What You’re Really Paying in California: The 2024 Tax Brackets Married Couples Need to Know

If you filed jointly in California for 2024, you didn’t just pay one tax rate. You paid multiple rates stacked on top of each other, and most married couples have no idea where their actual income landed. The difference between understanding 2024 california tax brackets married filing jointly and just guessing? Anywhere from $2,000 to $15,000 in overpaid taxes.

Here’s what trips people up: California uses a progressive tax system. Your first dollar is taxed differently than your 80,000th dollar. And because California’s brackets don’t match the federal system, you can’t assume your federal rate tells the whole story. This isn’t about tax avoidance. It’s about knowing exactly what you owe, when you owe it, and how to structure your income so you’re not surprised come April.

Quick Answer

2024 California tax brackets for married filing jointly range from 1% on the first $20,198 of taxable income to 13.3% on income over $1,354,550. Unlike federal brackets, California has 10 income tiers, meaning your effective rate depends entirely on where your total taxable income lands. For a married couple earning $150,000, you’ll pay approximately $10,939 in state tax before deductions or credits.

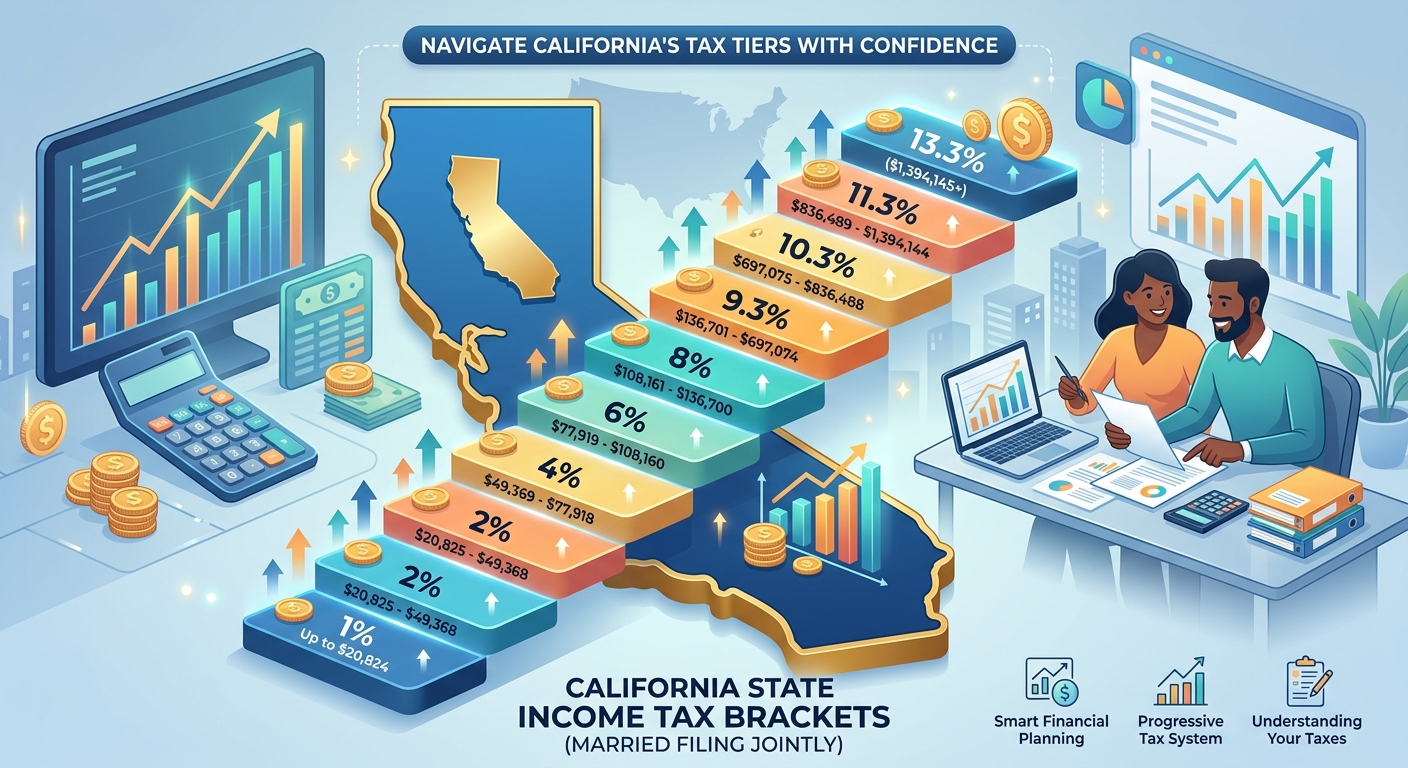

The Complete 2024 California Tax Bracket Breakdown for Married Couples

Let’s get specific. California divides taxable income into ten brackets for married couples filing jointly in 2024. Each bracket applies a different rate to the portion of income that falls within that range.

2024 California Tax Brackets: Married Filing Jointly

| Taxable Income Range | Tax Rate | Tax Owed on This Bracket |

|---|---|---|

| $0 to $20,198 | 1% | Up to $202 |

| $20,199 to $47,884 | 2% | $202 to $756 |

| $47,885 to $75,576 | 4% | $756 to $1,864 |

| $75,577 to $104,910 | 6% | $1,864 to $3,624 |

| $104,911 to $132,590 | 8% | $3,624 to $5,838 |

| $132,591 to $677,278 | 9.3% | $5,838 to $56,494 |

| $677,279 to $812,728 | 10.3% | $56,494 to $70,445 |

| $812,729 to $1,000,000 | 11.3% | $70,445 to $91,607 |

| $1,000,001 to $1,354,550 | 12.3% | $91,607 to $135,217 |

| Over $1,354,550 | 13.3% | $135,217+ |

Notice the jump from 9.3% to 10.3% once you cross $677,278. That’s where California’s “millionaire tax” structure starts kicking in. But even middle-income earners feel the bite. A couple earning $105,000 crosses five different tax brackets before they’re done.

How California’s Brackets Actually Work: A Real-World Example

Let’s say you and your spouse earned $120,000 in taxable income in 2024 after deductions. Here’s exactly how California calculates your state tax bill:

- First $20,198 at 1% = $202

- Next $27,686 ($20,199 to $47,884) at 2% = $554

- Next $27,692 ($47,885 to $75,576) at 4% = $1,108

- Next $29,334 ($75,577 to $104,910) at 6% = $1,760

- Remaining $15,090 ($104,911 to $120,000) at 8% = $1,207

Total California tax owed: $4,831

Your effective rate? About 4.03%. But your marginal rate is 8%, meaning every additional dollar you earn is taxed at that higher rate until you hit the next bracket at $132,590.

What Married Couples Miss: The Marginal vs. Effective Rate Trap

Here’s where it gets expensive. Your marginal rate is what you pay on your last dollar earned. Your effective rate is your total tax divided by total income. Most couples focus on effective rate and ignore marginal rate when making financial decisions.

That $10,000 bonus your employer offers? If you’re already at $115,000 in taxable income, you’re paying 8% California tax on that bonus, plus federal tax, plus Social Security and Medicare. Suddenly that $10,000 bonus nets you closer to $6,200.

Why This Matters for Year-End Planning

If you’re hovering near a bracket threshold in late December, you have options. Accelerate deductions into the current year. Defer income into the next year. Max out retirement contributions to bring your taxable income down. A married couple earning $133,000 could save $279 in state tax alone by contributing an extra $5,000 to a traditional IRA before year-end, dropping them from the 9.3% bracket back to the 8% bracket.

KDA Case Study: High-Income Married Couple

David and Jennifer, both tech professionals in San Jose, earned $685,000 combined in 2024. They had no idea they were sitting right at the edge of California’s 10.3% bracket threshold. When they came to KDA, they were on track to pay $59,847 in California state tax.

We restructured their compensation strategy. David negotiated a deferred comp arrangement for $50,000 of his year-end bonus, pushing that income into 2025. Jennifer maxed out her 401(k) and contributed to a backdoor Roth. We also identified $18,000 in overlooked business expenses from Jennifer’s side consulting work.

Result: Their 2024 California taxable income dropped to $617,000. They avoided crossing into the 10.3% bracket entirely, saving $7,015 in state tax. They paid KDA $3,200 for planning and execution. First-year ROI: 2.2x.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

Federal vs. California Brackets: Why You Can’t Use the Same Strategy for Both

The IRS uses seven tax brackets. California uses ten. The federal standard deduction for married couples in 2024 is $29,200. California’s? Only $10,404. That means you’re working with a much smaller cushion before California starts taxing your income.

And here’s the kicker: California doesn’t conform to all federal tax law changes. While the federal Tax Cuts and Jobs Act capped state and local tax deductions at $10,000, California never adopted that limitation for state purposes. If you’re itemizing on your California return, you can still deduct the full amount of property taxes and state income taxes paid.

The SALT Deduction Advantage for California Filers

For married couples who own property in California, this is huge. Let’s say you paid $14,000 in property taxes and $8,000 in state income tax in 2024. On your federal return, you’re capped at deducting $10,000. But on your California return, you can deduct the full $22,000 (if you’re itemizing). That reduces your California taxable income and potentially drops you into a lower bracket.

According to IRS Publication 17, itemized deductions must be allocated correctly between federal and state returns. Many tax software programs don’t automatically adjust for California’s non-conformity, which means you could be leaving money on the table if you’re not reviewing the calculations manually.

How to Calculate Your 2024 California Tax Liability Step-by-Step

Don’t wait until tax season to figure out what you owe. Here’s how to estimate your California tax bill right now:

Step 1: Determine Your Gross Income

Add up all income sources: W-2 wages, 1099 income, business profit, rental income, investment gains, retirement distributions. This is your starting point.

Step 2: Subtract Above-the-Line Deductions

California allows certain deductions before you calculate adjusted gross income (AGI). These include traditional IRA contributions (up to $6,500 for 2024, or $7,500 if you’re 50 or older), HSA contributions (up to $8,300 for family coverage), and self-employment tax deduction (50% of SE tax paid).

Step 3: Apply Standard or Itemized Deduction

For 2024, married couples filing jointly get a $10,404 standard deduction in California. If your itemized deductions (mortgage interest, property taxes, charitable contributions, medical expenses over 7.5% of AGI) exceed that amount, itemize. Otherwise, take the standard.

Step 4: Calculate Tax Using the Bracket Table

Use the bracket table above to calculate tax on each income layer. This is your baseline California tax liability before credits.

Step 5: Apply Tax Credits

California offers credits for renters ($120 per person), dependent children, child care expenses, and low-income households. These reduce your tax bill dollar-for-dollar. Check the FTB Form 540 instructions for a complete list of available credits for 2024.

Special Situations: What Changes Your California Tax Bracket

Your bracket isn’t static. Life events and income changes can push you up or down throughout the year. Here are the most common scenarios that alter your California tax picture:

Stock Option Exercises and RSU Vesting

Tech workers, listen up. When your restricted stock units vest or you exercise stock options, that income counts as ordinary income in the year it’s realized. If you vest $80,000 in RSUs and your base salary is $150,000, your California taxable income jumps to $230,000, pushing you well into the 9.3% bracket.

Strategy: If you have control over exercise timing, consider spreading exercises across multiple years to avoid bracket creep. Incentive stock options (ISOs) have different rules than non-qualified stock options (NQSOs). ISOs don’t trigger regular tax at exercise but can create AMT liability. California follows federal AMT calculations but with different rates and exemptions.

Bonus Income and Irregular Compensation

Bonuses, commissions, and severance payments all count as ordinary income. California doesn’t have special withholding rates for supplemental wages like the federal government does. Your employer might withhold at a flat 22% federally, but California withholding depends on your W-4 elections and estimated annual income.

If you’re expecting a $25,000 bonus and you’re already at $180,000 in income, you’re paying 9.3% California tax on that entire bonus. That’s $2,325 in state tax alone.

Capital Gains Treatment in California

Here’s a painful truth: California taxes long-term capital gains at the same rates as ordinary income. There’s no preferential rate like the 15% or 20% federal long-term capital gains rate. If you’re in the 9.3% California bracket and you sell stock you’ve held for five years, you’re paying 9.3% to California on that gain, regardless of how long you held it.

This makes tax-loss harvesting and timing of asset sales critical for California residents. Selling $100,000 in appreciated stock when you’re already at $150,000 in income means you’re paying an additional $9,300 to California, on top of federal tax and the 3.8% net investment income tax if you exceed the threshold.

Red Flag Alert: Common Bracket Mistakes That Trigger Audits

The California Franchise Tax Board is aggressive. Certain income reporting errors or deduction claims can flag your return for review. Here’s what to avoid:

Underreporting Income from Multiple Sources

If you have W-2 income, 1099 income, and investment income, make sure every dollar is accounted for. The FTB receives copies of all your 1099s and W-2s. If your reported income doesn’t match what they have on file, expect a letter. California’s automated income matching system caught over 1.2 million discrepancies in 2023 alone.

Overstating Itemized Deductions Without Documentation

Claiming $40,000 in charitable contributions on $120,000 of income? You better have receipts. The FTB cross-references itemized deductions against income levels and flags outliers. For any single charitable contribution over $250, you need a written acknowledgment from the charity. For non-cash donations over $500, you need to file Form 8283.

Failing to Report Out-of-State Income

California residents pay California tax on all income, regardless of where it’s earned. If you worked remotely for a Texas company while living in Los Angeles, that income is taxable in California. The FTB has become especially vigilant about remote work income post-pandemic. Report all income sources accurately and claim credit for taxes paid to other states on Schedule S.

How Business Owners in California Navigate the Bracket System

If you run an LLC, S Corp, or sole proprietorship in California, your business income flows through to your personal return. That means your business profit gets added to your spouse’s W-2 income, and the combined total determines your bracket.

A married couple where one spouse earns $90,000 as a W-2 employee and the other runs a consulting business that nets $60,000 has a combined taxable income of $150,000 (before deductions). They’re paying California tax at rates ranging from 1% to 9.3% on that combined income.

The S Corp Salary Strategy for California Filers

Here’s where entity structure matters. If you operate as an LLC taxed as a sole proprietorship, all your net profit is subject to self-employment tax (15.3% for Social Security and Medicare). But California doesn’t have a separate self-employment tax beyond the federal obligation.

If you elect S Corp status, you split income into salary and distributions. You pay payroll taxes on salary, but distributions avoid the 15.3% self-employment tax. However, you’re still paying California income tax on all of it, salary and distributions combined.

Example: Miguel runs a digital marketing agency as an S Corp. He pays himself a $70,000 salary and takes $50,000 in distributions. For federal purposes, he saves about $7,650 in self-employment tax on the distribution portion (15.3% x $50,000). For California purposes, all $120,000 counts as taxable income subject to the bracket rates. His California tax bill doesn’t change based on the salary vs. distribution split, but his federal bill does.

Want expert help optimizing your entity structure? Check out our tax planning services to see how we help business owners save thousands through strategic entity selection and income timing.

What Happens If You’re On the Bracket Edge

Let’s say you’re at $104,500 in taxable income. You’re $410 away from jumping into the 8% bracket. Should you care?

Absolutely. That next $410 will be taxed at 6%. But dollar 104,911 and beyond gets hit at 8%. If you can defer $5,000 of income to next year or accelerate $5,000 in deductions into this year, you stay in the 6% zone and save $100 in state tax on that $5,000 chunk (2% difference x $5,000).

Multiply that across multiple years and multiple income sources, and bracket management becomes a core tax strategy, not an afterthought.

Timing Deductions to Maximize Bracket Benefits

You have more control than you think. Property tax payments, charitable contributions, medical expenses, and retirement contributions can all be timed to your advantage.

If you’re going to owe $6,000 in property taxes in January 2025, consider paying it in December 2024 if you’re itemizing and you want to reduce your 2024 taxable income. California allows you to deduct property taxes in the year paid, as long as they’re not penalties or fees.

Similarly, if you’re planning a $10,000 charitable donation, consider whether making it in December 2024 vs. January 2025 will have a bigger tax impact based on your expected income for each year. The goal: keep your taxable income in the lowest possible bracket each year.

Estimated Tax Payments: How Brackets Affect Your Quarterly Obligation

California requires estimated tax payments if you expect to owe more than $500 in state tax after withholding and credits. Your bracket determines how much you should be paying each quarter.

If you’re married filing jointly with $150,000 in expected 2024 income, your estimated California tax liability is around $10,939. Subtract any withholding from W-2s, and the remainder should be divided into four quarterly payments due April 15, June 15, September 15, and January 15.

Miss a payment or underpay? California charges penalties and interest. The underpayment penalty is based on the amount you owe and how late you paid. For 2024, the interest rate on underpayments is 5% annually, compounded daily.

Safe Harbor Rules to Avoid Penalties

California’s safe harbor rule: if you pay 90% of your current year tax liability or 100% of your prior year tax liability (110% if your prior year AGI exceeded $150,000), you avoid underpayment penalties. This is critical if your income is volatile or you have large one-time gains in a given year.

If you earned $120,000 in 2023 and owed $5,000 in California tax, you can pay $5,500 in estimated taxes for 2024 (110% of prior year) and avoid penalties, even if your 2024 income jumps to $200,000 and your actual liability ends up being $15,000. You’ll owe the difference at filing, but no penalties.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently Asked Questions About California Tax Brackets for Married Couples

Do California tax brackets change every year?

Yes. California adjusts tax brackets annually for inflation. The inflation adjustment for 2024 was approximately 3.1%, which is why the bracket thresholds increased slightly from 2023 levels. Always verify the current year brackets at the California Franchise Tax Board website before calculating your liability.

How do California brackets compare to other high-tax states?

California has the highest top marginal rate in the nation at 13.3%. New York’s top rate is 10.9%. New Jersey tops out at 10.75%. But the real difference is where those top rates kick in. California’s 9.3% bracket starts at just $132,591 for married filers, while New York’s 6.85% bracket doesn’t start until $161,550. For middle and upper-middle income earners, California’s tax burden is measurably higher.

Can I reduce my California tax bracket by moving income to my spouse?

No. When you file jointly, all income is combined regardless of who earned it. The brackets apply to total household income. However, there are scenarios where filing separately might result in lower combined tax, particularly if one spouse has high medical expenses or miscellaneous deductions subject to AGI thresholds. Run the numbers both ways before deciding.

What if I moved to California mid-year?

You’ll file as a part-year resident. California only taxes the income you earned while a California resident, plus any California-source income earned while a non-resident. You’ll use Form 540NR and allocate income by source and residency period. Your tax is calculated on a prorated basis, but the brackets still apply to your California taxable income for the portion of the year you were a resident.

How does the Alternative Minimum Tax affect my California brackets?

California has its own AMT system separate from federal AMT. If you have large deductions for state taxes, property taxes, or certain business expenses, you might trigger California AMT. The AMT rate for married couples is 7% on AMT income up to $221,492 and 9.3% above that threshold. You pay whichever is higher: regular tax or AMT. Check the FTB’s AMT worksheet on Form 540 to see if you’re affected.

What’s the benefit of maxing out retirement contributions if I’m in a high California bracket?

Every dollar you contribute to a traditional 401(k) or traditional IRA reduces your California taxable income. If you’re in the 9.3% bracket, a $6,500 IRA contribution saves you $604.50 in California tax alone, plus federal savings. Over time, that’s significant. California allows deductions for traditional retirement contributions, but not for Roth contributions, since Roth contributions are made with after-tax money.

Are there any California tax credits that can reduce my bracket liability?

Tax credits don’t change your bracket, but they reduce your tax bill directly. California offers the Earned Income Tax Credit (CalEITC) for low-to-moderate income earners, the Young Child Tax Credit for families with kids under 6, and the Renter’s Credit ($120 per qualified person). These are non-refundable or partially refundable, depending on the credit. Check your eligibility each year.

If I receive unemployment benefits in California, how are they taxed?

Unemployment benefits are fully taxable for California purposes, just like they are federally. If you received $15,000 in unemployment in 2024, that’s added to your total income and taxed according to your bracket. California does not have an exclusion for unemployment like the federal government temporarily offered during the pandemic.

Book Your California Tax Strategy Session

If you’re tired of guessing what you owe and overpaying because you don’t have a clear bracket strategy, it’s time to get precise. Understanding exactly where your income falls, how to time deductions, and when to accelerate or defer income can save you thousands every year. Book a personalized consultation with our California tax strategy team and get a clear roadmap for your 2024 return and beyond. Click here to book your consultation now.

This information is current as of 6/6/2026. Tax laws change frequently. Verify updates with the IRS or FTB if reading this later.