What Is a 1099-SA and Why It Matters for Self-Employed Taxpayers

You just received a sample 1099-SA in the mail, and you’re wondering if it’s something you need to worry about or if it’s just another form to file away. Here’s the truth: that single page could be the difference between claiming a legitimate tax deduction and triggering an IRS audit. Most self-employed taxpayers ignore the 1099-SA until they’re staring down a notice from the IRS, asking them to explain why they withdrew $8,500 from their Health Savings Account without documentation.

The sample 1099-SA isn’t just a receipt. It’s a direct report to the IRS that tells them exactly how much you pulled from your HSA, and whether those distributions were used for qualified medical expenses. If you can’t prove the money went toward legitimate healthcare costs, the IRS will reclassify that distribution as taxable income, plus hit you with a 20% penalty on top of your regular income tax rate.

Quick Answer

A 1099-SA form reports distributions from Health Savings Accounts (HSAs), Archer Medical Savings Accounts (MSAs), or Medicare Advantage MSAs. If you’re self-employed and withdrew money from your HSA in 2025, you’ll receive this form by January 31, 2026. The form shows the total amount distributed and the distribution code. You must keep receipts proving these withdrawals covered qualified medical expenses, or the IRS will tax the distribution as ordinary income and add a 20% penalty if you’re under 65.

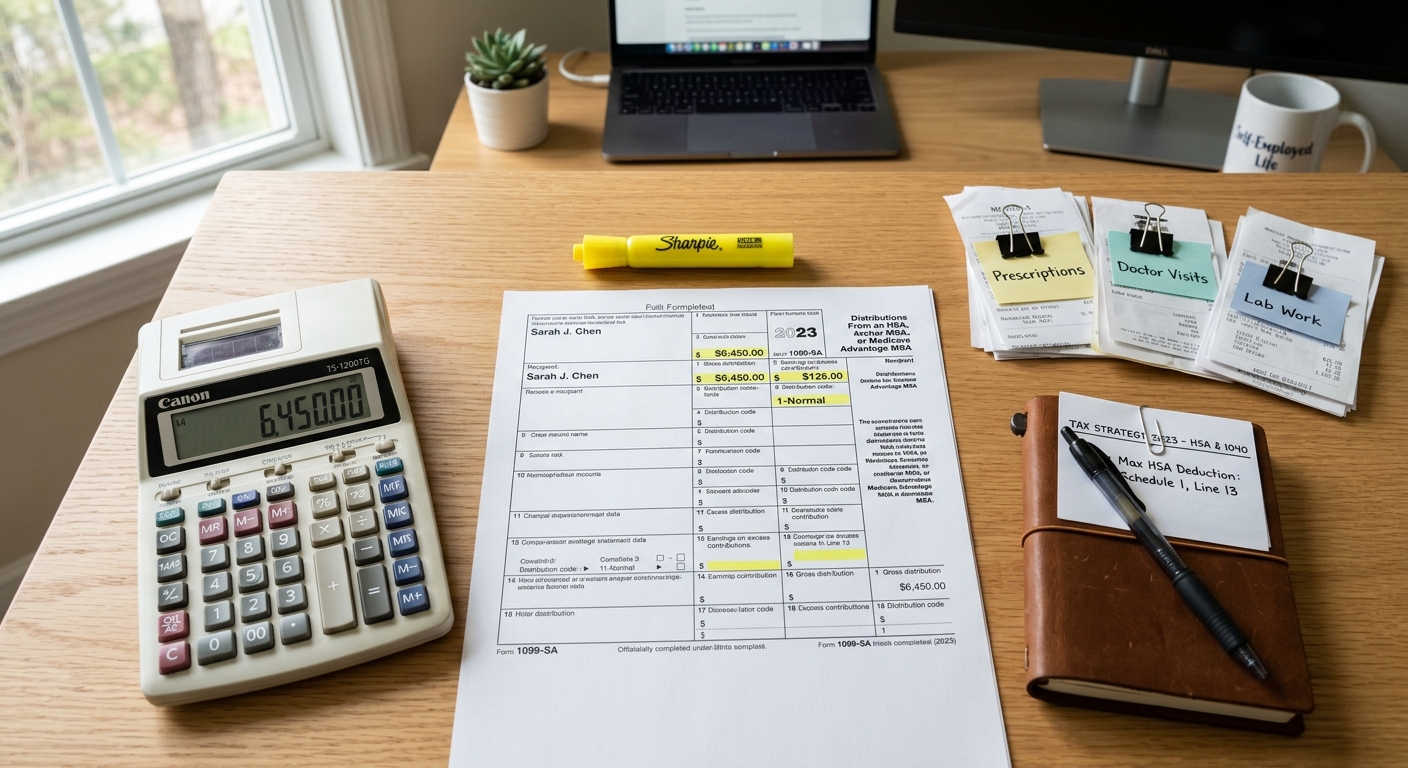

Understanding the 1099-SA Form Structure and Critical Box Entries

The 1099-SA contains seven critical boxes, but three of them will determine whether you owe additional taxes or walk away clean. Box 1 shows your gross distribution, which is the total amount you withdrew from your HSA during the tax year. This number goes directly to the IRS, so there’s no hiding it. Box 3 tells you what type of account the distribution came from using a single-digit code: 1 for HSA, 2 for Archer MSA, 3 for Medicare Advantage MSA. Box 5 is where things get serious. It shows the Fair Market Value of your HSA on the date of death if the account holder passed away during the year, which triggers estate and inheritance tax rules most people never see coming.

Here’s what most tax software won’t tell you: the 1099-SA doesn’t include a box that says “qualified” or “non-qualified.” That determination is on you. The IRS assumes all distributions are taxable unless you can prove otherwise with documentation. This is where self-employed taxpayers get burned. You pulled $4,200 from your HSA to cover dental work, physical therapy, and prescription medications. You receive the 1099-SA showing $4,200 in Box 1. But when April rolls around, you can’t find half the receipts. The IRS sees $4,200 in taxable income. You see a $1,260 tax bill you weren’t expecting, plus a $840 penalty because you’re 42 years old.

Distribution Codes and What They Actually Mean

Box 3 uses a numerical code system that determines which IRS publication you’ll need to reference when filing your return. Code 1 means you withdrew from a standard HSA, which follows the rules under IRS Publication 969. Code 2 applies to Archer MSAs, which have different contribution limits and qualification requirements. Code 3 covers Medicare Advantage MSAs, typically used by taxpayers over 65 enrolled in high-deductible Medicare plans. If you see Code 4, 5, or 6, you’re dealing with a death distribution, disability exception, or excess contribution correction, and you need professional help immediately because the tax treatment changes completely.

The distinction matters because each code triggers different tax forms and different penalty structures. An HSA distribution coded as 1 requires you to complete Form 8889 to report qualified and non-qualified distributions. An Archer MSA coded as 2 uses the same form but with different lines and calculation methods. Medicare Advantage MSA distributions coded as 3 may not require Form 8889 at all if you’re over 65 and using the funds for qualified medical expenses, because the age penalty no longer applies.

KDA Case Study: Self-Employed Consultant

Meet David, a 38-year-old self-employed marketing consultant earning $95,000 annually. In 2025, David contributed $4,300 to his HSA and withdrew $6,800 throughout the year to cover medical expenses. He received his 1099-SA in January 2026 showing the $6,800 distribution in Box 1 with Code 1 in Box 3. David kept some receipts but lost about 40% of them during a home office reorganization.

When David came to KDA, we immediately requested his HSA provider send duplicate statements showing every transaction. We matched his bank records to the HSA withdrawals and cross-referenced his insurance EOBs (Explanation of Benefits) to reconstruct missing receipts. We documented $6,200 in qualified medical expenses with verifiable proof. The remaining $600 became taxable income, which cost David $180 in federal tax and $120 in California state tax, plus a $120 penalty for non-qualified distribution.

Without professional help, David would have faced two choices: claim all $6,800 was qualified without proof (audit risk), or report the entire $6,800 as taxable income (costing him $2,040 in federal tax, $680 in state tax, and $1,360 in penalties). Our documentation process saved him $3,800 in unnecessary taxes and penalties. David paid $850 for our HSA reconstruction service, giving him a 4.5x first-year return on investment.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

The HSA Triple Tax Advantage and How the 1099-SA Fits In

Health Savings Accounts offer three distinct tax benefits that make them one of the most powerful tools available to self-employed taxpayers. First, contributions are tax-deductible. If you’re in the 24% federal bracket and contribute the 2026 maximum of $4,300 for self-only coverage, you’ll save $1,032 in federal taxes plus your state tax savings. Second, the money grows tax-free inside the account. Unlike a taxable brokerage account where you’d pay capital gains tax on growth, your HSA investments compound without annual tax drag. Third, distributions for qualified medical expenses are tax-free, which is where the 1099-SA comes into play.

The 1099-SA reports the third part of that equation: the tax-free distribution. But here’s the catch. The form itself doesn’t determine whether your distribution was actually tax-free. It just reports that you took the money out. You prove it was tax-free by keeping receipts, EOBs, and documentation that ties each withdrawal to a qualified medical expense as defined under IRS Publication 502. If you can’t prove it, the IRS assumes it wasn’t qualified and taxes you accordingly.

This is where self-employed taxpayers get strategic. You can contribute to your HSA, take the deduction, let the money grow, and then leave it untouched for years. Pay your current medical expenses out of pocket and keep the receipts. Ten years later, when you’re in a higher tax bracket or need a large cash infusion, you can reimburse yourself for those old medical expenses tax-free. The 1099-SA will show the distribution, but because you kept the receipts from 2026, the withdrawal in 2036 is still completely tax-free. There’s no statute of limitations on HSA reimbursements as long as the expense occurred after you established the HSA.

Qualified Medical Expenses: What Counts and What Doesn’t

The IRS defines qualified medical expenses in Publication 502, but the list is longer and more detailed than most people realize. Doctor visits, prescription medications, dental work, vision care, and hospital services obviously qualify. But so do acupuncture, chiropractor visits, smoking cessation programs, weight loss programs if prescribed by a doctor for a specific medical condition, and even certain home modifications if you have a disability. You can use HSA funds to pay insurance premiums if you’re receiving federal or state unemployment benefits, or to pay for COBRA continuation coverage, or to pay Medicare premiums once you turn 65.

What doesn’t count: gym memberships (unless prescribed for a specific medical condition), cosmetic procedures (unless medically necessary), vitamins and supplements (unless prescribed), and over-the-counter medications (unless you have a prescription). This last one trips up self-employed taxpayers constantly. You buy $200 worth of ibuprofen, allergy medication, and cold medicine from Costco. You pay with your HSA debit card. Your 1099-SA will show that $200 distribution. But unless you have a prescription from your doctor for each of those items, the IRS considers it a non-qualified distribution, and you’ll owe taxes plus the 20% penalty.

Documentation Requirements That Actually Hold Up Under IRS Scrutiny

The IRS doesn’t specify exactly what documentation you need to prove a qualified medical expense, which means you need to over-document rather than under-document. At minimum, keep the receipt showing the date of service, the provider name, the type of service, and the amount paid. Better yet, also keep the insurance EOB that shows how much your insurance paid, how much you paid, and what service code was billed. Best practice: keep a log in a spreadsheet that matches each HSA withdrawal to a specific medical expense with receipt numbers and filing locations.

If you’re audited, the IRS will ask you to prove that each dollar withdrawn from your HSA went toward a qualified medical expense. They won’t accept credit card statements. They won’t accept bank records. They want receipts and EOBs. If you paid with an HSA debit card, they’ll want to see that the merchant was a healthcare provider. If you wrote yourself a reimbursement check from the HSA, they’ll want to see the original out-of-pocket receipt proving you paid for qualified care before reimbursing yourself.

How to Handle Non-Qualified Distributions on Your Tax Return

If you withdrew money from your HSA for non-qualified expenses, you can’t just ignore the 1099-SA and hope the IRS doesn’t notice. The form goes to them automatically, and their matching system will flag your return if you don’t report it correctly. You need to complete Form 8889, which is the HSA reporting form that reconciles your contributions, distributions, and account balance. Part II of Form 8889 is where you report distributions, both qualified and non-qualified.

Line 14a asks for your total distributions from all HSAs, which comes directly from Box 1 of your 1099-SA. Line 14b asks for the amount you used for qualified medical expenses. The difference between 14a and 14b flows to Line 15, which becomes taxable income. That taxable income gets added to Line 16 of your Form 8889 and eventually lands on Schedule 1 of your Form 1040 as additional income. Then Line 17 of Form 8889 calculates the 20% additional tax penalty on the non-qualified distribution, which also flows to Schedule 2 of your 1040.

Here’s a real-world example with actual numbers. You’re 45 years old, self-employed, and you withdrew $7,000 from your HSA in 2025. You can prove $5,500 was for qualified medical expenses, but $1,500 went toward a gym membership and supplements. Your Form 8889 would show $7,000 on Line 14a, $5,500 on Line 14b, and $1,500 on Line 15 as taxable income. If you’re in the 22% federal bracket, that $1,500 costs you $330 in income tax. Line 17 adds another $300 penalty (20% of $1,500). Total tax hit: $630, plus whatever your state charges on that additional $1,500 of income.

Strategic HSA Management for Self-Employed Taxpayers

If you’re self-employed and enrolled in a high-deductible health plan, you should be maxing out your HSA contribution every single year. The 2026 limits are $4,300 for self-only coverage and $8,550 for family coverage. If you’re 55 or older, you can add an extra $1,000 catch-up contribution. That contribution is fully deductible on the front page of your Form 1040, which means it reduces your taxable income even if you take the standard deduction. It’s one of the few remaining above-the-line deductions available to self-employed individuals.

The strategic move is to contribute the maximum, invest the HSA funds in low-cost index funds rather than leaving them in cash, and then pay your current medical expenses out of pocket while keeping all receipts. Your HSA becomes a stealth retirement account that grows tax-free, and you can reimburse yourself decades later when you need the cash or when you’re in a lower tax bracket. This strategy works because there’s no time limit on HSA reimbursements. As long as the medical expense occurred after you established the HSA, you can reimburse yourself 30 years later and the distribution is still tax-free.

Need help optimizing your HSA strategy as a self-employed taxpayer? Our tax planning services include comprehensive HSA management and documentation systems designed specifically for 1099 workers and business owners.

HSA Contribution Limits vs Distribution Timing

One mistake self-employed taxpayers make is thinking they can only withdraw what they contributed in the same year. That’s not how HSAs work. If you’ve been contributing for five years and your account balance is $18,000, you can withdraw $8,000 in a single year for qualified medical expenses without any tax consequence. The 1099-SA will show $8,000, but as long as you have receipts proving qualified expenses, there’s no additional tax. The contribution limits control how much you can put in each year. The distribution rules control how you take money out. These are two separate calculations.

However, if you’re just starting your HSA and you contribute $4,300 but then withdraw $6,000 in the same year, you have a problem. You can’t withdraw more than your account balance. If your account balance only has $4,300, you can only withdraw $4,300. The HSA custodian won’t let you overdraw the account like a checking account. But if you contribute $4,300, it grows to $4,500, and you withdraw $4,500, your 1099-SA shows $4,500. All of that can be tax-free if you have qualified medical expenses to cover it.

State Tax Treatment of HSA Distributions

Most states follow federal tax treatment of HSAs, which means contributions are deductible, growth is tax-free, and qualified distributions are tax-free. But California and New Jersey don’t conform to federal HSA rules. If you’re a self-employed California resident, your HSA contributions are not deductible on your California state return. You’ll get the federal deduction, but California will add that contribution back as income on your state return. On the flip side, when you take distributions, California doesn’t tax qualified HSA distributions because you never got the deduction to begin with.

This creates a documentation problem for California taxpayers. Your 1099-SA shows up, and you need to track qualified vs non-qualified distributions for federal purposes. But for California purposes, you need to track your total basis in the account (all contributions that were taxed by California) so you can prove to the Franchise Tax Board that your distributions shouldn’t be taxed a second time. You’ll need to complete FTB Form 3853 to report HSA activity on your California return, which requires you to maintain parallel records for federal and state reporting.

Common 1099-SA Mistakes That Trigger IRS Audits

The most common mistake is not reporting the 1099-SA at all. The IRS receives a copy automatically. If you don’t report it on your return, their matching system flags your account and sends you a CP2000 notice asking why you didn’t report the income. Even if the entire distribution was for qualified medical expenses, you still need to report it on Form 8889 to show the IRS that it was qualified. Not reporting it at all makes the IRS assume the worst: that you took the money for non-qualified purposes and tried to hide it.

Second mistake: claiming the entire distribution was qualified when you don’t have receipts to back it up. If you’re audited and can’t prove the expenses, the IRS will reclassify the entire distribution as taxable income and add the 20% penalty. The burden of proof is on you, not the IRS. They don’t have to prove it wasn’t qualified. You have to prove it was. This is why HSA users need to implement a documentation system immediately, not scramble to find receipts when the 1099-SA arrives.

Red Flag Alert: Multiple HSAs and Multiple 1099-SA Forms

If you changed jobs, switched HSA custodians, or had multiple HSAs in the same year, you’ll receive multiple 1099-SA forms. Each custodian reports their distributions separately. You need to add up all the distributions from all the forms and report the total on Line 14a of Form 8889. Taxpayers often make the mistake of only reporting one form and forgetting about the others. The IRS sees all of them and will send you a notice if the numbers don’t match.

Another issue: if you rolled over money from one HSA to another, that transfer might generate a 1099-SA showing a distribution from the old account. If the rollover was done correctly (direct trustee-to-trustee transfer within 60 days), it’s not a taxable distribution. But you still need to report it on Form 8889 and indicate it was a rollover. If you missed the 60-day window, the IRS treats it as a distribution from the old account and a contribution to the new account, which could cause you to exceed contribution limits and trigger an excess contribution penalty of 6% per year until you remove the excess.

What to Do If You Receive an Incorrect 1099-SA

Sometimes the HSA custodian makes a mistake. They report the wrong distribution amount, use the wrong code in Box 3, or include distributions from the prior year instead of the current year. If you receive a 1099-SA that you know is wrong, contact the custodian immediately and request a corrected form (Form 1099-SA marked “CORRECTED” in the top right corner). Don’t file your tax return using the wrong information just because that’s what the form says. The IRS will match your return against their records, and if the custodian later issues a corrected form, you’ll receive a notice asking you to explain the discrepancy.

If the custodian refuses to issue a corrected form, or if you can’t resolve the issue before the tax filing deadline, you have two options. First, you can file your return with the correct information and attach a statement explaining why your reported amounts differ from the 1099-SA. The IRS calls this “taxpayer statement override,” and while it doesn’t guarantee they won’t follow up, it shows good faith effort to report accurately. Second, you can file using the incorrect 1099-SA information and then immediately file Form 1040-X (amended return) once you receive the corrected form. This keeps you in compliance with filing deadlines while fixing the error.

HSA Distributions After Age 65: The Medicare Transition

Once you turn 65, the penalty for non-qualified HSA distributions disappears. You can withdraw money from your HSA for any reason, pay ordinary income tax on it, but avoid the 20% penalty. This makes the HSA function like a traditional IRA after age 65. However, qualified medical expenses are still tax-free, which is better than an IRA where all distributions are taxed as ordinary income. This is why many retirees use their HSA as a last-resort funding source, preferring to tap Social Security, pensions, and IRAs first while letting the HSA continue growing tax-free for future healthcare costs.

One trap: if you enroll in Medicare, you can no longer contribute to your HSA. The month you enroll in any part of Medicare (Part A, B, C, or D), you lose HSA eligibility. However, you can still use the funds already in your HSA for qualified medical expenses tax-free. This includes Medicare premiums (except Medigap premiums), which are considered qualified medical expenses once you’re 65. Your 1099-SA after age 65 might show distributions used to pay Medicare Part B and Part D premiums, and those are fully tax-free even though they weren’t available as qualified expenses before you turned 65.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About the 1099-SA

Do I need to attach my 1099-SA to my tax return when I file?

No. The 1099-SA is an information reporting form, and you don’t attach it to your return. You use the information from the form to complete Form 8889, which you do attach to your Form 1040. Keep the 1099-SA in your tax records in case of an audit, but don’t mail it to the IRS with your return. If you e-file, the information from Form 8889 is transmitted electronically.

What happens if I don’t receive a 1099-SA but I know I took distributions?

Contact your HSA custodian immediately. They’re required to send you a 1099-SA by January 31 if you had any distributions during the prior year. If they haven’t sent it, either their records are wrong, or the form was lost in the mail. You still need to report the distributions on your tax return even if you didn’t receive the form, because the IRS got their copy. Use your HSA account statements to determine the total distributions and report them on Form 8889.

Can I use my HSA to pay for my spouse’s medical expenses even though the HSA is in my name?

Yes. If you’re legally married and file jointly, you can use your HSA to pay for your spouse’s qualified medical expenses tax-free. The distribution is still reported on your 1099-SA under your name, but the expenses count as qualified as long as your spouse meets the definition of a dependent. This also applies to children and other dependents claimed on your tax return. The 1099-SA doesn’t show whose medical expenses you paid, just that you took a distribution. You prove the expenses were qualified by keeping receipts.

If I use my HSA debit card at a non-medical merchant, will that automatically trigger an audit?

Not automatically, but it increases your audit risk if you can’t prove the purchase was for qualified medical expenses. HSA custodians don’t police every transaction. They report the total distributions on your 1099-SA regardless of where you spent the money. However, some custodians flag suspicious transactions and may request receipts from you before the year ends. If you used your HSA debit card at Target or Amazon, you’ll need to prove that you bought medical supplies, not groceries or electronics. Keep the itemized receipt showing exactly what you purchased, not just the credit card slip showing the total.

How long should I keep my HSA receipts and 1099-SA forms?

The IRS recommends keeping tax records for at least three years, which is the standard statute of limitations for audits. However, with HSA distributions, you should keep receipts indefinitely if you’re using the reimbursement strategy (paying expenses out of pocket and reimbursing yourself years later). There’s no time limit on HSA reimbursements, so you need to maintain proof of the original expense for as long as you plan to take the reimbursement. Keep the 1099-SA forms for at least seven years to cover extended audit periods and to document your distribution history.

Stop Guessing and Start Documenting Your HSA Strategy

The sample 1099-SA is more than just another tax form. It’s the IRS’s direct line into your health savings account activity, and if you can’t prove every dollar withdrawn was for qualified medical expenses, you’ll pay the price in additional taxes and penalties. Self-employed taxpayers have enough on their plate without worrying about HSA documentation failures that could have been avoided with proper planning.

At KDA, we build HSA management systems for self-employed clients that track contributions, distributions, receipts, and reimbursement timing to maximize tax savings while minimizing audit risk. If you received a 1099-SA and you’re not sure whether your distributions will pass IRS scrutiny, we can help you reconstruct documentation, calculate potential tax exposure, and develop a strategy to protect future distributions.

This information is current as of 6/8/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.

Get Your HSA Documentation System Built Right

If you’re self-employed and using an HSA, you need a system that documents every transaction before the 1099-SA arrives, not after. Let’s build you a compliance framework that protects your deductions and eliminates audit risk. Book your HSA strategy consultation now and stop leaving money on the table while exposing yourself to IRS penalties.