Quick Answer

Switching from a C corporation to an S corporation can be a powerful tax move, but the IRS will not let you sidestep corporate tax on appreciated “hot” assets just by filing an election. When a former C corporation becomes an S corporation, any built in gain that existed on the conversion date can be subject to corporate level tax for a recognition period under Internal Revenue Code section 1374. If you are not planning ahead for this, you can accidentally trigger a large, avoidable tax bill when you sell or distribute assets after the election.

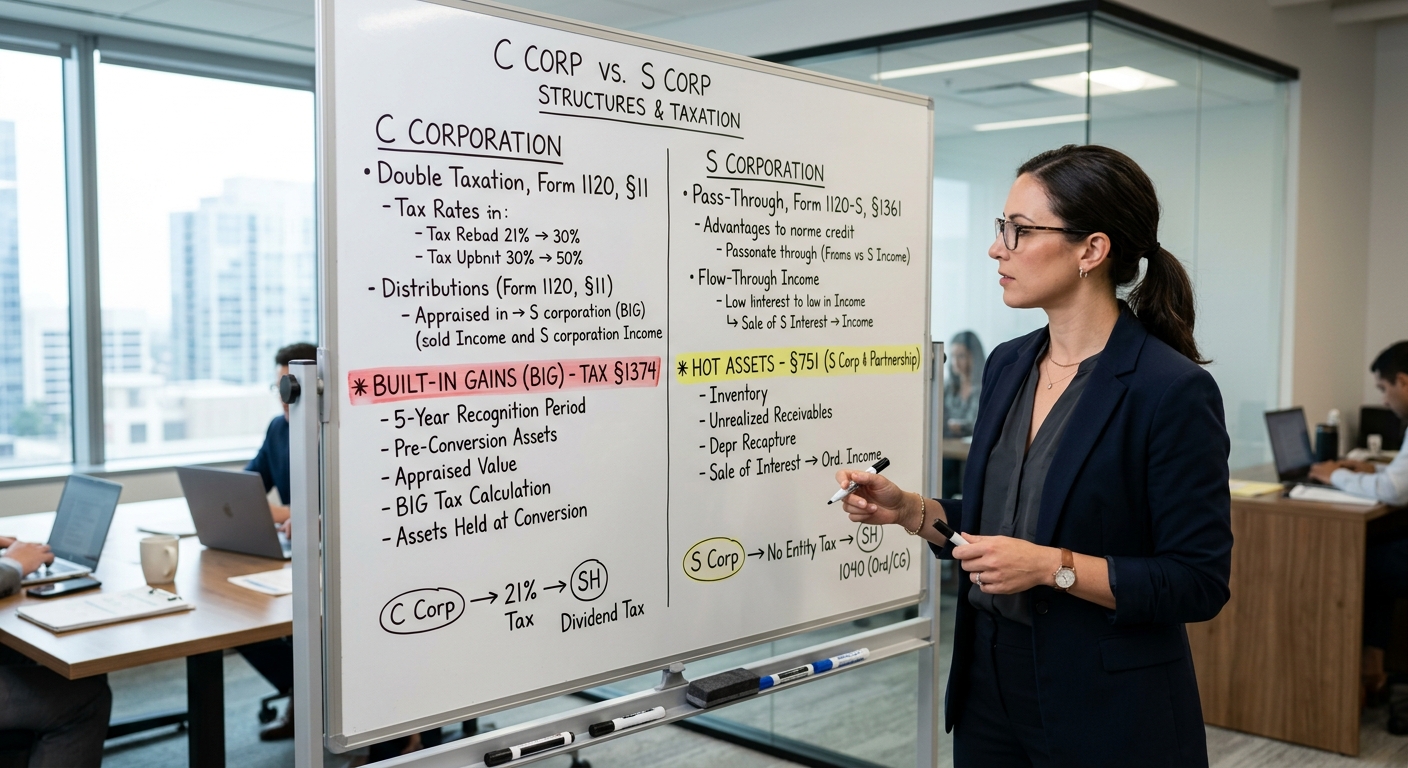

Understanding C Corp to S Corp Conversions and c corp to s corp hot assets

When owners of closely held companies hear about S corporations, they usually focus on the self employment tax savings. Pay yourself a reasonable W 2 salary, take the rest as distributions, and potentially save thousands each year. What often gets ignored is the hidden trap sitting on the balance sheet: appreciated business assets that carry built in gain from the company’s C corporation years.

These appreciated assets are what practitioners call c corp to s corp hot assets. Think of real estate that has gone up in value, a highly profitable customer list, or fully depreciated equipment that still has resale value. For federal tax purposes, the IRS wants to make sure that gain which economically accrued while the entity was a C corporation does not magically escape corporate tax just because the owners filed Form 2553.

The result is a complex set of rules under section 1374 and Form 1120 S instructions. If you do not map out your hot assets before you convert, you can find yourself paying both entity level and shareholder level tax on the same profit. That is exactly the kind of double taxation business owners expect an S corporation to solve, not create.

What Counts as a Hot Asset in a C Corp to S Corp Conversion?

Before you can plan around the rules, you need to know which items on your balance sheet qualify as c corp to s corp hot assets. In plain English, a hot asset is anything that has built in gain on the day before your S election takes effect. Built in gain means the asset’s fair market value exceeds its tax basis.

Common examples include:

- Commercial real estate bought for $600,000 that is now worth $1,000,000.

- Fully depreciated machinery with a zero tax basis but a resale value of $100,000.

- Intangible assets like customer lists or trademarks that have been amortized for tax but still produce income.

- Installment sale receivables from C corporation years.

If your corporation holds rental property, this is especially important. Many real estate investors incorporate early on, then later decide they want the flow through benefits of an S corporation. Without a detailed asset by asset analysis, they miss how much tax is baked into those properties for section 1374 purposes.

Red Flag Alert: A balance sheet with long held real estate or fully depreciated equipment almost always contains significant built in gains. Assuming the S election wipes the slate clean is one of the fastest ways to end up in an audit discussion about improper reporting.

How the Built In Gains Tax Works After Conversion

Once a C corporation makes a valid S election, the clock starts on the built in gains recognition period. Historically this period has been five years for most taxpayers, but you should verify the current rule in the latest IRS Publication 542. During this window, if the S corporation sells or distributes an asset that had built in gain on the conversion date, the corporation may owe a corporate level tax on that gain under section 1374.

Here is a simple example for context. Suppose your C corporation owns a building with a tax basis of $400,000 and a fair market value of $900,000 when you convert. That $500,000 difference is built in gain. Two years after the S election, you sell the building for $950,000. The S corporation has a total gain of $550,000, but up to $500,000 can be subject to the built in gains tax at corporate rates. The remaining $50,000 would flow through to shareholders without the extra entity level layer.

This is where c corp to s corp hot assets become a serious planning issue. If you were expecting all of that gain to enjoy a single level of pass through taxation, the corporate tax hit can feel like a nasty surprise. For owners in high tax states like California, the combined burden can easily turn what looked like a six figure tax savings play into a marginal result.

Pro Tip: Before filing your S election, ask your advisor to run your situation through a capital gains tax calculator using both “stay C corp” and “convert to S corp then sell” scenarios. Seeing the math side by side often highlights where the built in gains tax will actually bite.

Strategic Ways to Manage Hot Assets Before and After Conversion

Fortunately, you are not stuck with a binary choice between absorbing a large built in gains tax or abandoning your S corporation strategy. With thoughtful planning, you can often reduce the impact of c corp to s corp hot assets or at least control the timing.

1. Reevaluate Entity Structure and Timing

If your core business has strong profits today but your balance sheet is loaded with hot real estate, you might split operations from assets before you elect S status. For example, you can keep existing appreciated property in the C corporation and form a new entity taxed as an S corporation for active operations, using an intercompany lease. This type of restructuring should be modeled carefully alongside professional entity formation planning so you avoid triggering recognition of the very gains you are trying to manage.

For some business owners, the smarter move is to sell or dispose of key hot assets before filing Form 2553, taking a final C corporation level hit when they can control the rate environment and use any available loss offsets. Others may deliberately delay planned sales until after the recognition period ends, especially if they are comfortable holding real estate long term.

2. Use Losses and Deductions to Offset Built In Gains

Section 1374 generally allows built in gains to be reduced by built in losses and certain carryforwards. That means two corporations with the same balance sheet can face very different outcomes depending on how well they track old net operating losses, capital loss carryovers, and depreciation histories from their C corporation years. Smart tax planning services will dig into those records well before a conversion, not after the sale contract is signed.

One practical approach: if you know you will sell a hot asset during the recognition period, you may also accelerate deductible expenses or time other dispositions that create recognized built in losses in the same year. Even a $100,000 offset can translate into tens of thousands of dollars in avoided corporate tax.

KDA Case Study: Manufacturing Owner Navigates Hot Asset Exposure

Consider a California manufacturing company that operated as a C corporation for 15 years. The owner, Miguel, had grown annual profits to about $800,000 and was frustrated by the double taxation environment. His balance sheet carried fully depreciated equipment with a fair market value of roughly $600,000 and an industrial building with $300,000 of tax basis and a $900,000 market value. Both categories were classic c corp to s corp hot assets.

When Miguel approached our team, he was considering an immediate S election followed by a quick sale of the building to free up cash. We modeled the transaction and showed him that selling within the recognition period would trigger roughly $600,000 in recognized built in gain, leading to a six figure corporate tax bill before shareholder level tax.

Instead, we helped him refinance the building to access cash without a sale, separated a portion of operations into a new S corporation for future growth, and built a three year plan to replace older equipment in a way that generated offsetting deductions. Over four tax years, Miguel restructured his group so that the original C corporation slowly wound down, and the new S corporation inherited only assets without significant built in gain exposure.

The result: Miguel avoided more than $150,000 in corporate level tax he would have paid by rushing the sale, while still capturing estimated annual self employment tax savings of about $40,000 once the S corporation was fully in place. His advisory fees for the project were under $25,000, producing a first year ROI of nearly 8x and long term savings that will follow him into retirement.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

What Happens If You Sell Hot Assets During the Recognition Period?

Many owners only learn about built in gains tax after they have accepted an offer to sell property or shares. If you close the transaction during the recognition period, the S corporation will have to compute the portion of gain attributable to C corporation years and may owe corporate level tax. This is reported on Schedule D and other lines of Form 1120 S, and the computation can be complex.

For example, suppose you convert on January 1, 2025, and sell a major asset on March 1, 2028. If the asset’s fair market value was $700,000 on the conversion date and its basis was $300,000, that $400,000 spread is built in gain. If you sell for $750,000, your total realized gain is $450,000, but only $400,000 is subject to the section 1374 tax. The remaining $50,000 flows through like a normal S corporation gain.

Will this trigger an audit? The IRS is particularly sensitive to large transactions shortly after a C to S conversion, especially in industries with significant hard assets. According to the agency’s enforcement data summarized in the latest IRS Data Book, automated systems flag mismatches involving capital gains and entity elections at a growing rate. While a properly reported built in gain will not automatically draw an examiner, inconsistent or missing reporting can raise red flags quickly.

Common Mistakes Around Hot Assets and How to Avoid Them

Because the c corp to s corp hot assets rules are technical, even sophisticated owners and advisors can stumble. Here are some traps we see regularly in real world client files.

Assuming the S Election Erases Old Earnings and Profits

Many taxpayers believe that once the S election is effective, prior C corporation earnings and profits and built in gains simply disappear. In reality, old E&P can limit distributions and affect reasonable compensation analysis, and built in gains tax remains a risk during the recognition period. You must track both items carefully after conversion, not just toss old records in storage.

Failing to Value Assets at Conversion

The built in gain calculation starts with fair market value on the day before the S election. Guessing at values or using outdated appraisals can lead to overstated or understated tax. For major assets, especially real estate, getting a qualified appraisal at or near the conversion date is often worth every dollar.

Moving Assets Around Without Considering Section 1374

Transferring property between related entities or dropping appreciated assets into a new S corporation without understanding section 1374 and related rules under corporate liquidation guidance can accidentally reset or compound built in gain exposure. This is an area where DIY restructuring can backfire fast.

Will an S Corp Election Still Help If You Have Large Hot Assets?

For some corporations, the answer is still yes. You can separate old hot assets from new growth, design compensation strategies to balance payroll tax savings with retirement plan contributions, and use the S corporation structure for future profits while accepting that a portion of legacy appreciation will be taxed at corporate rates when realized.

If your manufacturing company, professional practice, or real estate holding structure generates $500,000 or more in annual profit, even a constrained S corporation strategy can produce five figures of yearly savings. Combining those benefits with a thoughtful approach to c corp to s corp hot assets is where a seasoned advisor earns their keep.

How to Prepare for a C to S Conversion if You Own Real Estate

Real estate heavy corporations are the most likely to run into painful built in gains outcomes. If your C corporation owns one or more properties, start with a detailed inventory:

- List each property with purchase date, original cost, improvements, and accumulated depreciation.

- Estimate current fair market value using recent comps or broker opinions.

- Identify any properties you plan to sell in the next five to seven years.

From there, your advisor can rank properties by built in gain exposure and sale probability, then design a conversion timeline. In some cases, it makes sense to sell a property before the S election when the corporate tax cost is acceptable and perhaps offset by other loss items. In other cases, you might hold the property well beyond the recognition period, using refinancing or related party leases to access cash without triggering gain.

Bottom Line

The tax code deliberately prevents owners from using an S election to erase the corporate level tax on appreciated assets accumulated during C corporation years. Understanding how c corp to s corp hot assets and built in gains really work is the difference between a smooth, strategic conversion and a costly misstep. The right plan balances timing, entity structure, asset management, and documentation so you are not surprised by section 1374 tax when you can least afford it.

This information is current as of 6/15/2026. Tax laws change frequently. Verify updates with the IRS or your state tax authority if you are reading this in a later year.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Book Your Tax Strategy Session

If you are considering an S election for a profitable C corporation and your balance sheet includes appreciated property, you should not move forward without a written plan for hot assets and built in gains. Our team specializes in complex multi entity planning for owners with significant real estate, equipment, and intellectual property. Click here to book your consultation now.