owner might set salary in the 40 to 60 percent range of total profit for many service businesses, backed by compensation surveys and documentation. That salary is hit with payroll taxes, while the remaining pass-through profit avoids self-employment tax.

C Corporation Salary and Bonuses

With a C corporation, there is more flexibility to use salary and bonuses as a planning tool. The corporation can choose to retain earnings to reinvest or distribute profits as dividends.

For many closely held C corporations, the strategy is to push most profits out as salary and bonuses to owners, reducing corporate-level tax. But the IRS can challenge unreasonable compensation if it appears to be a disguised dividend distribution, especially when salaries for shareholder-employees are far above market for similar roles.

When Payroll Tax Savings Tip the Scale

Suppose a single-owner California consulting business nets $180,000 before owner pay. As a sole proprietor, all $180,000 is subject to self-employment tax. As an S corporation, if you pay yourself a defensible $110,000 salary and leave $70,000 as pass-through profit, that $70,000 is no longer exposed to the 15.3 percent self-employment tax. The rough payroll tax savings alone can exceed $10,000 per year, even before income-tax-side planning.

For business owners in this range, S status is often a key leverage point. For those planning to raise capital, issue stock options, or retain large profits inside the company, the advantage may shift toward the C corporation model.

Which Persona Fits Which Entity?

While the difference between and s corp and a c corp is ultimately fact-specific, patterns emerge when you look at real-world taxpayers.

W-2 Employees With Side Income

If you have a W-2 job in California and a side consulting business that nets $30,000 to $60,000, an S corporation is often overkill. The costs of payroll, bookkeeping, and tax filings can eat most of the payroll tax savings at that level.

It is usually more efficient to stay a sole proprietor initially, then consider an S corporation election when consistent net profit moves north of $80,000. When that happens, many self-employed professionals benefit from restructuring into an S corporation and tightening their books.

Full-Time 1099 Contractors and Solo Consultants

For 1099 earners with $150,000+ of net profit and no plans for outside investors, an S corporation tends to be the default choice. It combines liability protection via an LLC with significant payroll tax savings and clean pass-through taxation. C corporation status rarely makes sense for a solo consultant unless there is a very specific reason, such as qualifying for certain fringe benefits or building a retained-earnings war chest for a future sale.

At this stage, professional tax planning services become crucial. They can coordinate S corporation elections, payroll setup, retirement plans, and accountable plans into a coherent structure instead of random tactics.

Multi-Owner Professional Firms

Think of law firms, medical practices, and engineering groups with three to ten partners. If the owners are all U.S. individuals, S corporations regularly win for these firms, especially when profits are distributed annually instead of being heavily retained.

However, once the group wants to offer meaningful equity to associates, bring in non-U.S. partners, or raise capital from institutions, C corporation status or a partnership structure may be more flexible, even if it is less tax-efficient on current profits.

High-Growth Startups and Investor-Backed Companies

For startup founders who expect angel or venture backing, the difference between and s corp and a c corp is almost irrelevant because the investor ecosystem overwhelmingly expects a Delaware C corporation with multiple stock classes and a familiar legal framework. In these cases, minimizing double taxation on current profits is less important than scalability, access to capital, and exit strategy.

Common Mistakes That Trigger IRS and FTB Problems

Whether you choose an S or C corporation, there are recurring mistakes that bring unwanted attention from the IRS or the California Franchise Tax Board.

Ignoring Reasonable Salary in S Corporations

A classic mistake is taking minimal salary and massive S corporation distributions to dodge payroll tax. If your S corporation nets $300,000 and you pay yourself a $40,000 salary, that is a bright red flag. The IRS routinely reclassifies distributions as wages in audits, adding back payroll taxes, penalties, and interest. According to IRS enforcement summaries, officer compensation is a consistent audit focus.

Using a C Corporation for Lifestyle Businesses Without a Plan

Another mistake: forming a C corporation for a small professional practice or consulting firm with no outside investors and no real need for large retained earnings, then distributing profits each year as dividends. This is often the worst of both worlds: you are paying corporate tax and second-layer dividend tax when an S corporation could have delivered cleaner pass-through treatment.

Missing S Election Deadlines

To be treated as an S corporation for a given tax year, eligible corporations generally must file Form 2553 no later than two months and 15 days after the beginning of the tax year the election is to take effect. While there are late-election relief provisions in Revenue Procedure 2013-30, relying on relief is not a planning strategy. Miss the timing and you may be stuck as a C corporation for the year.

Will This Trigger an Audit?

Choosing between S and C status itself does not trigger an audit. The problems come from abusing whichever structure you pick.

- Extremely low S corporation salaries relative to profit are a known audit trigger.

- C corporations paying huge salaries to owner-employees while posting tiny or no corporate profit can draw scrutiny for unreasonable compensation.

- Sloppy bookkeeping, commingled funds, and missing documentation are universal red flags in either structure.

Whatever path you choose, tight books and a defensible compensation strategy are non-negotiable. If you are not sure your records could survive scrutiny, running your numbers through a small business tax calculator and then having a professional review is a smart first step.

Bottom Line: How to Decide Between S and C Status

When you focus on the actual difference between and s corp and a c corp, a practical decision framework emerges.

Consider an S Corporation If:

- You are a U.S. individual or a small group of U.S. individual owners

- Your business is an active trade or business, not a pure investment holding company

- Net profit is consistently above $80,000 and likely in the $150,000+ range

- You do not need complex stock structures or foreign investors

- You are willing to run real payroll and keep accurate books

Consider a C Corporation If:

- You expect to raise money from venture capital or institutional investors

- You need multiple stock classes, stock options, or complex equity structures

- You plan to retain large profits inside the business for expansion instead of distributing them

- You may benefit from corporate-rate arbitrage by leaving profits in the corporation long-term

For deeper S corporation strategy, including California-specific rules and advanced planning moves, review our comprehensive S corp resource at this complete guide to S corp tax strategy in California and then tailor your entity choice with a professional who understands both sides of the equation.

Key Questions to Ask Before You Lock In an Entity Choice

Before you file anything with the IRS or California, sit down with these questions and your latest profit-and-loss statement:

- What are my realistic profit expectations over the next three years?

- Am I likely to bring in non-U.S. investors or institutional money?

- Do I want to reinvest most profits into growth, or distribute them to myself regularly?

- How comfortable am I with payroll, bookkeeping, and entity maintenance requirements?

- What is my exit strategy: sale, merger, or long-term lifestyle business?

Answering these honestly will do more for your tax outcome than obsessing over abstract arguments about which structure is “better.” A well-documented, reality-based decision will also play better in front of an IRS examiner than a hasty election done because a friend or social media post said everyone should be an S corp.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Book Your Tax Strategy Session

If you are unsure whether your current structure is costing you serious money, or you are about to form a new entity and want to get it right the first time, treat this as a one-time decision worth doing correctly. A short planning session can easily uncover savings in the five-figure range over the next few years for many California business owners. Click here to book your consultation now.

The IRS is not hiding the rules. They are just written for tax pros, not entrepreneurs. Once you truly understand the difference between and s corp and a c corp in your specific situation, you can use the tax code as a tool instead of treating it as an obstacle.

This information is current as of 6/19/2026. Tax laws change frequently. Verify updates with the IRS or FTB if you are reading this at a later date.