This blog explains the **what is the difference between s-corp and c-corp** question in practical, dollar terms so you can choose the structure that actually keeps more money in your pocket instead of the IRS taking the first cut. If you are a W-2 employee with a growing side business, a 1099 consultant, or you own an LLC that is finally profitable, this is for you.

Quick answer: S corporations are usually better for small, closely held businesses that want to avoid double taxation and reduce self-employment tax by splitting profit between salary and distributions. C corporations are generally better when you plan to reinvest profits, bring in outside investors, or eventually go public, but they expose you to corporate tax plus potential tax again on dividends.

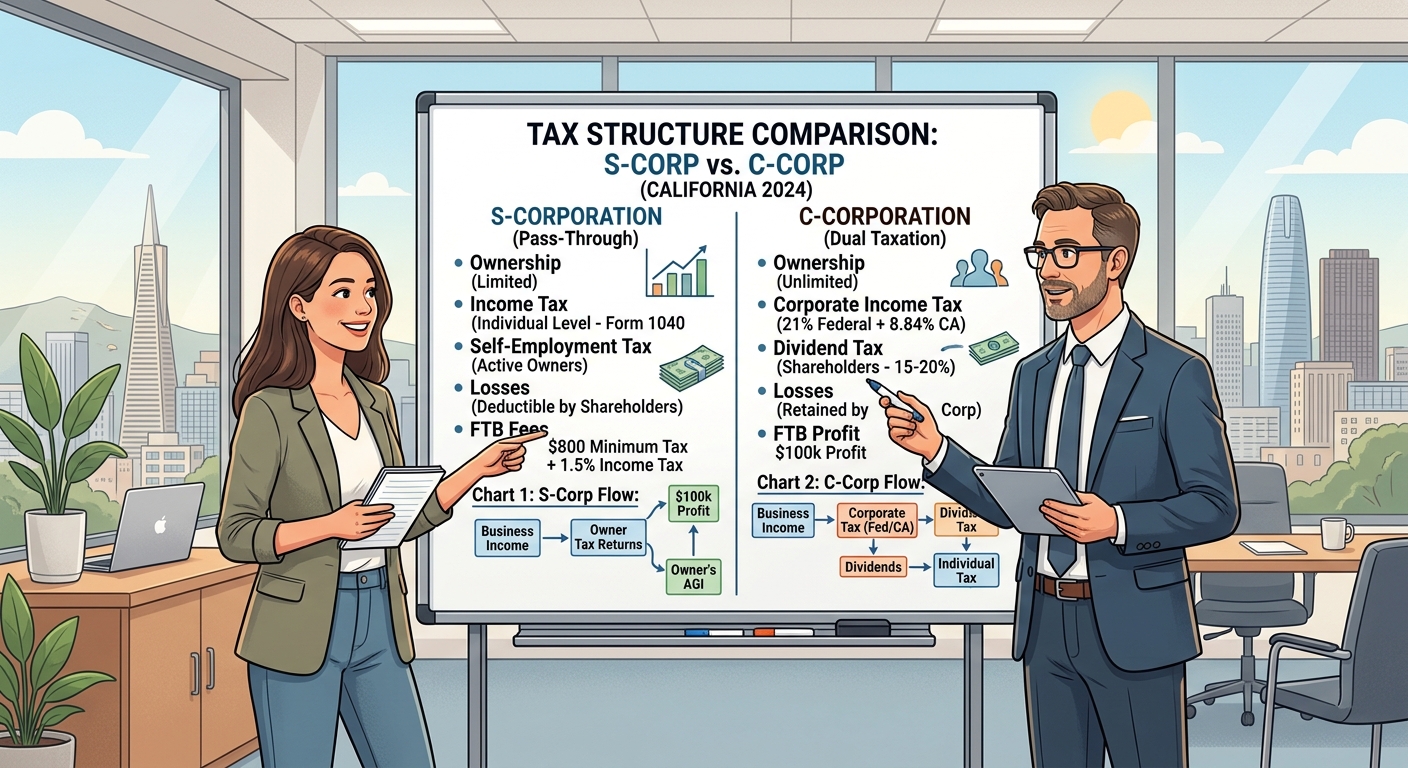

Breaking down what is the difference between s-corp and c-corp in plain English

On paper, S corporations and C corporations look similar. Both are corporations created under state law. Both give you limited liability. Both can pay you a W-2 salary. The real separation shows up in how the IRS taxes profits, how you take money out, and what happens as your income climbs.

At the federal level, C corporations pay tax at a flat corporate rate under Internal Revenue Code Section 11. Then shareholders may pay tax again when the company distributes profits as dividends. That is the classic “double tax” problem.

S corporations do not pay federal income tax in most situations. Instead, they are treated as pass-through entities under Subchapter S of the Code. The corporation files Form 1120-S, then passes income, deductions, and credits to shareholders on Schedule K-1, which gets reported on each owner’s Form 1040. The income is taxed once at the shareholder level.

California adds its own twist. C corporations doing business in California generally pay the 8.84 percent corporate tax on net income, plus the annual minimum franchise tax. S corporations pay a 1.5 percent California tax on net income at the entity level, and then shareholders still pay California personal income tax on their share. So even with an S corporation, you need to factor in that state-level bite.

If you want a deeper dive on California S corporation tactics such as reasonable salary, distributions, and multi-entity structures, see our comprehensive S corporation tax guide for California owners.

Numerical example: Same profit, different tax results

Assume your business has $200,000 in profit before any owner salary.

- Scenario A: C corporation. The corporation pays you a $100,000 salary and leaves $100,000 of profit inside the company. The $100,000 salary is deductible to the corporation and taxed to you as W-2 income. The $100,000 retained profit is taxed at the 21 percent federal corporate rate, or $21,000. If the company later distributes that $79,000 after-tax profit as a dividend, you may owe another 15 percent to 23.8 percent federal tax on that dividend, plus state tax. It is easy to see $30,000 or more go out the door over time.

- Scenario B: S corporation. The S corporation also pays you a $100,000 salary. The remaining $100,000 shows up on your Schedule K-1 as pass-through income. You still pay federal and California income tax on that $100,000, but that pass-through portion is not subject to federal self-employment tax. Depending on your other income and deductions, the tax difference between an S and a C corporation on this same $200,000 can easily exceed $10,000 per year.

According to IRS Publication 542, corporations have wide flexibility in timing and character of income. Your job is to use that flexibility in your favor, not the government’s.

How S corporations actually save self-employment tax

The biggest practical reason small business owners care about what is the difference between s-corp and c-corp is self-employment tax. If you operate as a sole proprietor or a single-member LLC taxed as a disregarded entity, you pay self-employment tax on your net profit. That is 15.3 percent on roughly the first $160,000 of combined wages and self-employment income for Social Security and Medicare, plus 2.9 percent Medicare on top of that, and an additional 0.9 percent Medicare surtax for high earners.

In an S corporation you pay yourself a “reasonable salary” as a W-2 employee. That salary is subject to payroll taxes, just like any job. But any remaining profit can be distributed as a dividend-like S corporation distribution that is not subject to self-employment tax. The IRS explains this distinction in its S corporation guidance.

Example: Consultant cutting self-employment tax with an S corporation

Maria is a 1099 software engineer in California netting $180,000 per year as a sole proprietor. She files Schedule C and pays self-employment tax on the full $180,000. Just the self-employment tax alone is around $25,000.

With planning, she forms a California corporation, then elects S corporation status using Form 2553. Based on her role and market data, she pays herself a $110,000 W-2 salary. The remaining $70,000 is S corporation profit distributed to her as an owner.

- Payroll tax applies only to the $110,000 salary.

- The $70,000 distribution avoids the 15.3 percent self-employment tax.

- Even after factoring in California’s 1.5 percent S corporation tax at the entity level, Maria can often save $8,000 to $10,000 per year in payroll-related taxes.

These kinds of structures require clean books and strong payroll processes. Many self-employed professionals discover they need professional help once revenue passes roughly $150,000 and the self-employment tax bill starts to sting.

If you want a quick sense of how an S corporation could affect your numbers, plug your projected profit into this small business tax calculator and compare sole proprietor, S corporation, and C corporation scenarios.

Reasonable salary is nonnegotiable

The catch is that S corporation owners must pay themselves a reasonable salary for the work they perform. If you try to zero out salary and take everything as distributions, the IRS can reclassify payments and assess back payroll taxes and penalties. The “reasonable” standard looks at what you would pay someone else to do your job, not how little you want to pay yourself.

According to IRS Topic No 762, the Service focuses on officers of closely held corporations who take small salaries relative to profits. Documentation is your best defense. Keep copies of salary surveys, job descriptions, time logs, and board minutes approving compensation.

C corporations, double taxation, and when they still make sense

Despite the double taxation risk, C corporations are not the villain in every situation. The Tax Cuts and Jobs Act lowered the federal corporate rate to 21 percent, and that flat rate will matter if your personal bracket moves higher in coming years.

Here is how C corporations can be useful.

Reinvesting profits instead of paying them out

If your strategy is to pour profits back into the company instead of paying large dividends, the C corporation structure may work in your favor. For example, suppose your startup generates $500,000 in profit. As a C corporation, it pays $105,000 in federal corporate tax at 21 percent and reinvests the remaining $395,000 into equipment, staff, and marketing. No second layer of dividend tax hits until you actually distribute money to shareholders.

In contrast, an S corporation passes that $500,000 to shareholders now. High income shareholders in California could be facing combined federal and state tax rates north of 40 percent on that pass-through income in the same year, shrinking the capital available to grow the business.

Attracting outside investors and stock options

Institutional investors and venture capital funds generally prefer C corporations. Qualified small business stock under Internal Revenue Code Section 1202 can allow certain shareholders of C corporations to exclude up to 100 percent of gain on sale, subject to limits. That is simply not available with an S corporation.

C corporations also allow an unlimited number of shareholders and multiple classes of stock. S corporations are limited to 100 shareholders, cannot have nonresident alien shareholders, and generally may only issue one class of stock. Those restrictions can block fundraising rounds or complex equity compensation packages.

At a certain growth stage, many business owners work with advisors to map out when to stay S, when to switch to C, and how to manage the tax hit of any conversion.

California-specific considerations for C corporations

California taxes C corporations at 8.84 percent on net income. There is also a minimum franchise tax for corporations doing business in the state. According to Franchise Tax Board guidance on C corporations, even loss years can trigger this minimum.

When you compare what is the difference between s-corp and c-corp from a California standpoint, you are balancing that higher corporate rate on a C corporation against the 1.5 percent S corporation entity tax plus higher personal rates on pass-through income. The math depends on your income level, whether you plan to distribute profits, and how long you will operate in California.

Red flag alert: Common mistakes that trigger IRS and FTB scrutiny

Choosing between S and C status is not the real risk. Sloppy execution is. Here are pitfalls that often lead to IRS or California Franchise Tax Board notices.

S corporation owners skipping payroll entirely

Some owners elect S status, never set up payroll, and simply pull cash out of the company account when they need it. The IRS treats those draws as disguised wages. In an audit, they can reclassify years of distributions as wages and assess payroll taxes, penalties, and interest.

For 1099 professionals who are used to simply taking draws from an LLC, this is a major adjustment. If you are converting from sole proprietor or LLC to S corporation, this is exactly where strong bookkeeping and payroll support pays for itself.

C corporations paying personal expenses

On the C corporation side, a frequent mistake is running personal expenses through the corporate account and deducting them as business costs. The IRS can treat those as constructive dividends, which are not deductible by the corporation and are taxable to the shareholder.

According to IRS Publication 535, only ordinary and necessary business expenses are deductible. When in doubt, pay personal expenses from your own account and take money out of the corporation properly, either as salary, bonus, or documented dividends.

Missing S corporation election deadlines

To become an S corporation, you must file Form 2553 with the IRS. There are specific deadlines depending on when your tax year starts. Miss the date and you may be stuck as a C corporation for the entire year, paying corporate tax you did not budget for.

The IRS does offer late election relief in some cases, but it requires detailed statements and often professional support. Filing on time is far cheaper than fixing it later.

KDA case study: Consultant family cuts five figures in payroll tax

A two-owner consulting firm in Orange County came to KDA after three years as a multi-member LLC taxed as a partnership. The couple had built their revenue to about $420,000 of net profit split between them. Every year their CPA delivered a tax return with a self-employment tax bill north of $50,000, on top of income tax. They felt like the IRS was a silent partner.

We analyzed what is the difference between s-corp and c-corp in their situation and recommended a California corporation with an S election. We structured each spouse as a shareholder-employee. Based on industry salary data and their actual roles, we set salaries at $140,000 each, for a combined $280,000. The remaining $140,000 would be S corporation profit.

Here is what changed in the first full year after restructuring:

- Payroll tax applied to the $280,000 in W-2 wages.

- The $140,000 in profit distributions avoided self-employment tax.

- Even after the 1.5 percent California S corporation tax, the couple reduced payroll-related taxes by roughly $18,000 compared with their prior LLC structure.

- They also simplified retirement plan contributions by running them through payroll.

Their total advisory and implementation fee with KDA for the entity design, election, and first year support was just under $6,000. That means they earned a roughly 3 to 1 first year return in pure tax savings, not counting cleaner books and less anxiety at tax time.

Ready to see how we can help you? Explore more success stories on our case studies page to discover proven strategies that have saved our clients thousands in taxes.

How to decide between S corporation and C corporation for your situation

You do not pick an entity type in a vacuum. The right choice depends on your income level, growth plans, investor expectations, and how quickly you want to pull money out of the business for personal use.

Key questions to ask before electing S status

- Is your expected net profit (after expenses, before owner wages) at least $80,000 to $100,000 per year on a fairly stable basis?

- Are you comfortable running formal payroll, including separate filings and deadlines?

- Do you expect to keep ownership limited to individuals who are US persons, with no foreign shareholders, trusts, or funds as owners?

- Is your exit strategy more about cash flow and long-term ownership than a big sale to institutional investors?

If you answered yes to most of these, an S corporation is often the better tax tool. Our tax planning services frequently revolve around this decision point for high earning consultants, online business owners, and professional practices.

Signs a C corporation might be smarter

- You plan to raise capital from venture funds, private equity, or institutional investors.

- You expect to grant complex equity awards, multiple share classes, or convertible instruments.

- You plan to reinvest most of your profits for years, with limited dividends.

- Your personal tax bracket is significantly higher than the corporate rate and you are comfortable managing future dividend and capital gains tax planning.

In these cases, the double taxation cost can be a manageable price for the capital and flexibility you gain with a C corporation.

Fast tax facts: S versus C at a glance

- Tax level: S corporation income is taxed once at the shareholder level. C corporation income is taxed at the corporate level and potentially again when distributed as dividends.

- Owner payments: S corporation owners typically take a mix of salary and distributions. C corporation owners take salary, bonuses, and dividends.

- Eligibility: S corporations are limited to 100 shareholders, generally must be individuals or certain trusts, and must be US persons. C corporations have no such limits.

- California tax: S corporations pay 1.5 percent entity-level tax plus personal tax on shareholders. C corporations pay 8.84 percent on income plus personal tax on dividends.

- Best suited for: S corporations fit profitable, closely held service businesses. C corporations fit scalable, investment heavy businesses aiming at major exits or public markets.

Bottom line: The structure you choose shapes not just today’s tax bill but how flexible you are in three or five years. Changing later is possible but can create its own tax events, especially when going from C to S.

Will choosing the wrong structure trigger an audit?

Choosing S versus C status alone does not trigger an audit. What gets the IRS or Franchise Tax Board’s attention is inconsistent reporting, missing forms, or patterns that clearly try to dodge payroll or corporate tax.

Common audit triggers include:

- S corporation owners taking extremely low salaries compared with profit.

- C corporations claiming large deductions for vague management fees to related parties.

- Entities that change elections frequently without clear business reasons.

- Corporations that ignore information reporting, such as missing payroll tax forms or shareholder K-1s.

According to the IRS Data Book and guidance in corporate audit statistics, closely held corporations with flows between corporate and individual returns are a consistent exam focus.

Ready to Reduce Your Tax Bill?

KDA Inc. specializes in strategic tax planning for business owners, S Corps, LLCs, and high-net-worth individuals. Book a personalized consultation and walk away with a clear plan.

Frequently asked questions about S and C corporations

Can an LLC become an S corporation or C corporation?

Yes. An LLC can elect to be taxed as a corporation by filing Form 8832 and then, if desired, elect S status with Form 2553. You do not have to form a brand new corporation in every case. The steps need to be sequenced correctly, and the elections must be filed on time.

Can I switch from S corporation to C corporation or vice versa later?

You can, but there are tax traps. Converting from C to S can trigger built in gains tax if the corporation holds appreciated assets. Going from S back to C may limit when you can reelect S in the future. These changes require modeling and usually hands-on guidance from a strategist.

How does the qualified business income deduction fit in?

The qualified business income deduction under Internal Revenue Code Section 199A can allow eligible owners of pass-through entities such as S corporations to deduct up to 20 percent of qualified business income, subject to limits. See the IRS QBI deduction overview for details. C corporation owners do not get QBI on corporate income, although they may benefit from the lower corporate rate.

Do W-2 employees need to worry about S versus C?

If you only have W-2 income from an employer that is a corporation, you generally do not control the entity choice. Where this becomes relevant is when you start a side business or receive equity, bonuses, or profit interests through that employer. The moment you are considering your own entity is when this comparison becomes critical.

Is this guidance current for 2026?

This information is current as of 6/4/2026. Tax law can change through new legislation, IRS regulations, or court decisions. Always confirm key thresholds and rules directly with the IRS or your advisor if you are reading this at a later date.

Book your tax strategy session

If you are still unsure how what is the difference between s-corp and c-corp plays out for your specific numbers, that is normal. The right answer depends on profit, payroll, family situation, and California exposure. Our team builds side by side scenarios so you can see, in dollars, what each path costs over the next three to five years, not just this April.

If you want a clear, customized recommendation on entity choice, salary level, and distribution strategy, along with help implementing the filings and payroll so nothing falls through the cracks, our strategists are ready to help. Click here to book your consultation now.