Quick Answer

What is the state income tax in California? California uses a progressive tax system with rates from 1% to 12.3%, plus an additional 1% Mental Health Services Tax on income over $1 million. Your actual rate depends on your taxable income and filing status. For 2026, single filers earning $70,000 pay an effective state rate of around 4.1%, while someone earning $500,000 pays closer to 9.8%.

The Myth That Everyone Pays the Same California Tax Rate

Here’s what most Californians get wrong: they think California has one flat tax rate, like Nevada or Texas (which have none). Reality? California operates one of the most aggressive progressive tax systems in the nation. If you earned $60,000 last year, you paid a fraction of what your neighbor making $250,000 paid, not just in dollars, but in actual percentage rate.

This matters more than ever in 2026. With IRS audit activity ramping back up (497,621 audits closed in 2025 with $26.8 billion in additional assessments) and California’s Franchise Tax Board tightening compliance enforcement, understanding exactly what is the state income tax in CA can save you from costly mistakes, missed deductions, and unwanted notices.

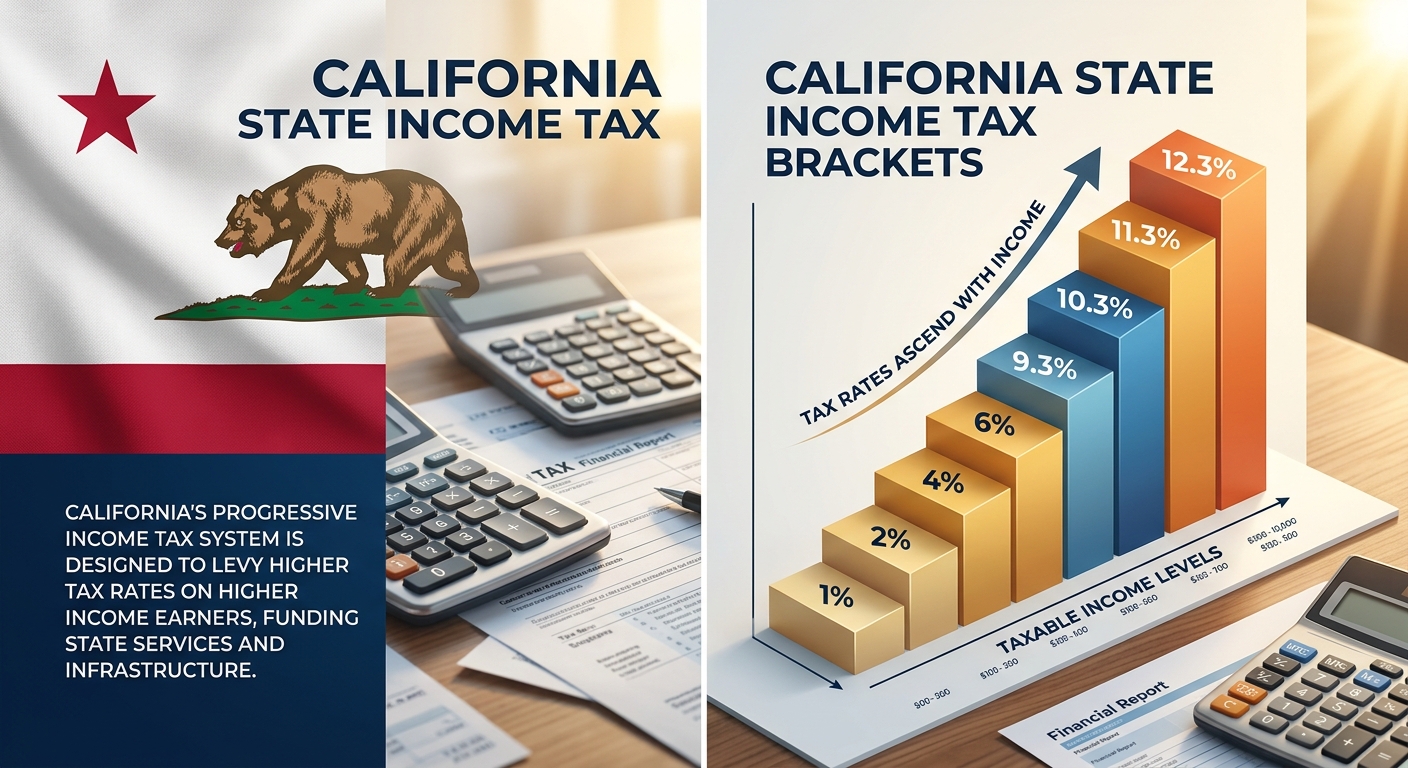

How California’s Progressive Tax Brackets Actually Work

California doesn’t tax all your income at one rate. Instead, it slices your income into chunks, taxing each piece at a different rate as you move up the ladder. This is called a marginal tax system.

2026 California Tax Brackets for Single Filers

| Taxable Income Range | Marginal Tax Rate |

|---|---|

| $0 – $10,412 | 1% |

| $10,413 – $24,684 | 2% |

| $24,685 – $38,959 | 4% |

| $38,960 – $54,081 | 6% |

| $54,082 – $68,350 | 8% |

| $68,351 – $349,137 | 9.3% |

| $349,138 – $418,961 | 10.3% |

| $418,962 – $698,271 | 11.3% |

| $698,272+ | 12.3% |

| $1,000,000+ (additional) | +1% Mental Health Services Tax |

Let’s break this down with a real example. If you’re a single filer who earned $85,000 in taxable income:

- First $10,412 taxed at 1% = $104

- Next $14,272 taxed at 2% = $285

- Next $14,275 taxed at 4% = $571

- Next $15,122 taxed at 6% = $907

- Next $14,269 taxed at 8% = $1,142

- Remaining $16,650 taxed at 9.3% = $1,548

Total California state tax: $4,557 (effective rate of 5.4%)

Notice you didn’t pay 9.3% on all $85,000. You paid different rates on different slices. This is how progressive taxation prevents lower earners from being crushed by high rates while still collecting more from high earners.

Married Filing Jointly: Double the Brackets

Married couples filing jointly get roughly double the bracket thresholds. The top 12.3% rate doesn’t kick in until taxable income exceeds $1,396,542. This structure benefits married couples significantly, especially when both spouses earn similar amounts.

Red Flag Alert: What Triggers California FTB Audits in 2026

The California Franchise Tax Board has been quietly automating its audit selection process, mirroring the IRS’s Automated Underreporter Program that caught 987,460 taxpayers in 2025 alone. Here’s what flags your return:

High-Risk Audit Triggers

- Mismatched W-2 or 1099 income: FTB receives copies of all your income documents. If your return shows $78,000 but your W-2s total $82,000, you’re getting a notice.

- Excessive business losses on Schedule C: Claiming $60,000 in losses while reporting $90,000 in W-2 income raises red flags, especially if losses repeat year after year.

- Out-of-state income claims: California aggressively pursues residents who try to shift income to lower-tax states without proper substantiation.

- Large charitable deductions: Claiming $25,000 in donations on $80,000 income (over 30%) will trigger verification requests.

- Home office deductions over $10,000: Especially for W-2 employees who can no longer claim this federally but try to on state returns.

Bottom line: California’s automated systems cross-reference your federal return, W-2s, 1099s, K-1s, and prior-year returns. Any inconsistency generates an automated inquiry before a human ever sees your file.

KDA Case Study: Small Business Owner

Marcus, a 38-year-old freelance software developer in San Jose, came to KDA after receiving an FTB notice claiming he owed an additional $11,400 in state taxes plus penalties. The issue? Marcus reported $140,000 in gross 1099 income but claimed $95,000 in business expenses, leaving just $45,000 in taxable income.

The FTB flagged his return because his expense ratio (68%) far exceeded industry norms (typically 25-35% for software contractors). Marcus had legitimate expenses but poor documentation. Many receipts were missing, and he mixed personal and business spending on the same credit card.

KDA’s strategy: We reconstructed his expense records using bank statements, project invoices, and vendor confirmations. We separated personal expenses, properly categorized business travel (which was significant), and provided detailed explanations for equipment purchases. We also helped him establish a separate business checking account going forward.

Result: FTB accepted our documentation. Marcus’s additional tax liability dropped from $11,400 to just $1,850. He paid our $2,400 representation fee but saved $9,550 in taxes and avoided $2,280 in penalties. First-year ROI: 3.98x. More importantly, we set up systems to prevent future audits.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How California State Tax Differs From Federal Tax

Many California taxpayers assume state and federal tax rules mirror each other. They don’t. These differences create costly mistakes:

Key Differences That Cost You Money

- Standard deduction: Federal standard deduction for 2026 is $15,000 (single). California’s is only $5,363. This means itemizing often makes sense for state taxes even if you take the standard deduction federally.

- SALT deduction cap: The federal $10,000 cap on state and local tax deductions doesn’t exist on your California return. You can deduct your full property tax amount on your state return.

- Qualified Business Income (QBI) deduction: The federal 20% QBI deduction for pass-through businesses doesn’t apply to California. If you own an LLC or S Corp, you pay California tax on 100% of your business income.

- Capital gains rates: Federal capital gains get preferential rates (0%, 15%, or 20%). California taxes capital gains as ordinary income at your full marginal rate. Selling stock with a $100,000 gain? That’s taxed at 9.3% or higher for most middle-income earners.

These differences mean you need separate calculations for federal and state planning. A strategy that saves federal tax might increase your California liability, and vice versa.

Special Situations and Edge Cases

Standard tax guidance rarely covers these scenarios, but they impact thousands of California taxpayers:

Part-Year Residents

If you moved to or from California mid-year, you’ll file as a part-year resident. California taxes you on all income earned while you were a resident, plus any California-source income earned while a nonresident. This gets complex fast, especially with stock options, bonuses, or business income.

Example: You moved from California to Texas on July 1, 2026. Your $120,000 salary is split evenly. California taxes the $60,000 earned January-June at California rates. But if you also received a $30,000 bonus in August (after moving), California won’t tax it because it’s compensation for services performed after you became a nonresident, and you have no California-source income at that point.

Nonresidents With California Income

Living in Nevada but working remotely for a California company? You might still owe California tax. California taxes nonresidents on income from “sources within California.” This includes wages for work physically performed in California and income from California rental properties or businesses.

The confusion comes with remote work. If you live in Oregon but your employer is in San Francisco, and you never set foot in California for work, Oregon taxes your wages, not California. But if you spend 40 days a year in California at the SF office, California wants its share of those days.

Mental Health Services Tax for High Earners

Single filers with taxable income over $1 million face an additional 1% tax on income exceeding that threshold. This effectively makes the top rate 13.3% (12.3% + 1%). Married filing jointly couples hit this at $1,198,024.

This impacts bonuses and stock compensation heavily. If your salary is $950,000 and you receive a $150,000 bonus, that bonus pushes $100,000 into the 13.3% bracket. Combined with federal tax (37%), FICA (if applicable), and other taxes, your marginal rate on that bonus exceeds 50%.

Strategic Deductions to Lower Your California Tax Bill

Understanding what is the state income tax in CA is step one. Step two is legally reducing what you owe. These strategies work specifically for California taxpayers:

Maximize Retirement Contributions

Contributions to traditional 401(k), 403(b), and similar plans reduce both federal and California taxable income. For 2026, you can contribute up to $23,500 ($31,000 if you’re 50+).

Real savings: A single filer earning $95,000 who maxes out a 401(k) drops their taxable income to $71,500. At the 9.3% bracket, that’s $2,186 in California state tax savings, plus federal savings.

Health Savings Account (HSA) Contributions

If you have a qualified high-deductible health plan, HSA contributions ($4,300 individual, $8,550 family for 2026) reduce California taxable income. These contributions also grow tax-free and can be withdrawn tax-free for medical expenses.

Charitable Contributions With Proper Documentation

California allows itemized charitable deductions without the federal percentage limitations. But you must have receipts for any donation over $250 and maintain mileage logs if you deduct miles driven for charity work (14 cents per mile for 2026).

Pro Tip: Donate appreciated stock instead of cash. You avoid capital gains tax and get a deduction for the full fair market value. This works better in California than other states because California’s high capital gains tax rates (same as ordinary income) make the savings even greater.

Work With a Tax Professional for Entity Structuring

Business owners can significantly reduce their California tax through proper entity selection and structuring. While we can’t eliminate the state tax, strategies like S Corp elections can reduce self-employment taxes, and strategic income timing can smooth bracket creep. If you’re operating as a sole proprietor with $100,000+ in net profit, you’re likely leaving money on the table.

Explore our tax planning services to see how entity optimization and proactive strategies can keep more money in your business.

What Happens If You Underpay California State Tax?

California doesn’t mess around with underpayment. Here’s what you’re facing if you short the state:

Underpayment Penalties

If you owe $500 or more when you file your return (after withholding and estimated payments), California charges an underpayment penalty. The rate varies but typically runs 3-5% annually. For 2025 taxes, the rate was 3% for most of the year.

How to avoid it: Pay at least 90% of your current year tax liability or 100% of your prior year tax (110% if your prior year adjusted gross income exceeded $150,000) through withholding or estimated quarterly payments.

Interest on Late Payments

Even if you file an extension, you must pay at least 90% of your tax liability by the original April deadline. Any balance owed accrues interest from the original due date until paid. California’s interest rate for underpayments is currently 5% annually.

Reality check: If you owe $8,000 and file in October (six months late), you’ll pay roughly $200 in interest even with a valid extension. The extension gives you more time to file, not to pay.

Failure to File Penalty

Don’t file at all? California charges 5% of the unpaid tax per month, up to 25% maximum. Owe $10,000 and don’t file for five months? That’s a $2,500 penalty on top of the tax owed and interest.

The IRS closed 592,773 Automated Substitute for Return cases in 2025, generating $2.9 billion in assessments. California runs a similar program. They’ll file a return for you using all reported income (W-2s, 1099s) and zero deductions. You get stuck with the maximum tax bill plus penalties.

California State Tax for Different Taxpayer Types

Your California tax strategy should match your income situation. Here’s how what is the state income tax in CA impacts different taxpayers:

W-2 Employees

If you’re a salaried employee, your employer withholds California tax from each paycheck based on your W-4 and DE-4 forms. Most W-2 employees slightly overpay through withholding and receive refunds.

Action step: Review your withholding if you consistently owe money or get huge refunds. Owing $100-500 is ideal. It means you kept your money all year instead of giving California an interest-free loan.

Self-Employed and 1099 Contractors

No employer withholds for you. You must make quarterly estimated tax payments to California (April 15, June 15, September 15, January 15). Underpay and you’ll face penalties, even if you ultimately get a refund due to deductions you claim when you file.

Pro Tip: Set aside 30-35% of every payment you receive to cover federal, California, and self-employment tax. Open a separate savings account labeled “Tax Holding” and transfer money there immediately.

Business Owners (LLC, S Corp, Partnership)

Pass-through income flows to your personal return where California taxes it at your marginal rate. Remember, California doesn’t recognize the federal QBI deduction, so you’re taxed on 100% of pass-through income.

S Corp owners: California charges an annual $800 minimum franchise tax regardless of profit, plus a gross receipts fee based on total California income. Factor these into your cost-benefit analysis when choosing entity structure.

Real Estate Investors

Rental income, property flips, and capital gains from California property sales are fully taxable to California residents. Depreciation deductions offset rental income, but you’ll recapture depreciation when you sell (taxed as ordinary income up to 25% federally, and at your full California marginal rate).

Strategy consideration: If you’re planning to sell a California rental property with significant gains, timing the sale in a lower-income year can drop you into a lower California bracket, potentially saving thousands.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions

Do I pay California state tax if I work remotely for a California company but live in another state?

It depends on where you physically perform the work. If you live in Oregon and work 100% remotely from home, Oregon taxes your wages, not California. But if you travel to California for meetings or work, California can tax the portion of your income attributable to days worked within the state. This is called “source-based taxation” and applies to nonresidents.

Can I deduct my federal tax refund on my California return?

No. Federal income tax refunds are not taxable income for California purposes. However, if you claimed a state tax refund as income on your federal return (because you itemized deductions the prior year), that doesn’t create California tax since you already paid California tax on the original income.

What if I can’t afford to pay my California state tax bill?

California offers payment plans for taxpayers who can’t pay in full. You can request an installment agreement through the FTB website or by calling. Interest still accrues, but you avoid the more severe collection actions like bank levies or wage garnishments. Don’t ignore it. California is aggressive about collections and can suspend your professional license or revoke your business entity for unpaid taxes.

How do California tax brackets adjust for inflation?

California adjusts tax brackets, standard deductions, and exemptions annually based on the California Consumer Price Index. For 2026, brackets increased approximately 3.2% from 2025 levels. This prevents “bracket creep” where inflation alone pushes you into higher tax brackets without real income growth.

Are Social Security benefits taxed by California?

No. California is one of the few states that does not tax Social Security benefits, regardless of your income level. This makes California relatively tax-friendly for retirees who live primarily on Social Security, pensions, and investment income (though investment income is still fully taxable).

What’s the difference between California taxable income and federal taxable income?

Start with your federal Adjusted Gross Income (AGI), then make California-specific adjustments. Common differences include adding back the federal QBI deduction, adjusting for different depreciation schedules, and modifying itemized deductions based on California rules. Your tax software should handle these automatically, but they explain why your California tax doesn’t simply equal a percentage of your federal tax.

California-Specific Considerations for 2026

California tax law changes frequently. These updates impact your 2026 filing:

Increased Filing Thresholds

For tax year 2026, single filers under age 65 must file a California return if their gross income exceeds $21,881. For married filing jointly (both under 65), the threshold is $43,762. These increased from 2025 due to inflation adjustments.

Pass-Through Entity Tax Election

California allows partnerships and S Corporations to elect to pay tax at the entity level (9.3% rate). Owners then claim a credit on their personal returns. This workaround helps business owners deduct more state tax on their federal return despite the $10,000 SALT cap. If you own a pass-through entity with multiple owners and combined income over $250,000, explore this with your tax advisor.

Wildfire Loss Deductions

California offers special deduction rules for taxpayers who suffered losses due to declared disasters, including wildfires. If you lost property in 2025-2026 disasters, you may qualify for expanded casualty loss deductions beyond what federal law allows. Document everything immediately, including FEMA claims and insurance settlements.

Book Your California Tax Strategy Session

Now you understand what is the state income tax in CA, but knowing the rates is just the beginning. The real question is whether you’re structured correctly to minimize what you pay while staying fully compliant with increasingly aggressive FTB enforcement.

With California’s top marginal rate hitting 13.3% and the FTB automating audit selection using the same technology that caught nearly a million federal taxpayers in 2025, proactive planning isn’t optional anymore. It’s financial defense.

Whether you’re worried about an FTB notice, trying to figure out estimated payments, or wondering if your business structure is costing you thousands in unnecessary state tax, our team has defended hundreds of California taxpayers and optimized entities for maximum legal tax savings. Book a personalized consultation with our California tax strategy team and get clear answers, compliant solutions, and confidence that you’re not overpaying. Click here to book your consultation now.

This information is current as of 6/9/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.